Detailed Notes with Commentary and Actionable Insights: Premier Explosives Limited Q1 FY '26 Conference Call

I. Document Overview

• Nature: Transcript of the Conference Call hosted by Stellar IR Advisors Private Limited for Premier Explosives Limited (PEL).

• Date of Call: August 13, 2025.

• Purpose: Discussion pertaining to the company’s financial results for the first quarter ended June 30, 2025.

• Key Management Present: Mr. T.V. Chowdary (Managing Director) and Mr. Vijay Kumar (Chief Financial Officer).

• Disclaimer: The call contains forward-looking statements based on the company’s beliefs, opinions, and expectations as of the date, which are not guarantees of future performance and involve unforeseen risks and uncertainties.

II. Q1 FY '26 Financial Performance Highlights

• Revenue from Operations: INR 142.1 crores, marking a strong growth of 72% year-on-year (YoY) and 92% quarter-on-quarter (QoQ).

◦ Commentary: This indicates a significant acceleration in the company’s top-line growth, especially compared to previous periods.

• Operating Profit (EBITDA): INR 20.9 crores, growing 35% YoY and 118% QoQ.

◦ Operating Margin: Stood at 14.7%.

Commentary/Actionable Insight: A participant noted a 4% drop in EBITDA margin YoY. Management attributed this to most defense products being dispatched in the next quarter and valuing stock at cost or market value, whichever is lower. They expect margins to improve from Q2 FY '26 onwards. This suggests that Q1 may have had a temporary impact due to inventory valuation and timing of dispatches. Investors should monitor Q2 margins for the anticipated recovery.

Commentary/Actionable Insight: A participant noted a 4% drop in EBITDA margin YoY. Management attributed this to most defense products being dispatched in the next quarter and valuing stock at cost or market value, whichever is lower. They expect margins to improve from Q2 FY '26 onwards. This suggests that Q1 may have had a temporary impact due to inventory valuation and timing of dispatches. Investors should monitor Q2 margins for the anticipated recovery.

• Net Profit (PAT): INR 15.3 crores, showing a substantial growth of 110% YoY and 314% QoQ.

◦ PAT Margin: Stood at 10.8%.

• Cash Profit: INR 18.2 crores generated in Q1 FY '26.

• Key Driver for Revenue and Margin Improvement: Higher contribution from the Defense and Space segment, which accounted for 86% of the revenue in Q1 FY '26, up from below 80% previously.

◦ Commentary: This shift towards the higher-margin Defense segment is a positive trend for profitability.

