Thanks Krishna and Bhaskar. you are right. my bad.

My suggestion is …delete cyclical companies and No.2 players from the portfolio.And add some index funds in USA .For HUL vs Godrej Consumer Products, HUL is the market leader,so no logic for taking Godrej Consumer unless it have the 10x factor in its products…please read "Zero To One- Notes On Start Ups Or How To Build The Future " by Peter Thiel

@sanjay192 I have a different view on HUL vs GCPL. We can’t simply select a stock by just looking at one dimension “Market Leader” as stock price appreciation happens based on multiple dimensional factors.

At current price, HUL is valued at 13x sales and 75x profit and OP Margins are at peak 25%. If HUL successfully doubles it sales in next 5 years without significant margin contraction, it could provide decent returns to investors. We should think, how likely it is?

I’m not saying that “Market Leader” factor wouldn’t work, but thats not the silver bullet to look at.

1 Like

As matter of fact GCPL is market leader in insecticides business which form a major category for them. Leading market share in soaps/personal wash as well. Good growth in new categories it has entered. So depends on which category you are looking at. HUL is not a market leader in all categories it is present in. It is a leader in most…just like a Marico or GCPL or Tata Consumer or Dabur is…leader in most categories they present in…

You are right.“Market Leader” is an indicative term based on the parameters that have you mentioned.I am just saying that there is a huge gap both in sales and revenue in between HUL and GCPL and HUL against the similarities between them.

Yes You are right.HUL,MARICO,Britannia,Nestle all are market leaders in specific category.Interesting thing is that they are not competing with each other for the products from which they earn their market share.Each of the companies have some product portfolio which have 10x factor with them.But in my opinion I am unable to find the product in GOCPL which have 10x factor and has escaped competition and become market monopoly.

1 Like

They had insecticides, growth for which had plateued. Until recently many didn’t think even Marico had any such 10x categories but they kept their innovation in Foods and that got fillip in pandemic. GCPL is purely a Personal and Homecare company with no Foods division…rest all have elements of Foods and today Foods are doing well. Give time to right management and they will work for you. Protekt in Personal wash and now ProClean in Homecare can be future cash cows with lookout of extra growth in niches like salon brands, hair colour and other discretionary products…I agree today things seem little slow but that’s the case for all other companies operating in GCPLs categories…I believe they too will have their moment. If they can build a super insecticides category, they certainly can few more…

Disc. Not a buy/sell recommendation. Invested in FMCG companies like Marico, GCPL mentioned above

1 Like

Wow.You have already done a lots of research on GOCPL.Thanks for the valuable information.

I have never studied about their “insecticides” product portfolio.Now I will study it.

I had a hard time choosing between GCPL and Marico. I wanted to own only one . A big chunk of GCPL”s revenue ( close to 50% I think ) , comes from overseas markets . In past 10 years they have successfully entered these markets . Indonesia is on growth path . In Latin America and Africa they are at nascent stage.

HUL grows at 8-9% and I believe GCPL can grow revenues and profits at 12-13% over next decade . Seeing past performance, this looks likely. I could not convince myself that Marico will grow at same rate or higher rate than GCPL . Hence I didn’t buy Marico .

P.S. I read concall report of GCPL and it’s frustrating to see that almost all questions are dedicated only to Indian market. I assume that the analysts are too lazy to do research and ask questions on their overseas markers

2 Likes

You can reach them yourself by reaching their investment query guidance support.

