Prince Pipes is an evolving story. The degrowth in the Q-on-Q volume seems to have spooked and many questions around it. It appears that the chief reason was channel inventory was high in Q4 end just before lock down & many days in Apr were lost due to it. Now the channel inventory is very low at the end of Q1. Cross-selling CPVC seems to be the main growth plank. The co became long term debt free and other aspects of the balance sheet continue to improve. Co is trying to break into the B2B business and certainly has the power of all these strong alliances with 2 new ones added , Corzan & also Ultratech Building solutions.

Key Excerpts from Con call

Our results were impacted due to three reasons. Firstly, as we had indicated during the last quarters call, we took a strategic decision in March that we wanted to have a high product availability in the market due to the uncertainty of a potential lockdown. Also, with the anticipated decline in PVC prices We kept our capacities running high to produce and sell to align with the above goal. Hence, in April, the channel inventory was relatively high.

Moving forward June performance had been better than May and July performance had been much better than June. We are returning back to our regular growth trajectory

The real estate sector has been reporting positive growth. This augurs well for us signalling traction in piping products.

Aligning with our strategy of winning In many India’s the Ultratech building solution and Prince Pipes Synergy is well placed to be a mutually beneficial partnership, especially for the semi urban and rural markets. The UBS platform has a vast network of around 2000 dealers and Prince can now leverage the relationship of registered dealers on the UBS platform.

At Prince we have been able to build a range of innovative products, consistently catering to applications across the board in a market like India which is typically been late in the adoption curve of technology and products that are well accepted globally

I am excited to introduce Prince Onefit industrial CPVC pipes. We are confident that this product will replace the conventionally used mild steel pipes for industrial application. Onefit will be licenced from Corzan with our global partner of Choice Lubrizol. This Corzan product of Lubrizol is the preferred industrial CPVC solution across the globe. Firstly, the Indian industrial piping market size is expected to be around approximately 16,000 crores. This is today dominated by the conventional MS pipes in India today, CPVC is majorly used only for the domestic application whereas globally CPVC pipes are very well accepted for industrial application as well. Secondly, the Industrial CPVC segment is underpenetrated and has low competitive intensity.

Also, the pipe to fitting & valve ratio is favourable, making this a key value proposition.

Lastly, this segment has high barriers to entry because of high gestation periods for orders and the required techno commercial expertise.

Prince Onefit will provide an optimum solution to industries such as chemical, power generation, metal treatment, paper and pulp, mineral processing, water treatment, plants, among many others. Now with this new product, Prince is India’s first company to have a three polymer solution for industrial application. Easyfit in PVC pipes, Greenfit PPR pipes and now Onefit CPVC pipes.

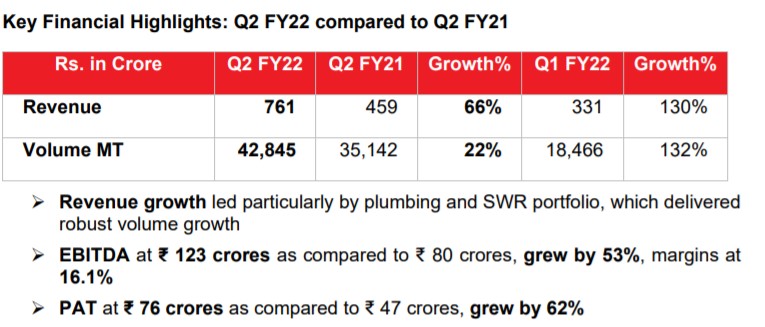

This was owing to an overall improvement in performance at the EBITDA level, added by a sharp decrease in finance cost by 60% due to the complete repayment of long term debt and continuous improvement in cost of short term borrowings. On the key balance sheet parameters for the quarter ended we would like to state our gross debt as on 30th of June 2021 stood at 157 crores compared to a gross debt of 256 crores as on 30th of June 2020. We’ve repaid our long-term outstanding debt and have become long term debt free as on date. While we have been able to reuse the borrowing costs for the past six quarters, I’m glad to share that we have achieved partial recourse terms on our channel financing facility.

