Indian company Premier Explosives Limited (PEL) has agreed to explore opportunities for collaboration with Israel Aerospace Industries (IAI), it was announced on 6 January.

In a filing to the Bombay Stock Exchange, PEL said that its memorandum of understanding (MoU) with IAI will enable the two companies to “explore potential business opportunities”.

Terms of the MoU were not disclosed, although it is likely that the agreement will look to leverage India’s operation of the Barak-8 medium-range self-propelled surface-to-air missile (SAM) system, which was designed by IAI in collaboration with India’s Defence Research and Development Organisation (DRDO).

PEL is a major supplier to India’s missile manufacturing network providing its products to support systems including the Barak-8, the Akash self-propelled SAM, and the Astra radar-guided air-to-air missile.

I started researching on this company as the stock price hit a 52 week high recently. I went through the 2016 AR and posting my observations:

Company operates in providing explosives for commercial (Mining, etc), defence space.

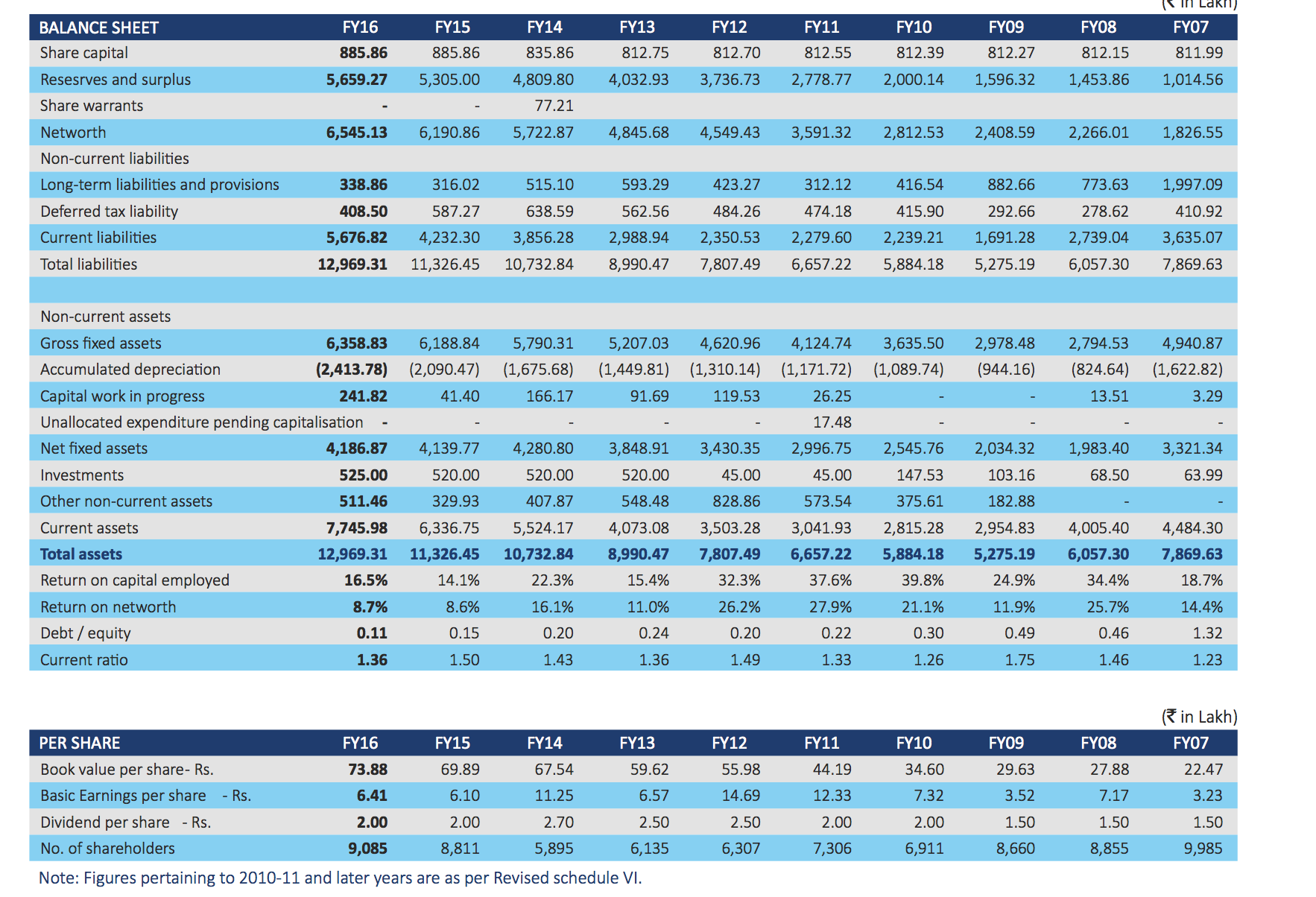

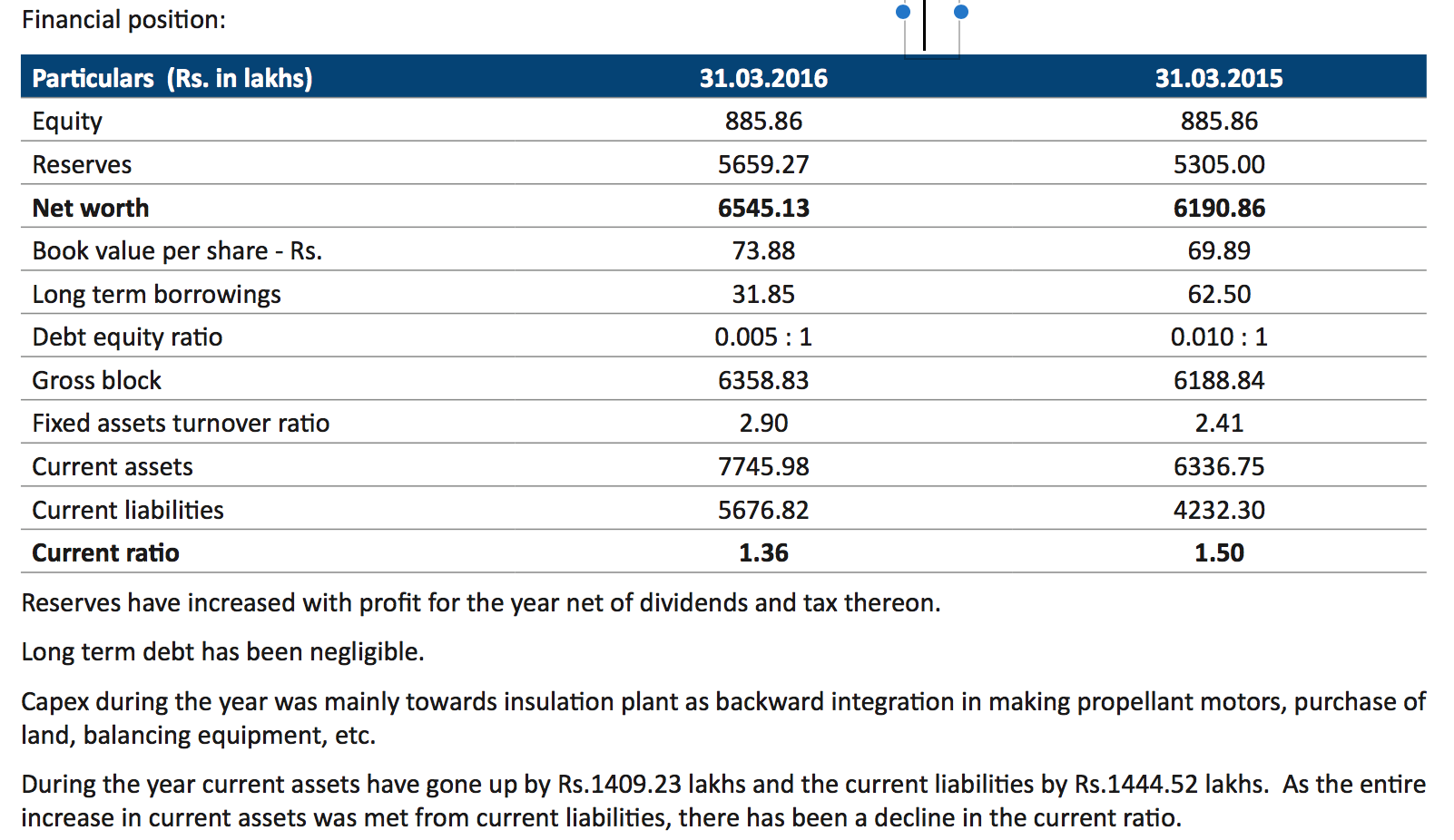

These are the 10 years data for the company. As it can be seen, the company has maintained decent topline growth. FY16 profits would have been higher had it not been for exceptional items of 269 lacs which was due to voluntary retirement of multiple staff members. 2017 topline has been 23071 lacs and PAT has been 1475 lacs. Also the company has been paying out dividend regularly:

