This thread is needing frequent updations in these times - once every 2-3 months.

Both Opportunistic bets - Avanti Feeds, and Canfin Homes continue to deliver stellar results; However with Valuations becoming richer and richer - and allocations in Portfolios going up (from 15% to 30% plus, despite several trimmings), its a wise risk-adjusted policy - to continue to trim such holdings. (Mistakes are inevitable - when we can get caught up - in trying to extract all the juice - all the time)

Pharma businesses as a pack have been facing several headwinds. More stringent inspections/standards, distributor consolidations in developed markets, currency risks for those with lots of exposure to rest of world markets like Ajanta - against the backdrop of strident measures from drug price control regimes, in almost every market. Folks like me who have enjoyed a super-ride with Pharmaceuticals sector for over last 5 years, now need to acknowledge the writing on the wall for the pack - except maybe where one has good visibility for FY18/19.

What is interesting though is that for a few businesses (like it somehow always does) competitive position has become stronger but valuations have actually moderated. Have you done enough homework/have the conviction to buy more as your favourite businesses become cheaper?

A request - please don’t put anybody on the spot here - there are no universally right or wrong answers - we can all be proved wrong - better do your own diligence and find out what actually resonates with your individual investing style - which of my businesses valuations have moderated, but Competitive Position has become only stronger & why? If there is one key “Quest” for concentrated Compounders to live-by - this is probably it!!

Also the quest for newer, stronger horses (for next 2-3-5 years) HAS to continue. Time to work that much harder on this aspect - basking in the comfort of existing achievers can be detrimental to our health!!

This thread seems to be the most informative and learning experience. Good break up of portfolio in smaller parts which are always easy to understand and take a call on sizing etc. I have always believed that more than the stocks selection it is way more important that sizing of a stock or a group of stocks in portfolio is given more attention. You have discussed about in the past as well somewhere about allocating the most in high conviction and low valuation. I generally follow the two portfolio strategy Core and Satellite with core taking up 80% and have 10 stocks which are steady and core growth compounders. Few of them take rests for extended period of time as well. Within these two portfolios I have sub categories just as you have defined above.

I would like to understand following from you’

What is the percentage of allocation of all above categories in general which remains most of the time in portfolio except few occasions when one changes them based on market or stock specific conditions.

How to deal with sleeping stocks which are not doing anything for past 2-3 years but seem to be good stories going ahead. For example Vguard for me was a sleeping story for almost 2 years before it started up its journey a year back and almost tripled from then. I always had the conviction. However stocks like Lupin and Alembic, Tata Elxsi are testing patience big times. I feel the time has come again for stocks like Havells and Vguard to sleep for extended time for any up move. However one does not feel like exiting them.

Smart investor say that average up in investment. But my calculation shows bad results.

Let us say I am following simple method of regular investment in rising stock at 20% interval with stop loss of 16.67% i.e.

time-1: Buy 1 unit at price 100

time-2: Buy 1 unit at price 120: Now 2 units at average price 110 with profit of ~ 10%

time-3: Buy 1 unit at price 144: Now 3 units at average price 121 with profit of ~ 20%

time-4: Buy 1 unit at price 175: Now 4 units at average price 135 with profit of ~ 30%

time-5: Buy 1 unit at price 210: Now 5 units at average price 150 with profit of ~ 40%

time-6: Buy 1 unit at price 250: Now 6 units at average price 166 with profit of ~ 50%

time-7: Buy 1 unit at price 300: Now 7 units at average price 185 with profit of ~ 62%

Now if we hit Stop loss at 250 then 7-units * [Buy@185 and Sell@250] => Profit of 35%

Now if we hit Stop loss at 210 then 6-units * [Buy@166 and Sell@210] => Profit of 20%

Now if we hit Stop loss at 175 then 5-units * [Buy@150 and Sell@175] => Profit of 16%

Now if we hit Stop loss at 144 then 4-units * [Buy@135 and Sell@144] => Profit of 6%

Now if we hit Stop loss at 120 then 3-units * [Buy@121 and Sell@120] => Profit of 0%

Now if we hit Stop loss at 100 then 2-units * [Buy@110 and Sell@100] => Loss of 9%

Now if we hit Stop loss at 83 then 1-unit * [Buy@100 and Sell@83] => Loss of 17%

So “average up in investment” also not that fruitful OR am I missing something here ?

i feel we need to modify selling approach in this. Generally after 33% down means downtrend started. I would prefer to exist all with 33 to 35% max. Before that one can sell as he wants…like 50% once it is down by 20%.

