do you mean Life or General Insurance? Whats your thoughts on Life vs non Life in India?

I meant Life insurance . Chinese companies have market cap of around 40 billion dollars .

Over next decade or so , we should reach there . China still has good VNB and margins of VNB are quite high . Remember China has same penetration in life insurance as India. We should break into top 15 insurers in the world in next 15 years .

For non- life , there is no clean leader till now. HDFC Ergo is not listed , Bajaj Finserv is not pure insurance play. The only option left is Icici Lombard . As time goes by, small players will exit and consolidation will happen. Looking at US and western country, non life companies have done well during 80s and 90s. Also, there are lot of insurance products like lawyer insurance, home repair insurance, jobless insurance in west which will come up in India in future . Health insurance will become big due to increasing medical costs .

My strategy is just stay in there for a decade and stick to #1 . Don’t worry much about short term blips.

1 Like

Agree most points, In Non life, precisely only pure play listed option is ICICI. Waiting for Ergo to list.

Any reason for why non life did well in US in 80s and 90s and not currently? Also, I believe Life insurance in US is also stagnant since long time now…so is Insurance longevity of growth not that secular say as consumer/pharma?

Also, chances of companies going bankrupt seems more in non life where underwriting mistakes seem common in history e.g. how Gieco rose from ashes…what are your thoughts over bankruptcy and big trouble issues in Life Vs Non Life over long term?

Lastly, when you see so much growth and longevity of growth then why you not investing in the leader and waiting…dont you think valuations would catch up eventually? Thanks

1 Like

I assume that stagnancy for years happens when the market is fully mature . We won’t run into such problems soon.

But as you mentioned, we will see some downcycle in non life . One or two guys will go bankrupt ( just like ILFS, Yes Bank) . I have no idea how it will happen and in which form it will happen. Then we will know who is swimming naked

Non-life is a sector in itself and within that, there are different types which are too diverse and complicated. Since I am not an actuarial expert , I try to take very high level view and stick to leader which avoids most of the problems .

For life , I stick to HDFC life as it’s clear leader among private players. They are very slowly chipping away market share from others.

Regarding non-life , I have started investing in Icici Lombard and will slowly increase my allocation going forward . It would be interesting if HDFC Ergo lists .

2 Likes

I am not sure how the regulations were in US when Geico almost collapsed. However, currently, in India, insurance companies are regulated very tightly (perhaps even more than banks). The solvency margin is greater than 100%, which means the company has more than enough capital to pay each and every claim. Is there a possibility that things may break? Especially when we are talking of plain vanilla life term policy.

1 Like

Mr Surya Prakash,

You have invested in 16 stocks, which is in my opinion too diversified.

You mentioned you red Peter Lynch book. Peter stated that “Owning a stock is like having children. Do not have more than you can handle”

As per Peter you can have portfolio like this.

Slow/fast Growth stocks = 30%, Philips Carbon, IT, Pharma

Stalwarts stocks = 15%, Nestle, Asian Paints

Cyclical stocks = 15%, Jindal Steel, Hind Zinc

Turnaround stocks = 30%, Vodafone,

Asset Plays = 10% Bombay Dyeing

Please read Mr.Basant Maheshwaris book Thoughtful Investor. He is Peter Lynch of India.

1 Like

Hello.

Why you holding Sbi bonds. Even though coupon rate is around 9.5% if you are holding bond today you won’t make a dime till April 2021. As this is a callable bond, which Sbi might exercise call option in March given the current low interest rates,

For eg. the bond price today is around 10900 rsIf Sbi calls the bond in March you will get 10000 rs back in bond value and around 900 rs in interest.

If you sell the bond today at 10900 you can use the proceeds and get bank return for next 3-4 months.

This is just my opinion/ logic

Disc: held this bonds for long time and redeemed few months back.

what I suggest focus on basic process-

a. Focus on growing company

b. it must not have high debt, debt to equity to be remain below 1

c. free cash flow and cash flow from OPS must be >1

d. No pledging of the shares by promoters

e.look at product line and is there enough demand of its products and scope for growth?

there are a few more parameters too, which one need to focus for example ITC is burning cash on hotel business which means, market knows it and its not getting good valuation, look at its chart!!

I am not aware that these bonds are callable. But these bonds are there for quite long time ( more than 7 years ) and I don’t know any scenario where they were called . Thanks for the info . I will investigate .

Except for cyclicals , most of the stocks in my portfolio have very low debt. ( except GCPL . D/E= 0.5)

Also most are decent growth stocks ( not ultra-growth ones)

ITC “was” spending some amount on hotels , but i am sure that it was not too much. Hotels contribute to less than1% of revenues & 4% of profits. The company had always spent on hotels and the company still delivered good returns over period of 20 years . Since the stock is down, hotel is shown as excuse . The management has no intention to put more money in hotels . So it doesn’t matter now .

1 Like

this bonds were issued somewhere in 2011, the first call option was after 5 years which was in MArch 2016- where SBI did not exercise the call option reason being in March 2016 interest rates were around 9% which makes no sense to call the bonds. The second call option is after 10 years which comes in Mar 2021 - probability of SBI exercising the call option is high as the interest rates are around 5% now.

