Incorporated in 1987, Prince Pipes and Fittings Ltd (PPFL) is one of the leading polymer pipes and fittings manufacturers in India. PPFL market its products under two brand names: Prince Piping Systems; and Trubore.

Company overview:

PPFL currently manufactures polymer pipes using four different polymers: UPVC; CPVC; PPR; and HDPE, and fittings using three different polymers: UPVC; CPVC; and PPR.

PPFL has six manufacturing plants, which gives it a strong presence in North, West and South India. Plants are located at the following locations:

- Athal (Union Territory of Dadra and Nagar Haveli)

- Dadra (Union Territory of Dadra and Nagar Haveli)

- Haridwar (Uttarakhand)

- Chennai (Tamil Nadu)

- Kolhapur (Maharashtra)

- Jobner (Rajasthan)

The total installed capacity of its six existing plants is 241,211 tonnes per annum as at October 31, 2019. Company plans to expand the installed capacity at Jobner (Rajasthan) from 6,221 tonnes per annum as at October 31, 2019 to 17,021 tonnes per annum by December 31, 2019 and to 20,909 tonnes per annum by the end of Fiscal 2020. PPFL currently using five contract manufacturers, of which two are in Aurangabad (Maharashtra), one is in Guntur (Andhra Pradesh), one is in Balasore (Odisha) and one is in Hajipur (Bihar).

PPFL to set up a new manufacturing plant in Sangareddy (Telangana), with a total estimated installed capacity of 51,943 tonnes per annum. PPFL is likely to commence production at the Telangana plant in FY21.

PPFL sell Prince Piping Systems products to distributors, who then resell the products to wholesalers, retailers, and plumbers. As at October 31, 2019, PPFL sold Prince Piping Systems products to 1,151 distributors in India. PPFL sell Trubore products directly to wholesalers and retailers. As at October 31, 2019, PPFL sold Trubore products to 257 wholesalers and retailers.

Industry Overview:

Overall sales of the plastic pipe industry at Rs 29,000-30,000 crore for Fiscal 2019

India has very low per-capita plastic consumption of about 11 kg, compared with the global average of 30 kg

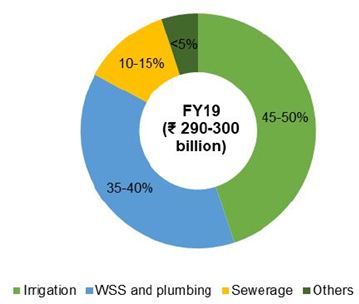

Segmentation by end-users:

Resin:

Resin is the key raw material for plastic pipe

Resin manufacturing process: EDC (Ethylene Dichloride) -ethylene, and directly from VCM (Vinyl Chloride Monomer)

The total installed capacity of the domestic PVC industry is about 15.57 lakh tones; Reliance 625,000 MTPA; Finolex Industries 272,000 MTPA; DCW- 90,000 MTPA; DCM Shriram 70,000 MTPA

India is the largest importer of PVC resins in the world – sourcing more than 50% of its needs from import

As on September 2019: PVC price at $900/MT vs $973/MT; EDC price at $317/M vs $332/MT; Ethylene price at $780/MT vs $1242/MT and DCM price at $735/MT vs $733/MT

Plastic Pipe category:

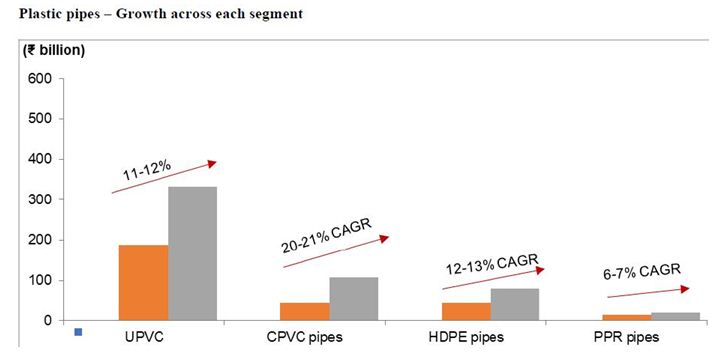

Plastic pipes are made of different types of polymers. The four key types are unplasticised polyvinyl chloride (UPVC), which represents 65% of industry demand, chlorinated polyvinyl chloride (CPVC) – 15%, HDPE –15% and polypropylene (PPR) – 4%

