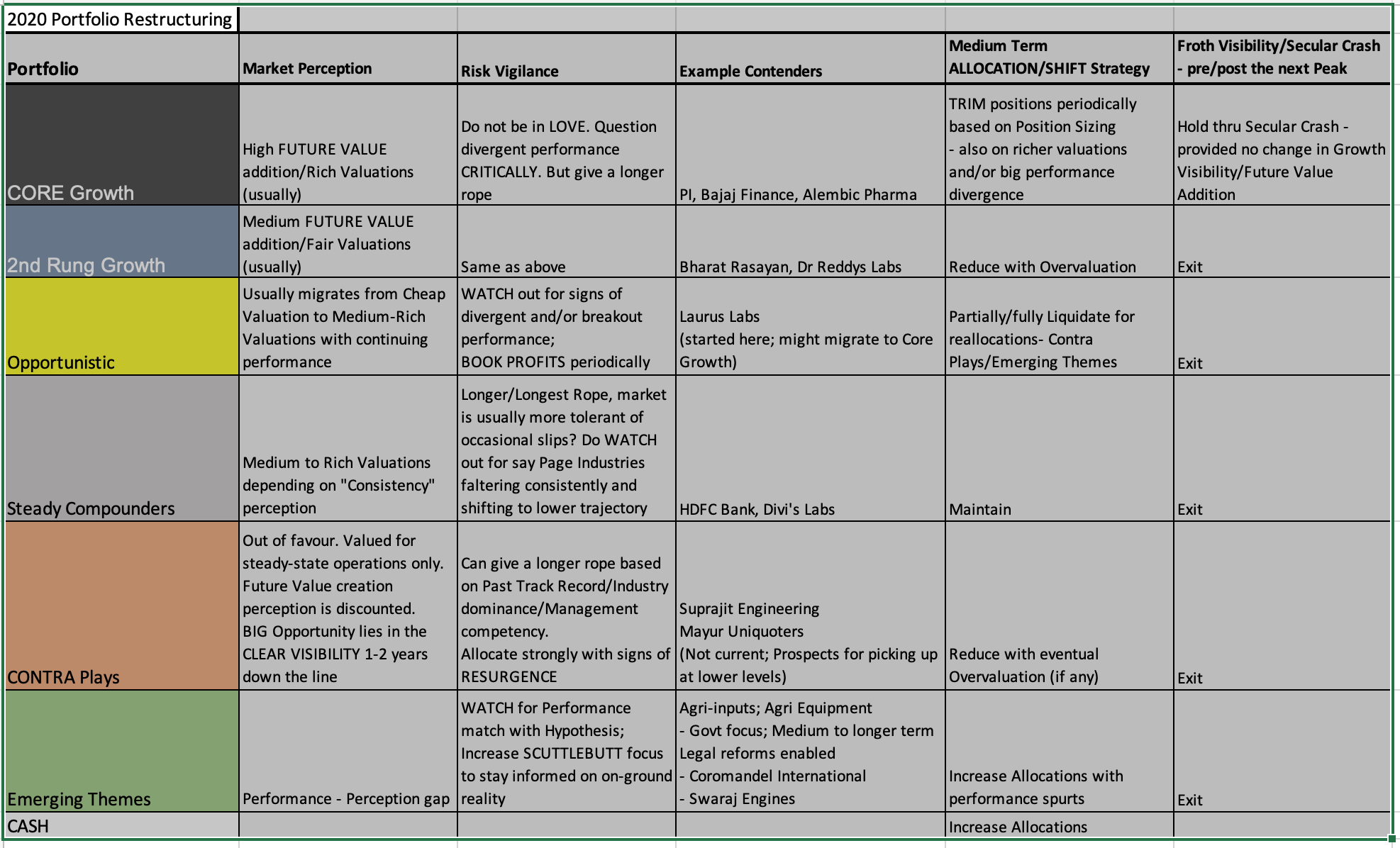

Have been receiving some requests again for a proper update on this portfolio re-structuring thread.

So the above, is an updated summarised table on the same.

Next comes the oft-asked rejoinder, how should we be thinking - given the way markets are behaving currently. There are some signs of clear froth emerging, which many of my senior friends indicate may well get extremely heightened over the next 30 days, and more.

I have found that a well-hedged strategy always works best for me.

a) In March I had moved to 40% CASH levels - that allowed me to stay put in Core bets along with Compounders like HDFC Bank

b) Once there were clear signs of first-order positively affected sectors providing the ONLY visibility, added more of Pharma and Agrichem to move to 25% cash progressively to 15% Cash currently

c) I will be getting back to 25% Cash, and progressively to 40% CASH levels (probably soon)

Having a hedged position - where I do NOT try to maximise the juice - helps me sleep well, all through. Whether the markets produce V-shaped recovery - which it did in select sectors - and was getting more broad-based, to now becoming a Trader’s Mecca - someone like me is CONTENT having participated meaningfully. And if say it goes on to a prolonged bear-market of 1 or 2 years plus after a big build-up and melt-down, I think I will sleep well. I will be more energised to work harder on the next-set of opportunities. I will have ammunition to back me up.