Roughly around 65 odd percent is building material, 30 odd percent is Agri and 5 percent is Infrastructure

I think the only reason you know there has been a significant volume de-growth is like we mentioned, the channel inventory was very high.

CPVC would be around 18-20% and the balance would be the other polymers

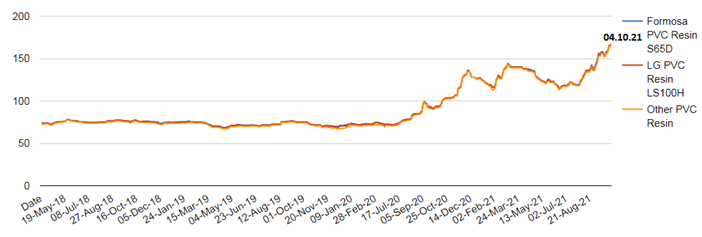

If you see the PVC trend, actually it has started moving upwards as demand is normalising and supply continues to remain tight. There was a slight inventory loss in the June quarter of around 5 cores.

On Channel finance - So we had it around 54crores in terms of the utilisation so far and we wanted to be slightly moderate over there because we are also moving to partial recourse type of structure but slow but steady is what we’re looking at is around 54-55 crores

Supply of PVC continues to remain a challenge.

I think we need to target double digit growth in CPVC every year. It’s hard to comment on what that will be as a percentage of the overall revenue, but I’m pretty optimistic about strong growth in CPC from here on.

On Margins So if it’s hard to give guidance when we’ve always been conservative, as a company, So I think 13 to 15% is something that we have already always guided at, and I would like to stick to that. And then we are happy to keep working and trying to exceed I’ll, you know,

On Volume - and July have been much better than June. A few reasons for that is channel inventory was very low by the end of the quarter. And we have just started seeing an increase in the PVC pricing. And typically, when the when the prices are rising, generally the distributors would tend to stock up more.

And today the key influencers are retailers and plumbers in some cases. In rural India it could also be the individual homeowners. So we have to target across these segments.

Today, if you see, you know we were talking about a few quarters ago. Smaller players were struggling to get access to raw material after the anti dumping duty.

Today, larger players are also unable to get supply of raw materials, so today they do not have the supply security in the marketplace, so price is only going to be on paper unless you’re actually going to be able to sell. So today not only the smaller players, but larger players also are running here and there for product, whereas today we are in an absolutely strong position as far as supply security is concerned and any price hikes you know will be industry wide.

On RM costs - And that holds true through today as well, so I don’t think that delta in our costs has moved significantly. The delta, in terms of the finished good pricing, has reduced to the market leaders

Sure, so Agri has not been the only reason for the drop in volumes, but it has been one of the key reasons. Usually for us in Q1 Agri would be you know around 38 to 40%, which in this quarter has been around 30%.

In my mind, one is whether it’s North America, Europe, Latin America. Inherent demand has been very, very robust for PVC, so they are choosing to sell locally and not export as much. And freight costs globally have gone up in multiple which have kept this pricing buoyant.

So Industrial is still not developed, we’re still relying on traditional products. I think plastic plastic pipes are still being penetrated. There is some further room to be penetrated in the industrial space and today in India, if I look at the CPVC industrial space, there is only maybe 1 clear leader in India and It’s not easy to import simply because of the freight cost.

And you know, if we are, you know I’m fairly confident because the product (Industrial CPVC) is so much superior to the conventional solution.

Because the Y-oY is also was impacted by Covid, but in our industry, I think QOQ is never the right comparison, especially March quarter to June quarter simply because the dynamics are so much different for Agri and for plumbing as well. Because Q4 is where you know all the distributors are gunning for their targets and you know.

Demand is going to improve from here on , and that direction has already started moving. Also, channel inventory was very low at the end of the quarter and with the increase in the PVC prices starting, I think that will be a further boost for the demand.