Did anyone attend the concall? Or can someone please share the concall transript/link to listen to

While I do believe that PSP construction quality is top-notch, i am in a bit doubt here. The sold propery by promoter has an area of around 760 sq yd while there is no mention of area of property sold to promotor but the neighbourhood is surely in a premium locality.

I am new to this site and investing. Can please someone tell me about following:

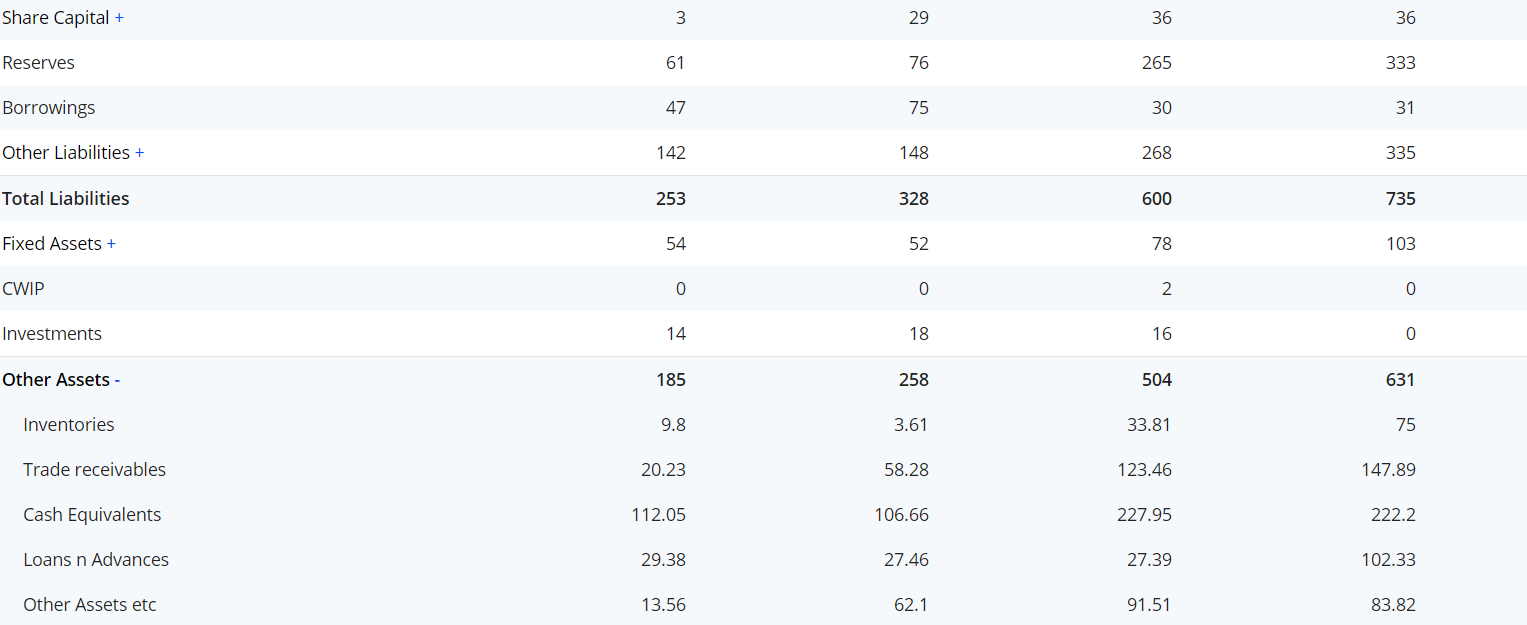

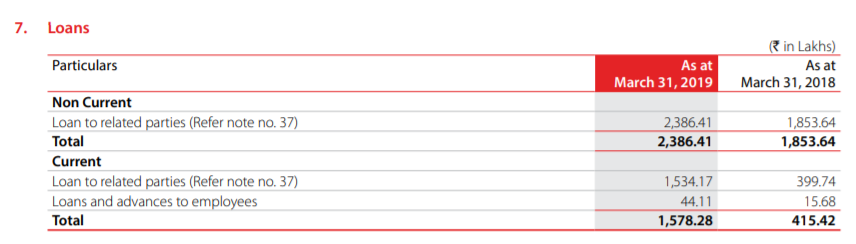

Though the promoter has salary, why is PSP paying him for services for around 50 L? (Related party transactions)

Higher and higher amount is paid to related party A P Constructions without more info.

