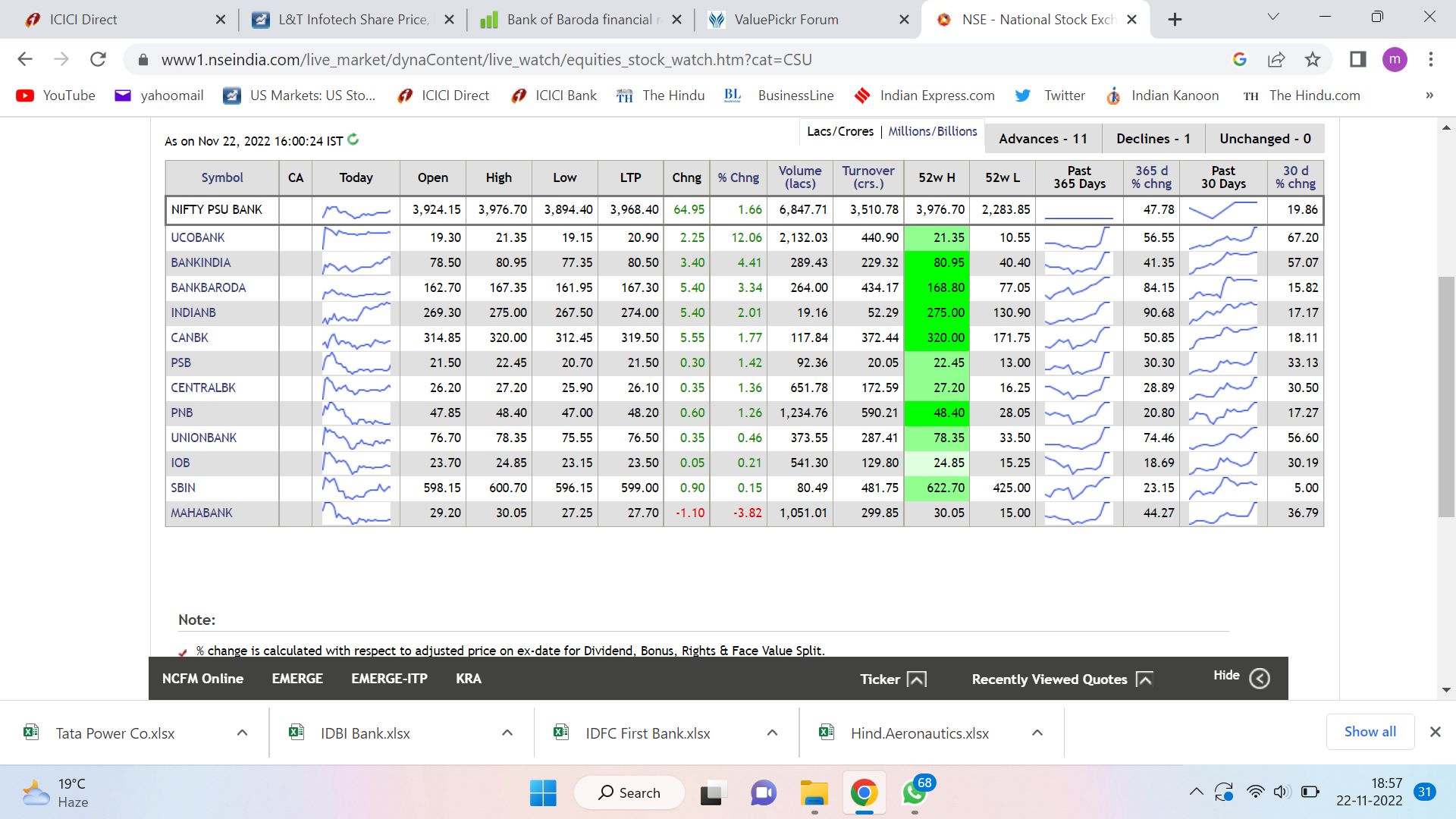

It is the daily news of rising PSU Banks which is giving me heartache. CNBC TV 18 said they have risen more than 40% this month.

