This looks like some sort of exchange of the property (Company getting PSP House in lieu of two land parcels to the promoter). I will urge you to get a clarification about this deal from the company.

2 Likes

Outlook Business Magazine dated December 22, 2017 contains coverage/recommendation of this stock by Bhavin Sha ( Founder Sameeksha Capital). Worth reading. This issue is a special edition and contains recommendation / Coverage of 16 stocks.

5 Likes

PSP Project - concall update

Discuss Highlights of Q3 and Nine month Performance

- Q3 Performance

o Company is now awarded with project of “ Surat Diamond Bourse “ which is a single project of 1575 Cr excluding GST .This project include 9 Buildings with Ground+15 floor covering 65 lakh SQ FT construction. This will be the single large complex in the world standing on basement area.

o Company has to complete this whole project in tight timeline of 30 month out of which 2 month has already gone started in mid of November.

o Also get 1 more order of 201 Cr. Total order at this quarter standing at 1776 Cr.

o Orders are received from diversified sector like Government, institution, private, Industrial.

o The other major project awarded include School of Art and Science for Ahmedabad university.

o There are 3 more projects which are expected to come.

EPC project for injectable unit of Punishka Healthcare is an industrial project

Construction of Corporate house for Punishka Healthcare is a commercial project

o Q3 - Revenue book 770.80 Cr

o Nine Month

• Revenue book 466.15 Cr which is after listing on Stock exchange.

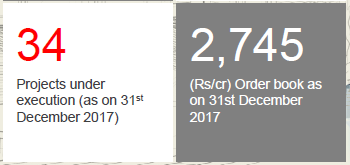

• Outstanding order book as on 31st Dec 2017 is 2745 Cr including 34 major project and spread in Gujarat, Maharashtra and Karnataka.

o Company completed 3 projects in this quarter which increase number of completed project to 97.

o Company also received scope by “Amul Dairy project” in Delhi of about 20 Cr before we complete the unit in Karnataka this show satisfaction of client.

o Company average project price has been shoot up to 116.93 Cr compare to 2.55 Cr in 2012-13

o Financials:

Standalone

• Revenue 178.80 Cr increase on YOY basis 127 % as compared to previous year Q3 revenue of 75.41 Cr.

• EBITDA for Q3 is Rs 26.63 Cr which has gone 180 % on YOY basis as compare to previous year Q3 of 79.43 Cr.

• EBITDA margin stand around 15.45 % which was 12.52 % in Q3 of previous year. Higher EBITDA margin is possible due to execution of various projects and some of the project supplied by client material also executed this quarter.

• PAT stand at 15.40 Cr which has increased on YOY basis by 106 % which was Rs 7.34 Cr in Q3 of previous year.

• Company achieved PAT margin of 8.73% as compared to 9.13% in previous year Q3

o QOQ

Revenue was 139.55 Cr for Q2 FY18 which has increase to Rs 170.80 Cr in Q3.

PAT increased by 19 % compared to Q2 FY 18. While PAT margin has marginally reduce from 8.75 to 8.70 %.

o Total Work on hand is 2745 Cr as on 31st Dec which comprises of

85 % from institutional project

8 % from industrial project

4 % from government project

2 % from residential

1 % from government residential.

This is to be executed over next 30 month period.

o The outstanding order book of Rs 2745 Cr is distributed over 3 regions :-

91% from Gujarat

5 % executed in Karnataka

4 % of work on hand will be executed in Rajasthan.

o Utilisation Of IPO Money which was 167 Cr raised by company

63 Cr being plan to be utilised in goods and capital which is fully utilised by end of Q3

52 Cr kept for CAPEX out of which 17 Cr is utilised for purchase of machinery and shipping material.

26 Cr allocated for General Purposes out of which 17 Cr is utilised till the end of Q3

Q&A - How much revenue did company book from Surat project till now?

o Company has not booked any revenue till date because it is no stage of execration so in January company will complete the basement and start PCC and water proof treatment So some revenues has to come in January and February. - How much revenue company expecting from Surat project in Q4?

o Probably 30-40 Cr from the project of Surat. - On margin front our supply cost and employee cost has come down so what can we expect in next year when surat project will start kicking in full swing ?

o Margin will depend on tenders so company expect same margins which is coming from past 3 quarters. It will be in 12-15 % range. - Is working capital stable including payable and receivable?

o Yes - Any new big order in pipeline?

