(Declaration: I am terrible in writing long report type stuff and never done it after college days! But, finding that the company is not having a discussion thread so starting one…… Critics and views invited to make the discussion better. I have many data point and rationale in the head…. Your questions can help me to bring that out cogently. So please contribute profusely…… )

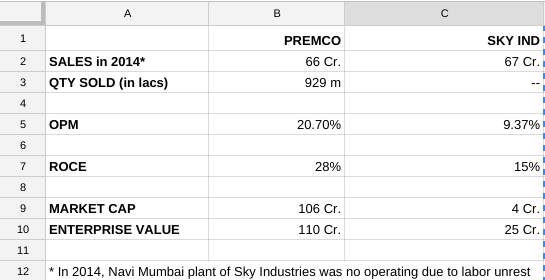

Premco Global is a Rs. 66 Cr company manufacturing Narrow Fabric. The product show case is available here http://www.premcoglobal.com/showcase.html

Narrow fabric includes elastic and non – elastic ribbons, straps, bands, packing tapes used in inner wear, packaging, sports, medical, furnishing and automotive industry.

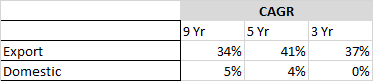

Sales and profit have grown for the company at 17% and 44% CAGR in last 5 years (refer screener data). ROCE as per my calculation is around 40% last year. Company is virtually debt free, don’t need much cap-ex till productivity is optimized. 85% of the product is exported.

Indian inner wear industry Is 17K Cr in 2014, going to be Rs. 32K Cr in ’18 and 59K Cr in ’23; 60% is market for women growing at 15% and 40% is market for men growing at 9% (as per estimate in Page industries AR 2014).

World market is growing slowly and many paid reports are available where the total market size is pegged to be anywhere between US$ 25 billion to 35 billion and growing about 3% to 5% range.

I am unable to come across name of any large global player in this field and seems industry is fragmented with too many small players. Some names are : Bowmer Bond, Kikuchi Narrow Fabric, Landwell Corp etc and in India Shivam Narrow fabric claims to be the largest player (any information about this company is welcome value addition). But I know of umpteen very small scale elastic manufacturer in Delhi and Kolkata.

Premco claims to supply to some marquee brands (http://www.premcoglobal.com/credentials.html) however, more realistic would be to assume they supply to tier one or tier two level of vendors to these large behemoths. Their top 3 shipments destinations were to …

QST Industries De Mexico; Elastica Surqui SA (Costa Rica); Telas Elasticas (Mexico) — These companies are the intermediaries for the final buyer like Hanesbrand, Fruit of the Loom, Limited Brands Inc etc.

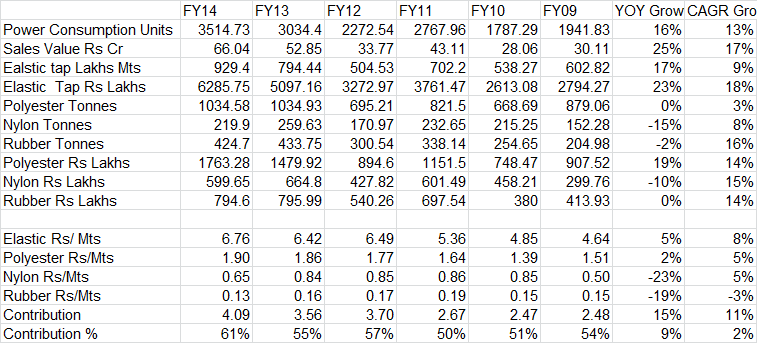

Main raw materials are Polyester, Nylon and Rubber and all are produced locally and RM constitute 50% of sales. Out of these Polyester is 25% of the total Sales.

Last year they sold 929 Lakh Meter of Narrow Fabric at average realization of Rs. 7.5 /- meter. An pdf file is enclosed which gives a rough estimate of setting up a basic narrow elastic business in SME sector. The “bazar” price of per meter of narrow fabric appears to be Rs. 6.5/- per meter.

The company I found worth investigating due to high profit growth, strong return ratios, company’s export focus targeting quality customer (so can assume quality better than rest) and increasing growth of premium category inner ware in India and other places compared to the overall growth.

Elastic is one of the most critical part of an inner ware and it constitute less than 5% of the sell price of an inner ware (assuming average sell price 200 and average premium quality per meter is Rs. 8/-). I conjecture that like sanitary ware sector where shift from unorganized to organized sector has happened, a similar trend may be possible in this industry for premium and consistent quality requirement. Secondly, GST, at rate below 25% would surely help the organized sector.

Quality of accounts: Nothing abnormal. Seems to have over valued the finished goods inventory. If the closing stock is valued at average sale price for the year, then profit would be reduced by about Rs. 2 Cr for the year 2014.

Quality of Management: Unknown. They take very low salary but I am told that they own Beachfront Villa in Florida. Also, a non-promoter shareholder holding 6% plus share appears to be a relative of the promoters. Both these may be rumors and I can’t vouch for its veracity. But the company performance has surely started looking up since Lokesh Harjani took over management. They guided only about 20% growth in sales in 2015. Profit and cash is growing faster.

Questions please……

Disc. : Invested from a much lower level and less than 2% of portfolio.