1 Like

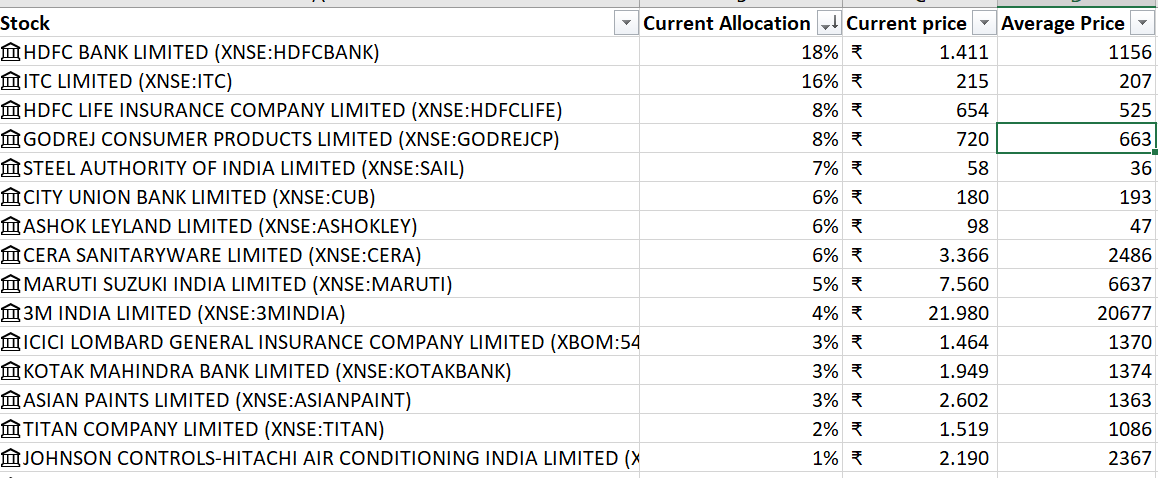

Here’s portfolio update . SIP for December done.

- No more adding HDFC Bank, ITC due to high allocation

- planning to add Cera, 3M or icici lombard for next SIP

- Want to add Kotak, Asian Paints but with recent run-up , it is difficult to convince myself to buy

- don’t want to add SAIL further

3 Likes

Excellent stock selection, your portfolio must compound well in long term. But 27% allocation for banks seems to be a risk to me, see if you could reduce it. Also keep an eye on Ashok Leyland and SAIL. both must do well in short to medium term if recovery happens as expected but you should jump out at some point.

1 Like

Thanks for the feedback

I don’t plan to add bank stocks . Also for Ashok Leyland and SAIL , I am waiting for auto cycle and commodity rally.

I plan to exit when it happens .

2 Likes

My comments are only for 2 stocks and advice on NCDs:

Ashok Leyland and Maruti

–> I will suggest VST Tiller , Hero Moto, or M&M for above 2. or go for some tyre or battery company as both those compnies will continue to be in business for next 50 years when you see EVs everywhere. M&M has better angle on EV technology and it has pie in both CV and PV vs Leyland ( pure CV)

for NCDs -->

- Its risk reward ratio is not favourable.

- Interest is taxable so if u are in highest tax bracket- it will be at 30%

- u get 7% on savings bank account ( IDFCFirst) with ample liquidity and 40K interest is nontaxable.

- SBI PP bonds give yield of 7.74% pre tax so i dont see any logic for going in NCDs.

- go for some Debt MFs instead which can get you better returns than NCD while derisking your investment ( albeit watch out for Franklin Templeton-esq type of MFs) and if u opt for MF, go for direct plan

1 Like

You mean 10k?

Under section 80TTA of the Income Tax Act, from all savings bank account, interest up to Rs 10,000 earned is exempt from tax. This is applicable for all savings accounts with banks, co-operative banks, and post offices. If the interest earned from these sources exceeds Rs 10,000, the additional amount will be taxable

Whether it is NCD or Bank FDs, i have to pay tax and hence 10.4% SBI NCD is better than 7% FD with a small private bank. Moreover, i buy only SBI NCDs which i assume are less riskier than small private bank FDs.

Debt MF are also an option, i will check out. The main reason for allocating some amount in NCDs is that during times of crash, i can move some money from fixed instruments to equities. During March crash, i was doing my monthly SIP, but didn’t have extra cash to put money in equities.

As the market inches higher, i plan to add fixed instruments going forward and increase the allocation going forward.

As per section 80TTA deduction of Rs 10000 is available for all for interest from Savings account,this does not include FD.

While the interest is taxable,the bank will not deduct TDS till Rs 40000 FD interest but for the tax payer it will have to be added to income and tax paid accordingly as per slab rate.

As per section 80TTB,Rs 50000 deduction is available to senior citizens(age>=60) for interest that accrues from SB as well as FD.

Yes. No TDS does not mean its not taxable.