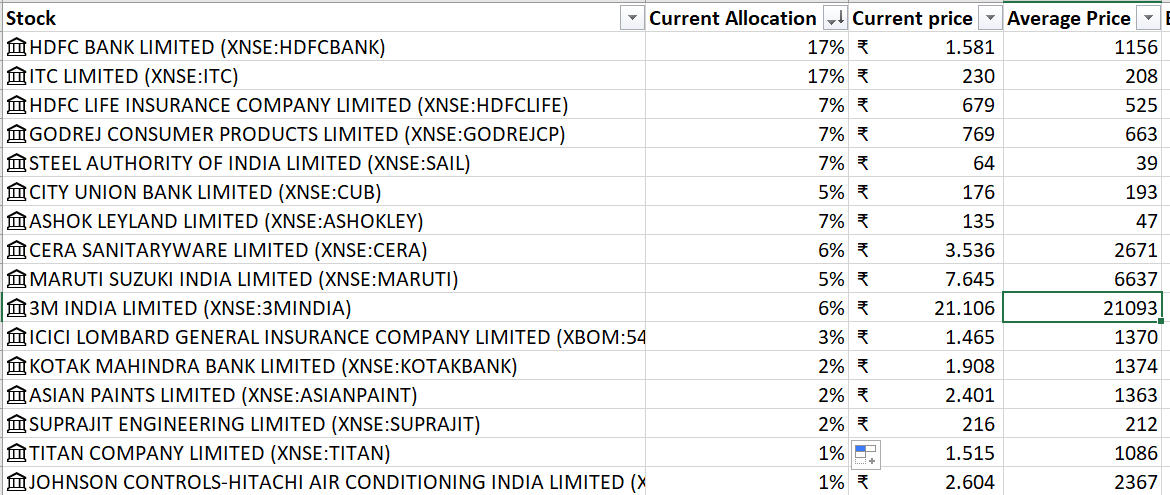

Portfolio update :

- Added small quantities of Cera, 3M , SAIL and ITC

- Added gold ETFs. 4% of portfolio is in Gold ETF now. close to 10% is in NCDs and 4% in Gold etfs now.

- New addition: Added Suprajit . Now 2% of the portfolio.

Why Suprajit?

- Good and lengthy track record over 10 years with consistent ROCE and ROE and decent FCF

- Conservative promoters

- Moderate Debt

- Decent valuation (Mcap/sales = 2)

2 Likes

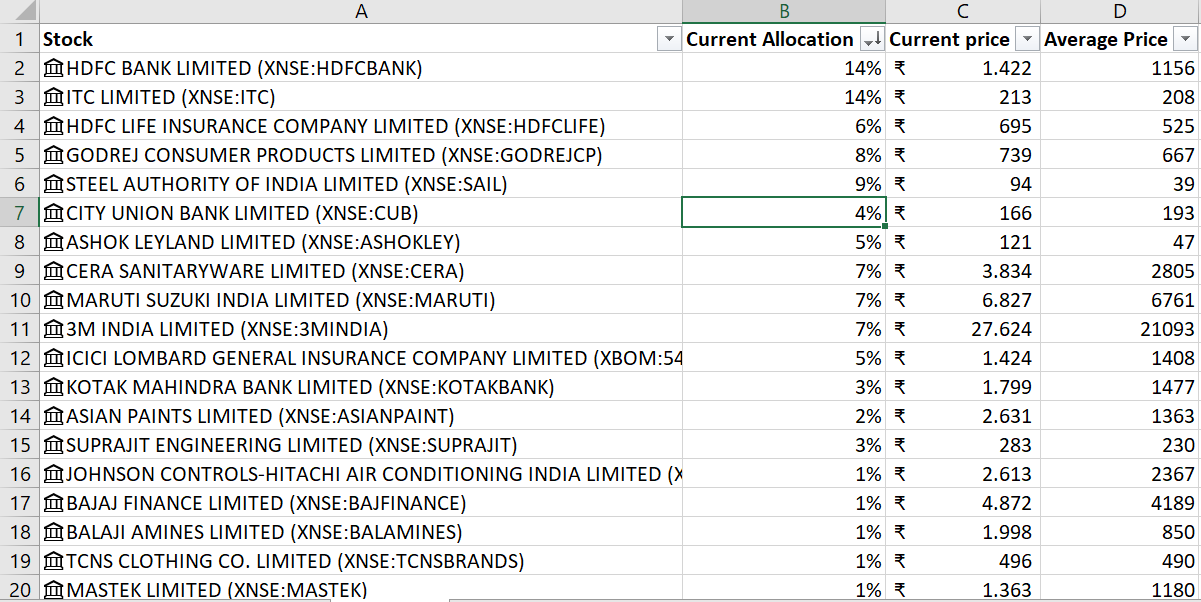

Some new additions to portfolio . all are having 1% weightage . i will track them and if i develop conviction, i may increase allocation.