Can someone pls tell me where to dig further for information about loan interest and the two points above?

Disc: Invested ~1% of portfolio

1 Like

Here you go:

New order win:

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=aed2008c-caee-40f9-ac24-a88f90ef1238

Key things to monitor remain the progress on SDB, WC normalisation which has spiked because of SDB, company’s ability to win and execute bigger ticket projects in parallel while competing with the likes of SP.

Company has recently got order from NESTLE Sanand which is big order. CAPEX of Nestle is 700Cr.

The Nestle order is 99.72 Crores and not 700Cr.

Source- https://www.bseindia.com/xml-data/corpfiling/AttachHis/f9a524ec-2ba9-4676-bd0c-ae06a98c1d7b.pdf

2 Likes

New order won in UP.

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=63a1c170-e7ae-4dc2-b158-76478361aa5c

The UP government has spent Rs 300 cr on acquiring buildings to be demolished as part of the project. The development and beautification project that PSP Projects has won is worth another Rs 339 cr.

PSP outbid Mumbai-based Shapoorji Pallonji Group to emerge as the lead candidate by submitting the Rs 339 cr bid. Shapoorji Pallonji Group had submitted a bid of Rs 422 cr.

The Kashi Vishvanath Dham project, locally known as the corridor project, involves creating a high-class tourism destination in the 400 meter stretch from the famous temple and the Ganga river. It also involves creating a temple courtyard as well as boundary walls for the Kashi Vishvanath temple with four gates in each direction. The total project is estimated to be cover 50,000 square meters (5.4 lakh square feet).

Source: https://ultra.news/t-t/49293/ahmedabad-based-psp-projects-to-create-kashi-vishvanath-corridor

3 Likes

Some thoughts on the company:

Runway for Growth:

Long runway for growth in terms of new projects from geographical expansion, order size increase, number of orders able to execute in parallel. The focus of the company is on Industrial and Institutional projects majorly driven by private capex, which should see revival going forward.

The execution of the Surat Diamond Bourse by Dec 2020, should expand the pre-qualification credentials of the company, allowing it to bid for larger and more complex projects. On that note, the company is looking to source additional funds in expectation of increased WC requirement from potential large orders to be bid going forward, as per the recent board resolution.

Margin Expansion:

In the AR, the company mentions that, “Currently, we are qualified to bid for projects amounting to approximately 5 Bn - 6 Bn. With the execution of SDB Project, this will increase to above 15 Bn. As we progressively bid for larger and complex projects, it will help us to strengthen our profitability.”

Competition:

As mentioned in recent concalls, as far as competition is concerned for projects more than 500 Crores there will be competition between large players like L&T, Shapoorji and JMC, but till the projects of up to 100 Crores, there is not much competition from organised players. If people are seeking organised company, there is less competition seen with maximum three or four bidders per bidding.

And from my limited research on the industry, there is a vacuum among the organised players in the space between 100-300 crores, as the larger players typically focus on bids more than 500 crores and when asked by clients to quote for projects lesser than 500 crores, they tend to quote higher to accommodate higher overheads. So, the orders between 100-500 crores is the sweet spot for the company in the medium term.

Management Bandwidth to Execute:

The future growth of the company has less to do with capital and machinery and rather more on the top and middle management bandwidth to execute multiple large projects in parallel. A LinkedIn search confirms a lot of Senior Engineers and Junior Engineers hired over the last year wrt previous years, as well as hiring of Management Trainees from premier institutes like NICMAR, which signals management intentions in this regard.

Further, the style of the company is to give it’s senior engineers a period of 4-5 years to get trained in the company and make them project heads, rather than hire laterally from larger construction companies. And further there is a rotation of the middle management across different projects to get them more exposed at the different sites and situations.

But further clarity on this aspect to understand how the company is approaching this aspect of its business is required as it forms a key part of the equation to understand whether this will be a 3x or 10x growth company.

Other details regarding the metrics including low debt, cash on books, better WC management, better operational ratios compared to the competition has been discussed previously in the thread.

@ankitgupta, I understand you were tracking JMC Projects earlier and had been in concalls with PSP Projects. If you have any notes on the company or how it fares with respect to JMC Projects or risk associated with PSP Projects, could you please share? Always had very high regard for your research notes and this thread could immensely benefit from it. Thanks.

9 Likes

Any specific reason why most of the mutual funds sold out their stake in the company as per latest annual report?

