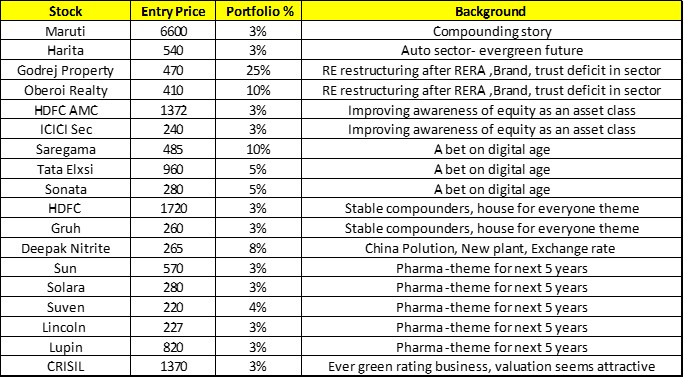

There are few factors for preferring real estate apart from Rera

a) The sector is in down-cycle for last 6-7 years , if economy and jobs picks up ,it should revive fast , so rather than directly investing in flats , taking the bet through real estate companies.

b) Choice of these 2 companies is a hedge in case the demand does not revive. Small players are getting out from the market due to trust deficit and funding issues, the established brand names would take bigger market share. Even in a slow market, there’s always some demand from end-users . In that scenario ,betting on Godrej for mid-income and on Oberoi for luxury. Mumbai being a stable market is also an added factor for choice of Oberoi. Godrej’s asset light model and brand credibility led to higher allocation.

I have been watching 3M for sometime now. Woukd be interesting to understand the thesis on this?. (sustained growth rate, ROE,ROCE, economic growth proxy etc. )

I am a little bit confused on this.

You have suggested HDFC Bank and not HDFC. I feel if we buy HDFC, we get a part ownership of bank along with a few fast growing subsidiaries. Also, we consider the value of the subsidiaries, HDFC’s core business trades at < 2 BV.

Despite this, many are saying that HDFC Bank is a better buy. Even if HDFC Bank grows, HDFC will also grow due to bank.

Thanks for your suggestions. Few of these I’ve already kept in my portfolio.

For RE, had looked at your suggestions, but thought of sticking with market leader.

In IT , have kept LTTS in watch list. Found Saregama more convincing due to recent management change and its focus on encashing the changing scenario.

Credit : Somehow not convinced with HDFC Bank as there are number of new banks are coming ,hence too much competition.

Pharma :Thanks for suggestions, would keep these in watchlist.

Evergreen :Yes these are good stocks , but did not want to have too many stocks in the portfolio.

Well , this is a no-brainer portfolio . Should give >15% CAGR in next decade. Effort is to catch next 10 companies at an early stage that someone put in this kind of portfolio in 2025.

You have done away with the challenge of MoS, by looking ten years fwd, so now you can think more clearly. Great going.

List has stocks with good RoE and RoCE, but in recent times the sales growth is poor, in single digits.

The market is paying a PE upwards of 50, because they expect a certain growth in EPS. If that doesn’t happen even for a few qtrs, market will react. High PE stocks, mid caps tend to react sharply.

Companies are good, but sales are slacking, due to which price could see a 30 to 50% from the top. Are you comfortable with that?

Till 2016, all was very nice. Then growth came to a grinding halt. Sales growth, RoCe, Roe, profitability hence EPS growth… Slumped. Stock got decimated… Down 60% from the top… with recovery not in sight.

Agree with your assesment. The 10 companies ,chosen by our friend, are great companies with more than decent historical record. But they are very much reflection of the economy, if economy does well these would keep delivering numbers but in case slowdown, the results may not be on expected lines.

These are high PE stocks; the price swings are likely to be sharp, is the point.

Since stocks are good recovery is certain, but to face the period of drawdown without making the ultimate mistake, is the key to getting compounding returns YoY.

Suggest we should do reverse valuation. Quality and high PE is given. Let’s estimate what growth and for what foreseeable future its visible. I mean how is market estimating its EPS growth for next 5 or 10 years. Now one can analyse whether that kind of growth is realistic, probable, triggers present, effect of Industry headwinds if any, dying competition etc etc. If own analysis and estimation of growth is same as market, then go ahead to buy or hold. Else avoid or sell. I think this way we can evaluate such companies.

That is the tough part… To estimate future EPS. Who would have guessed the current state of EPS for pharma back in 2015.

This is the only problem with High PE stocks, else everybody would happily shortlist based on high roe and buy only those stocks, if things were so discernible.

When high pe stocks show a regression in sales or profitability… They fall bad.

I honestly don’t understand pharma business. Will study history and get my concepts right when I find some free time. Another thing I plan to do, don’t know when is to pick stocks which were say 50 bagger in 10 years. 1st 5 years, 10 bagger and next 5 years say 5 bagger… Now will analyse at mid point how past was and how future played out… Will do some back testing to understand. I am not a excel master though, neither get time out of hectic sales job, but will give my research a shot. Any one who has done it, or may refer some existing study will be of great help. Thanks!

It seems you’ve either already made 1000 crores or read too many books.The way you write and the language you use , it seems you know everything.

Are you here to help others or learn ? If answer is yes, would request you to be humble in writing. Don’t know your age, but I am 60 +, and don’t want to be lectured .But yes, I’m ready to be taught but by the people who understand that no one is perfect.

is to pick stocks which were say 50 bagger in 10 years. 1st 5 years, 10 bagger and next 5 years say 5 bagger… Now will analyse at mid point how past was and how future played out… Will do some back testing to understand. I am not a excel master though, neither get time out of hectic sales job, but will give my research a shot. Any one who has done it, or may refer some existing study will be of great help. Thanks!

is to pick stocks which were say 50 bagger in 10 years. 1st 5 years, 10 bagger and next 5 years say 5 bagger… Now will analyse at mid point how past was and how future played out… Will do some back testing to understand. I am not a excel master though, neither get time out of hectic sales job, but will give my research a shot. Any one who has done it, or may refer some existing study will be of great help. Thanks!