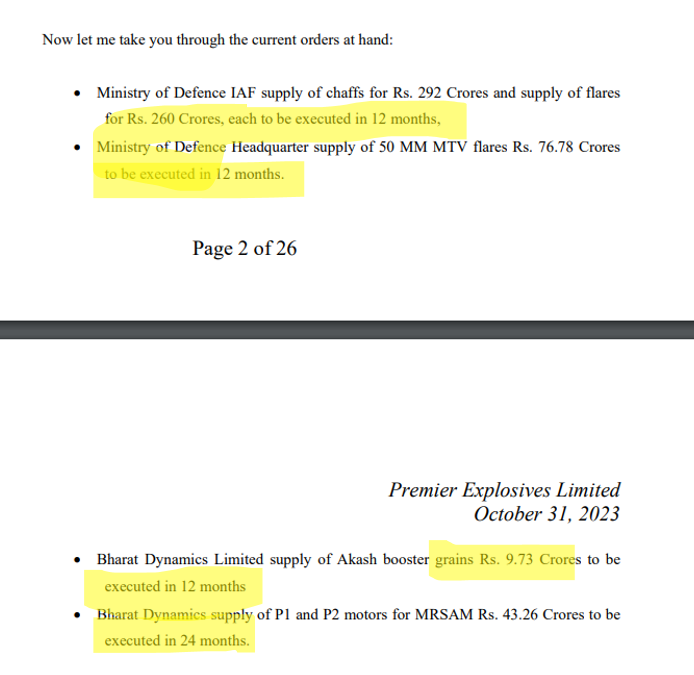

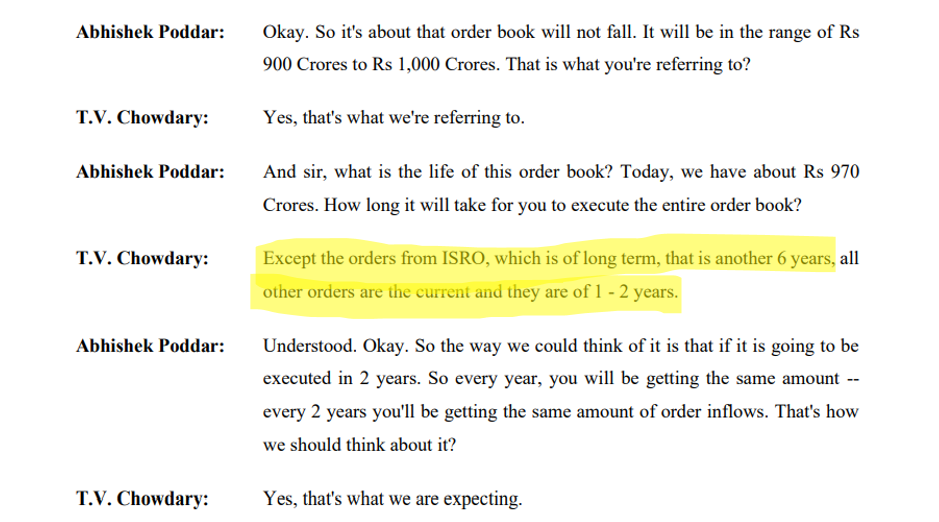

• Outstanding Order Book: INR 988.5 crores as of June 30, 2025.

◦ Significance: This represents 2.4 times the financial year 2025 revenue.

◦ Segment Split:

Defense segment: INR 860 crores (87% of total).

Explosives segment: INR 69 crores (7% of total).

Service segment (Operational & Maintenance): INR 59 crores (6% of total).

◦ Commentary/Actionable Insight: The strong and growing order book, heavily skewed towards the high-margin Defense segment, provides excellent revenue visibility and confidence in future growth trajectory.

III. Operational Status & Challenges

• Fire and Explosion Incident (Katepally Village, Telangana): Occurred on April 29th, 2025, in one of the 61 production buildings (big solid propellant mixer unit).

◦ Impact: Did not have a material impact on overall operations, but the propellant plants remain under suspension as a regulatory measure.

◦ Regulatory Action: Pollution Control Board temporarily directed the plant shutdown.

◦ Resolution Expectation: Actively engaging with authorities to obtain necessary clearances within a few weeks. The propellant plant is expected to start within 1 month.

◦ Financial Impact of Suspension: Approximately INR 20 crores over 2 years.

◦ Insurance: Facilities are fully insured, and the company anticipates receiving the insurance claim in the coming months.

◦ Reconstruction: The building that collapsed will take 2 years to reconstruct.

◦ Status of Other Plants: The two manufacturing facilities in Katepally and Peddakandukur (high explosives, warheads, ammunition) are already functioning and producing.

◦ Commentary/Actionable Insight: While the incident caused a temporary setback to the propellant plant and an estimated financial impact, management indicates it’s contained, insured, and other key operations are back online. The expected restart of the propellant plant within a month is positive. Investors should monitor the actual timeline for clearance and the receipt of insurance claims.