1 Like

PSPProjects_Transcript_Q2_FY20.pdf (1016.2 KB)

The management said in 2017 AR they were looking 2000cr revenue in 2021. So to achieve this they should grow at 100% growth rate… I think that is impossible

Management has been guiding for 30% growth in topline. So, they should be able to clock 1700 cr type of number for FY 21.

1 Like

Hi Ashwin,

I have been tracking PSP for quite some time now and have been impressed by their track record. The numbers speak for themselves. The company has been able to scale up in past few years while managing its working capital pretty well and generating healthy cash flows and RoCEs. On qualitative side, they have got many repeat orders from clients. In fact, people in the construction industry consider it among the best in building segment in Gujarat. I have had an opportunity to interact with the promoter, Mr. PS Patel in their last AGM. He came across as pretty level headed and focused person.

However, there are few concerns I thought I would highlight. First and foremost is the geographical concentration risk with company deriving more than 80% of its revenue from Gujarat. Reaching 1000 crore revenue from a single geography is one thing and growing from there is another. They will have to expand to other geographies if they have to grow from here. Other aspect is how they will manage working capital and cash flows when they expand to other states. It does become difficult if you have many sites under construction at many locations. Furthermore, currently, there is a big reliance on Surat Diamond project which till now has been largely in line with company’s expectation albeit with 3 - 6 month delay which is ok in such a large project. In addition, we will have to see delegation of responsibility in top management with the promoter himself engaged in most of the projects. With growing size and increasing number of projects, it will become difficult to do that and hopefully they would have build a good team to manage them. I will continue to track the company and monitor their execution.

21 Likes

Hi @ankitgupta Have you got the opportunity to ask what are the payment schedules for SDB. Are they getting payments on timely basis from SDB? As the overall diamond industry is facing slowdown there is a chance payments may get delayed.

The Surat diamond industry is likely to face a loss of around Rs 8,000 crore in next two months as Hong Kong, which is a major export destination, has declared a state of emergency due to the coronavirus outbreak in China.

Impact on PSP??