Expansions are being planned in existing sites. Also a new greenfield project is being provisioned at a new site. Estimated capex will be 3000 lacs out of which 2300 lacs worth of loans have been sanctioned. Also the wind power business now accounts for lesser than 10% revenues. Hence company now focuses entirely on explosives business. This is good as per me.

The company has an MOU with Israel Aerospace Industries and also a collaboration it BITS Pilani for research in high energy materials.

Dr.Amarnath Gupta, Chairman and Managing Director of the Company, has been, awarded with an Honorary Fellowship’ for the year 2016 by the High Energy Materials Society of India (HEMSI), for his outstanding contributions towards Establishment of Advanced Propellant Processing Technology.

They have good amount of licenses with them which can act as entry barrier for other players.

Overall, I feel the company can do good in next few years and with the capacity expansions kicking in, we can see better numbers in next 1-2 years.

Views invited.

Capex for next 2 years is approx 150 crores. 60 crores to be utilized in FY17-18 for ammunition factory and land and basic infra for ISRO. Remaining 90 crores for FY18-19 for completing factory for ISRO(The company has received a letter from Andhra Pradesh Industrial Infrastructure Corporation (APIIC) for provisional offer of 202 acres of land at Routhsurmala village in Chittoor district of Andhra Pradesh for establishing a unit to manufacture Solid Propellant.).

Opportunity size from ISRO is huge. As per the CMD, if the initial delivery of the strap on motors go well (please note that this is a trial order), then ISRO has capacity to consume these as fast as they can be produced. Currently Premier will operate at capacity of one motor in 3 months. Aiming to target 2-3 per month in 2 years time frame.

66 crores raised from QIP in May 2017. 30 crores raised through warrants @408

Receivables are high as few exports happened in March for which payments are pending.

Bidding intensity increases in defence orders: As per CMD, not much threat from new entrants as they may be able to deliver the metallic parts, however high energy materials (which is PEL’s forte) cannot be delivered without support from a experienced player. Hence it is too early to comment and differentiate between the serious and non-serious players.

Target for FY17-18 is 25% increase ~300 crores top line with a wish of closer to 50% defence orders.

Few items made by the company are going to be useful for Airforce, Navy as well as Army. Hence if they get order from one, there is a good chance of getting order from the other.

Out of the total raw material cost, most of it was for ammonium nitrate.

This field is subjected to approvals and licenses and hence there can be delays in the execution plan for the capex. That could lead to delay in delivering orders.

Increased competition in Defence space. However management seems not to bothered by the same.

