As you have a no of pharma companies in your portfolio, I suggest you to go through this VP thread…

Thanks for your views , everyone’s views are valuable unless those are not preachy. Your suggestions are real good. As far as different asset classes are concerned , I go with following ratio since last many years:

RE : 30%

Equity : 40%

Gold :10%

Debt Funds : 15%

Cash :5%

Thanks, would go through it.

@jamit05 . I dont think Lupin is a good example. The consumer names will be more apt. The best part is that , one can get out with minimal or no damage if things dont work. (Of course, eventually they may price/time correct. But it wont happen right after the earnings announcement.) For example in Q2, Asian paints, Pidilite, Gillette had a average/poor result. But hardly any damage to the price despite being > 50 PE. I have been observing this pattern for a long time now…

2 Likes

What I mean that as you tend towards 100% predictability, your returns will tend towards risk-free return. But we know that no biz is 100% predictable.

Also, Index in not Nestle or ITC. It has lot of cyclical, financial and export biz which are far from being predictable and hence need risk premium adjusted returns.

1 Like

No need to delete anything, there’s lot of wisdom in what you said. The comment was on the tone not the content. And as far as respect for age is concerned, people at my age don’t expect anyting (expectations lead to frustration) .

9 Likes

Hello Radheyshyam, its nice to see your enthusiasm to build portfolios and seek adivce at this age (I do not mean to say you are too old for it  ) It would be intersting to know your motivation.

) It would be intersting to know your motivation.

For us to share our feedback on your portfolio, it would be better if you share you expected returns (CAGR) until 2025 and your risk taking ability. As we all have different risk profiles & expectations our feedback will be more inwardlooking than from your point of view.

Would you mind adding delta corp ? Biggest trigger is shifting of ship based casinos on land. Please have a look.

Thanks for encouraging words. I’m a businessman by profession , involved in distribution of agro-chemical products of Bayer, Sumitomo Chemicals and PI industry. Initially I used to buy the shares of only the companies involved in my line of business as I understood them very well.

For last 5 years, I started to study other industries also ( especially the one where my children work). Found the investing not so difficult if someone does the home work and does not go by hype.

Motivation of being in equity is to generate consistent returns over a long period of time. Above all, I have started liking this market and these days have lot of time to study about the companies and sectors as I’ve started to reduce scale of my business (next generation is in other sectors ). So investment is more for keeping myself engaged, preserving the capital and enjoy the life.

1 Like

Would study about it. Thanks for suggestion. I think there’s a thread on the same in this forum.

Great to hear that. Any agrochemical company worth investing for medium to long term at these levels. Was invested in Dallas but it has had inconsistent results for last few years.

I have no guts to have something like this in my PF with 62PE and PBV at 11.4…what is the margin of safety in high flying expensive ones?

Hi,

What is your view on Rallis India and Coromandel international? How do they fare with respect to mnc competitors and what are the competitive advantages they have?

Regards,

Govind

Rallis & Cormandal (and many other Indian generic companies )are more or less dead companies as far as agrochemicals are concerned. Many of these survived and prospered in last 15 years due to their exclusive access to Japanese molecules and cheap Chinese sources.

Now Japanese companies are coming direct to India and Chinese sources are also facing lot of issues, so tough time for them.

In agrochemical space,you can look at PI Ind (have long term agreements for R & D with MNCs ) and UPL (bit risky because of too much debt and recently acquiring a big company ) , but need to wait long and only buy at dips as valuations as of now are streched. In MNCs, try to pick Bayer at 10% lower than CMP.

7 Likes

Page is locked in. It is a great company, and will continue to be so. Astral, Gillette, 3M, Gruh too. This is established.

Let’s take another company, say Castrol. It has to plough in a lot more money to earn at the same pace as Page. But both are great businesses probably just as good as each other. With strong management reliable too.

So I believe the buying of Castrol should be at a certain discount to that of page. What is going to be that discount, is the question.

I will project the future EPS of the two companies, and future PE ratio. Best estimates of course. And see which gives me better returns in the near term. At least two years. If the gap is favourable, then Castrol or even TaMo may be a better stock to buy than Gruh or Page, given the numbers at hand.

1 Like

I appreciate your train of thought, when you say that the management is ones ultimate MoS. Unique. Never heard someone put it so bluntly.

Investment in a company is advised only if the above factor is glaring, present and established over the last decade or two. Because if one holds a portfolio of 15/20 stocks… He is going to concentrate 5 to 10% of his wealth in each company. It better be worth it. No gambling there.

One needs to make a universe of such stocks, with impeccable management record. Only Then consider valuations.

In case of High PE stocks like Page, if one is demanding of entry at lower PE, then his only chance will be when the Nifty PE corrects. When for whatever international reason, the whole tide is turning out, and money is leaving our shores.

For no company specific reason, the PE just drops 10 odd units. That is your MoS.

PS: we want good stocks cheap that’s it. The euphemism we use is MoS

4 Likes

Basically, you mean… Page Pidilite are trading at high PEs and will continue to, because they not only have a good track record of RoCE and management but also growing market. Whereas, Castrol does not seem to have a growing market.

Therefore, If one buys Castrol when it’s cheap, he is bound to get out when it’s expensive. Effectively, he will be flipping, trading valuations and not really Investing in the truest sense.

Agreed.

Flipping looks good theoretically. Often times, cheap gets cheaper. See BHEL, Tata motors, Sun, Lupin. However, the overall returns would be more than the returns of the index, not that much more though.

On the other hand, if one is truly Investing, he would buy a stock because it’s sales would be growing each year, has RoCE > 20 and great management. If any of this changes, then it would not justify paying high PE. Until that happens, our investment sees a comounding effect for years… Decade may be. Therein lies the real power of Investing… in compounding.

