Why ?

Not much publicly available information about this company but what attracted me is their underwriting which dodged the covid- bullet.

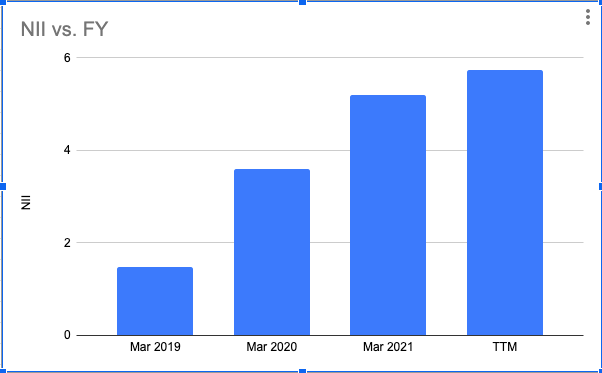

from FY 21 - Q4 Financials

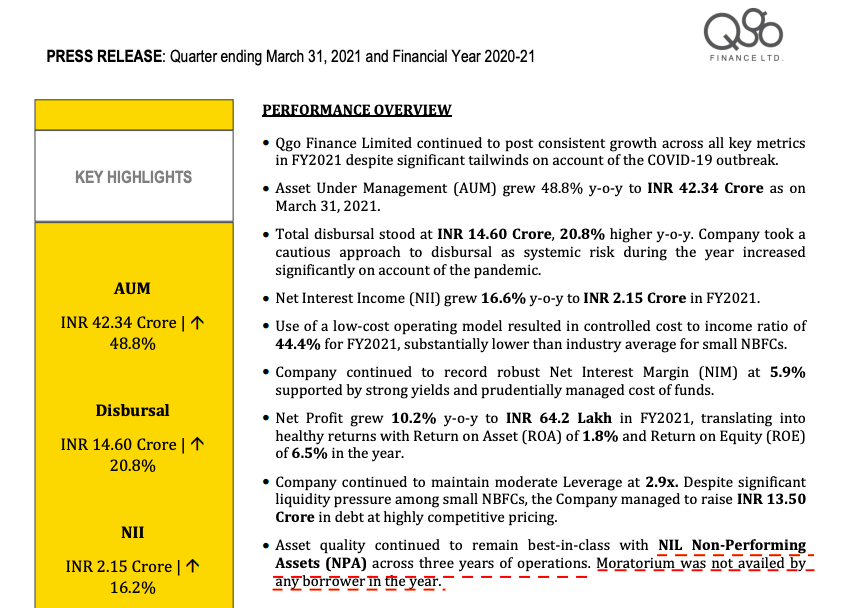

Company has been showing high & steady growth

QGO finance (formerly known as parnami credits ltd) was formed in 2018 after new promoter Rachana Singi acquired the company.

New promoter background - She is C.A and She used to run Rs 25 Cr textile company (Anika apparel ltd) before venturing into lending with QGO. (Anika apparels pvt ltd is a ready-made apparel manufacturing company basically dealing with exports of high fashion womens wear catering to the Europe market.)

Open offer for public shareholders were at Rs 11.59 per share .

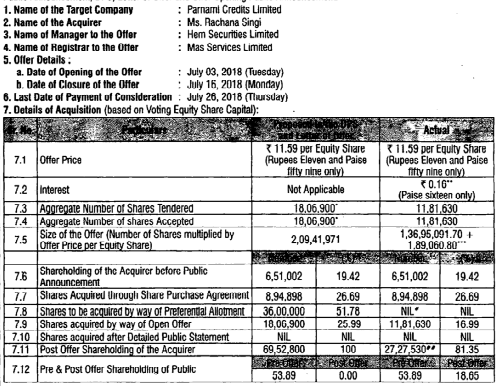

Prior to open offer she acquired 19% of the company via open market , for 12 months.

And rest she acquired from the promoters at Rs 9.3 per share

Overall Looks like She was able to buy 91% of the holding by paying some 3-3.5 Cr , then she raised the debt at 12% via NCDs ( today total of 29 Cr worth of NCDs hv been issued) & was able to build loan book of 42-50 Cr with Nil NPAs mostly focused on real estate financing.

Important thing to notice is they came into the market when there was serious funding crunch for the developers for IL&FS crisis ( DHFL was going bust, India bulls , PEL were de-leveraging etc) , which i supposed opened the gates for them to raise fresh capital lend at their own will without much competition.

Company has been growing steadily - (NII have grown by 3x)

Financials -

https://www.screener.in/company/538646/

What future holds ?

Company is not trading cheap at Mcap 20 Cr if one looks from PE = 30 , PB = 2x book but if we factor in the

same growth rate which 300% in last 3 years, So if they able to double revenue from 5.5 Cr to 10 cr in two years then at Rs 20 Cr mcap they might be trading cheap.

Near term growth visibility is there -

If you go through recent updates - Company has just approved to raised Rs 10 Cr via NCD in Aug ( Mcap 20 Cr) and again they are further planning to raise more growth capital.

If real estate sector going to see the tail wind then this company will sure find it easy to grow near term.

Negatives / Risks -

"If ROE remains low despite growth "

Today company ROE is 8.18 % , their COC is very high 12% and due to low revenue base just 5 cr and 1 Cr fixed cost not much is following into bottom line.

Company has to work on improving ROE, It may improve if COC comes down and revenue become >> fixed cost in future.

“Promoter selling” -

Promoter has bought down her stake from 91% to 65% in last 3 years. One reason could be as she take out just Rs 7.7 Lac as salary ( net profit = Rs 1 cr) most of the income made via selling shares at attractive gain from acquisition price.

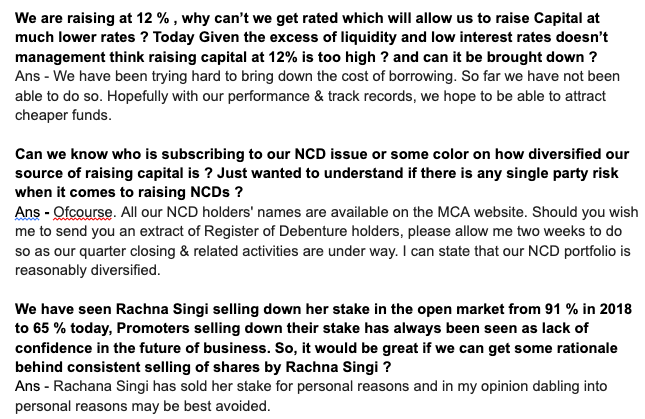

Some Email clarification i got from management -

AGM link for more insights -

https://youtu.be/APKwi-iuEGQ

Looking forward to more information sharing on this and learning new things from community members.

Disc - Invested in the company.