o All pipeline projects have been disclosed and company will get 200-300 Cr range project in every quarter. - Any key project company is focussed on?

o Key project include power project of torrent pharma and torrent power project and Company is already prequalifying stage in college project for IIT Ahmedabad . - What are the criteria for recognising revenue on projects?

o It is based on quantity wise not phase wise. Every month company will put bill on quantity and get the payment. Real execration was started in December in surat project and in December we can’t do the expected quantity so company didn’t placed the bill. Also there is a criteria of placing minimum bill of 20 Crore rupees. So now it will be easy to bill and recognise revenue because multiple activities are running on the project. - In the first phase Debtors were too high and management told that it is because of GST issue has that number normalised?

o It will normalised in the second half of the year. There was a confusion of finalising GST rates at that time in which company now getting bill cleared at every month and everything is now cleared. So trade receivable number will come down from next quarter. - In current order book what will be the portion of order with material?

o About 14-15 crore project are without material rest all are with material. So it is very minimal. - How big ability can be there to participate in bid?

o For government and institution projects company’s ability is 500-600 Cr. In private or corporate type of projects, we recently qualified for 1675 Cr Diamond Bourse project. So it depends on what type of project it is. - Can company increase internal capability like 2000-3000 Cr revenue a year and what kind of resource will be mobilised?

o Company has started with 28 Cr in 2006 and come to 600 Cr in 2018. Gradually company is expanding to 30-40 % and will maintain it by increasing man power. For a construction company to expand is more on execution. It is more important about the top management resources rather than capital and machinery. - What amount of working capital requirement company see in a year?

o Mostly company is working with corporates groups and private sector there is clause of mobilisation of advance of 10 % so that itself is more than sufficient for working capital. Rest require is Bank guarantee which company has already reach to 410 Cr banking facilities. - How company see competitive intensity?

o The type of projects, type of name company get in market like Ahmedabad and Gujarat company is known for quality. There is a big vacuum in project from 25 Cr to 100 Cr. L&T and Shaporji both company bid for 100-200 Cr projects so they cant focus on small size projects. So as far as delivery time and quality is concerned there is no big competition for smaller size projects. - How many active sites company have and how it is compare to year ago?

o Presently active sites is 34 and now when company is getting large size projects so company is trying to reduce project of 25 Cr in Ahmedabad , out of Ahmedabad company has limited it to 50 Cr, out of Gujarat company has limited to 100 Cr… Probably in future it will be in a range of 20-25. - How difficult it is to find high skilled manpower in Ahmedabad that would be used to working on these kinds of projects?

o It is all about training your own people and getting them experience of about 4-5 years within the company and putting them on larger size projects has given good example all the time working well. It is about company culture and company system. Company believe to train own people rather than getting people from market. - Is company avoiding private residential project?

o Company believes that if private residential project is above 100 Crore then it is worth to work for it less than that for example 25 Cr private residential projects then it is better to work in other construction because company will complete it and get easily free from it. - Why company is not expanding geographically in real estate sector?

o The real estate market runs on selling and openly driven by sell market so it is little risky. As you don’t know the client and developer it will be risky then if they are capable to pay on time or not. Projects in which finance is depend on sell company believe that they should be selective on ground. - So company will be on net cash basis?

o Yes, company will be on net cash basis only , even if diamond bourse is concern. - What difference come after get listed on stock exchange ?

o Before listed on exchange company has to pay 40 % margin to bank out of which 30 % is mortgage and 10 % is margin. After listed on stock exchange it has come down to 25 % margin. Even company is getting competitive cost of funding. - Does company say no to new projects as it grown 3-4 times after getting listed ?

o No company don’t say no instead of that company has divided it to sizeable projects. A project is more than 100-150 Cr of worth company bid for it competitively. It is not like that once we get diamond bourse project company stop bidding. Company always keep on expanding as it was in last 10 years in Ahmedabad also . - Kindly provide breakup of institutions ?

o Company is working with pharma companies , Industrial , BSE is also there in institutions. - How company see the competition among private players and residential projects?

o Presently company is based from Ahmedabad so focus is on nearby city. Now company is working for diamond bourse in Surat then after 4-6 month company will get good opportunity from Surat also. - Is it will true to say that alone 600 Cr revenue will come from Surat diamond bourse project only?

o It depend on work out of 1575 Cr only 600 Cr is structure part rest include phased that is lift and MAP So this portion of 775 Cr can only be done after 18 month once structure is completed. 450 Cr revenue can come then rest will come further. - Do company see any receivables problem from Diamond bourse project ?

o No they want to make it the largest Diamond Bourse and this project is full with money right now. Out of 100 % land still 10 % is left for some selected people to come later. So company don’t see any problem in it. - In next year how much top-line company is expecting?

o In FY 19 the projection is in the range of somewhere 900-1000 Cr revenue.