Buy and Hold is the way to go. Agreed. (Finally)

Hence, now we know the “How”.

We also know the “What”.

The “Why”

The “When”

This is common knowledge. However, I guess, what only a few people know is “For How Long”.

My question is… Have u ever exited such a high PE stock, a high flier? What sort of correction does such a stock go through, when it becomes undeserving. Do investors go into wishing and hoping mode, and lose a lot before they can exit.

Does the weakness in the business start showing in the numbers or does it take a Sanjay Bakshi to understand/see it?

1 Like

I have read this discussion off late. But I would like to add my view when you build your portfolio for more than 3-5 years. All Portfolio stocks move in their own orbit of ups and downs. You must look at reviewing them always from Risk Management point of view also. Sometimes you are unable to book gains at good times and then your full one cycle is wasted in waiting for the up move again after months of waiting. I am not a valuation expert but I manage my high concentration scripts with my unique excel algorithms. Queries Welcome for interested persons. Can give examples by stating recent downfall in market and exits signals as per my Risk Management Algo Excel. Thanks for sharing your views. It was a great learning.

3 Likes

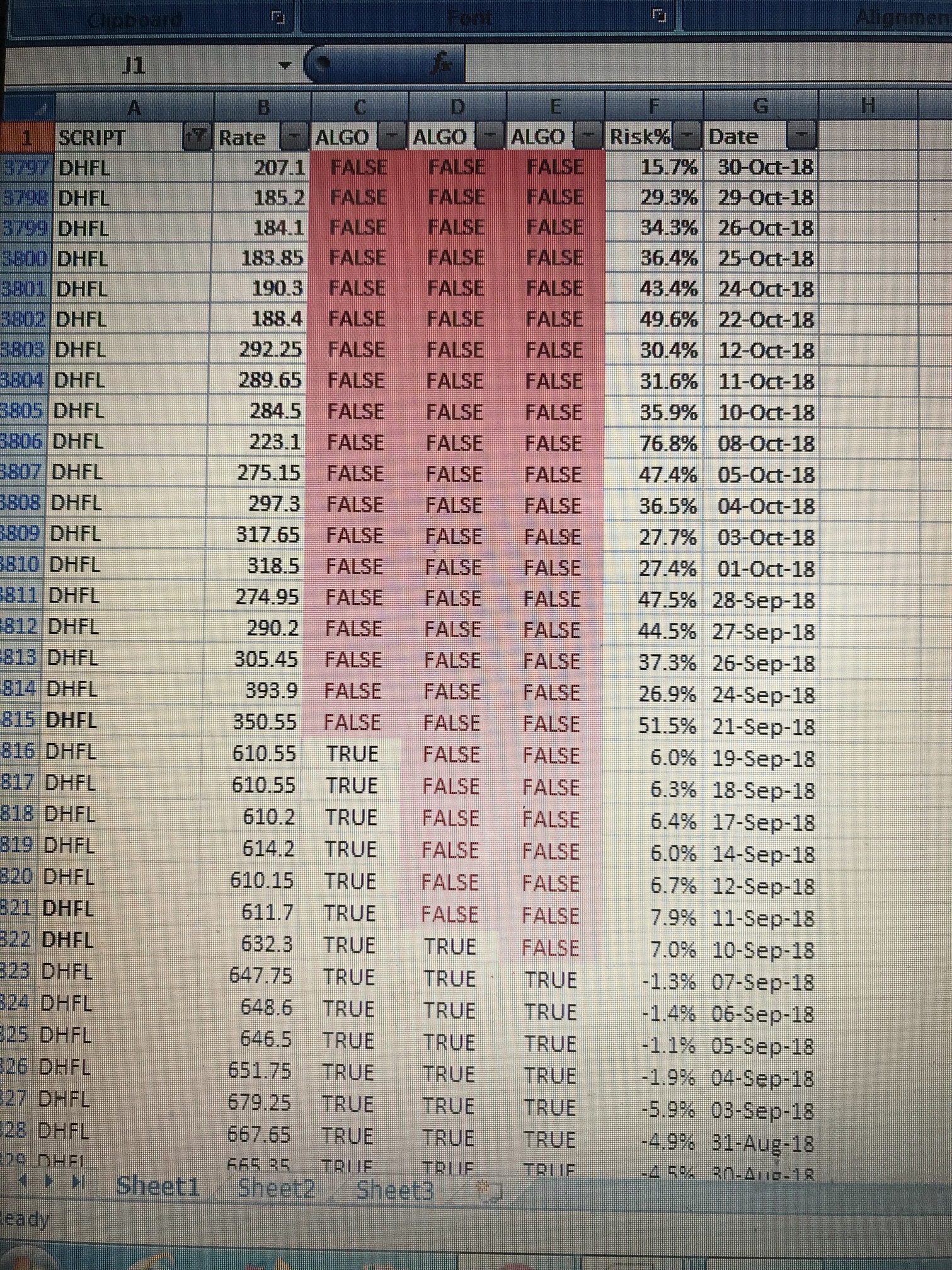

Please explain, I am interested. Give the story of one of your sold stocks, when did you sell it and what happened later, the price went up or down, did you buy the stock again later etc. Selling is one thing that bother investors more than buying, although if one is convinced in the company, one can hold till eternity.

1 Like

Hi ChaitanyaC , thanks for your query. As per my algorithm DHFL gave exit near 632 611 and finally at 350. Those who could sell have been able to save a lot. Again you also get buying it back signals. Sharing the report replica. This update is sent on email. Queries Welcome for other scripts also. You can mail your top holdings and we can send you Report for your group stocks. Happy to help who are interested. Thanks again

2 Likes