One point cited by someone was that New Zealand built a rocket with 3D technology at lower cost. Could this lead to slow down in ISRO? CMD replied well saying if New zealand can make it so can ISRO. Also he said that 3D printing(as per his limited knowledge) cannot be extended to high energy particles which means that PEL will be unaffected.

We wish to inform you that the Securities Allotment Committee of the Board of Directors of the Company at its meeting held today i.e. on August 02nd , 2017, inter – alia, approved the Allotment of 1,27,564 equity shares of face value of Rs. 10/- each at issue price of Rs. 408 per equity share including a premium of Rs. 398 per equity share for an aggregate amount of Rs. 5,20,46,112; and 1,35,100 Warrants convertible into Equity Shares of face value of Rs.10/- each at issue price of Rs.408 per Warrant including a premium of Rs.398 per Warrant on payment of 25% of the Issue price with the amount received for Warrants, aggregating to Rs.1,37,80,200; to the allottees as listed in attachment.We request you to take the above ON record and be treated as compliance under the applicable regulations of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015. The Meeting commenced at 11.30 A.M and concluded at 01.30 P.M.

Anyone still following this scrip? I invested it at Rs 508 per share but the CMP is hovering around the Rs 360 range. Any view on whether this will regain lost ground?

A few observations on Premier, ISRO, the space business and valuation:

Space was earlier a strictly govt-regulated business. Now they’re opening it up to private companies. For eg, currently Godrej Aerospace (engines and boosters for ISRO’s rockets) has had to turn down inquiries from private players, and doesn’t assemble the final engine itself, but sends parts to ISRO. Overall regulation in space will decrease. Antrix is focused on profit making and trying to get clients in broadband space. Premier is a supplier of Antrix. An article from livemint shared by another member on this thread has details about this. http://bit.ly/2N4Srst

ISRO is paying attention to branding and spreading awareness about its operations to the public, and seems to have a lot planned for the future. http://bit.ly/2PXfHaC

While direct-to-home TV is losing demand (which was the main source of satellite launching in the private space business) broadband internet is the next area of growth. Data exchanged is expected to increase from 1 trillion GB in 2016 to 2 trillion GB in 2020. (again from the article shared by another member on this thread). They mentioned wishing to increase the satellites launched per year from 4-5 in 2016 to 18 in 2021.

The bearishness of the market regarding the business from coal and cement seems to be irrational (personal opinion). Coal demand isn’t going to go down significantly in the matter of 1/2/3 years. It should go down eventually but slowly. Until then they will still need explosives for mining.

The defence + space business seems to be a huge growth opportunity for Premier given the competetive positioning of the company in the industry as well as higher margin businesses. The competitors and Keltech Energies and Solar, and Premier managmenet mentioned in a conference call that they haven’t even heard of Keltech (seemed odd and worth pointing out). Regarding costs, Premier has lower raw material costs than competitors, but higher employee costs. Operating margins of both Solar and Keltech are better mainly due to a much lower employee expense as compared to Premier. The raw material cost is mainly towards ammonium nitrate, which being a commodity product, might suggest that Premier is doing a better job managing costs in RM and spending more on people.

Premier has recently done a ₹150 Cr capex in setting up a plant in Telangana, obtaining funds via QIP and promoter funds, when the net worth is not even half of that. With ISRO’s plans to increase space operations, private players getting more interested in space each passing year, MOUs that Premier has with international defence agencies/govt organisations, and the recent licenses obtained by Premier - it seems that there is a huge potential for growth especially in the defence and space industry. The management seems to believe so since they purchased warrants at ₹ 408/share.

Revenue contribution from defence has increased in the last few years. Even if the commercial explosives business continues to grow at less than 15% (Premier’s last 10 years’ revenue growth rate), the defence business could compensate for that easily, and then some.

At the EV of ~₹250 Cr, assuming a 15% growth rate in revenue and a PE multiple of 15, the stock should to be fairly valued at ~₹215/share. I’ve assumed no increase in net margins of 3%, but also hoping for no more capex in the foreseeable future. Any improvement in margins could increase the fair value by a lot.

