Infact i would like to see them writing more of 40- 100 Cr loans, that will bring growth and improve ticket size to 100 Cr in future.

1 Cr loans to builders doesn’t sounds like wholesale lending business in Mumbai, where a decent single 1 BHK doesn’t cost this much.

Risk never happens due to client concentration ,always happens due to bad underwriting.

even Rs 100 Cr loan to a good project is a good loan and 100’s of 1 cr loan to 100 bad projects doesn’t guarantee any safety.

2 Likes

Did u find any real estate stocks gets a higher PE multiple, why?

Because industry itself is not steady. Every piece of land has its own pros and cons. And 100s of factors affects it’s valuations as well.

In such situations how u can affords to have above 1cr ticket size. Specially when u have 50cr AUM.

Ticket size of Arman finance is rs.38k even with 1000cr AUM and MAS has 65k ticket size with 6000cr AUM.

Fair points you quote, but a company with 50 Crs AUM and 40 Clients is not bad IMHO and the weightage on each account will change very fast depending on the additional disbursement/collection they do in these accounts along with the increase in total AUM which also can be fast.

To allocate 20 Cr to 1 client Rachna would have definitely assessed the risk/returns from this client, Afterall she’s running this business as promoter and you have to have some confidence in her ability and accordingly allocate in your PF, this is inherent with this size of a company.

Your non sizeable stake could still be my 20% in value terms and vice versa. The company is not even of 20 Crs so this is all relative, with the info at hand I have allocated 1% of PF to them and keeping a watch on their execution. Everyone risk appetite is different so should be your allocation which is of extreme importance in any pf.

there are some unemployed IITan’s as well in the world. Not everyone is paid millions who pass from IIT, but that is not to say he isn’t that capable. Maybe he has a view of the business which you and I may not have for 3-5-10 yrs down the line and he may be working towards that, Afterall this is kind of a startup and there are enough risk takers in the world.

Rating is not the only parameter which decides the coupon. Every company/Promoter has their links and connections which they use to get things done in their business. We being investors do not have an actual view of what’s going on the ground and things can be very different from what it seems from the filings and pictures and write ups, for a company of this scale. Of course, there is huge risk involved and so is the expected returns so as long as the corp governance is not an issue I would stay invested.

Arman should not be compared with Qgo as that’s a microfinance company primarily and their ticket size will be accordingly. Also, Avg ticket size does not mean they cannot have a client which is of a significant value expose of total AUM. So that avg number could be misleading.

2 Likes

Who is the IITan working there ?

Chief Financial Officer : Alok Pathak and Chairman: Rear Admiral Vineet Bakhshi

List of questions for QGO MANAGEMENT:-

- Who is buying their NCD.

- How they will get funds in future, as they mentioned they want It at less than 12%.

- Piramal also pays 11% then who will invest in their NCD , why they r not investing in shares.

- Who is actually working at ground level , means who had knowledge of land documents and all .

What are the parameters they looks when they lend 20cr to single party.

- They will arrange concalls in future or not?

- What are the parameters they monitor after lending , like when ticket size is big one has to watch UTILISATION OF FUND.

- If someone fails to pay For 1 or 2 qtrs,what r their plans.to over came situation.

8.Liquidation of property takes minimum 1.5yr time , if land owner not cooperates with qgo.

What’s ur mechanism ?

Disc . Invested want to sell my position but not getting enough buyers.

3 Likes

Good to see company is raising more funds -

Raising 5 Cr more - 10% of AUM

2 Likes

Some key numbers -

Their average lending rate is : 17%

NCDs are raised at : 12%

NII : 5%

Average loan size is Rs 5Cr

Average loan duration is 5 years

NCDs are raised 5-7 years of duration. (No ALM risk)

1 Like

Ohh my god…

That’s fantastic I mean only golden words are written by dhruva , Rachna made many false/funny statements.

That is completely removed  , I warn small investors to do ur own diligence. It’s biggest learning lesson for me also.

, I warn small investors to do ur own diligence. It’s biggest learning lesson for me also.

Some jokes cracked by promotors.

- In 5k sq.ft. office 3k is occupied by fitness equipments. Even when office space is rented.They answered it’s for fitness of our employees.

- She sells shares to creat market liquidity. Coming down to 64 from 91%.

- Company was run by 3 persons.4th person is Chairman who is living in Kota Rajasthan.

- They have their own construction company to complete NPA projects. I mean that’s fantastic.

- They said in case of NPA we sell projects at 50% below rate but how? Which agreement allows u to do so? They r not able to answer.

Disc. I am there at video conferenc. I own some shares . I own NBFC.

3 Likes

There is very low liquidity - Any one wants to sell in bulk at Rs 27 let me know - I’ll interested in buying in good quantity.

Promotors told me there is sufficient quantities available in the market, it means what ? They know who is selling.

At same time when I show interest in buying below 25 very same time buyers came and stock went 30.