This is the first time in 10+ years of active investing - that I have purposely added trading positions where I found there is high visibility (among my current portfolio bets; none additional). I believe this is a “Traders Market” till the inevitable fall, and felt confident enough to try out a few things - of course under my Mentor Hitesh Patel’s able guidance ![]() . Which means for certain portions of the Portfolio, I am on the look-out to Cash Out progressively as froth builds in them/overall market. Already considering trimming positions in the best-performers (read already frothy, or big position sizes) to allocate more to those moving slower, more consistently (another Comfort Zone breaking/New style training for me)

. Which means for certain portions of the Portfolio, I am on the look-out to Cash Out progressively as froth builds in them/overall market. Already considering trimming positions in the best-performers (read already frothy, or big position sizes) to allocate more to those moving slower, more consistently (another Comfort Zone breaking/New style training for me) ![]() .

.

While I will remain well-hedged for practicality reasons, I do belong to the Camp that thinks this merry-state of affairs has to end sooner than later. The disconnect with real-economy, rising inflation (which is inevitable), hugely widening disparity between haves and have-nots - will prevail over the liquidity-driven (?)/otherwise rally. When that will happen there is no point second guessing. I am happy to leave some juice on the table, again - in tune - with my progressive discomfort, wherever I see frothy valuations. And perhaps in a month or two months - that may well be across the board, given the current momentum.

Another very important aspect I think I should be highlighting - else I will not be doing justice to my role, perhaps.

Market Awareness - Different Phases/Different Strokes (?)

It’s been surprising for me to notice how many years of active investing/reflection it takes, before something very crucial registers strongly in us. Most of my colleagues have proven to be super successful investors over the last 5-10 years - and very interestingly, most with very different styles. But with super-success, there seems to be a price to pay ![]() .

.

We seem to start discounting the fact that our performance record is first a function of the Opportunities that Mr Market offers us, and only then a function of all other things - hard work, investing acumen, temperament and self-knowledge, process discipline, ability to be patient and strike hard when Mr Market offers the opportunity, and so on.

The Deep-Dive-Works-Best Phase

The price inevitably is that we start to think that our style (that worked so beautifully for us) is the ONLY style!! I can certainly confess that by early 2016 (2010 -2015 I had seen only one way up, up and up - from 10x to 20x on many bets to 50x even - witness VP Pubic Portfolio). It was a function of the Opportunity that Mr Market offered primarily between 2010-2013 - you could buy 30% growers with 30% RoE at 5-6x to max 12x earnings. By some strange luck everyone of our so-called strongly differentiated business models we picked was growing at 30-40-50% plus levels. And we could be very very choosy while picking - not many were interested in the markets then (unlike now).

Low-Hanging-Fruits - Anything Works - Phase

And then came 2016-2017 timeframes - where everything was flying. Everybody made money in Markets. You could throw darts and come up with big winners. Lots of lots folks decided to turn full-time Money Managers. Luckily for me Avanti Feeds and Bajaj Finance best performances came to the rescue and shored up the Portfolio beautifully (thanks to high allocations) and I didn’t feel that useless a guy. But I did recognise hey my style, isn’t working that well, there were no cheap bets around anymore - certainly not the strongly differentiated business models I preferred; let alone that - anything that offered a hint of being special or little extra growth was bid up to over 25x earnings or more. High Allocations were NOT possible (Undervaluation simply didn’t exist).

In such environments - when it is too easy to make money - due process gets thrown out of the window - except for the extremely extremely disciplined (and I don’t think I know of one good example among my investor friends ![]() ). In the information over-supply environment, things run up in a week or less, folks advise you to first buy, and then complete your homework. And then another inevitable happens - quality of portfolio bets drop significantly if we keep adding to the tail. This happens even to concentrated portfolios like mine too. Widely diversified portfolios probably suffered more deterioration (because by its nature, one doesn’t have to be too picky).

). In the information over-supply environment, things run up in a week or less, folks advise you to first buy, and then complete your homework. And then another inevitable happens - quality of portfolio bets drop significantly if we keep adding to the tail. This happens even to concentrated portfolios like mine too. Widely diversified portfolios probably suffered more deterioration (because by its nature, one doesn’t have to be too picky).

In such environments, Fear of Missing out (FOMO) takes over - and something like a Shivalik Bi-metal I felt compelled to jump on to the bandwagon - knowing fully well that there indeed was a lot of promise, but my/our homework was incomplete (being based primarily on Mgmt. version of things sans any meaningful market/industry scuttlebutt).

Only Operating-Leverage Works Phase

We all know what happened subsequently in 2018 and most of 2019. Small and Midcaps were hammered out of shape. What helped the Portfolio was having a few well-performing large Caps like Bajaj Finance, HDFC Bank or a large mid-cap like PI industries, all with large allocations.

