excellent results 8e94e590-c3cc-4fa8-87d9-19c8208091bc.pdf (bseindia.com)

When I look at the PAT and compare with the year before, we have profit coming in from:

- Increase in Other income

- Positive impact due to Changes in inventories

- Reduction in “other expenses”

Revenue has declined QoQ and YoY.

@HIMSHAH, am curious to know what other factors make this as excellent result. I understand that textile went through a rough phase and it is recovery phase now. Is the result excellent because the expectation was far worse?

Disc: tracking

3 Likes

Attended AGM today virtually. Find enclosed my quick note for Premco AGM.

Current capacity utilisation is 70-80% for Woven elastic and 50% for Knitted elastic. FY23 decline in India was due to lower demand in domestic market while Vietnam performance was adversly affected due to lower demand from USA which is main market for export in Vietnam capacity.

The company added 10 new customer, 6 in domestic market and 4 in Export market. FY24, the company expect 10-15% growth

New plant in Umargaon is expected to commence production from FY25. Expect total turnover of Rs 50 Cr at optimum capacity utilisation, on total capex of Rs 18 Cr. In First year of operation expect turnover of 10-15 Cr.

Trying to add new customer from Europe market, which would assist in long term growth propsect of the company.

Vietnam cost of production is lower due to lower Power cost and income tax as compared with Indian market.

Audit fees, there was no major jump. FY22 Taxation fees was not included in Audit fees which has been reclassify which show in major jump in FY23.

The company has no plan to list on NSE in short term.

Top 5 cusomer account for 60% of revenue.

The company paid Rs 1.39 Cr to minority partner in Vietnam (actual investment by selling investor was Rs 1.25 Cr)

The company taken note of investors about excess cash on balance and would increase dividend payout/ buyback of equity share future.

While the shareholder attempted to ask where pointed question, the management continue to remain reserved answering question in my view. They are not very open about their future growth plan. In fact critical question about rationalising production to two new plant vis current manufacturing at 5 location (including Mumbai/Palghar) remained unanswered. Overall, get feeling that management /promoter are happy with status quo and it would take some more time for extenal/internal factors to move management out of their confort zone. Till that time, company would continue to run in auto pilot mode with no major growth in my view.

Disclsoure: Among my Top 15 investment due to higher dividend yield and strategic geography for capacities in India and Vietnam. My view may be positively biased due to my investment. I may exit/increase my allocation in the company without informing the forum. I am not SEBI registered investment advisor. I am not recommeding any investment action in company.

14 Likes

i think for listing on nse minimum capital must be 10 cr . so its not possible for them. atleast they can split the shares to 2 rs so liquidity increases.

1 Like

Its very interesting example…

i am tracking premco since 6 -7 years now, Its a sweet small little angel ![]()

Why this 100 cr annual sales was splited between 5 wide spread locations…

my internal feeling says it will rewards share holders sooner or later but at same time they are very lethargic , why they r not taking any aggressive steps to atleast reach 100% capacity utilization. what 50% utilisation “Halwa he kya”.

Disc. planning to take some position

1 Like

They can never run on 100% capacity utilisation. If I remember correctly once in agm I had asked them when it was not held virtual. They had said that when there is design change or some changes in products order they need to stop the machine and they need few days to restart production on that machine so that days and capacity wasted.

Any one having technical knowledge of textile can guide.

1 Like

Hello everyone,

I have been following this company since 2017, but never bought it till date. But, after going through the full thread and looking at current dividend yield and other valuation metrics I feel that I should buy it now. But I have a very basic question about the ongoing CAPEX in Gujarat.

Premco did the sales of 66Cr in 2014 and in 2023 it did 70Cr, meanwhile the Vietnam facility came on stream, which expanded the existing capacity by 50%. And now they have announced the new capacity which could do the sales of 50Cr at peak utilisation. Why do they need the new capacity if the existing capacity is not utilised fully?

2 Likes

But, they have already increased the capacity in Vietnam and I could not see its impact on sales. I already mentioned in earlier post that prem I had clocked same level of sales even after 8-9 years. Then why they need to increase the capacity or the volumes have increased but realisations have come down that much?