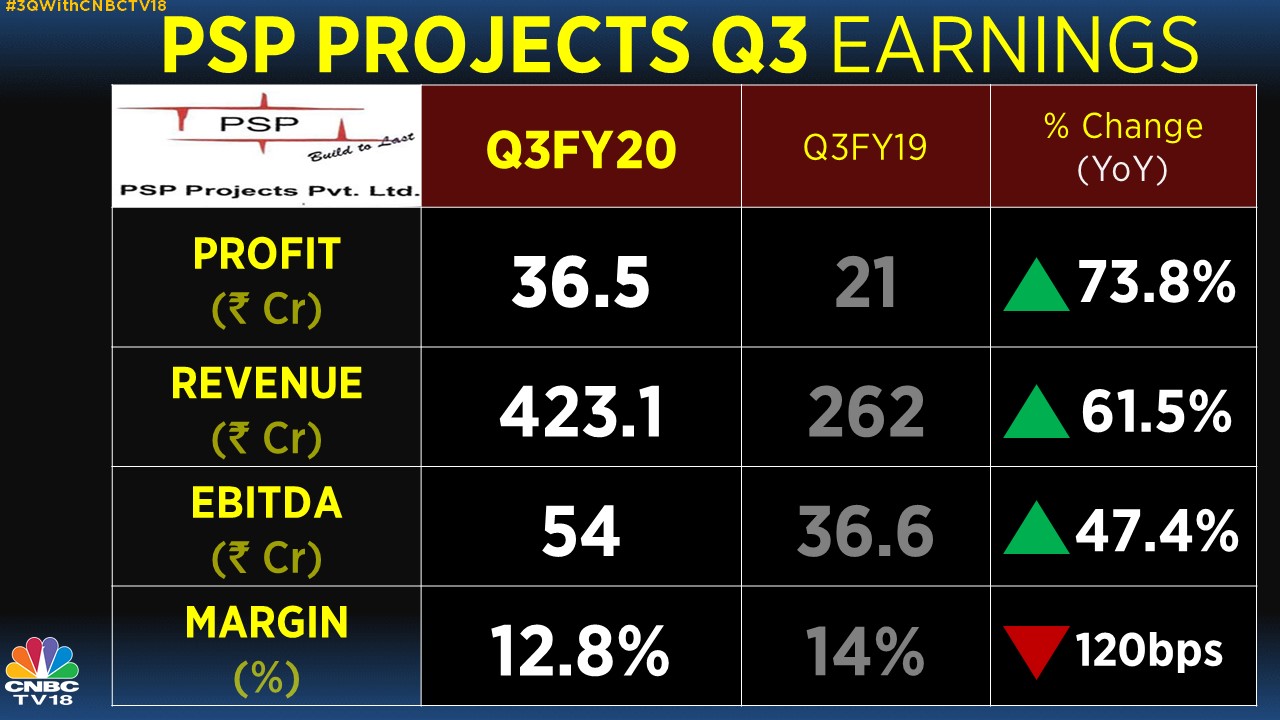

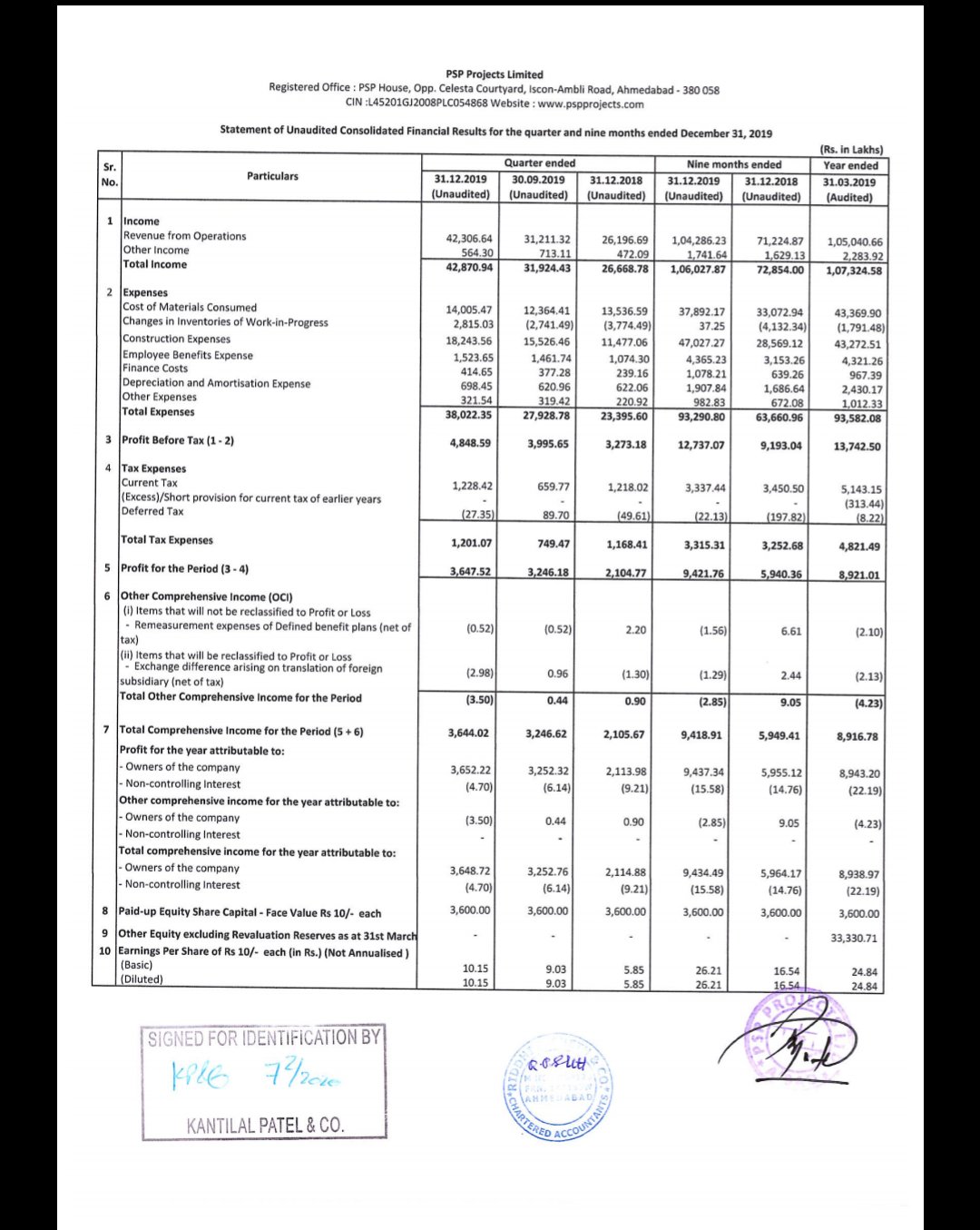

Good Result!