At what seems a fair price right now, we’re getting a business that is competetively well positioned in its industry, and will grow decently in the coal and defense sector. The solid propellants used in rockets could at least double in the next 3 years due to increased spending by private broadband companies and ISRO.

The company is making great strides in defense sector, and now defense sector is contributing meaningfully to the financials of the company. Recent developments reported by the management is as follows:-

(i) The company manufactures solid propellants for tactical missiles (Astra, Akash and LRSAM / MRSAM) strategic missiles (Agni) and Pinaka rocket.

(ii) Entered in Indian Space programme as approved supplier of PSOM-XL Motor for use in Polar Satellite Launch Vehicle(PSLV) to ISRO.

(iii) Only domestic manufacturer supplying countermeasures like Chaffs and Flares to

Indian defence.

(iv)Undertaking Operation & Maintenance services for solid propellant plants of ISRO at SHAR, Sriharikota and DRDO at ASL, Jagdalpur.

(v) DRDO successfully flight tested its state-of-the-art Quick Reaction Surface-to-Air Missile (QRSAM). Solid propellant used in the missile was in-house developed, manufactured and supplied to DRDO. Sole Supplier of Solid Propellant to DRDO for QRSAM

(vi) Indian Air Force successfully test-fired Astra Missile from Sukhoi-30 jet; the company developed and supplied the Propellant for the said missile.

(vii) Recently the company exported a few defence consignments.

The company has reported current order book of around 400 crores- and out of which 38% are defence orders, and 43% are service orders.

Though industrial explosives are still a major item in topline, the company has successfully transitioned into defence space. The company offers an investment opportunity as moat is quite high in defence space, margins are better in defence and India is trying to become a defence player.

The company has come out with real bad result; resulting into almost 20% fall in the stock prices. Nevertheless, a few good points are there in the investor presentation.

Order book at around 480 crores [2 times annual revenue] is highest in history. 49% of the order book is from defense sector and 34% from services sector. RDX/HMX export order to turkey worth 75 crores is to be executed in next 5 months. It gives some visibility in the topline going forward. Industrial explosive segment is not doing well. Only the services segment has shown some improvement in topline. Promoters holding is continuously increasing, though marginally. HNI holding is also increasing.

The investor presentation looks good, but when will it be delivered?Investor Presentation- Q3, 2020.pdf (2.6 MB)

These are obviously testing orders & rest will follow as it will go through gestation for trial on ground, as the missiles are carrying forward as well PSLV the orders to be followed very soon, also the margin guidance leading the stock, as a Tier 2 supplier their margins will be much ahead than Tier 1, also the biggest moat is gestation, as related to defense so change of vendor is not going to be easy thus creates a huge moat automatically,

Brief Profile:

Premier Explosives Ltd was founded in 1980, by Dr. A.N. Gupta, a Gold Medalist in Mining Engineering and a first-generation founder.

The business has 2 major divisions:

Detonator, cartridge explosives, detonator fuse, Non-Mining - Cloud harvesting, Riot Control devices; used in Civil applications

Propellant, Pyros, Explosives, rocket motors- Defense and Space

Milestones

1st in India to manufacture Explosives and Detonating fuse with indigenous technology.

1st in the world to produce Safer and Greener NHN detonators on commercial scale.

1st Private Company to manufacture Solid Propellants to India’s missile programs.

The solid propellants used in renowned Indian defense missiles like Akash, Astra, LRSAM, etc. PEL has seven modern production facilities spread across Telangana, Madhya Pradesh, Maharashtra, and Tamil Nadu. Its products are used in the mining, cement, infrastructure, defense, and aerospace industries. The company has employee strength of over 800 out of which 100 are engineers and & scientists.