Premco, poor results continues in the series for the company. Dividend declared for quarter also declined to Rs 2 per share during Q3FY24 as against Rs 6 per share declared in Q3FY23. The decline in dividend declared is major concern for me.

During the quarter. while consolidated profit declined by 53% yoy, standalone profit declined by more than 61%. So, India business continue to adversely affected. Even depreciation charge for quarter is almost same last year in standalone business, hence assume that company has not commericalised new plant. When the new capacity would be operational, the company performance is expected to remain lower than normal level of profitability due negative operating leverage.

Overall, no positive take away from the results in my view. Proftiablity in Vietnam and India under pressure, No update on capex commencement, Major drop in Dividend, No attempt from management for NSE listing. Critically evaluating my investment in company.

Disclosure: My view may be biased due to my investment in the company. I may increase/decrease/exit my holding in the company without informing forum. I am not SEBI registered advisor. I am not recommening any investment action in the company. Reader shall do his/her own due diligence/consult financial advisor before making any investment decision.

7 Likes

seems company has no strategy… expansion without sales. margins coming down… then why increase capacity?? It is anyway a very fragmented market with many small players and low margins…

only 2 years of COVID sales and profits were high - maybe due to supply crunch from other countries…

should go back to pre-COVID prices.

2 Likes

ordinary results - sales, profits flat… i think this is steady state of company. PE is above historical average…

stock will stagnate or even come down… highly competitive industry.

www.bseindia.com/xml-data/corpfiling/AttachLive/eb92f851-ec27-49ec-b97a-e385ae012b88.pdf

Since standalone are inferior in profitability as compared with Consolidated, I infer that Vietnam operations did well during the quarter. Also, around Rs 1 Cr for FY24 has been capitalised as Capital WIP for Umargao plant as per notes. Assuming that plant would be operational from FY25, we shall see further increase in fixed overhead (Depreciation+ Increased expenditure of new plant), which would also likely to adversely impact company performance in domestic market. In order to stock to see major movement, it would need major improvement in domestic market, stable Vietnam market and good capital allocation decision like Buyback and listing of stock on NSE. For last decade the company has delivered on any of these. Hence, not expecting any magical swing in the stock price.

Discl: My view may biased due to my holding. I am not SEBI registered advisor. Not suggesting any investment action. I may exit/change my holding without informing forum.

4 Likes

will they be able to show improvement in domestic market. It seems to be struggling for many years.

it is a highly unorganized and competitive industry - if they could have increased sales in domestic market they would have already done it by now… given their vintage in the industry.

1 Like

Have been trying to understand the company, assuming garments industry is doing well and all inner wear companies doing well. But somehow Premco is not doing well both on sales and margins(only 2021-22 margins were good).

Seems management issue… decided against investing…

Also, was there a need for a new plant when sales are stagnant. It seems their strategy is not right. Surely profitability will be hit. Return ratios are also not great.

PE multiple of 15 for such companies is quite high. its 5 year average PE is 11.

It could be a good investment at Rs. 300.

As expected flat sales with lower margins… margins will be under pressure and go down to 10 to 12%. Competition is very high in this business…

1 Like

I attended Premco FY24 AGM. Find enclosed my notes. Please note that there may be communication error from my side while taking down notes.

New Plant: Umbergaon plant Phase I commenced during the years. By end of CY2025, the plant would be fully operational. It would service Indian and export market. Peak sales can be achieved from the plant would be around Rs 50 Cr. New plant is expected to contribute around Rs 10 Cr sales during FY25.

Capacity utilisation: The peak utilisation company can operate is around 85-90%. In FY24, various plant (excluding Umbergaon) are around 70-75%. So for next 2-3 years, can service the market Existing and Umbergaon Capacity.

New Market/ Client: The company is at advance stage of discussion with European Client. Current inspection and approval process is at advance stage. At appropriate stage they would inform shareholders. They are present in North America/South America/Africa market beside India and Vietnam, Have limited presence in European market which intend to penetrate shortly. The large professional fees spent in forex is in order to get right skillset to support and get new clients. Also, company supplies almost all major players in Indian market, like Lux, Dollar, Rupa and Amul.

