Request @Debojit_Kangsa_Banik to kindly share the latest updated excel sheet.

1 Like

Updated till Aug 24 Resorts Detail - Google Sheets

One key notice while making the entry, the ARP for some of the tents have decreased if we compare between May24 & Aug24, which will definitely impact realization, have marked them as red

7 Likes

I am unable to open link of audio recording

Praveg Update.pdf (199.2 KB)

Can anyone have ? Please share

Download from here, it works.

1 Like

Why Praveg management is planning to stop quarterly con call with investors (as per latest con call)? Are they not ready to answer investors queries? In this Q2FY24 con-call management not having much more interest to give details asked by investors.

Why there is no rating agency report on company’s rating? I could not find rating agency’s detail report on its company rating.

Am I missing something?

4 Likes

Generally, Q2 and Partial Q3, no revenue generating Quarters and Number of Investors want to understand Revenue model

1 Like

Praveg Update.pdf (250.0 KB)

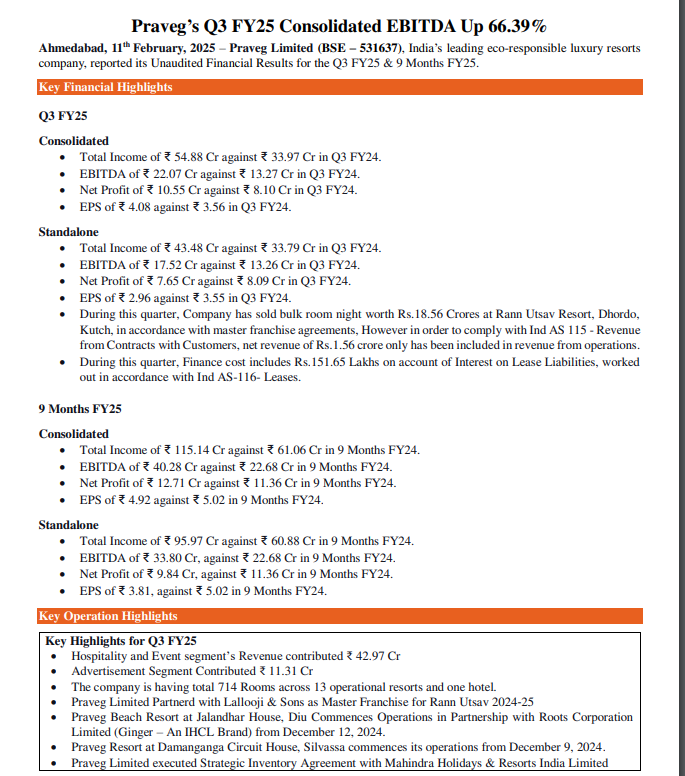

Praveg Resort at Damanganga Circuit House, Silvassa, commences its operations from December 9, 2024

1 Like

CG is big red flag here… Not sure how Sage One came in…Some of the CG issues are -

- Change in accounting policy. Earlier they use to write off tent expenses in same year. Now they do in 5 or more years. Not sure if tent life is 5 years or more (might or might not)

- Buying TV license and then sold - unrelated business

- Dubious transactions by promoters, changes in shareholding

- Buying marketing / billboard companies. This business is not worth investing…

- NGT stay in Varanasi on tent operations. Outside Gujarat, they might lack the connects

- Acquisition of a hotel. Do they have competency to run 1 single hotel… Either they buy more or don’t buy at all.

- Biggest - Where is B2B business of events? It has been shifted in some other entity… it has evaporated like anything…

3 Likes

yes totally agree… i have been tracking and see lot of subtle here n there changes that mgmt is making.

Dont hold any position.

3 Likes

Praveg is struggling to improve EBITA due to its lower operation leverage. Most of Praveg location has limited number of tents/rooms (mostly less than 50). However, they have to invest in all things which has good operating expenses like kitchen, common amenities, reception and administration staff, etc. These all common amenities will increase overall negative impact on margins and it does not have much operation leverage due to limited number of tents/rooms.

3 Likes

Praveg Limited’s share price has been continuously falling over the past year, dropping from ₹1300 to ₹465. The question now is whether the investors who bought shares at high prices will get a chance to exit. Research on the company has revealed several facts:

• Too small company. Despite being a 20-year-old company, it has not yet reached an annual turnover of ₹100 crore.

• Over 75% of the company’s 14 resorts are built on government land, for which the company pays an annual royalty of over ₹60 crore. Number of employees increased from 100 to 1500 in just 2 years.

• The land leased for all resorts is for less than five years, and with the costs of building temporary resorts, no one knows when or how much profit the company will make after depreciation and fixed operation cost ? This remains an unanswered question.

• In the small area of Diu and Daman, Praveg operates 8 resorts, increasing the business risk for the company.

• The 200-tent tent city project in Varanasi is shut down and stuck in legal battles, raising doubts about its future.

• The company had projected the launch of 25 resorts by March 2025, but so far, it has only launched 14 resorts. This has led to a loss of investor confidence.