14 Likes

Company is executing the plans fairly well. Looks good at 28x trailing (cmp 485) with projects lined up for next 30-36 months. They are saying that company will remain net cash positive despite executing large surat project. I am sure working capital needs will rise gradually. Despite 10% advance and reduction in margin money from banks, they need to put receivables under check. If they manage well, this will be a long term growth story. If they flutter on receivables and working capital, they will be like numerous other small sized builders.

It is good that they are focussed on a few cities. Saves on expenses and working capital. Spreading too much without much mgmt bandwidth can be messy. They were focussed in Ahmedabad… now doing that in Surat.

Disclaimer: Invested from 260. Traded positionally many times.

2 Likes

Thanks mate for the summary.

Did they mention how much is the actual difference in numbers?

Did they mention when the rest of the IPO money will be utilized? Will they do more capex for Surat project?

As a fallout of the PNB scam, funding for construction of the Surat Diamond Bourse might be delayed. This will have an impact on PSP revenue visibility in the near term.

5 Likes

Sir, any basis for apprehension in funding, when company says project is sold with and 90% land sold, 10% reserved. Regards

1 Like

Tarun Advani: Understood, Sir do you see any challenge for example if we keep on billing say Rs.40 Crores,Rs.50 Crores every month, what is your view on how the receivable would shape out, do you PSP Projects February 08, 2018 think that the client would have enough money to timely pay us and our working capital wound

not get stuck?

Reply:

The basic idea of this old Diamond Bourse if you have gone through the history of this Diamond

Bourse, they are going to create this as the one of the largest infrastructure Diamond Bourse

industries coming up and you will not believe about this total area of 66 lakh square feet, they

have sold 90% of the sales, 10% they have kept reserved for some selective persons to come

later, so presently if you see that the project is fully with money, so this is all depends on how

fast I did go and how fast they get the payment from the tenant so I do not see any problem in

terms of receivables as far as SDB Association is concerned.

When a project is sold, it means tenants have committed to purchase an office and paid booking amount with an agreement to pay the rest based on certain construction milestones. Tenants enter into these type commitments based on projecting their own business growth and cashflows. This is similar to someone buying an under construction house.

Some of these tenants may get into trouble if working capital funding to diamond industry is reduced by banks as a result of PNB scam. Some tenants might have to pay higher interest rates to fund their working capital which will affect their profitability. Since industry is so heavily dependent on working capital, any disruption there can have ripple effects and buying a new office would be the last priority of such businesses.

This is a large contract for PSP and any change in delivery schedule will impact PSP results. company has hired several employees, made investments in machinery and already spent few months of efforts on this project. As per Mr. Patel, initial construction activity generally does not result in much billing so that will have an impact even though it will be limited. Any delay in billing will impact bottom line since company is already incurring expenses for this project.

I had written to company last week about construction update and this is what I received.

Dear Sir, With reference to your query, it is hereby informed you that Construction activities are going on at the site of Surat Diamond Bourse. Further, with regards to PNB scam on funding of Surat Diamond Bourse Project, We can say that we do [NOT] have any indication from our client which shows such impact on execution of the projects at present. The construction activities have not been delayed or hampered due to this element. It is also hereby informed you that payment are being released timely till now. I trust I have explained the matter to your satisfaction. Regards, Minakshi Tak Company Secretary & Compliance Officer cid:image001.png@01D24D62.7DC60970 PSP Projects Ltd. ‘PSP House’, Opp. Celesta Courtyard, Opp. Lane of Vikramnagar Colony, Iscon-Ambli Road, Ahmedabad – 380058 Office: 079-26936200/6300/6400 Email – minakshi@pspprojects.com URL – www.pspprojects.com

However, it will be too early to see any impact and the potential impact (if any) will play out over next one year.

