TL;DR - Noob, Late entrant to market, Looking to stay invested for period of 15 (or more) years, seeking review of targeted portfolio and investment pattern over next 3-5 years.

Hi,

I have been somewhat interested in how economics work and stock since late 90s. Been observing stock market behavior from same period. But truly understood the principle of compounding and thus the opportunity lost only in the last couple of years. But never late than never, so last year after the crash (Approx aug 20 I started studying with a goal to invest). The last 6 months have been repeated rounds of reading (amidst all the other stuff life throws at you, hospitals, offices, kids, bills etc). Tried to ingest as much of ROE, ROCE, EPS, P/E, D/E, P/E By Industry P/E (this is something I made up to judge relative over or under valuation - because in current scenario, everything is over valued) value investing, growth investing, contrarian investing as much as I could. Discovered screener in the process (thank you, thank you. If you IPO, I am buying). Also discovered Saurabh Mukherjea and Ashwath Damodaran. Regretfully I could not finish the intelligent investor. Have a copy, but it progresses very slowly. Should I force myself through to the end? Sahil’s suggestion of ‘The Swedish Investor’ is much more my type. Read a lot of annual reports and other bse/nse docs as well (Understanding of the same has lots of room for improvement though). Also discovered valuepickr, and have read through most of the threads about the firms I have chosen. Usually from 2020 onwards, some from 2019. Have not read all the way from top to bottom though - you guys discovered some of these when they were basically non-entities.

My final portfolio chosen for investment is given below. A brief note of the investment rationale is also given. I follow it up with a brief about some of the other companies which came very close but I finally discarded with a heavy heart (Nestle for example). The portfolio has been chosen to approximately be equally exposed to large cap blue chips (consistent compounders), growing mid caps (growth) and small and micro caps (just discovered or undiscovered or value unlocking yet to happen). Don’t know if my choices are appropriate or not.

My plan is to invest in SIP fashion over the next 3 years, equal weights when buying. May not rebalance - but not decided yet. I have been looking for the last 6 months for the economy to catch up to the market, or vice versa, but that is not how the ground reality is playing out. So finally almost ready to jump in. Choosing SIP mode over lumpsum + SIP, cos with current valuations, markets correcting is very likely, but irrationally it may go up. Over the next three years though, we will probably have seen the up and the down and I would have managed to average - now whether I average upwards or downwards remains to be seen.

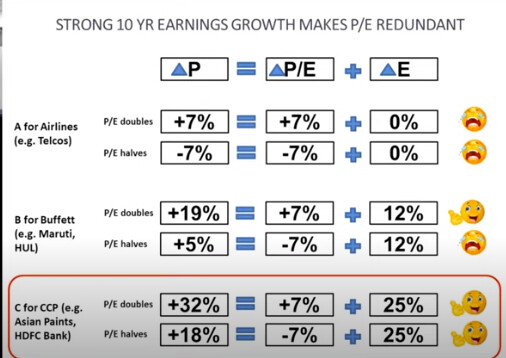

I would like to achieve long terms 20%+ on my portfolio - Otherwise funds like Axis Equity, Quant Active, PPFAS are doing 19%. Advisory services like Purnartha - 35%+, Rohit Chauhan and Vijay Malik - 19%, any one of those would work.

Current Targeted Portfolio

Category 1 : Blue-Chip or close, Consistent YOY growth, Relatively low volatility on screener charts, High ROCE - consistent compounder theory. I add the key tipping point or key doubt next to the stock.

Pidilite - excellent on all parameters. Secondly, this is an industry which should be dependent on the economy, but it hardly cares, good eco, bad eco, it keeps going upwards.

Atul - again rock steady growth, firm is around for almost like 100 years or so, international presence, highly diversified, favorable sector.

Whirlpool India - best rock-steady growth among the consumer durables, also good appreciation.

Britannia Industries (won over Nestle on account of better stock appreciation and lower per stock price, in spite of its near 97% monopoly in baby powder). Also more fair value (PE to industry PE) at the moment.

HDFC Bank - still don’t know very well about understanding banking and NBFCs, so going by recorded history on this one.

Bajaj Finance - primarily on account of the Saurabh Mukherjee analysis about the big data aspect of this business,

Asian Paints - again the Saurabh analysis about business process efficiency.

Abbott India - Growth Charts and relatively undervalued still. PE to Industry PE is 1 or thereabouts. (Divis is 2.47). Pharma sector.

Category 2: Growth Stocks - Usually mid-cap to large firms. Expectation is these have momentum, tailwinds and are in the expansion stage of their businesses, should be high gainers for a few years before they settle down to steady growth (but with the current markets and economy, will have to keep fingers crossed).

Aarti Industries - Undecided about this, late entrant, growth is rock steady, the DMAs are like straight lines, but the debt is worrisome.

Fine Organics - Rock steady growth since inception, high ROCE, good reputation, favorable sector.

