how good results? Both revenue and profits are down. are they running at full capacity?

Their was substantial wave of covid in Vietnam from June ending to mid October( one can google it) Sales and profit both is down in Vietnam , wich could be the reason.

They have increased interim from last year

3 Likes

That’s true…

They sustained margins and sales …

But needs to see how market reacts on that…

Disc. I own some shares

2 Likes

- Are they running on full capacity utilization?

- why arent they doing any expansion when they have so much of cash (good thing is they are regarding shareholder with good dividend.)

1 Like

3rd interim dividend

2 Likes

Excellent results as well as 50. % 3rd interim div declared https://www.bseindia.com/xml-data/corpfiling/AttachLive/2854761a-c943-4031-9790-7cf3a7369eca.pdf

2 Likes

Yes indeed a decent results. Net profit is lower on YOY mainly on account of higher taxes in current qtr in comparison with Drc’20.

Indian entity did better than veitnaam subsidiary.

Dividend is increasing every qtr, highest didvidend payout in history by premco.

I think there is change in management mindset and they are showcasing investor friendly behavior.

3 Likes

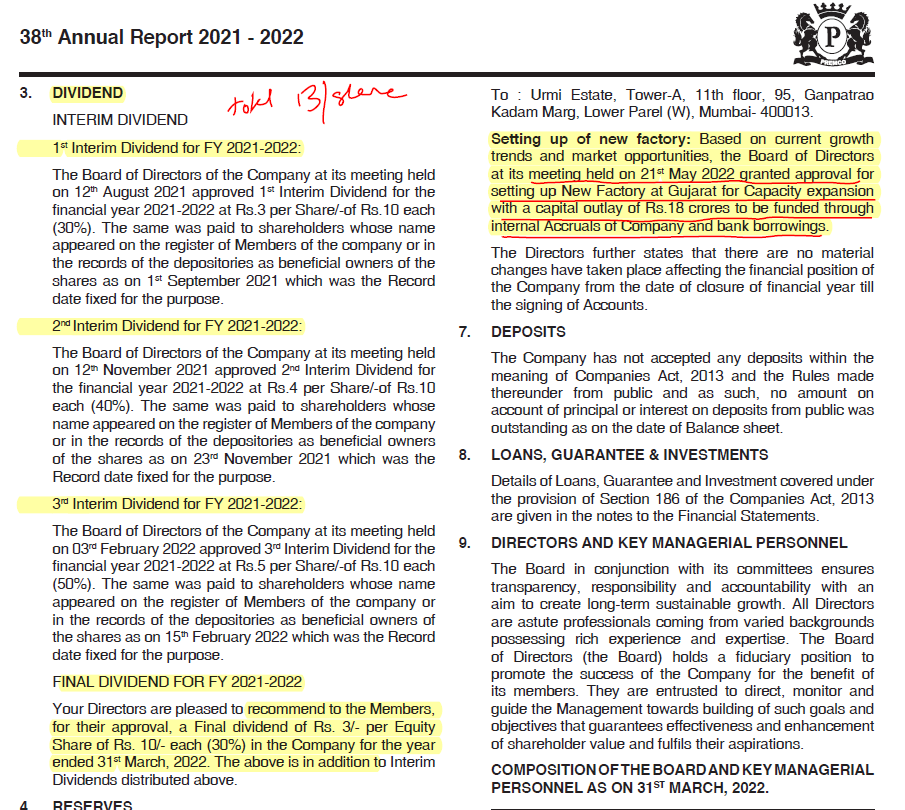

Premco Global has given very disappointing numbers in Q4, which was very surprising as it has been giving superlative numbers in last few qtrs. What is more surprising, the management has not given any reasons for sharp drop in revenue, both in standalone as well as consolidated basis. As the textile segment is doing well this was a surprise. Company is going for expansion due to good product demand. Good final dividend of Rs 3 declared, taking total dividend to 150% in this year. So there is a lot of confusion in absence of management commentary. Any member tracking the Company can throw some light on it ?

1 Like

they are very conservative in giving future outllok as well as details. but i dont mind one or two quarter sales is down as if u see sales is down in vietnam , and they supply to hanes and others in vietnam . many times they have orders but delivery is at later date as per requirement of hanes. and still it has shown 50 rs eps so its avaialble at only 6 PE. they must have confidence in demand else why they will go for another factory, they can easily use vietnam facility. also they dont make garments or final products , they are like OEM making elastic for innerware manufacturere like hanes and all big MNC . so inventory management plays crucial part in their business.

if by chance it comes down i wont mind adding further. if by chance it comes down around 200 ( seeing market anything is possible) its good investment

my views may be biased as holding from lower level

5 Likes

Was going through the FY22 annual report. Good that they are again looking for expansion. Given the cash flows and surplus perhaps they could be more aggressive.

Perhaps one of the rare small/micro cap company to be paid dividends every quarter.

Disc: Invested in family and client acs. Views may change.

20 Likes

Total paid 15 rs dividend for this year. And they sound more optimistic if one goes thru AR . They were waiting for Vietnam plant to stabilise and putting up new plant is good sign. Main IS 3.3 cr capital, 293 rs book value , 50 rs EPS and honest management.