- Mastek

- TCNS clothing - pure speculative play because some investor bought it .

-Balaji Amines - bought at 850 rs

Other additions

- Added 3M, Maruti, icici lombard in past 2 months as there was some price corrections

The allocation percentage remains largely same because some stocks have moved up and i have put more money.

2 Likes

Management has told that they are just allocating capital for ongoing projects and no further projects will be commissioned in Hotel line due to the low ROIC.

1 Like

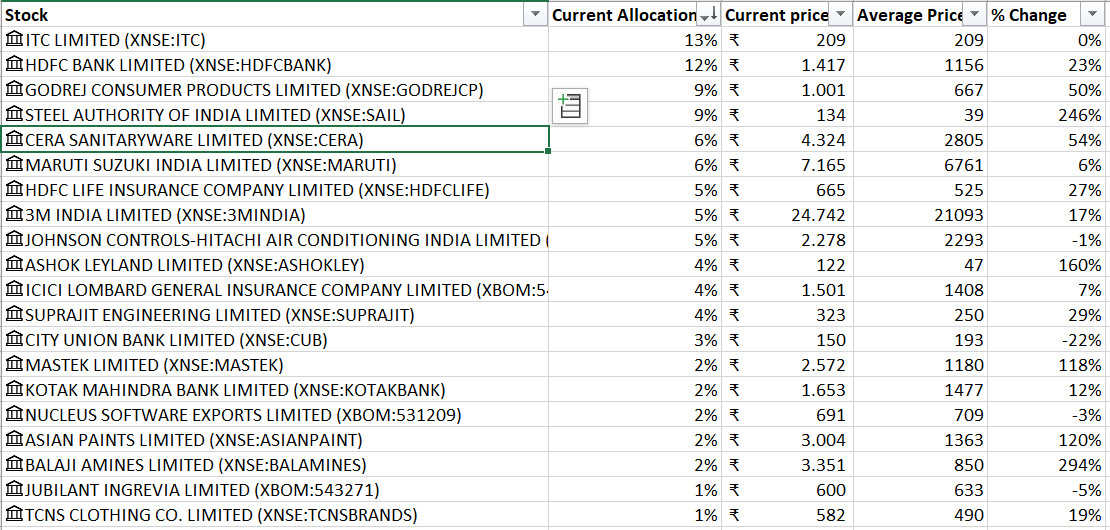

Here’s the update to the portfolio.

i am trying my luck at momentum stocks (5-6 stocks with <2% allocation ) and have allocated 10% of portfolio to those stocks. i am not expert in momentum stocks , just trying my luck and don’t want to have FOMO.

- in past 3 months , i have sold Hikal after making 3x in it. switched to jubiliant ingrevia.

- added Expleo after the recent restructuring news

- added Nucleus software

The following stocks are cyclical and i plan to exit them when it hits the target - SAIL target of 200 rs. Already sold 25% of SAIL.

- Ashok leyland - target of 200rs.

In the core portfolio, i am adding the below stocks on SIP mode every month. i plan to have this for long term and i have not sold anything in past 2 years

- Johnson Hitachi

-icici lombard - Kotak

- HDFC Life

- 3M

- gold bees

8% is in Gold and 4% in NCDs, 4% in cash.

Good to see someone other than me adding on to a consumer durables these days ![]() Out of all consumer durables, why you have chosen Johnson Hitachi? Why not a Whirlpool or a Voltas or even havells?

Out of all consumer durables, why you have chosen Johnson Hitachi? Why not a Whirlpool or a Voltas or even havells?

I wanted to own AC company and i believe that in the next 10 years, they may triple their sales.

My first preference is MNC and Johnson is pure AC play (residential + commercial).

i did try to compare Johnson vs Whirlpool vs Voltas, Blue star .

It was tough choice between Johnson and Whirlpool. Johnson being pure AC play, i choose it.

3 Likes