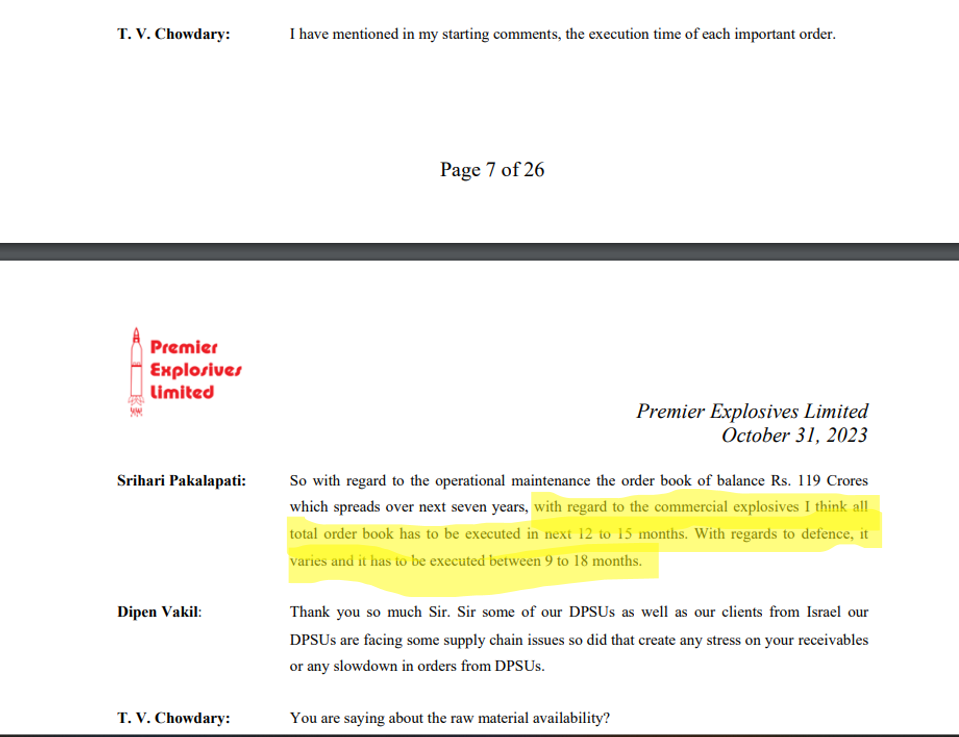

• Chaffs and Flares Order: 62% executed so far, with the balance 38% (approximately INR 180 crores) to be completed by December 2025 or March 2026 (before financial year-end).

◦ Penalties (LD): The company is already at the maximum 15% penalty slab, so no further penalties are expected.

◦ Waiver/Share: Application for waiver of Liquidated Damages (LD) is pending with the Ministry, with positive results expected before March 2026. The company is also working with its vendor to share the LD.

◦ Impact on Margins: Once executed, an uptick in margins is anticipated.

◦ Commentary/Actionable Insight: The completion of this order and potential waiver of penalties could further boost margins in subsequent quarters. Monitoring the outcome of the waiver application is relevant.

IV. Strategic Outlook & Growth Drivers

• “Atmanirbhar Bharat” Initiative: The Ministry of Defense’s promotion of domestic production and reduction of imports directly supports PEL’s growth by driving local manufacturing.

• Core Competencies/Specializations:

◦ Only Indian company qualified to manufacture countermeasures.

◦ Specializes in exporting fully assembled rocket motors.

◦ Also manufactures and exports warheads, mines, and ammunition.

• Market Focus: Focused on becoming a key player in both domestic and export markets.

• Emergency Procurement Orders: Actively participating in emergency procurement orders.

◦ RFPs in Pipeline: Participated in approximately INR 700 crores worth of RFPs .

◦ Commentary: Even securing a portion of these RFPs would significantly boost the company. While defense orders take time to mature (5-6 months even for emergency procurement), this indicates a strong potential pipeline.

• Revenue Guidance for FY '26: Stands by the previously indicated turnover of INR 600 crores .

◦ Commentary/Actionable Insight: This guidance implies continued robust growth from the Q1 FY '26 revenue of INR 142.1 crores.

V. Capex Plans & Funding

• Odisha Plant (Greenfield):

◦ Products: Ammunition, warheads, and raw materials like HTPB.

◦ Phases: Divided into 3 phases.

◦ Status: At a nascent stage; land identification by the Odisha government is in process, which may take up to a year. Planning and design will start after land acquisition.

◦ Capex:

Phase 1 (initial and infrastructure development): Around INR 100 crores .

Total Capex (over 10 years, across 3 phases): Around INR 800 crores .

◦ Commentary/Actionable Insight: This long-term, substantial capex plan indicates a significant growth ambition and future capacity expansion. The timeline for land acquisition is a key determinant for the project’s progression.

• Katepally Plant Capacity Enhancement:

◦ Areas: RDX, HMX, and integration of rockets.

◦ Timeline: Immediate. RDX plant expansion has already started and is expected to come into production before December 2025 .

◦ Capex for RDX Plant: Approximately INR 25 crores .