While stock is solid and trending up, rarely it falls 20%. Other can chip in share their approach what they will do. hope this helps

Fantastic write-ups and discussions, and particularly where samples, and backtesting was provided. It proves the point.

But…

What is see is that in Bull Markets, the non-diversified concentrated portfolio with lots of small and midcaps which will normally become part of portfolio (like today), does phenomenally well. If not vigilent, then these stocks take a deep downturn, which means this ‘concentrated portfolio business’ if for the vigilant and active investor and not for the guys who go buy, hold, sleep, pray and then come back a year later, talking about losers in the portfolio. And, this happens more so than not…

So, if one want to be Buy and Hold, then make a mutual fund out of your portfolio is the lesson I am learning from here.

If one wants to see great returns, then spend time monitoring, acting on portfolio of stocks, and forget about the stock-market or market-of-stocks. Managing the buy prices, sell targets, stop losses, and having discipline, without necessarily watching 1 minute charts will be needed here. 10 min to 1 hour per day during market hours is what I am talking about.

Just my 2 cents on having invested in many different ways in the market including doing day-trading, and including holding stocks that I have in the portfolio with a holding timeframe beyond my age (purchased in 1954, yes no type 1954) from previous generation, and still holding.

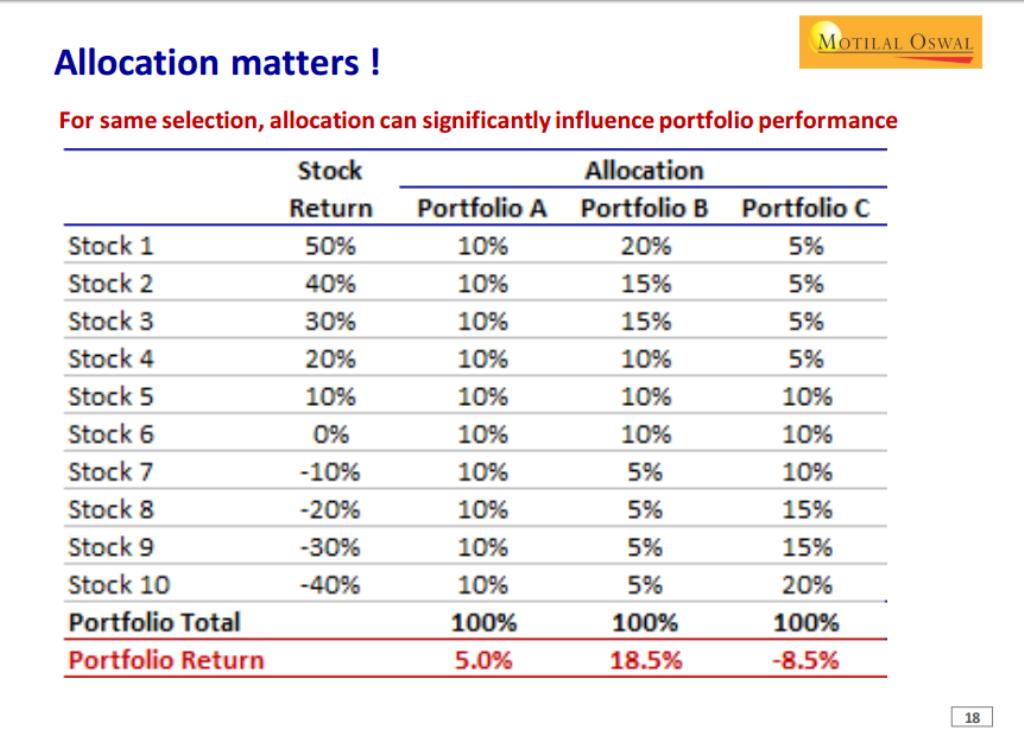

Although I have been forewarned that I am didactic, my thinking is possibly colored by envy, am missing the big picture of this thread and such (all fair, I concede), I could not stop myself from putting up this wonderful slide by Mr Raamdeo Agrawal.

That’s because it highlights the importance of putting most money in your best ideas (subject to the assumption that your best ideas make more money than your next best; and, much more often than not). The slide tells you that even if you are able to generate a lot of good ideas; unless you allocate lots of money to them, you will not make much money. So someone who generates mediocre ideas but allocates bulk of capital to such ideas may end creating far more wealth than someone who generates great ideas but allocates little to them, for whatever reason.