DISC, INVESTED

7 Likes

Ok results as premco Vietnam was affected and no profit from their. As per note 7 in results

And next quarter will be as usual usiness

1 Like

While results are below my expectation due to major issue in Vietnam has highlighted by you (Note 7), one more positive is step to make Vietnam operations fully owned subsidiary from currently JV. We need to understand what are commecial to give exit to the JV partner. However, prima facie a positive factor in my view.

Discl: Added as part of Settelite portfolio during Q1FY23. Last purchase was on 4 August 2022. Not a SEBI Registered advisor/ Not recommeding any investment actions.

4 Likes

This is the reason

3) Accorded approval to Subsidiary Company ie Premco Global Vietnam Co Ltd (PGVCL) to repay the Capital Contribution of its deceased shareholder at a mutually agreed price and make necessary amendments in its Charter & Investment License.This will transform the type of enterprise of PGVCL from Limited Liablity Company with two members to one member limited liability Company by way of Capital Reduction which would result in Subsidiary Company being converted into Wholly Owned Subsidiary Company.

If we just take out Indian operation then Vietnam had only sales of 6 cr this quarter and nil profits. They have kept stock with them and it’s part of business to maintain relation with MNC

4 Likes

Anyone has attended today’s premco AGM then please update as I couldn’t due to some reason.

My notes from Premco Virtual AGM from Q&A, held on 18 August 2022.

New Expansion:

The company intend to spent Rs 14 Cr on New Plant in Gujarat. In October 2022 they expect to finalise land. The installation and commencement of machinery would begin after land acquisition. Management expects around 12-18 months from land acquisition for commencement of plant which shall be in phased manner. They expect Peak revenue of around Rs 50 Cr from new facility. The new facility would address demand from domestic and export market. The capex would be funded by debt (taken at concessional interest rate Textile Upgradation Fund loan) and internal accrual, in order to get benefit of lower interest cost.

Q1FY23 performance:

The conflict between Russia/Ukraine and also China related geographical development impacted performance of company, particularly in Vietnam. Polyester and Nylon, key input for company also seen spurt in price due to higher crude price. While the company was attempting to transfer the increase to customer, it would take some time to pass on full hike to customers. The management expect to meet top line of FY22 in FY23 conservatively and aim to report higher top line, despite adverse Q1FY23.

Vietnam operations:

Profit Margin in Vietnam are high due to lower income tax rate. Income tax rate in Vietnam is around 8.5%. Currently, Vietnam plant is operating at around 70%, (Peak Capacity utilisation can be achieved is around 86%). In FY22, they reported sales of Rs 54 Cr and anticipate that maximum sales can achieve from this facility at around Rs 60 Cr. Once supply chain issue gets normalised, they may explore further expansion in Vietnam.

Other Points

- Do not intend to list shares in NSE in short term

- Would explore over suggestion of Share Buyback given the high cash balance

- India capacity can run at maximum level of 86%, as against current utilisation of 70%. Indian production is supplied in domestic as well as export market (US/EU/Bangladesh). In India, Lux, Dollar, Rupa and Van Heusen are the main customer for the company.

- Current order book is around 30 days, as against normal level of 60-90 days. Once the supply side issue are resolved, management expect order book to resume to normal level.

- Contingent liability increase in FY2022 was due to wrong assessment order by IT officer. The officer did not account for RM cost while calculating profit. The company has already provided necessary information to IT and expect same to be resolved without major tax liability at company end.

- Currently market share of company is less than 5% of global demand.

- 80% of the company revenue come from long term contract while balance 20% from spot business.

- Spica (missed other 2-3 names also mentioned) are competitor to the company in India.

Note: There may be error of miscommunication at my side while taking notes in the AGM meeting. Please note that I have tracking position of around 1% of equity portfolio in the company which I have invested in last 90 days. My view may be biased due to my holding. I am not SEBI registered investment advisor. I am not recommending any investment decision in the company. Investor shall do their own due diligence before taking any investment decision.