GMM Pfaudler - The current correction from highs seem like an opportunity, Otherwise firm seems like a very good monopoly play across a whole bunch of industries, but especially a very solid proxy for the pharma and chemical sectors, both of which are pretty good sectors now.

Muthoot finance - Growing steadily, has harnessed the untapped gold in our country, lots of expansion still possible, caters to masses.

Dr Lal Path - Same as Muthoot basically, except this has harnessed health instead of gold.

Indiamart intermesh - Somewhat of a conviction bet against the valuation aspect. Platforms will be the next thing - google, facebook, whatsapp, airbnb, uber, ola, - same for this. Additionally first mover, and profitable. How many profitable tech unicorns there are out there - almost zero (uber, zomato, swiggy, etc etc). Info-Edge I let go just because of the profitability angle. Also their mobile first approach.

KPIT tech - Sahil was looking for an IT firm, Maybe he could take a look at this. Everything they are doing is in the sunrise sectors of tech - AI, robotics, etc. Recent listee.

Ratnamani metals - consistent compounder, only slower. Steady growth. even in a horrible sector. let go of maithan alloys, APL Apollo and APL Apollo Tricoat here just because this seems safer.

Indraprastha Gas - Best Gas bet I could find. Gas reserves in our country, drive against fossil fuels, solid growth.

Indian Energy Exchange - Sits squarely in the intersection of the platforms, deregulation, anti-fossil fuels, and mass participation plays. monopoly to boot.

Relaxo Footware - Consistent compounder, Consumer, Mass market, Steady growth.

Garware Tech Fibres - Parameters are good. But the story - An old indian company (in ropes, of all things), reinvents itself, rebrands itself, and becomes a leading player in scandinavian and australian fishing nets and in general, value added fibres - the management capability (vision, direction, execution) required to be able to pull off something like that is imho, incredible.

Category 3- Basically bets.

PI Industries - solid steady growth - consistent compounder type, big old company, agro-chem. This beat both coromandel and vinati.

Suprajit - valuepipckr forum thread was what convinced me at the end. Especially donald’s notes. And especially the part about where it foresaw the decrease in halogen OEMs and went for the after-market. International, quite diversified, seems to have fixed its problems in recent past. If auto revives, is well poised for growth.

RACL Geartech - The client list. Growth is somewhat steady but the spike last year worries me. Do we have runway still?

Chemcrux - quite old, very solid management with great academic backgrounds, excellent numbers. Easiest annual reports to understand.

Dixon - Overpriced, but huge opportunities and is perfectly placed. Wins over amber for its diversification.

Galaxy Surfactants - This is basically from Little champs by Saurabh Mukherjea, but their web-site was what convinced me. Also the client list. Basically a proxy for FMCG growth.

CDSL - again the platform play, duopoly, and consumer participation in stock market will invariably increase over the gyears.

Laurus - Similiar to Dixon. Very well placed, Very overpriced. Pharma tailwinds.

Suven Pharma - somewhat risky, but seems like proper value unlocking after demerger is not yet through. Plus pharma sector tailwinds.

IRCTC - monopoly. Will grow as the india railways grow.

Thats it.

Category 4 - Companies which lost out -

Affle India, AIA Engineering, Alkyl Amines, Amber Enterprises, Apollo Tricoat Tubes, Astral Poly Tech, Avenue Super., Bata India, Berger Paints, Colgate-Palmolive, Coromandel Inter, Dabur India, Deepak Nitrite, Dhanuka agritech, DISA India, Divis Labs, Frontier Springs, Gujarat Gas, Havells India, HCL Technologies, HDFC, Hind. Unilever, Honeywell Auto, Info Edg.(India), ITC, Jubilant Food., Kotak Mah. Bank, L & T Infotech, Larsen & Toubro, Lumax, Mahanagar Gas, Manappuram Fin., Mangalam Organic, Mishra Dhatu Nig, Navin Fluo.Intl., Nestle India, PPAP, Pulz Electronics, Refex Industries, Reliance Industries, Sanofi India, Shree Cement, SRF, Symphony, Tasty Bite Eat., Tata Consumer Products, Timken India, Titan Company, Trent, TTK Prestige, Hawkins, Vaibhav Global, Varun Beverages, Vinati Organics, Voltas, Axtel Industries, Maithan Alloys, MoldTek Packaging, TCS

A few questions that bother me -

Should I be entering the market at this time?

What should I be looking at for exit criteria?

What should be my monitoring frequency - in my understanding, if I have to monitor this daily, then my choices are, most probably, already wrong.

Apologies for a very long post. I understand this sort of question has probably been asked many times on this forum before so you may be tired of it. I wouldn’t have posted this, except that the current market valuations are very scary and diving in just like that seems, you know, a little foolhardy.

Any advise, ideas, suggestions, opinions - will be much appreciated. Thanks.