There could be two approaches to this news. One way is to join the crowd. Many investors have, I am sure, made money in the rush. The other way is asking “Why they are sudden darlings of the investors?”

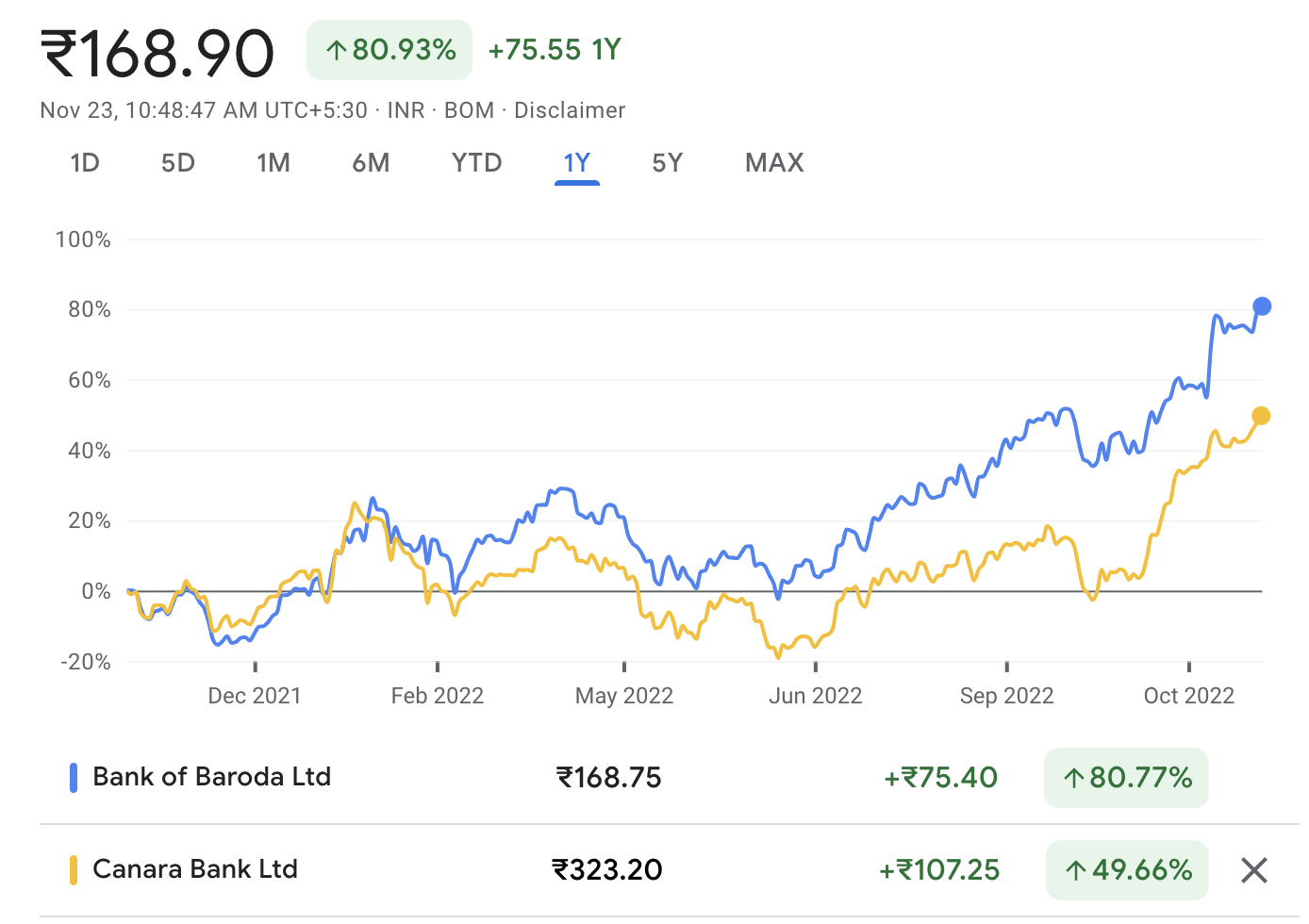

Every time I look at the financials of a PSU bank, I wonder what is in them. In many cases, their PE is more than the ROE/ROCE. Take BoB for example. The PE is 8.78, while the ROCE is 4.02%. Yet it is continuously rising. In June it was ₹96, today it is ₹166.75. Yes, its Net Profit has increased from ₹1942 cr in the June 22 ending quarter to ₹3392 cr in the Qtr ending Sept 22.

Canara Bank, another example. PE is 6.16, and the ROCE is 4.49%. To my uneducated eyes a company with that sort of ROCE would be a basket case! You don’t get even what you would get from its savings deposit. Yet, in September this year it was ₹210, today it is ₹318. In the June Qtr its Net Profit was ₹2193 cr. In the Sept '22, the Net Profit is ₹2730.