10 Likes

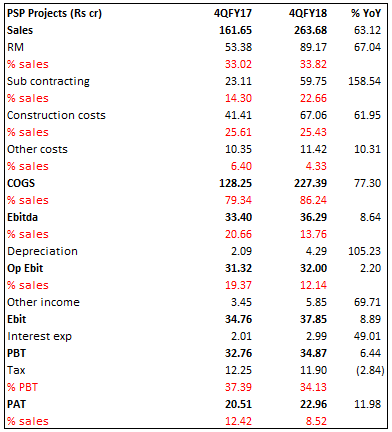

Has anyone seen the PSP results? I managed to grab a few minutes to make a table. comments appreciated.

PSP results. I think the results are quite good. The rise in profits is only 12% vs sales rise of 60% due to increase in subcontracting costs. I think the sub contracting costs may have gone up due to the breaking ground on the Surat project and will come down over the next 2-3 quarters. What I like is that the construction costs have been well contained. I think the worst of the expensing is done with and next quarter on he will make money. Notably, if I keep subcontracting costs to past years level as % of sales, the PAT would have gone up by 110%.

Interestingly, the consol FY18 Sales and PAT came in at Rs770 crore and Rs66 crore respectively. This is sharply ahead of the estimates made in a recent (30th April) Edelweiss Report on the company of Rs667 crores and Rs57 crores.

Writing in a hurry to excuse any typos, please do let me know what you think of the results.

Disc: Owned.

2 Likes

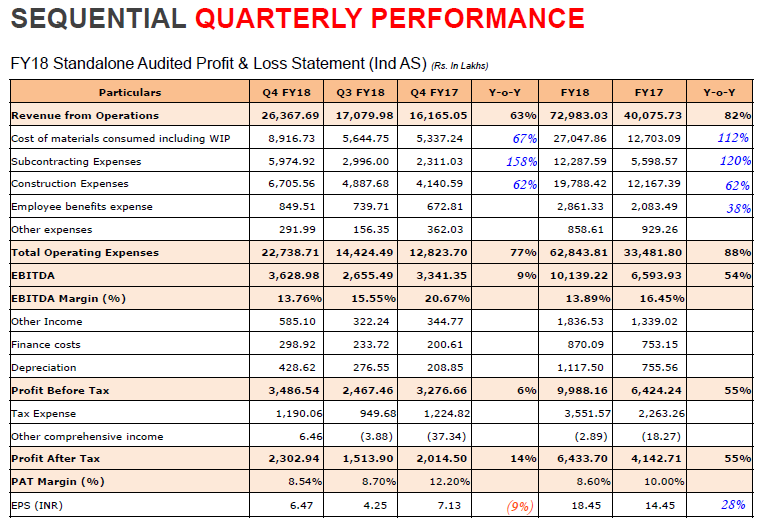

Overall good results from PSP Projects.

Source: Company Presentation

Strong revenue growth for Q4 as well as FY 18. This is due to SDB project getting accounted for in Q4. As previously mentioned by the company, expenses are higher at the start of the project and margins are lower so that is visible in the Q4 results.

FY 18 results show a strong revenue growth, good EBITDA and PAT margins. FY 19 should see a strong revenue growth and some uptick in margins are costs are front loaded.

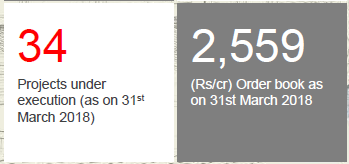

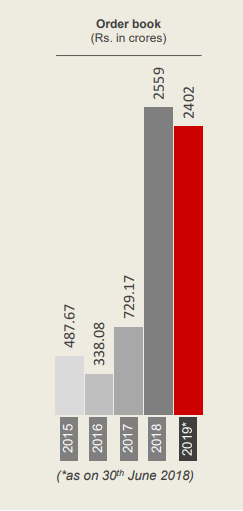

Order Book.

Company has a strong order book of 2,559 Cr which is 3.5 times FY 18 sales. Order book has dipped by about 186 cr from Q3 to Q4 and number of projects under execution is same at 34. Since SDB is a large project, company is not adding any more projects at the moment.

Source: Company Presentation Q2

Source: Company Presentation Q3

Source: Company Presentation Q4

Disc: Invested.

8 Likes

Was going through the Concall Script. I am not able to understand which figure Mr. P S Patel is referring for Rs. 150Cr. Can anybody help on the same.

"Abhijeet Vara: Sure Sir. Just one last question Sir, in terms of working capital limits, banking limits, do you have sufficient to sustain this year’s growth, go for enhancement of limit?

P.S. Patel: After coming to IPO we have increased that limit to 425 Crores

, which is the earlier bank guarantee and out of which maximum was to be utilized for the diamond bourse project for advance of 78 Crores and performance guarantee, we have more than 300 Crores?

