If u see Promoter is drawing 7.5 lac as salary ( looks decent for Rs 1 cr net profit company) and selling Rs 15-20 lac worth of shares from last two years.

Total earning they are taking out is Rs 21 lac which is okay but true she is making mistake selling shares at depressed price.

1 Like

She is C.A and She used to run Rs 25 Cr textile company(I think she knows how to run the company). If you know this company will worth more in the future, Why would you sell? There is not much information available about this company to be sure that the story is not other way around. ( something that we can not see taking place in the company). I would like to allocate a sizable percentage to my portfolio but need some fact that supports our confidence in this company. however, I haven’t come across a company of this size providing quarterly results on time and impressive annual reports.

1 Like

See more or less there is considerable demand in Real estate segment one thing, second no one is lending real estate companies easily. So thry can charge higher percentage interest. Of course they are financing against collectral only so risk was manageable.

Now if as they said suppose to issue 30cr worth of NCB .successful then there is no limit for this model.they will do same thing for 100cr next year or more.

Disc. Being owner of nbfc i dont find any fault in this model, if any black swan event not happenes in near futute they easily became 200 ,300 or more AUM company. Invested 10% of pf.

1 Like

Thanks Kuldeep. I was wondering if you have your own analysis of this company I would love to see it!

1 Like

Hi Kuldeep , One doubt i have - most listed nbfc’s are around 4x leveraged (Debt/ equity) , i think today QGO is also around 3-4x , how far they can raise debt relative to their equity ? shouldn’t we expect some equity dilution or they can just do 100 Cr of issue if they can raise ?

1 Like

There is no predefined guidelines for D/E ratio at some point in times its 15in case of BAJAJ FINANCE if markets allowed u to raise fund or u have meaningful usage of fund than u can go ahead.

I guess thats the biggest fency of NBFC companies specifically mannapuram growen its profit from 4cr in 2002 to 600cr in 2012. Thats because they have secured lending so they raise fund upto any extent.

What makes me discomfortable is promotors selling even this week, today if u place purchase order for 5000 shares within 10mins u gets shares.

Disc.invested

1 Like

How do you know this week ? last she sold in Aug

https://trendlyne.com/equity/insider-trading-sast/all/PARNAMI/4078/qgo-finance-ltd/

As i said delivery of 5000 shares comes within 10mins in such a illiquid stock. Where 6% of company hold by 350 small investors so its likely that this selling is from promotors only.

QGO finance considering to pay out dividends for the first time -

and issuance of NCDs (raising growth capital) continues.

I hope now promoter will stop selling ( as now will start receiving dividends )

2 Likes

She is completely on the right track…

I mean what she has created in 3yrs is a table which can easily manages 100 or 200cr . At the same time its becoming investors friendly.

So pe re rating will happens too early…

Disc .invested

1 Like

What PAG did with big builders, QGO did with small builders - "Coming in and filling the space which banks were leaving and where the rest of the lending community was cautious

3 Likes

It’s a win win situation I guess if they paid atleast 10% dividend .

That resolves many qurries like why promotors selling ??

And also it clears promotors intention for small share holders.

My personal sense is if they manage to creat second level management than there is no risk ,or you can say remaining everything is manageable.

As per my knowledge it’s a one women show!

Chairman is living in quota.

Results are out

50% rev growth half yearly and Quarterly (sep vs sep)

30% growth over previous Quarter.

Rs0.01 /- dividend.

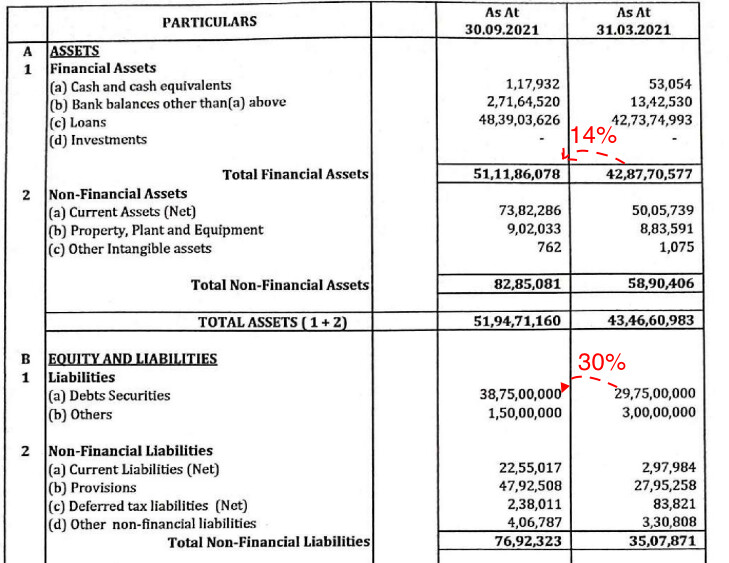

Total loan book is around Rs 48 Cr Vs Rs 42 (fy 21) - grown by 14% half-yearly.

Facevalue is 10 so if they declared 1% of dividend than amount will be 0.10 why they are saying 0.01

Is it 0.10% dividend?

Results are good , they are consistent and if 0.10 dividend is correct than they are suppose to spend 7lacs on dividend. Which is indeed good sign.

It’s fairly priced at current level.

Disc .invested

1 Like

I was expecting AUM to grow by 50% , based on the NCDs raised (Rs 20 cr) but AUM growth is just 14% may be bulk of lending might happen in the second half based on what they have raised so far.

they have fixed it -

https://www.bseindia.com/xml-data/corpfiling/AttachLive/ace7d353-eede-483a-b814-61f23106f348.pdf

Rs 0.1

AUM has grown by 14% and NCDs issue have grown by 30%, looks like there is some timing lag between they raise and they deploy.

looks like they will do > Rs 1 cr profits for the first time this financial year for sure ![]()

2 Likes

I don’t understand why QGO is paying dividend. company growing in double digits, reinvesting the profits will make more sense to me.

2 Likes

2 Likes

Very little is known about the future plans of the company. Can and will they scale up the business steadily? The company should share an investor presentation and conduct an investor concall.

I talked with CFO , and figure out some points.

- They have 40 clients to whom they have disbursed 50crs. So avg ticket size is 1.25cr.

Largest customer had 20cr loan. Which is enough for me to not have any sizable stake.

2)How some IITian with 10+ yrs experience works at 6lacs/yr. Along with his wife.

Salary to the employees and head office environment both creates some doubts.

3)Piramals gets funds thru NCD at 11% and qgo gets at 12% , even though it was not rated.

Arman gets funds at 12%.

4)Who is buying their NCD. Kind of flow will continue in future? - client concentration, & geographical concentration are two major concerns.

- I guess the office premises and even staff was on co working basis. There is some other working also going.

Disc. Invested . After knowing their exposure of 20cr to single client, trying to reduce my holding but no buyers

4 Likes