◦ Commentary: This shorter-term capex for existing facilities will provide quicker returns and operational boosts.

• Fundraise Plans: Looking for either QIP (Qualified Institutional Placement) or preference issue.

◦ Amount: INR 300 crores .

◦ Purpose: Primarily for capex (around INR 200 crores) and the balance for repayment of term loans and general corporate purposes. Also includes INR 50 crores for a JV payment.

◦ Timeline for Results: New investments are expected to start yielding results in FY '26-'27.

◦ Commentary/Actionable Insight: The fundraise is critical for supporting the ambitious capex plans and strengthening the balance sheet. Successful completion of the fundraise will be a positive trigger.

VI. Joint Ventures & Partnerships

• JV with Global Munitions Limited: Formed Global Premier Limited .

◦ Proposed Manufacturing: RDX, HMX, rocket motors, energetic materials, propellants, and warhead filling.

◦ Status: In early stages, assessing total investment needed. Land is under acquisition.

◦ Expected Contribution: Will take at least 1 more year to get licenses and start trial production.

• MOU with Astra Micro Products: No significant development.

◦ Commentary/Actionable Insight: The JV with Global Munitions appears to be a strategic move to broaden product offerings and capacities, aligning with PEL’s focus on energetic materials and rocket motors. Its contribution is a medium-term prospect.

VII. Specific Product & Segment Discussions

• PETN: Produced and consumed for self-consumption (detonating fuse, cast boosters). Also sold and exported to international buyers. The company was one of the first to manufacture PETN in India in 1985.

◦ Commentary: Clarifies that PETN is not largely imported, and PEL has a long history and capabilities in this area.

• Explosives Business (Mining): Expecting growth, but it won’t compete with the Defense segment due to fierce competition and reverse auctions leading to lower prices.

◦ Current Supply: Not supplying bulk explosives to Coal India, but supplying to Singareni Collieries and recently won a tender for accessories. Expected to participate in bulk explosives tenders later in the calendar year.

◦ Commentary: Management prioritizes higher-margin defense business over low-margin bulk explosives, which is a prudent strategy.

• QRSAM (Quick Reaction Surface-to-Air Missile): PEL is the qualified source for the propellant of QRSAM, meaning any QRSAM production (by BDL or BEL) will require propellant from PEL.

◦ Timeline: Expected to go into FY '27.

◦ Commentary: This positions PEL as a critical supplier for a key domestic defense program, ensuring a steady revenue stream once production scales.

VIII. Other Financial Notes

• Other Income: Increased significantly due to the reversal of a previously recognized loss provision on some long-term contracts that are no longer expected to incur losses.

◦ Clarification: Not related to the LD charge for chaffs and flares.

◦ Commentary: This one-time gain contributed to the strong Q1 results.

Overall Actionable Insights for Stakeholders:

-

Monitor Defense Segment Performance: The strong shift towards the high-margin Defense and Space segment is a key driver for PEL’s profitability. Continued high contribution from this segment will be crucial for sustained growth.

-

Watch Capex Execution and Fundraise: The ambitious capex plans, particularly for the Odisha plant, are long-term growth enablers. Successful fund-raising (INR 300 crores) and timely execution of capex (e.g., RDX plant by Dec 2025) are critical.

-

Track Propellant Plant Reopening: The restart of the suspended propellant plant, anticipated within a month, is important for full operational capacity.

-

Observe Chaffs and Flares Order Completion: The completion of the remaining INR 180 crores of this order, along with the outcome of the LD waiver application, could provide an additional boost to margins.

-

Evaluate RFP Conversion: The participation in INR 700 crores worth of RFPs represents a significant pipeline. Conversion of these bids into firm orders will provide further growth visibility.

-

Understand JV Progress: The Global Premier Limited JV is a future growth avenue. Monitoring its progress, especially land acquisition and licensing, will indicate its potential contribution.

-

Long-Term View: Given the nature of defense contracts and large-scale projects like the Odisha plant, PEL requires a long-term investment perspective.

-

Risk Awareness: The forward-looking statements carry inherent risks and uncertainties, as explicitly stated by management. Recent safety incidents (e.g., the fire and the unfortunate loss of life outside the process building) highlight operational risks, even if management considers their financial impact limited