Hetal Patel:

No it is 150 Crores we have balance fund.

P.S. Patel: So 150 Crores that is still we are having, so once we complete

the project all the projects needs to be completing, you are getting the performance guarantee and for those projects mobilization advance

is also recovered, so that bank guarantee is also coming. So probably I think we brought at least up to 1000, 1000 plus Crores, I do not need any further enhancement of the BG facility of the company.

"

1 Like

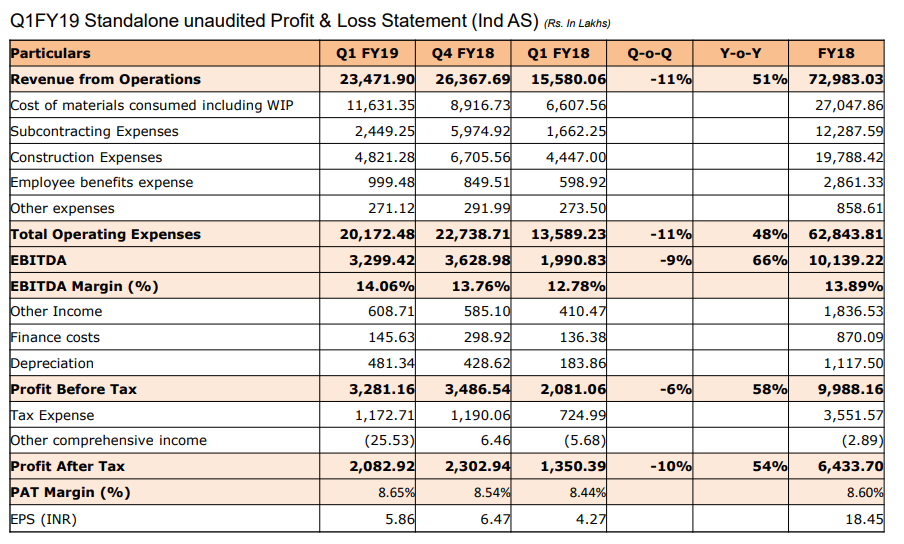

I think another good set of numbers by PSP Projects, with sales rising 51%, Ebitda by 66% and PAT by 54%. (all YoY)

The slight disconnect between Ebitda growth and PAT growth appears to be due to the 162% YoY rise in depreciation expense.

Notably, PSP has incurred Rs21crore capex in the first quarter (used entirely for the Surat Diamond Bourse project), which accounts for ~26% of the FY18 net block. The FY19E full year capex is expected to be about Rs50 crores (~63% of opening net block) suggesting that the company is rapidly scaling up.

While Ebitda margin has shown a sharp improvement from 12.78% last year to 14.06% in 1QFY19, the Management clarified that the steady state margin will remain in the 12-13% levels (also the guidance for full year FY19). Margin will vary based on the stage of construction that dominates in a particular period. In 1QFY19, RCC work dominated hence margins were higher, during the finishing stage the margins can drop to 12-12.5%.

Notably, the company has bid for a Rs450 crore RCC only contract in a south Indian state (60% of FY18 revenues, 17% of order book). The outcome of same is pending, though the PSP management has indicated that bids have been opened and the client has already held the first round of negotiations with PSP.

The order book was healthy at Rs2,576 crores as on the date of the con-call vs. …

The company is targeting an annual order inflow of Rs1000 crore (tenders worth 1200-1400 crore already submitted.

Balance sheet remains healthy with the debt levels estimated at maximum to be at Rs40crore (vs. overall credit limit of Rs410 crore). Free cash on hand is Rs50 crore. Inventory days are at 20-25, debtor at 45 days and creditors at 50-60 days.