CPVC:

The Indian CPVC market stood at Rs 3,000-3,500 crore

Domestic market size for CPVC around 150,000-180,000 MT. There are four major suppliers of CPVC raw materials in India; two from Japan, one each from Europe and US. China and Korea supply around 40,000 MT

The Govt of India has recently on August 2019- imposed antidumping duty (ADD) of 10% on CPVC resin/compound originating from China and Korea

EBIT Margin in PVC pipe is around 8% while for CPVC it is 12%

Outlook:

Of India’s 160 million hectare of cultivated land, a little less than 50% is irrigated

Plastic pipes and fittings industry to post a CAGR of 12-14% to Rs 50,000-55,000 crore in Fiscal 2024

Fittings to piping ratio for agri is around 7-7.5% while for non-agri the ratio is around 15% (in value terms)

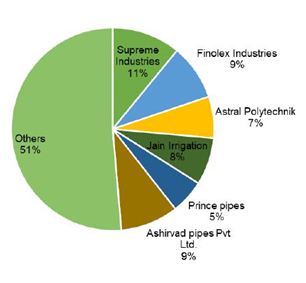

Peer companies:

Capacity: Supreme 418,000 MTPA; Finolex- 370,000; Astral- 221,000 MTPA; Ashirwad- 108,000

Market share:

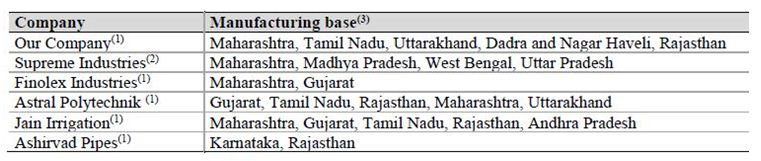

Manufacturing base:

PRINCE PIPES AND FITTINGS LIMITED

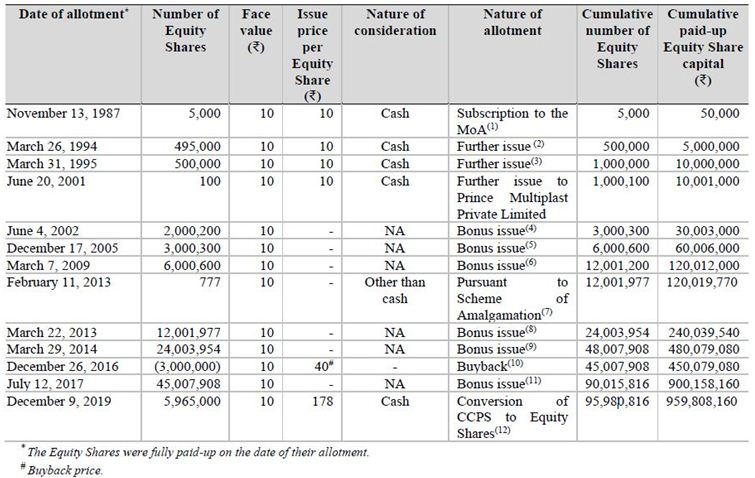

Capital History:

PPFL has not diluted any equity in the last 17 years, while it bought back 30 lac shares in December 2016 at Rs 40/share.

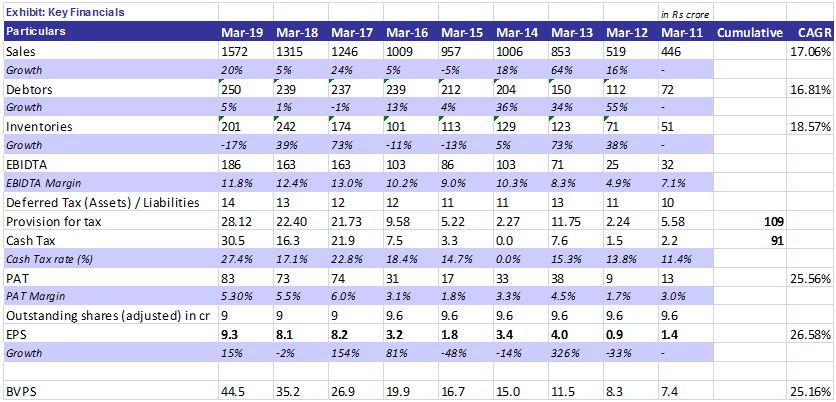

Financial Snapshot:

• Company has reported above industry average growth rate in last eight years

• Margin has improved which resulted into higher profit growth compared to revenue growth

• Company has maintained both and inventory and debtors very well

Dupont Analysis:

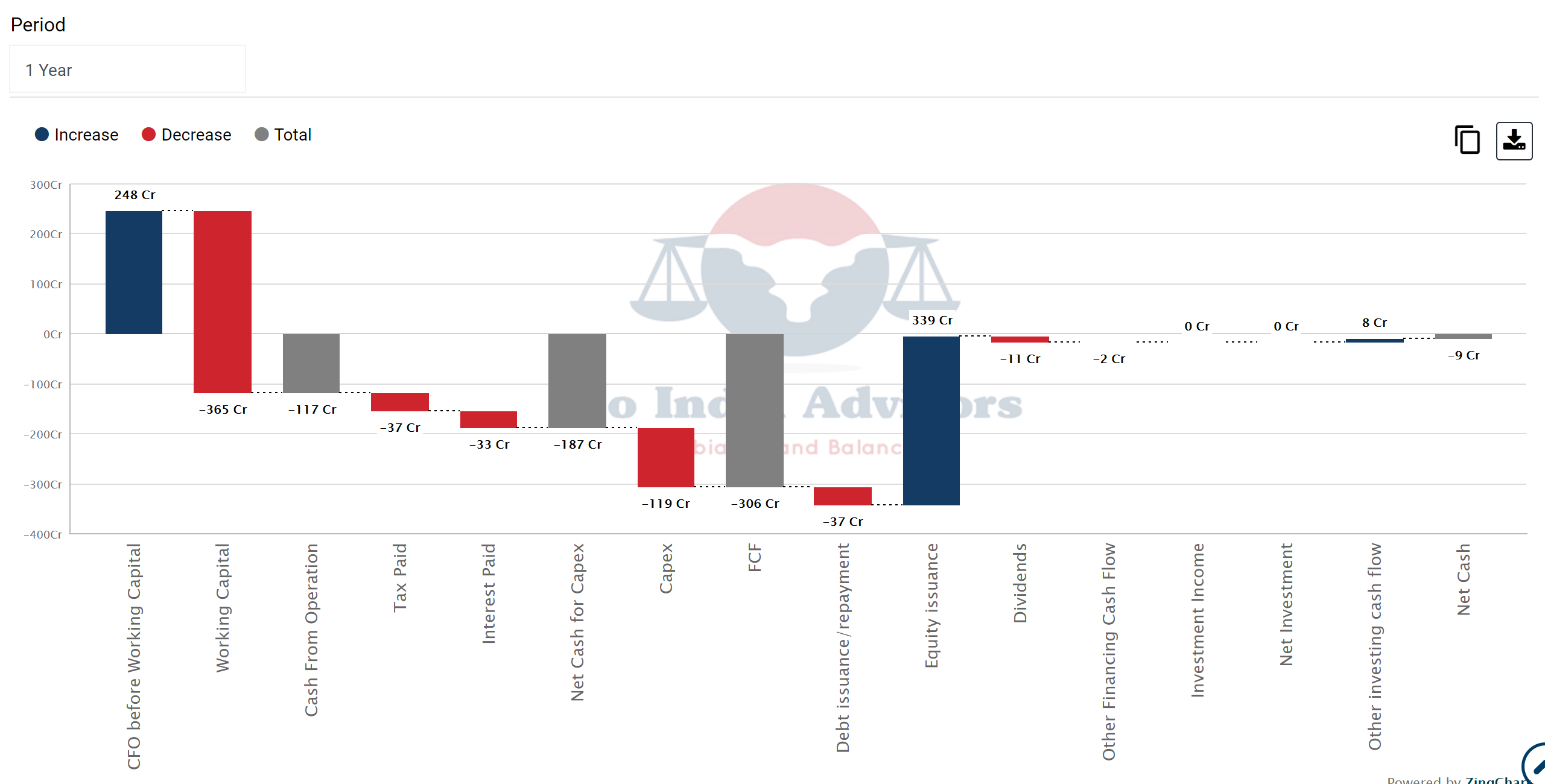

Cash-flow Analysis:

• PPFL is generating very strong cash over a period of time

• Cash conversion cycle has improved mainly due to increase in payable days (see below Ratio Analysis)

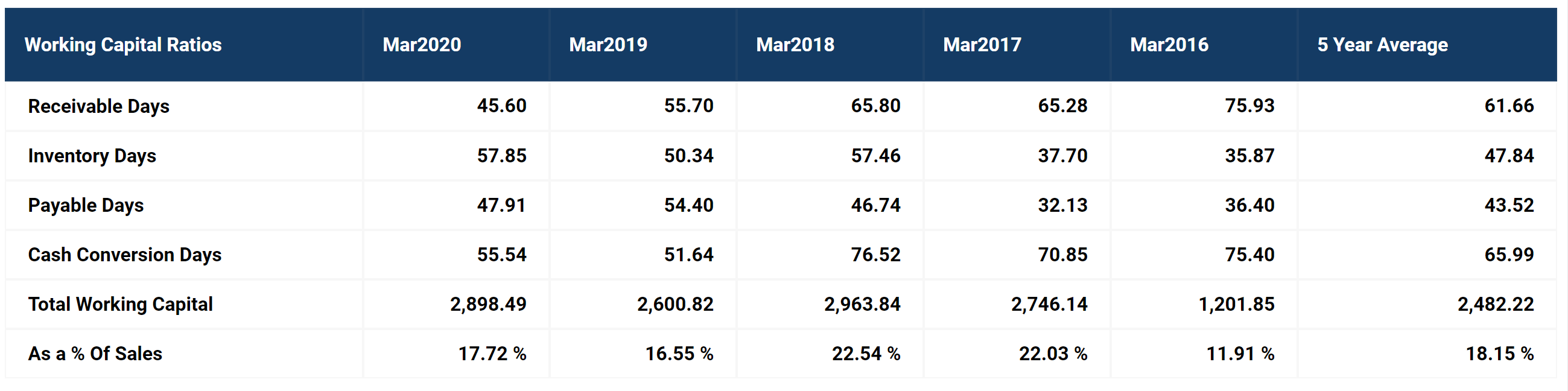

Ratio Analysis:

• Requirement of working capital gradually decreasing

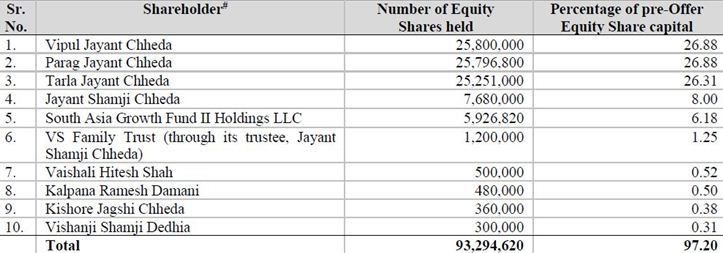

Top ten Shareholders:

**(Chheda’s are promoter and promoter group)

Pre IPO placement:

In pre-IPO placement, Prince Pipes issued 5,926,820 equity shares, representing 6.18% stake for cash consideration of Rs 106.18 crore to South Asia Growth Fund LLP at Rs 178/share

IPO details:

The Rs 500 crore IPO comprises an Offer for Sale (OFS) of Rs 250 crore and fresh issue of Rs 250 crore. Company will issue fresh 1.4 crore equity share at a price band of Rs 177-178/share. Post the issue promoter group’s stake will reduce to 65.8% from 90.1%.