FY25

Forecast: The company intends FY25 sales to grow by 10%.Also, expect to manage margin at around 17% EBITDA. They are trying cost rationalisation efforts in all the plant which would result in saving of around 2%. That shall assist company to manage EBITDA margin in case cost escalate. With Umbergaon plant, the company can reach peak sales of Rs 120-140 Cr.

New product line: The company has new product like Leap tag, Recycled yarn-based elastic, Micro elastic. These products would continue to drive growth in revenue.

Competitors: Spica, Elastica, Bena Regal Tape and Kohinoor (not sure of name/spelling) are main competitor to the company

Share buyback: Limited time is available to complete formalities and hence would not be possible. However, may look at rewarding shareholder with dividend.

No plan to list on NSE.

My view

The management appear to be very conservative and performance is likely to see moderate growth despite great business and relationship. It has still not reached is peak valuation of Rs 900+, Sales and Profit achieved in FY22. So investor shall be patient to hold this investment in my view. While no clarity on growth in medium term, downside is also limited in my view due to dividend yield of 3% and free cashflow generating business model. Despite large capex (almost 40% of gross block), the company is very comfortable in in liquidity position with HDFC Bank (among the conservative banks) as lender. There are my current view and can change any time.

Disclosure: The company is my core equity holding with around 3.25% allocation. My view may be positively biased due to my investment. I may increase/decrease/exit from the company without informing the forum. I am not SEBI registered advisor. I am not suggesting any investment action.

9 Likes

If capacity utilisation was only 75% what was the need for new plant at Umbergaon - additional 10cr sales could be easily done from existing plants.

This business is very competitive and has low margins. Margins will surely go down to 10% (pre Covid levels). COVID they must have got additional orders due to restricted supply from competitors.

Performance of the company is more likely to go down… not up.

1 Like

As per managment, they can use practically capacity at level of 85% given the number of batches would reduce the operating time for change in new production order. Hence, at 75% they can increase sales by 10/75, i.e. 13% from the current capacity. However, there might be some new products as well which may need new machinery. Hence, in my view, new capacity expansion is much needed for the company for future growth. One shall not wait for 13% growth, which can happen in 3-6 months time and end up with siuation that there is demand but no capacity to fulfil that demand. While optimum utilisation and just in time improve productivity and margin, at time, particularly given the current geopolitical situation, some buffer for supply shocks are good in my opinion.

Secondly, on margin, your observation that margin at 10%, is not true business margin.

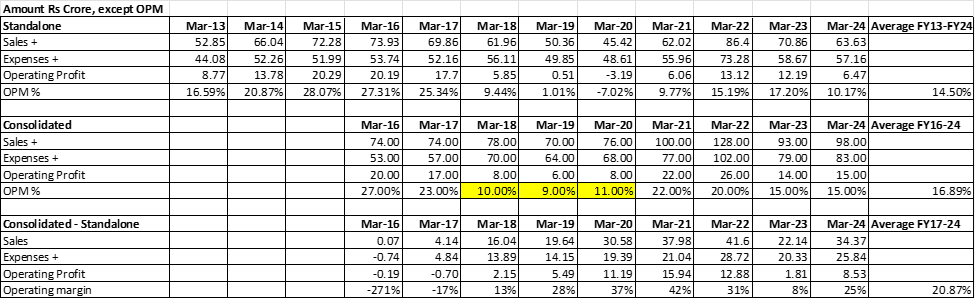

Find enclsoed sales, operating profit and operating margin of Premco Standalone and Consolidated financial over past 10 years sourced from screener.

Your obersvation is correct that during FY18-FY20 period, Consolidated operating margin was 9-11%. However, that was period when Vietnam operation was about to stabilise. If one look at FY16-FY24 period, than consolidated maring are around ~17% which is very good in my understanding.

Further, in my understanding, while the company has not grown signficantly during last few years, they have also not compromised on margin to enhance sales. I find that trait being long term value accretive. Again, this is my subjective evaluation which may biased and wrong.

Disclosure: Same as last post.

7 Likes