Surat Diamond Bourse project is going as planned, to put in the management’s words:

“As an update I would like to brief you about Surat Diamond Bourse work progress also, so work progress at Surat Diamond Bourse is going on well and we have booked revenue of about Rs.83 Crores in the Q1 and thought there was heavy monsoon in the first half of monsoon season, there was a big disturbance during for six to seven days at the site but presently, we are going with full fledge and about 3500 people are working and out of nine blocks, five blocks have reached second basement and four is in the first basement level. There was a heavy inclusion of plant and machinery approximate Rs.21 Crores invested in these quarters and that is for the Surat Diamond Bourse project only”

Disc:invested

4 Likes

Notes from Annual Report 2018

Promoters -

- Prahaladbhai Shivrambhai Patel (PSP) - MD + CEO (55 yrs)

- Has been in construction business for last 30 years

- Moved proprietorship business in civil construction to PSP projects in 2009

- Shilpaben Patel - wife of MD (51 yrs) - Whole-time Director - mostly looks after CSR

- Pooja Patel (25 yrs) - ED - daughter of PSP and involved in execution of Surat Diamond Bourse project

- Sagar Patel - son of PSP - not on board and mostly not involved with operations of company

Shareholding (as of June 30, 2018)

- Promoter holding at 72.44%

- PSP increased shareholding by 0.14 % in Q4FY18 and by 0.31% in Q1FY19

- Mutual funds - 7.61%

- Corporate bodies - 6.57 - not sure which ones

- FPI - 1.21%

Board -

- 3 promoter directors, 3 independent directors

- Besides the family, none of the directors have experience in construction industry as such

- Total board remuneration (including promoters) ~ 9% PAT

Key Management Team -

- PSP - MD + CEO

- Pooja Patel - ED

- Hetal Patel - CFO

- Mahesh Patel - VP Operations - been with company since inception, 25 yrs of experience in construction industry

- Maulik Patel - Director Procurement - with company since inception

- RB Parmar - GM, Tender - 30 yrs of experience in contracts + tendering

- Pratik Thakkar - GM, Business Development - 10 yrs experience

- Mittali Christachary - CS - replaced Minakshi Tak in Apr 2018

- Statutory auditors - Prakash Sheth & Co to be replaced by Kantilal Patel & Co

Business

- Construction of all kinds of building projects - industrial, institutional, residential, govt. residential, government

- Consolidated order book ~ 2644 crores - ex-Surat Diamond Bourse ~ 1128 crores

- Has done projects for marquee clients including Torrent Pharma, Cadila, Gujarat state govt, Hiranandani, Godrej, etc.

- Ongoing projects include clients like Prestige, Brigade, GIFT city buildings for BSE, etc

- Structure of subsidiaries

- PSP Project Inc (100%)

- JV P&J Builders LLC (50%)

- PSP Projects & Proactive Constructions Private Ltd (74%) - for GIFT city

- GDCL & PSP JV (49%)

- PSP Project Inc (100%)

- Listed the company’s shares in May 2017

-

Current order book - 5700 crores,

- Management expects a 25% hit rate ~ 1425 crores could be won

- Expects 2000 cr top line by FY21 ~ 40% 3-yr sales CAGR

- Credit rating raised to A+

- Enters contractual agreements that allow it to pass material cost increases to customers

- Sector wise break-up

* Govt - 27%

* Govt residential - 1%

* Industrial - 21%

* Institutional - 44%

* Residential - 7% - Geographical break-up

* Gujarat - 84%

* Rajasthan - 4%

* Karnataka - 9%

* Delhi - 3%

Financial highlights for FY18

* Aggregate sales increased by 69% to 752 cr, 59% increase in net profit

* EBITDA margin ~ 14%

* RoCE ~ 28%

* Debt to equity ~ 0.1

* Interest cover increased from 9.42 to 14.42

From Chariman’s message -

- Key message - we build to last and we build it fast

- Five points

- Driven to become a differentiated construction company - to build what most people would consider difficult and set sectoral benchmarks

-

Revenues must come from longstanding customer base - once a customer always a customer

- Proportion of revenue in 2017-18 from existing customers was 40%

- Technology driven - use of CANDY software

- Focus on processes rather than decision making by handful of people

- Focus on welfare of construction workers - to seek their commitment to the company

-

Have transformed pre-qualification credentials with award of Surat Diamond Bourse - which is 6x largest previous project

- Visibility for next 30 months + stable margins

- First mover advantage in GIFT city - where they accounted for 6 out of 8 projects

On operational performance in FY18 -

- Surat Diamond Bourse construction is on track, collected 59 cr in last quarter

- Contract was won in Oct 2017

- Plan to finish project by Feb 2020 (period of 24 months) as against government approval of 30 months

- Local site office that works as a strategic business unit for decentralised decision making

- Revenues have also increased because moved from core construction activity to turnkey project manager including billing of materials

- GST likely to be beneficial to organised players such as PSP

- Optimistic in FY19 due to ability to aggregate stable on-site workforce through contractors in multi state recruitment and multi-month deployment across sites