But even in the 2018-2019 environment there were friends who made tons of money ![]() . These were the guys focused solely on Operating Leverage plays. Nothing was cheaply available, right? So the only thing that works consistently in such an environment is business out-performance. They were smart enough to figure this out and would only bet where growth visibility was very good, Operating leverage at play evidence was almost a no-brainer (Rs 1 of incremental sales would clearly land Rs 2 or Rs 3 of incremental EBITDA), and this fore-knowledge/anticipation of enhanced earnings curve was no-doubt bolstered with hard scuttlebutt work, and that worked fabulously! They merrily hopped around from one to the next - once the curve seemed to flatten.

. These were the guys focused solely on Operating Leverage plays. Nothing was cheaply available, right? So the only thing that works consistently in such an environment is business out-performance. They were smart enough to figure this out and would only bet where growth visibility was very good, Operating leverage at play evidence was almost a no-brainer (Rs 1 of incremental sales would clearly land Rs 2 or Rs 3 of incremental EBITDA), and this fore-knowledge/anticipation of enhanced earnings curve was no-doubt bolstered with hard scuttlebutt work, and that worked fabulously! They merrily hopped around from one to the next - once the curve seemed to flatten.

Moral of the story?

-

Even these guys started thinking/saying - Yes - Operating Leverage is the ONLY game in town

While there is some grain of truth in the statement that Operating Leverage focus is great and a MUST-ADD in everyones investing toolkit (irrespective of style), there also comes a time when Operating Leverage doesn’t work anymore - witness March 2020 and thereafter, or the early stages of any bear market, which may again come on us sooner than later, inevitably. That is the time our Deep-Dive VP style works best (we have all the time to keep dissecting, be very very choosy, keep allocating more as higher conviction builds up on those that execute well to stand out from the rest - allowing us to separate the wheat from the chaff). I know some of us are waiting eagerly for that eventuality

While there is some grain of truth in the statement that Operating Leverage focus is great and a MUST-ADD in everyones investing toolkit (irrespective of style), there also comes a time when Operating Leverage doesn’t work anymore - witness March 2020 and thereafter, or the early stages of any bear market, which may again come on us sooner than later, inevitably. That is the time our Deep-Dive VP style works best (we have all the time to keep dissecting, be very very choosy, keep allocating more as higher conviction builds up on those that execute well to stand out from the rest - allowing us to separate the wheat from the chaff). I know some of us are waiting eagerly for that eventuality  .

. -

While everyone MUST stay true to what works best for them (their own personal style that proves highly successful for them) everyone MUST learn to add complimentary styles. I picked up on the OPPORTUNISTIC bets style from Ayush and Hitesh (insisting all the while that my Opportunistic bets had to be a smaller subset of theirs - only those with the promise/ability to migrate to core/2nd rung bets passed muster). Now I am picking up the focus on OPERATING LEVERAGE at play (again with the insistence that they should belong to Core or second rung growth quality transition). I have also added CONTRA style (1 to 1.5 years strong visibility) since 2016 as mentioned earlier, since I find that allows me to allocate heavily to out-of-favour businesses with high margin of safety. A couple of bets there usually suffices for me.

-

All of us can learn from highly successful folks around us.

Be adamant enough to stick to our Core styles (and keep refining/strengthening that success plank) but also be flexible to experiment/add a little bit of other highly successful styles (we see around us) to the mix slowly, but surely. Actively seek out folks exhibiting success with styles complimentary to ours. Above all start becoming AWARE that there are DIFFERENT phases of the Market - where different mixes works. And what is working very well now, will inevitably change. I am convinced NO one style by itself, can do justice to the eternal quest for the all-weather/all-conditions, well-structured Portfolio.

Can we be better prepared?

I am sure we can. Think we need to PLUG this hole in VP for better Market-Phase-Awareness focus. That will help us all become more well-rounded investors - whatever be the level of our current Investing maturity.

PS: Usually I need to add only 2 bets a year to the Portfolio as a couple of bets inevitably mean-revert. This year I was lucky (due in part to March excesses, and due to excellent colleagues supporting to educate quickly) to add 4 seemingly excellent mid to long term prospects - Alembic Pharma, Bharat Rasayan, Laurus Labs, and Dr Reddy’s - subject to execution track/conviction build-up).

Most of the Credit goes to my super colleagues. Again goes to illustrate - make it a point to hear out our colleagues with strong conviction. Make it a point to work with folks smarter than us. Inevitably, we get smarter!!

Disc: This Portfolio structure is for educative purposes only. This is NOT a buy/sell recommendation. I may or may not be invested in all the stocks mentioned/discussed. My views on the Portfolio structure/components can change suddenly with more insights on the business/industry/Market Phase. I may not be prompt in updating the Portfolio Structure and/or Components.