Generally Q3 is strong for PRAVEG…

" Its the name Praveg=Acceleration" ![]() (My two cents on the lighter side)

(My two cents on the lighter side)

1 Like

R a bhai, ho kya raha hai Praveg mai? ![]()

Its on steroid, as most of names are these days, praveg in particular seems to have been injected with higher doses in the form of news ! ![]()

Enjoy the ride.

D-Not invested.

1 Like

Praveg promoters definitely have some good connections, they also organized the G20 Summit.

Disclaimer: Invested 5% of my PF.

2 Likes

Couldn’t agree more…The ayodhya set up is also ultra spl and well timed…they have really thrown up a massive surprise on these 2 sites

These connections…how do we see them? Competitive advantage…or with caution (political patronage?..or…)

The entrance of Sage One was so well timed…now with two top MF (TATA and KOTAK) also on board, can one say that they have finally arrived on the big stg

Today HP govt has thrown open 12 eco tourism sites for bidding …all great locations…would be interesting to see if Praveg has any interest.

Now all sights on revenue uptick in Q3…if there is a bump up ( as expected)…that’ll be a kicker.

1 Like

Now praveg (P/E >100) have limited upside, if earnings miss the expectations, market will treat Praveg very badly.

Although the company is looking good but valuation shoot up alot.

Disc- Not invested but tracking.

1 Like

Also depends on how many orders they get in future alongwith if management can execute so many new tent city orders as things are scaling so fast.

Real test of management.

2 Likes

Thank you Debojit, for updating the sheet every month!!!

Basically, the real test of the management HOW successfully executed all tents / Properties under PP in H2-FY25. ![]()

FY24 is the year to ensure order and development!!!

2 Likes

Good detailed coverage

How much did it rally after announcing the merger ?

Observations:

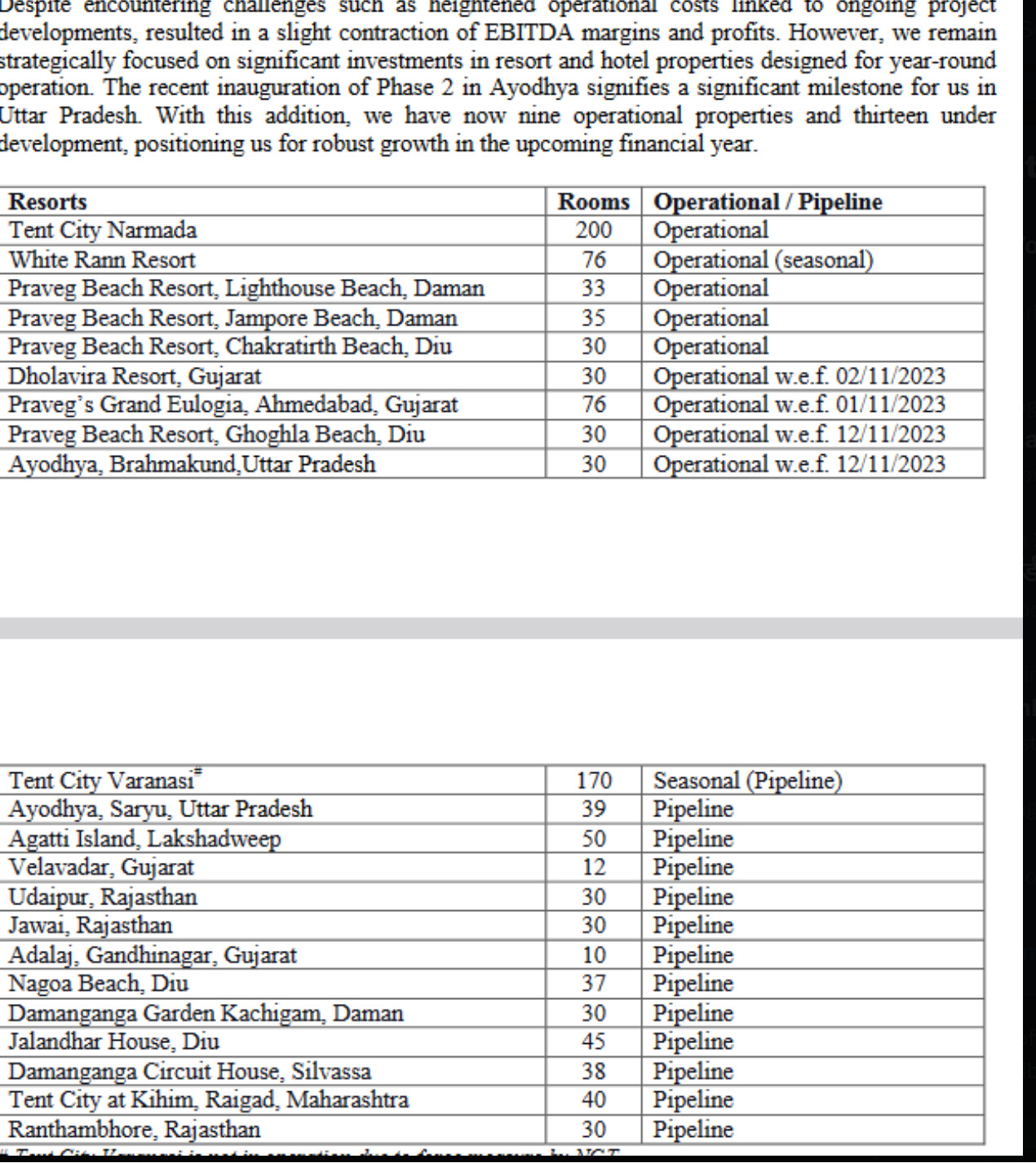

- Latest filing they mentioned 10 resorts are in operational, but as per my calculation 9 are operational (link) . Can someone confirm if I missed any?

- Hospitalities revenue for the quarter is Rs 2561 L

Rough Calculation: 579 rooms operational → per room revenue quarterly is Rs 4.42L → per day per room Rs 4915 - Hospitalities revenue growth YOY 123%.

As per the above almost 710 rooms are operational status; Out of which 336 have started operations after mid q3

Someone asked a very good question in concall. With 1000 rooms at 50% occupancy and 10k ARR the revenues would be 180 cr and not 300 cr. I hope the management does a reality check.

Risks:

- Its asset light model, with tourism flourishing, it won’t be surprised if we see other companies emerging with same model.

- It’s hard to justify the company at current valuation, even forward looking valuation seems to be high with the recent run up.

- Its cyclical industry, no one knows when it will reverse.

Advantage:

- Current Govt is trying to boost tourism a lot which gives a huge upside for the industry.

- With affluent class growing more, tourism likely to improve. Simple example can be of Lakshwadeep, the UT itself is getting better connectivity n improving. Goa thrives on tourism, so can Lakshwadeep in future.

2 Likes

management responded that there will me some resorts where ARR will be 25000 Rs, which will contribute to the growth + There will be income from event and exhibition as well… I think 300 Cr is doable given government thrust on increasing tourism sector

If we consider 300 Cr revenue , EBIDTA will be around 120 cr, Depreciation will be 15 Cr and PBT = 105 CR , and PAT will be around 75 CR

Current Market Cap is around 2160 , which translate of Forward PE of 28 which is reasonable

Considering technical , stock is forming base around 50 EMA. Market will look for results and another announcement regarding timely opening of resorts and new order wins.

Deviation from target will punish stock and if it seems that results are good then stock price can reach 1800 Rs (at PE of 60 of FY 25 earnings)

2 Likes

One should focus on EPS as they are doing lot of equity dilution. As I stated earlier, I think the moat of this company is relation with government / politics !! I don’t think there is any entry barrier for this business, if business is so lucrative, many brand hotel business might have entered in this tent business.

One should always keep enough margin of safety while buying such company.

Sage One entered keeping good margin of safety (at less than 500) (and reduce holding at peak valuation). But for retail investors, FOMO will hurt

Disc - Not invested

1 Like