* Considers the ability to retain workers due to worker welfare as one of its biggest competitive advantages -

Expects total revenue of 1450 crores this year

- SDB to contribute ~ 450 crores

- Other projects expected to contribute ~ 1000 crores

Some marketing material and justifications

- Moved from small sized projects to large ticket constructions

- Average size of project went from 8.54 cr to 110.51 cr

- From hands on promoter to SAP driven empowerment

- From construction revenues to construction cum treasury revenues

- Total treasury funds of 249 crores out of which 172 crs is pledged against bank guarantees, overdraft facilities - nearly 77 crores were available for deployment in liquid instruments

- From fiscal fire-fighting to fiscal discipline

- Excellent interest cover, low debt to equity ~ 0.1x, cash on books of 222 crores

- From large number of vendors to rationalised vendor list

- Moving from pan Gujarat to pan Indian presence - currently 84% revenue still comes from Gujarat

- Plan to bid for projects > 50 cr in Gujarat and > 100 cr in other states

- Plan to bring non-Gujarat revenue to 30%

- Culture of calculated risk taking

- Idea to get seven things right out of ten

- CMD visits every site once a fortnight

- Construction worker welfare

- Electronic payment of weekly wages + rest at end of month

- Free accommodation in housing colony made with pre-fabricated material

- Creche in are where workers stay

- Lighting and water facilities in worker areas

- A number of projects demonstrated where PSP has completed well before time limit

- A number of customers, workers have been quoted talking about professionalism

Disc.: Invested, 6% of portfolio

10 Likes

This information can be verified from the quarterly shareholding disclosures. However, I am surprised that there were no corporate announcements for the same. Also, a search on BSE database on Prohibition of Insider Trading (PIT) rules 2015 does not reveal any results even though PIT mandates disclosures for transactions > Rs. 10 lakh in value

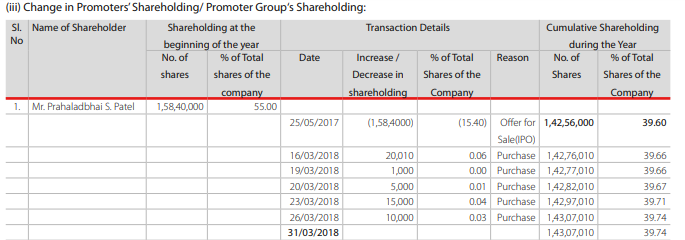

For Q4FY18 quarter, we can know the dates these transactions were done from the AR - snapshot below, but for Q1FY19 the specific dates are not available

Just putting this out here for other members to confirm lapses, if any. We can reach out to the company after this.

Beyond that, I would be interested to know how senior members such as @Yogesh_s perceive these incremental increases in shareholding. Do you consider them material in your analysis of the promoter and company’s growth prospects? If you could share your thoughts, it will be useful. ![]()

1 Like

Disclosures are available here.

Thanks @Yogesh_s. Clearly I wasn’t searching for it properly. Should I delete my earlier post - it adds no value.

Good to see the promoter has continued buying since the last quarterly disclosure.

it is interesting to see industrial 21 % and institutional 44% in Sector wise break-up

As per http://www.the-laws.com/Encyclopedia/Browse/Case?CaseId=202102030300

PRAHLADBHAI SHIVRAMBHAI PATEL Vs. STATE OF GUJARAT

![]()

LAWS(GJH)-2012-3-220

HIGH COURT OF GUJARAT

Decided on March 01,2012

Prahladbhai Shivrambhai Patel Appellant

VERSUS

STATE OF GUJARAT Respondents

JUDGEMENT

- (1.) THIS petition, under Article 226 of the Constitution of India, has been preferred with the following prayers: “(A) Your Lordships may be pleased to issue a writ of mandamus or any other appropriate writ, order or direction directing the respondent authorities to investigate into the matter as to how the government waste land being Revenue Survey No.976 and 1107 in Ganeshpura (Tarabh) village, Tal. Visnagar, Dist. Mehsana, which was shown as gaucher land upto 2004 in revenue record is converted into private land and further be pleased to restrain the authorities from recording transfer or alienate the land being Revenue Survey No.976 and 1107 in Ganeshpura (Tarabh) village, Tal. Visnagar, Dist. Mehsana question; (B) Pending admission, hearing and final disposal of this Writ petition, Your Lordships may be pleased to direct the respondent authorities to restrain the authorities from recording transfer or alienate the land being Revenue Survey No.976 and 1107 in Ganeshpura (Tarabh) village, Tal. Visnagar, Dist. Mehsana question; © Be pleased to pass such other and further reliefs as may be deemed just and proper by Your Lordships in the facts and circumstances of the case.”