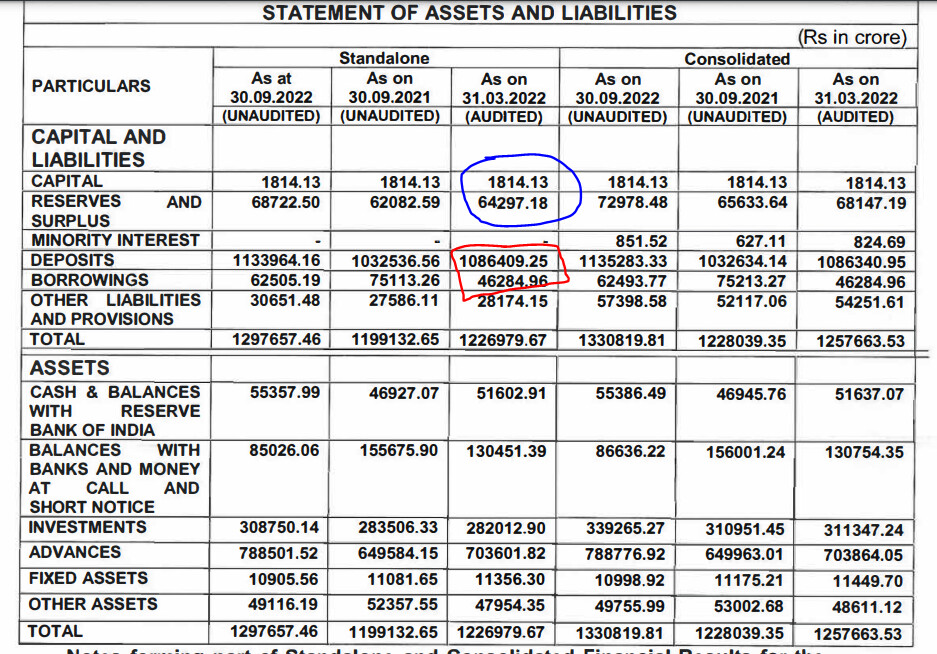

Of course the case of Book Value is different in many cases. The Book Value of Canara Bank is ₹ 386. This is higher than the price. For BoB the Book Value at ₹ 178 is again higher than the price.

But doesn’t the book value include a lot of inert assets? Or at least assets which have not been monetised. In the case of many PSUs, they have enormous land banks.

I wanted to make a point that in the case of the private banks it was different, but the statistics is again startling. The PE of ICICI Bank is 21.7. The ROCE is 5.59%. To a naked eye it seems to be doing worse than the PSU Banks. Its price by the way was ₹678 in June, and today it is ₹923.

Taking this yardstick, I should reject the ICICI Bank too.

My question then to the community is: if you do not want to blindly join the race, how do you assess stocks, specially bank stocks?