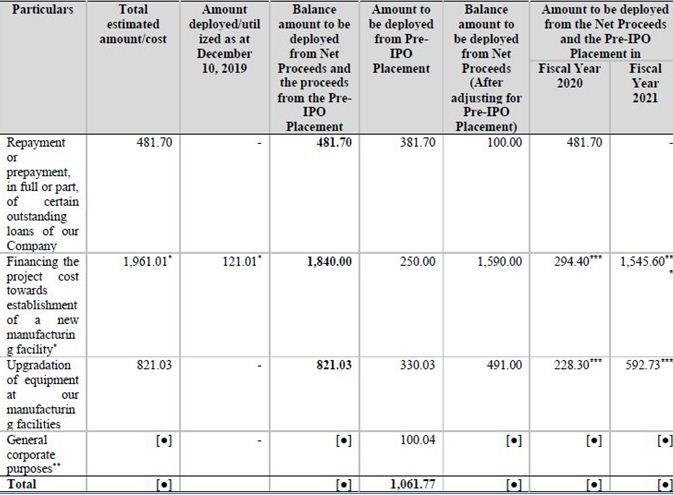

Requirement of funds and proposed schedule of deployment:

Key Risk:

Litigation against the directors:

-

Montana Developers Pvt Ltd (Montana) filed a criminal complaint in January 2013 before the Metropolitan Magistrate at Andheri against M/s. Aditya Developers (Aditya) and its partners, including Jayant Shamji Chheda, MD of PPFL and Heena Parag Chheda (each hold a 10%). Montana alleged misrepresentation of certain material information in JV Agreement leading to fraudulent inducement to enter into the JV Agreement and making an interest free deposit of Rs 46.25 crore to Aditya

-

Montana filed a statement of claim dated November 30, 2013 before the appointed arbitrator; the amount claimed by Montana in this litigation is up to Rs 904.65 crore along with interest at the rate of 27% per annum to be paid by the Aditya and its partners

-

Montana had alleged that since the promoter group had not disclosed about the litigation in its DRHP the rating agency (CARE) should withdraw the rating for the company and also the erstwhile CS & Independent Directors step down from the board.

For details about the litigation click here

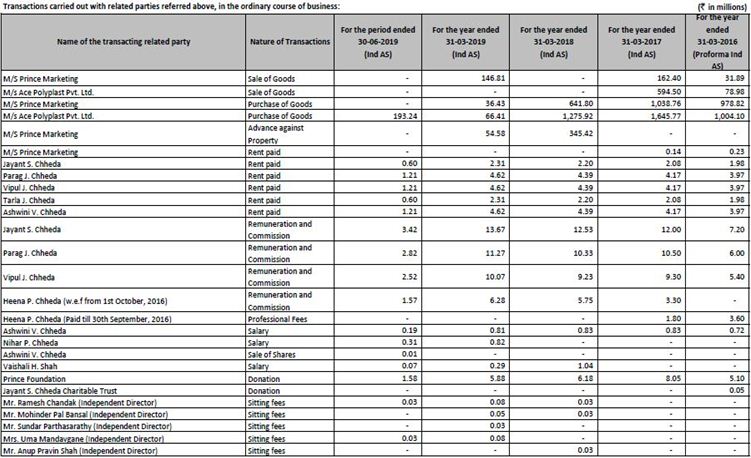

Related party Transactions:

PPFL has entered into certain related party transactions with Promoters/Promoter Group/Group Entities/Key Managerial Personnel. For Fiscals 2017, 2018 and 2019 and the three-month period ended June 30, 2019, the amount of such transactions was Rs 350.4 crore, Rs 232.67 crore, Rs 37.2 crore and Rs 21.06 crore respectively, representing 26.35%, 17.62%, 2.37% and 5.55% of Revenue from Operations, respectively.

Though the percentage of related party transaction in total revenue has come down, we have keep monitor it regularly as it was very high earlier.

Disclosure: No holdings in the stock and didn’t apply for shares in their IPO (as it is going to list in few days). This is an introduction post on the company. Financial data have been taken from Ace Equity