If we agree up to here, then we should push the thinking forward by saying that allocation of capital is atleast as important as the stocks to whom they should be allocated. Unfortunately, my observation is that we pay little attention to it. I suspect that’s because generating ideas is more hard work, more intellectual and more exciting. Allocating capital is none of these, but just temperament.

For those who want the entire presentation - may be found here http://www.flame.edu.in/pdfs/fil/presentations/Raamdeo-Agrawal-FLAME-Presentation-July-2017.pdf?curator=alphaideas&utm_source=alphaideas

Absolutely. There can be no 2 arguments about this.

I do not think anyone who has grown with VP disputes the importance of Capital Allocation - brought home to us by Mr D in 2011. He said it doesn’t matter how many times ytour stock goes up, what matters is how much you have put into the stock. He drove it home into us by this simple poser, “suppose your stock goes up 5x but you have put only 1L into it, how much did you make” I said 4L. Then he said “suppose your stock goes up only 2x but you have put into it 5L” and I said 5L!! And then gave us (as enunciated in the thread) the very simple, powerful, easily executable Capital Allocation framework that we swear by today.

That was a great insight for us in 2011, and that changed the course of thinking/investing at VP, and started the habit of capturing distilled practical investing wisdom (from practitioners of the craft) every year - a la Success Patterns, Business Value Drivers, Art of Valuation, EPA, and the like - stuff that you usually do not find talked about much in investment books)

I am making bold to announce the latest initiative of capturing which most senior practitioners are urging us to do next - an Investing Process Maturity model - which is in progress (going back and forth amongst a few of us). We hope to present the first public version in 6 months, inshaallah!!

The idea being (NOT to present a finished product, none of us are) but a W-I-P Investing Process framework, where we can keep plugging incremental learnings every year - that also serves as a benchmark of our individual progress curve. We felt there is so much to learn - invariably, there is too much of (for want of a better word) disjointed or fragmented learning. With an investing process maturity framework in place - we may be better placed to weigh any incremental learnings, and place them where they belong - on the investing maturity curve !!

Tall aims. Surely - and its an uphill task - not for the faint-hearted - but as always, this is what energises us at VP and with the help of this wonderful community and our super Mentors, we make bold to strive and raise the bar again!

I was just wondering is it possible to share knowledge and learnings from VP meet in Goa this year ? (hope I heard it right that it happened this year too).

Excellent initiative Donald.As some one who has invested in markets from 2008 and it has taken me a whole decade to understand that capital allocation is as important as stock picking .I have more times worked with a mental model and it has lot of times of backfired for reasons of lack of discipline ,conviction or fear.This will be excellent addition to VP and Godbless to all of you involved in it.

@Donald, Sir what would be the recommended price range (based on current valuation) for some of the steady compounders (Bajaj Finance, Avanti Feeds, Gruh Finance etc.) if market corrects further and gives us opportunity to enter into these companies at much lower levels? I do see, you suggested to trim holdings of most of the companies when its valuations are stretched and wondering good price points to re-enter. It would be good to know your approach / strategy around this? Look forward your response sir. thanks.

You have assimilated the journey of the concentrated investor in most elegant way. Your post will help me in fine tuning my portfolio structuring .One question comes to my mind when to exit from a good performer and a non performer,

Yes you are. By averaging up you are increasing ABSOLUTE PROFIT not profit %. So instead of just Rs 100 on 1 unit you are earning Rs 264 if you exit at 210 with 6 units. Averaging up is a better technique than averaging down which one should avoid as it is an open way to disaster !!

First of all Thanks for helping me and other newcomers like me with such distilled practical wisdom. reading the books/ letters is one part and seeing that in action is another. Please take my sincere gratitude.

I am a newcomer and would have definitely benefited a lot if I had followed VP forum to understand the process to build the conviction and perhaps clone the VP portfolio to get rewarded along with the learning.

Now, coming to the core issue of this thread to identify the good quality growth company - I am not sure why we are not considering good Pvt Banks. Irrespective of which sector is the next big thing ( AI, AH,FMCG, robotic) they all will have one thing in common - they will need capital (Wcap /expansion). We have examples of SBI, HDFC, Kotak, Yes generating good returns. I am not an expert in assessing financial institute but I am willing to work on compiling some high level numbers to “rank” private banks. Let me know how I should go about this research in an organised manner, i.e. asking the right question.

Greetings in the New Year!

Have been receiving lot of queries and feedback from fellow investors, of late

Thought of summarising the gist of those interactions, to throw some light on what most of us are thinking/doing going forward in 2018.