15 Likes

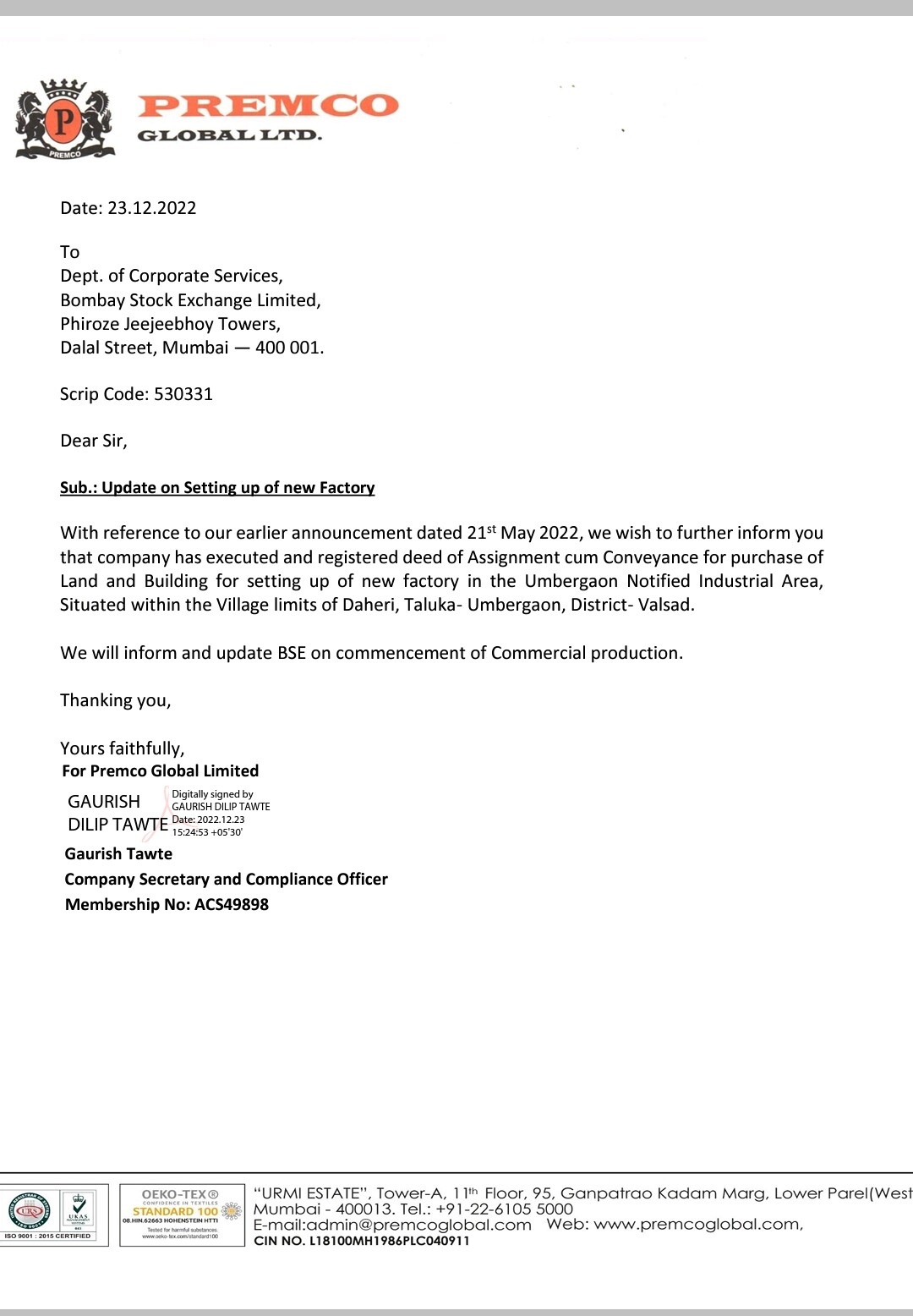

Update on new factory.

Premco is now available at mcap of 100 crores.

The current valuations seem to be quite attractive given that the company has net cash of 31 crores and also coming up with new capacities. Also, quality of management is also good. Only concern is liquidity, the stock is highly illiquid.

Disclaimer: Invested and biased

9 Likes

Premco Q3FY23 results announced.

The company’s operation in India (as indicated by Standalone numbers) showing stability in profitability (YOY), although sales continue to remain lower than last year.

Consolidated number have gained from exceptional income booking from Vietnam operation. However, at PBIT Level, Vietnam contributed negatively Rs 1.2 Cr Loss (Difference between Standalone PBIT for Q3FY23 over Consolidated PBIT before exceptional items for Q3FY23). During Q3FY22, the same difference was Positive Rs 2.3 Cr. So Vietnam operations continue remain concern during Q3FY23 as comapred with Last year.

However, excellent improvement in Indian operation as compared Q2FY23. Vietnam operation also shown sequential improvement in sales from Rs 2 Cr in Q2FY23 to Rs 5 Cr in Q3FY23. So, trends are showing improvement and I am hopeful that with China re-opening from Covid, even Vietnam operations shall show improvement during next 2-3 quarters.

My optimism is also supported by highest ever quarterly dividend of Rs 6 per quarter. This almost 45% payout of quarterly profit. If the company continue to maintain rate of dividend, at current price of Rs 320, Rs 24 annualised dividend give dividend yield of 8%, which is very good in my understanding.

Discl: Holding tracking position (1.2% of my portfolio). Not a SEBI registered advisor. Not suggesting any investment action for reader. I have been wrong multiple time in past. I may change my investment holding (including exiting from the company), without informing the forum members.

8 Likes

Very well put up @dd1474 ![]()

Despite subdued last one year, on TTM basis it still trades at around 6 on EV/Ebitda.

Haven’t came across any other microcaps where cash flows are as good as premco.

2 Likes

Was looking at related party transactions. Noticed this.

It is not repayment of loan. So, puzzled on what this could be and how this is almost twice that of remuneration of 63.46 lakhs…

Disc: Tracking

1 Like