I don’t agree. You have to understand that current hotel industry managements and thought process has been around for years and not easy to change. Thus their business model will take time to evolve. Also with already so many assets in traditional hotel buildings, how they think about capital allocation at a scale in setting up structures like praveg. Praveg started with eco tourism and thus offers them to pick venues which are very differentiated and execute them very efficiently with lowest cost. Think margins and op leverage once their desired count of resorts are operational. Market is giving such high PE for this reason. By the time this moat gets impacted, Praveg would have scaled enough domestically and in international markets as well because they have first mover advantage. In regards to connection with politicians / government, I would think it is naive to take investment decision based on this half truth or totally false facts (false because they are not proven in public domain). Hypothetically even if they are connected, as investors our focus should be to compound in a stock with sound business model and should there be any political connection, I won’t mind if it benefits my investment. There has been enough talk about connections of Reliance and Adani, most long term investors have done well in these stocks

Refer all company announcement on allotment of equity shares after Dec 2023 (Q3) and try to estimate EPS on dilution basis for Q4 and FY2024.

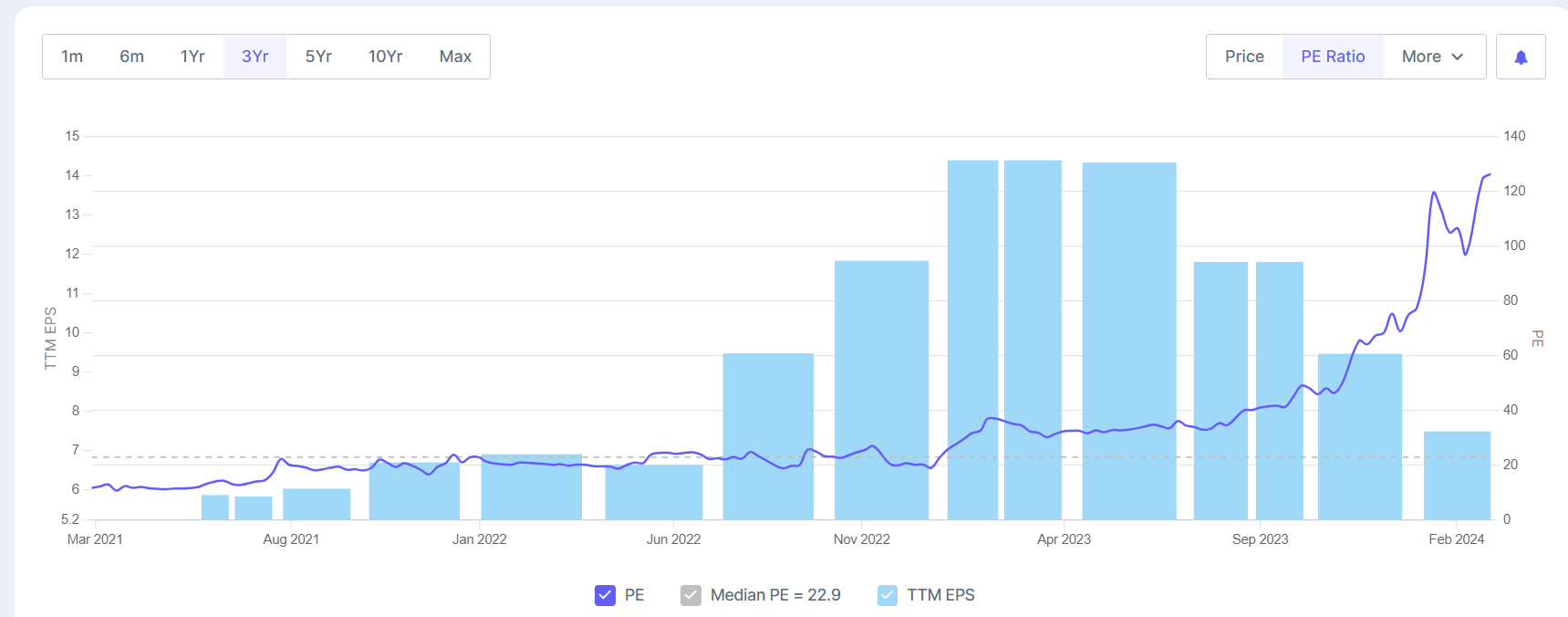

Expecting correction in share prices as it should align with mean PE ratio

Some random points-

- Praveg is going to add approx 10 resorts/year going forward.

- From next year all the new resorts will be funded by internal accruals only.

- On average 10 crores is needed to setup a new resort.

- All the resort assets, guests, staff are covered under full insurance.

- They use fireproof material to build the tents and keep fire preventing measures in place for any fire eventuality.

(Noted these from a private interview on value educator yt channel).

Can the ppl in the know please provide details with regards to the latest plan of QIP. I think last time @Niraj_Punjkaran provided this valuable info. Can you also pls let us know the source of your info ? Can individual investors participate in preferrential alottment.

Thank you very much. If I follow the SEBI guidelines on pricing, the price of preferred and warrants must at least be 900 which means company is raising around 200 cr. Does anybody have a clue whether dilution of equity upto such an extent is justified ?

Looks like they were unable to make new resorts operational with available funds, as per last Q con call, they should have got about 8 resorts operational as compared to only 1 as per the announcement. Further there is no news on their international expansion. One comfort is that good funds have participated and goldman sachs bought decent chunk around 850. Let’see. Disc: Invested

Concall Notes

Detailed dscn on redn in Ebitda…mgt conveyed that most resorts became operational in Q3/Q4 so realisations are yet to pick up…logical reasoning.