• The company management had estimated ₹300 crore sales and ₹120 crore profit for the current financial year, but when combining the first three quarters, the company has achieved only about ₹100 crore in sales and less than ₹14 crore in profit. This clearly indicates. Are the promises made to investors not being fulfilled ?

• The company management seems to be rushing to show performance by forming alliances with new companies, rather than focusing on its core business. Seem that they are struggling to manage the business.

At current price of around 465 and PE multiple of around 85, the valuation is very high for the quality investors. This is my personal opinion.

6 Likes

More over the main concern is the promoter doing random businesses like selling tv license and advertisements

Should focus on core and try to build a brand

2 Likes

PRAVEG LIMITED - Is There Still Any Hope?

I invested in this ultra-small hospitality company after hearing big promises from the management. They painted a rosy picture for investors, promising 2x annual growth and multibagger returns. Impressed by these claims, I purchased shares at Rs. 1200, expecting substantial gains.

However, now all those promises have fallen apart. The management has failed to deliver. The Chairman, a Chartered Accountant by profession, seems ill-equipped to lead the company. It feels like there is no one capable of steering the ship. They keep recycling the same optimistic narrative while continuing to underperform and, frankly, exploit investors.

Against their promise of Rs. 300 crore in revenue this year, the company has barely managed to hit Rs. 100 crore in the first three quarters. They are nowhere near meeting their 2023 vision, not even halfway. Yet, they’ve already unveiled a new “Vision 2028,” promising 65 resorts with 2500 rooms.

I’m at a crossroads and unsure whether I should hold onto my shares or cut my losses. I’ve already lost over 60% of my investment, and the stock price continues to decline day by day. Is there anyone who can offer advice on what my next steps should be?

5 Likes

Business model of this company is flawed, even current valuations are expensive, long term support for stock is near 150, PE 97, market cap to sales is 10, How they will scale to 2500 rooms and 65 resorts? Its not easy to develop a resort.

Booking losses is toughest part of investor journey and most important. Freeing up capital by selling laggard and using capital in a good company is best way.

If you want to remain in travel sector than Thomas cook offers great bargain price, own Sterling holidays, SOTC, forex Business is very strong. You will be able to recoup your losses in next 12-18 months as tourism sector will boom.

Above are my views only, ultimate decision is always yours as capital is yours.

3 Likes

Business model is good but it takes time and mgt also given big topline targets which are not achieved and now market is punishing the stock.

but at price of 1200, p/e is of 100+ so you bought good company but at a high valuations

as per me, it will take 2 more years to reach to 300cr of topline

You can book partial loss now. Follow it closely over next 4 quarters. Keep liquidating every quarter unless it shows improvement in quarterly results. In case you see improvement, hold on to your remaining quantity. I would have done the same thing if I were in your place.

Thank you.

1 Like

Despite massive correction, the stock continues to trade at multiples higher than industry leader indian hotels. The company has no moat, promoters have no experience in hospitality. Massive red flags exist , such as change in depreciation accounting policy and increasing in useful lives of assets to increase pat. Apart from that, promoters have continuously diluted stake multiple times , despite company being debt free. Also Mgmt execution has been very weak as compared to guidance. There were strings of resignations in 2023 of kmp and internal auditors. Now the latest new red flag is merger of promoter related entity to increase promoter stake to above 50 percent . Despite all these issues can’t understand why is the stock trading at such high multiples.

2 Likes

![]() Praveg Limited: Valuation Disconnect?

Praveg Limited: Valuation Disconnect?

Even after a sharp correction, Praveg still trades at a steep ~111x P/E—far above Indian Hotels (~60x). This premium is hard to justify given the underlying fundamentals.

![]() No Clear Moat: The company lacks a defensible competitive advantage in the hospitality space.

No Clear Moat: The company lacks a defensible competitive advantage in the hospitality space.

![]() Promoters Lack Hospitality Experience: Raises concerns about strategic depth and execution.

Promoters Lack Hospitality Experience: Raises concerns about strategic depth and execution.

![]() Accounting Changes Raise Eyebrows: Extending asset life to boost PAT feels more cosmetic than operational.

Accounting Changes Raise Eyebrows: Extending asset life to boost PAT feels more cosmetic than operational.

![]() Frequent Stake Dilution: Despite being debt-free, promoter stake has steadily declined.

Frequent Stake Dilution: Despite being debt-free, promoter stake has steadily declined.

![]() Execution Misses: Guidance has been weak, and 2023 saw multiple resignations (KMPs, auditors).

Execution Misses: Guidance has been weak, and 2023 saw multiple resignations (KMPs, auditors).

![]() Governance Concerns Deepen: Recent merger of a promoter-linked entity pushes promoter stake over 50%.

Governance Concerns Deepen: Recent merger of a promoter-linked entity pushes promoter stake over 50%.

![]() With so many red flags, the market’s continued optimism seems overly generous. Valuation looks stretched—caution warranted.

With so many red flags, the market’s continued optimism seems overly generous. Valuation looks stretched—caution warranted.

2 Likes

I started tracking this company recently, and found the red flags on reading the financials those got further after reading the comments here, searched on Google and Youtube and found the below video, this guy has covered few more points like number of employees and compensation to the auditors etc.

3 Likes