Defense and Aerospace Explosives [growing cagr@5.3%]

The future prospect of Indian explosive industry looks brighter since government is pushing procuring defense items from domestic suppliers only under ‘Atmanirbhar Bharat’. Central government earmarked Rs 5.94 lac crore in the budget (i.e. 13.18% of total budget) to meet India’s defense requirements.

We have seen volatility in the margins in 2019-2020 and 2020-2021, however post that the company has witnessing an improvement in the order book and margins. In Feb’23 all defense stocks are in a limelight due to filthy allocation by Central Government in Federal Budget.

Triggers/ Future Plan:

The company has a current order book of Rs 1,108cr (i.e. 5.48x) as on Jul’23; which has to be executed in next 18 months. As per recent con-call, the company is expecting to report a minimum topline of Rs 500cr in the current fiscal. [Strong revenue visibility]

PEL acquired the majority of orders worth Rs 725cr during the H1CY23 period, indicating that many more opportunities in the remaining 3 quarters of FY23

The company is executing a greenfield expansion in Katepally for Solid Propellant Plant. This will enable Company to manufacture Solid Propellant of larger size for ISRO & DRDO. The management is actively working towards expanding its product portfolio for warheads, rocket motor hardware, thermal insulations, and more.

Now, as per the current PE of 91+ the stock prima facie looks expensive. However, considering the large order book we can expecting a significant improvement in financial metrics of the company since operating leverage will start kick in from Q2 onwards.

Going forward; we have to closely track quarterly revenue and profit figures to make sure the company is delivering well on the projects.

Warning: The stock has already rallied 170% in last 2 months. Disclaimer: Biased/ Invested from lower levels…No transactions since last 60 days. No buy/sell recommendation by any means.

90% of it is defence. Domestic is 88% and export is 12%

Order inflow for YTD FY 24 is at 632 crore. Includes orders from BDL, L&T and MoD (IAF), IAI to be executed over the next 9-18 months.

Will be maintaining 1000 cr order book going forward too

Confident of executing these from present capacity, no need for any fresh capex as on date.

Impact of Geo political issues –

Shipment Deliveries to Israel impacted due to Red Sea crisis. However conditions have improved of late. Expecting delivery to completed in Feb.

Planning to export more by air currently than by sea, to counter the issue. All shortfall of Q3 will be made up in Q4. Have not lost any orders in Q3. No issues on pricing front.

Working on other requirements from Israel and next orders likely to come up by Q1 FY 25

Lower margins- Margins impacted owing to delay in defence orders

Margin dependency on product mix. Product mix in defence keeps on changing.

Expect to maintain 18 to 20% margin.

26 to 28% margin for defence orders – guidance remains intact.

Gross margin has improved sequentially.

Exports – currently forms 12% of order book

Some more export orders are in pipeline… Have not lost any orders

Adding mines, ammunition, RDX in the product portfolio – exporting these products

Receiving queries from Europe too.

Chaffs and flares order

Chaffs and flares order which was to be started in Feb 24 is now delayed to Mar 24 (subject to approvals from MoD)

Chaffs and flares – Order cycle not predictable. Next order of 300 to 400 crore – RFP may come up by either by end of this calendar year.

Entered into manufacturing of mines and ammunition. Production of Nipun mines has started and pre-dispatch likely to start in Q1 FY 25

More on Nipun mines here

Approx 270-280 cr guidance for FY 24. Revenue likely to be approx. around 600 cr in FY 25

Space opportunities

Already producing strap-on motors for PSLV

Expected to be 400 cr annual opportunity in next 4 to 5 years

Qualified for manufacturing of rocket propellants mark I and II. Some other companies are involved currently. If there are opportunities in future, capable of taking it up.

2 Things to keep in mind with defence adjacent companies.

Order Delay/Cancellation happens routinely. Confirmed Orders are just that. Only Delivery and acceptance by end user are a reality.

Be ready for Long WC / delayed payments.

Apart from this company seems to be pursuing multiple opportunities across adjacent spaces. Execution will be key. CP seems overextended and can be range bound and even fall with broader markets.