(2.) THE facts of the case, as emerging from the memorandum of the petition, are that the petitioner is an agriculturist who makes two ends meet by farming and cattle rearing. According to the petitioner, he and other villagers were grazing their cattle in the Gauchar land bearing Survey Nos.1107 and 976, admeasuring 38172 square metres and 26529 square metres, respectively, registered at Account No.112, situated in the periphery of village Ganeshpura (Tarabh). It is the case of the petitioner that upto the year 2004, this land was shown as “Government Waste Gauchar” in the revenue records and the village people used to graze their cattle thereupon. However, on verifying the record, it was found that Entry No.664 for Revenue Survey No.1107, and Entry No.934 for Revenue Survey No.976, had been mutated, by virtue of which, the names of Patel Ramchand Kuber, Mulchand Talja, Bechar Javra, Haribhai Kalubhai, Hirabhai Dayalji, Chatur Valabhai and Haribhai Revabhai, were shown with the remarks that “the said land was continuously waste land and before 20 years along with Raichand Kuber has been purchased in partnership in an auction”. According to the petitioner, the said Ramchand Kuberbhai Patel was the then Mukhi of Ganeshpura village who, in collusion with the TalaticumMantri, got his name inserted in the revenue record for land bearing Survey Nos.1107 and 976, by way of Entries Nos.664 and 934 respectively. It is the case of the petitioner that the heirs of said Ramchand Kuberbhai restrained the villagers from entering upon the land and grazing their cattle. Representations were made to the Collector and Deputy Collector (respondents Nos.2 and 3) respectively, to take appropriate action in the matter, but none was taken. The petitioner issued a legal notice to the authorities, asking them to make inquiries and take action in the matter as, according to him, Government Waste Gauchar land has been wrongly converted into private land. The petitioner has also filed a criminal complaint against the alleged encroachers. Under these circumstances, the petitioner has approached this Court by making the prayers reproduced hereinabove. Mr.Dakshesh B.Mehta, learned advocate for the petitioner, has submitted that the petitioner has a right to graze his cattle on the waste Gauchar land. That, the land was entered as Waste Gauchar land of the State Government upto the year 2004 in the revenue records, and it is only due to the collusion of the then TalaticumMantri that the name of the then Mukhi of the village has been inserted in the revenue records, whereby Government land has been wrongly appropriated by a private party. That the petitioner and other villagers have been deprived of their right to graze cattle on the Government waste land that was being used as Gauchar land, and in spite of strenuous efforts on the part of the petitioner, the authorities have not paid any heed; therefore, the Court may grant the prayers made by the petitioner.

(3.) MS .Nisha M.Thakore, learned Assistant Government Pleader, has strongly opposed the prayers made by the petitioner by submitting that the land in question was never Gauchar land and a wrong statement in this regard has been made by the petitioner. In support of this submission, the learned Assistant Government Pleader has drawn the attention of the Court to a copy of Form1 of the year 19171918, annexed as AnnexureRI to the affidavitinreply filed by respondent No.2. It is further submitted that the land in question was sold in auction to Ramchand Kuberbhai, Mulchand Talija, Bechar Javra, Haribhai Kalubhai, Hirabhai Dayalji, Chatur Valabhai and Haribhai Revabhai somewhere in the year 1930 and thereafter their names have been inserted in the revenue record. The learned Assistant Government Pleader has supported this submission by pointing out the copies of Village Form No.7/12 from the year 1952 to 1998, annexed as AnnexureRII collectively, to the affidavitinreply. It is further contended by the learned Assistant Government Pleader that the entries in favour of the persons to whom the land has been sold in auction have never been challenged in any proceedings by the petitioner. That, as the land was never Gauchar land, the petitioner has no right to graze cattle thereupon. It is further submitted that the petitioner was well aware of the auction sale and the entries pertaining to the auction, but did not raise any objection at the relevant point of time, therefore, the prayers made in the petition may not be granted, and the petition be dismissed.;

Is there a way to get a copy of the full judgement of this case to be able to deep dive into which party was the victim and which party was the accused in this court case? I presume the “petitioner” mentioned in the case is the promoter himself.

PSP Projects bags order worth INR 372.72 crores

1 Like