Q3 FY 20

YOY Revenue - 428.70 cr vs 266.68cr

Net Profit - 36.47cr vs 21.04cr

EPS - 10.15 vs 5.85

Profit would have jumped further but for ‘Changes in inventory of work-in-progress’.

5 Likes

Concall q3

Company bagged orders worth Rs.271 Crores in this quarter from government industrial, institutional and residential sectors.

out of the total four projects of our contract there are three projects either design build contract or composite package including annuity, so steadily we are seeing growth of lot of shift of projects in our order book from just civil contracts to contracts with all services and allied activities.

post Q3 we have been awarded a prestigious project of Shri Kashi Vishwanath Dham beautification amounts into Rs.339 Crores

total projects awarded in this year is Rs.1552 Crores till date, this does not include project worth Rs.307 Crores including GST there we are put lowest and which is not included in about 50-52. We have successfully completed 12 more projects this quarter, which is highest in a single quarter so far.

outstanding order book as on December 31, 2019 is Rs.3078 Crores including 43 projects under execution without Surat Diamond Bourse work on hand is Rs.2290 Crores.

have a bid pipeline worth Rs.1000 Crores from various industrial and institutional sectors.

company has executed 50% of the total contract value of Surat project.

Debtor days are 54 days, payment days are 51 days and inventory days are 25 days for the nine months period

our current borrowing short-term borrowing is Rs.70 Crores

the total FD outstanding in the books of company is Rs.229 Crores.

Question: if I exclude the SDB project that number has basically reminded fairly constant at around Rs.220-odd Crores so what I was wondering was that once this SDB in the next two quarters substantial execution will be done so are we in a position to ramp up the current orders so that our quarterly revenue run rate does not reduce that is question one and the second is on the fund raising plan that we had if you can just share any details if at all?

The projection for the new order book which we gave for this year was in the range of Rs.1500 Crores out of which we have already reached 1550 and if we consider the Rs.307 Crores L1 order, it will mean in the range of Rs.1700 to Rs 1800 Crores so there will not be any issue related to ramp up of the sales

Margin will be similar going forward

Question: what will be now after significantly completed on 50% SDB project so what will be our qualification like is have to bid for the government projects now so how much would be certified qualification as of now?

I think we have at the end of the project which will be in the range of minimum 3000 Crores projects and even may be in between there is a tender that we are completed more than 60% of work and I think it would be in the range of from bidding of Rs.2000 Crores.

revenue guidance for FY2020 and FY2021 may be in the same range of whatever we have been performing till today

15%, or more than 15% growth we can expect. (Last 3-5 years growth has been 30-40% range thus base effect is going to impact now.)

SDB will be completed by dec 2020 seems 4 month earlier than expected

would not be much cash required as far as working capital , but there will be requirement in terms of cash when we are bidding for large size projects, non fund based bank guarantees for large size projects , which we will be in the range of 25% in bank guarantee. ( interest cost will go up or will need qip )

Bid pipeline is about Rs.850 Crores to 1000 Crores.

expecting Rs.2000 Crores of ordering for next year.

newspaper reports are indicating some major losses for the diamond industry due to the China coronavirus, Till today there is no delay and we have also read that news, but I think that industry may have that impact from the size of the office that we have been telling you, that each office owner is investing too much per office, so I think it will not impact too much on the payment side from SDB.

US project will require 6-10cr additional funds

3000-4000 cr top line aim in 3-5 years

I believe in my middle management more and middle management work from the ground so we are trying to create more and more process within the company so that people does not have any problem in execution.

Question:Sir just one question on bid pipeline which was about Rs.3500 Crores at the end of FY2019 has come down to I think you mentioned in the call Rs.850 to Rs.1000 Crores so what has happened, why has our pipeline shrunk so much?

See when we are talking on that side, we have been also mentioning Essar Project and Jamnagar project, both of these two projects were totalling to more than Rs.1000 Crores and that we have now considered that they did not going to come again, so the outstanding of pipe bid line is around 1000 Crores.

Disclosure: was invested earlier now booked profits.

3 Likes

Hi Nityanand,

They have been receiving the payment form SDB on timely basis as indicated during AGM as well as concalls.

1 Like

This is surprising, as SDB has collected a majority of payments from its members (at least those who have paid on time).

Any idea how much PSP is charging SDB per sellable sq ft? SDB has already collected more than 6k per sq ft from its members. And more than that for those who have opted for parking.

1 Like