Eulogia. Expect strong Q3/4 marriage season, booked 70%, monthly RR 1.5 Cr but anl potn is 35 Cr

Headcount. From 150 to 1000 now on payroll. Incr in emp expdr

Depreciation Policy. 5% residual value, 95% charged off over 10 years

Avg Occupancy . 45-50% in PFY

Active Resorts . Mar 23 - one resort, Mar 24 - 12 resorts, likey by Mar 25 - 22 Resorts

Lakshwadeep . 5 resorts (incl water and adventure activity, 386 rooms, marriage and events), likley to be op - Nov, Constr commenced, Jun -Jul no work on site

Guidance. 300 Cr rev expectation, EBITDA 40% plus

Misc .

With new acqn, addl rev stream in advt will open up

Properties are getting better ratings from TRIPADVISOR

Share holding . Promo Hldg - 45.77%; FII - 7.95%; DII- 4.88% total - 58.6%

Disclosure. No holding.

Updates:

- Update the sheet for month of May.

- Expenses likely to be high going forward as well coz of ramping up of Lakshadweep Resorts.

- We will have better understanding by Q3 on the potential profit it can generate.

Most of the resorts are seasonal and impacted by weather. Having asset heavy structure, more direct manpower will increase cost to the books, which is round the year cost!. Seasonal resort with outsourcing model is more cost competitive and have higher margin as it offset seasonality.

Rapid growth of tents, without evaluating much about cost and profit model and learning from the past operational tents about hits and misses will provide more inputs for future tents opening but it seems Praveg is going very rapdily by dilutig equity and drastical reduction in EPS

The kind of valuation Praveg is getting does not leave any margin of safety.

Very poor result…

EPS is almost 50% down (YOY) !

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8ac59b98-bffc-4e26-af06-6266d3865e25.pdf

Praveg business model from Sep to Feb (6 months), so good revenue Quarter Q3 and Q2 and Q4, 70-75% as compared to Q3. If Q3 will be poor, at that point is the addressable!!!

Praveg’s Investors meet -

28 Aug - Kotak Insurance, SBI Insurance, Lucky Investments(Ashish Kacholia Sir), Goldman Sachs

29 Aug- JM AMC, LIC AMC, Monarch AIF

After Q1FY25concall, Institutional Investors showing interest in the co means co is going on right track.

Q1FY25 concall highlight-

- Top line target is 300cr(330% up YoY)

- Capex for FY25 is 175-200cr (150cr capex for lakshaweep)

- Operating hotels - 12 (619 rooms), in Q2FY24 they had 4 hotels (301 rooms only)

{2x in less then 1 year}

Monarch has initiated research on Praveg -

They have forcasted -

FY22A Sales, PAT & PAT Margin - 45cr, 12cr & 26%

FY23A Sales, PAT & PAT Margin - 84cr, 28cr & 33%

FY24A Sales, PAT & PAT Margin - 91cr, 13cr & 14%

FY25E Sales, PAT & PAT Margin - 223cr, 28cr & 13%

FY26E Sales, PAT & PAT Margin - 410cr, 87cr & 21%

FY27E Sales, PAT & PAT Margin - 500cr, 110cr & 22%

But, Company has given guidance for 300cr topline in FY25.

For me, FY25 sales - 300cr

FY26 sales - 420cr (+40%)

FY27 sales - 590cr (+40%)

40% - my own expectations.

PAT margin expectations - 25-26%

So, FY27 PAT - 150cr

Current Mcap - 2300cr

FY27 Forward P/E - 15.33

All projection number on excel sheet looks promising. But one need to be cautious more about weaknesses of the business when one is paying very high price to buy it ! -

Big red flag: Company business is highly depending on the government. Most of land lease deal is with government and change in government could have serious impact on this company!

Most of locations has seasonality and fixed cost is going to remain round the year for maintaining it. Company has increased more fixed cost (man power, etc.). Promoters are not focused on core business earlier they entered in TV business and now they entered in advertisement business, etc.

YES, all Equity Research Reports is based on projections & excel sheet

We can only wait for the results and hoping that management do WALK THE TALK.

Add on to above mentioned points, hotel industry is cyclical in nature,

A change in trend will drastically take away PAT

Any update on the company participating on Khumbu Mela?

Bookings for Lakshadweep are opening starting from December 15, fingers crossed

As per company vision statement FY28:

FY24: Rooms 680

No of rooms sold: 62592

Rooms occupied days at current: 92 days

Total Revenue including other income: 94.55 Cr

Per Room Tariff (2 days): Rs 15105/- , Average room per night : Rs 7500/-

Now apply to same math’s on FY28 (Refer slide 41 of Q1 presentation)

Estimated room sold 2500 X 92 days = 230,000

Assume no change on room tariff / without inflation adjustment = 15000/-

Total Revenue = Rs 345 Cr

PAT @ 15% = Rs 51.75 Cr

PAT @ 25 % = Rs 86.25 Cr

EPS @ PAT 15% = 51.75 / 2.58Cr shares = 20.04/- (Base case)

EPS @ PAT 25% = 51.75 / 2.58Cr shares = 33.40/- (Bull case)

Wait and watch Q2 result and management commentary on business!!