As the Guru’s say, Markets are driven primarily by three things A. Liquidity B. Sentiment C. Fundamentals. In 2017 Markets were driven hugely by liquidity and sentiment even in the absence of earnings growth. Now, we are seeing Earnings growth coming back for sure, while domestic liquidity is unlikely to fizzle out in any hurry. What can queer the picture though is Sentiment!

While everyone felt good that the long term India story has got stronger with big-time structural reforms initiated and their shock-effects behind us, rising crude scenario has taken away much of the (economic buffer) sheen of that feel-good. Especially as there are additional concerns of rising inflation, credit growth unable to take-off in a hurry, and worse populism (Govt measures) taking over now in the run up to 2019 elections. So there are enough triggers for “Sentiment” to temper down in 2018

Everyone though is agreed on one thing - that 2018 will probably be a year of Consolidation. That it is going to be very difficult to make good money in 2018, on the back of a stupendous 2017 where most things doubled :). The other factor where most seem to be agreeing is - Kuch correction to banta hain, especially in view of changing sentiment levels.

If we speak to seniors, there is also agreement that while 10-15-20% corrections may happen anytime (due to over-heated pockets/other triggers), there is no case for a big secular crash/peak bubble stage yet. Despite the buzz in markets (more and more uninitiated folks getting drawn to MF/Direct Equity), they cite absence of mainly three things - which are essential preconditions for bubble peaks A. Where is the huge “Leverage”? B. Where are overwhelming “Sectoral Manias” (at the exclusion of everything else - when if you are not present in these - you feel you have missed out on the bull market) C. Where is the case where you find money-making is too easy?? (Infact most of us are finding it very tough to make money now in these markets, isn’t it? )

So, what are some of the strategies for our Portfolios going forward - at this stage of our markets? Let’s start putting some pointers forward.

Some of my friends have mentioned one big learning from 2017. Not to take extreme positions. A few had too much of over-valuation concerns, and sat out most of 2017 with 50-60% Cash, which wasn’t productive. Similarly a larger number (though still small) are now moving/thinking of moving to 30-40% Cash, given what we have outlined above.

Many cite that the other extreme position of - remaining 100% invested in 2018 again may not be that productive a strategy given what we have outlined above. We must have some Cash (always) to take advantage of Market situations. As markets have got progressively more heated, they have progressively trimmed allocations and/or exited completely some over-valued pockets to get to some 20% Cash levels.

I belong to this segment - that believes in playing a risk-adjusted game - not try to extract the maximum juice - happy to leave something on the table, always; so yes I have moved to 15-20% Cash across Portfolios. I truly think if we are patient and hardworking Mr Market always gives us couple of opportunities every year - based on my experience of watching Markets from 2005. If we have no extra Cash to deploy, how would we take good advantage of corrections to enter some businesses cheaper!

In these Markets one useful Risk-Edict to follow (since nothing is cheap) - is to ensure that wherever we remain invested - those businesses must exhibit growth visibility. Good to strong Earnings growth is something that takes care of most of our mistakes (even staying put in over-valuation territory).

Corollary to above - some friends cite the reversion to mean rule - what has moved a lot in 2017 is unlikely to move much in 2018 - more likely to consolidate the huge gains already made - much of the earnings growth (& visibility, if present) is probably already priced in, there. So a starting strategy is to look at sectors that haven’t moved that much, or not moved at all?? Especially where you see signs of growth visibility emerging!

They cite Oil & Gas as one such sector. Logistics as another. 4G equipment suppliers/Digital Content as the other. Insurance sector - at heightened valuations, everything is priced in?? Wealth Management has still lot of leg-room to run fast, and the like

Some very good points made by Donald.Had the same experience of holding 30% cash most of 2017 but now fully invested and no regrets.However it is essential to keep some cash now because 2018 would be very volatile and there could be some earnings surprises down the line.

Headwinds in 2018 could be crude, US Interest rates,China growth issues and to some extent valuation. Unfortunately there are not many hiding places even in the defensives barring some IT and Pharma stocks.

But if we look at the past many years despite the crude prices and all other issues, the consistent performers (Gruh,HDFC,Bajaj,Britannia etc) have always delivered positive returns. So why should 2018 be different? Yes there could be time corrections and sharp declines in many of the mid & small caps.

At the same time India is all poised to overtake France and UK in GDP terms which itself will create lot of continuing opportunities for existing and new players. A case in point is HDFC mopping up huge cash to invest in affordable housing space and in affiliate cos.In summary if we pragmatically look at 2018/19 together and also keep some cash to invest, should be able to get some decent returns.