They know who is interested in the company will definitely buy at 30 or 35.

The very same thing applicable to you why u r not buying at 30. If u really agrees with their model.

You can contact promoter they are really interested in selling further.

Kindly contact Aalok pathank CFO +91 98334 49911.

I REQUEST YOU TO SHARE DETAILS OF CONVERSATION YOU DO WITH MR.PATHAK.

Disc. I own some shares.

1 Like

Was this conference call informed about? Is there a recording for the same?

Last years AGM’s transcript:

1 Like

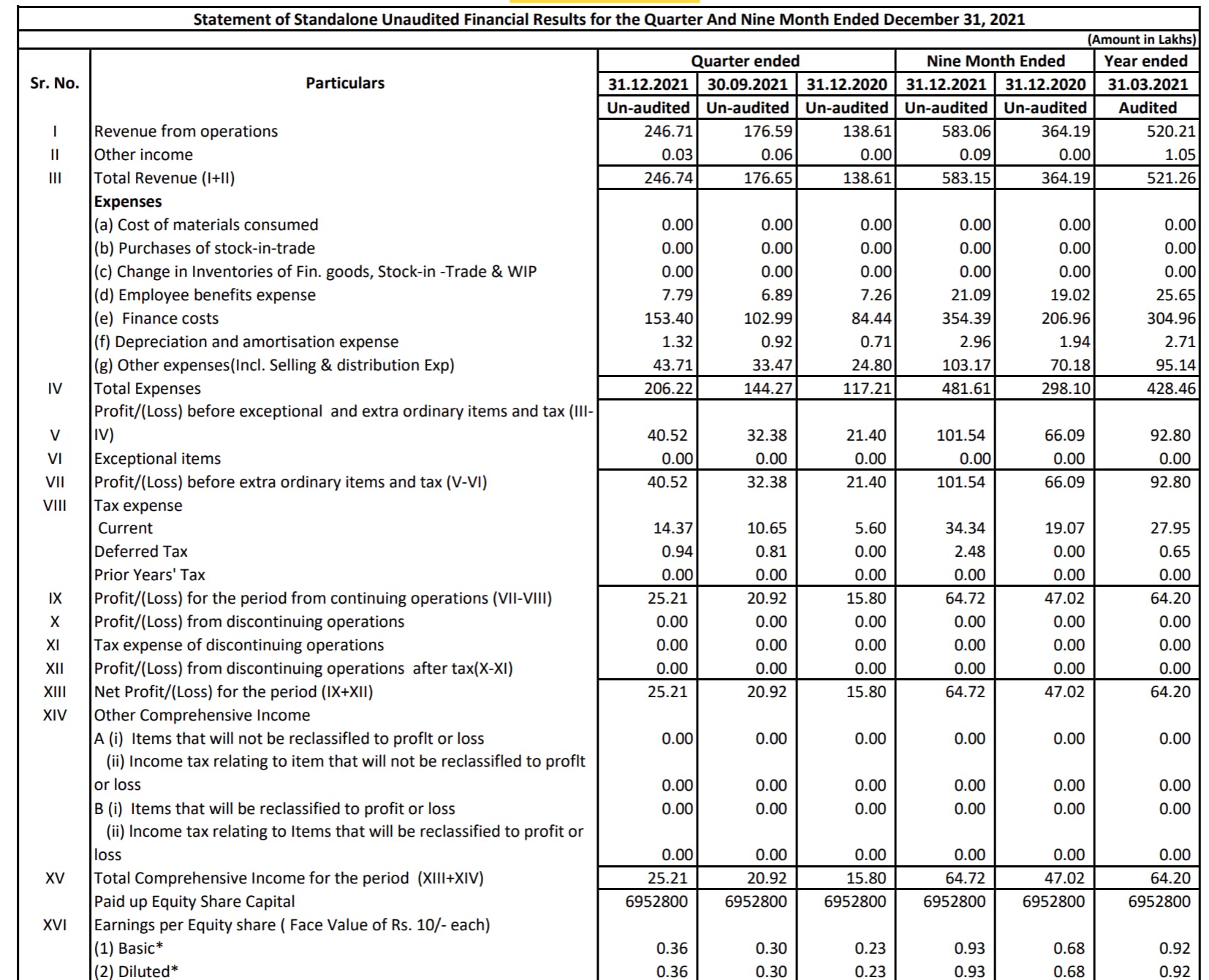

Decent set of numbers, The total book is 63 Crs against the total NCDs 53 Crs.

For how long will they be able to maintain the current growth rate without risking much, remains to be seen.

Disc:- Invested & Biased.

1 Like

They should be able to do Rs 1 cr net this financial year.

How fast they will become Rs 2 cr company will decide returns from here on.

The thing is low base in favourable but now they will have to raise equity to fund further growth.

Disc : want to buy below 25

1 Like

Companies largest client(Borrower) is Mazagon Dock Omkar. Borrowed about 15-18 crores.

1 Like