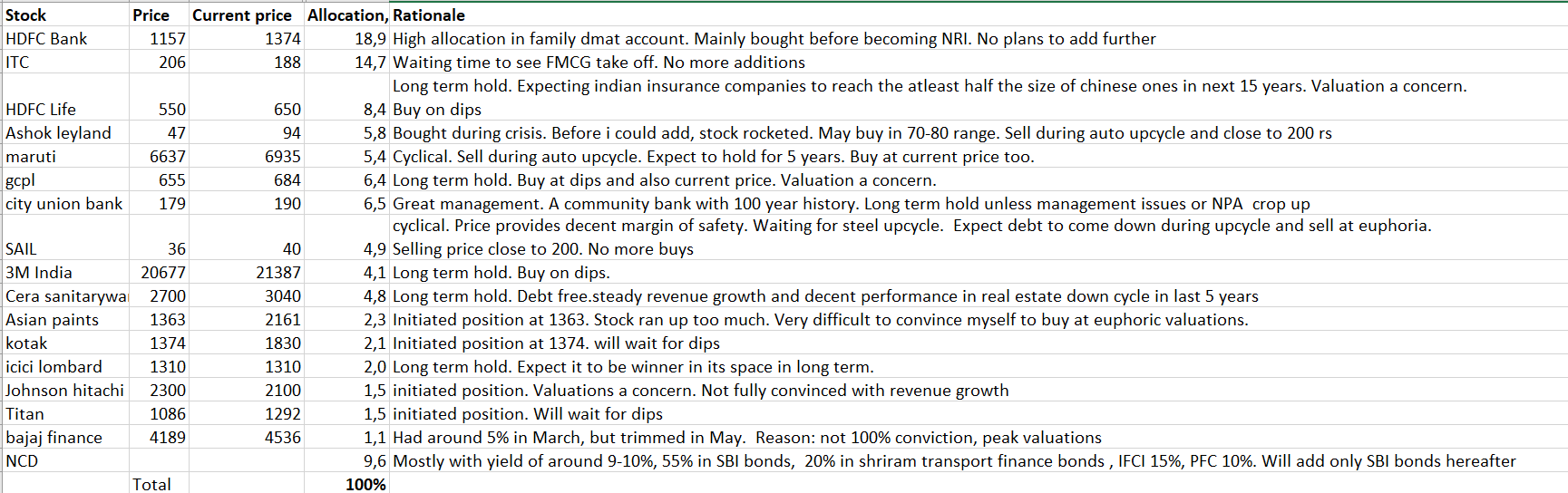

ASIANPAINT

Market Leader/Zero Debt Company/Free cash flow/Organic Growth opportunity.Handsome Margins.

sourabh mukherjee mentioned that Asiuan Paints have no distributors in between the retailers and them.I will check whether this is a fact or not.If yes,then I wil increse my investments gradually

I will listen to the analyst conference calls of the company

BAJFINANCE

An excellent NBFC,which focusces on small loans like mobile phones,Electronics goods etc.They also focus on giving personal loans to professionals who are not salaried but have excellent cash flows (ex-Doctors,Cas etc.)

BRITANNIA

Daily Essential product/Market Leader/Having brand loyalty i.e. if I want to buy “Britannia Marie Gold” at the Groceeries store and the shop keeper offers me anothger brand,theny I will go another store and to buy the biscuit.This makes the company to create entry barrier and the can company has the pricing power to maintain its margins. But in airlines company I will go to who is offering lowest price because brand loyalty is not there.

I checked the profit loss and balance sheets every quarter.If I find any concern there ,I carefully listens the analyst conference calls to check whether Mr. Varun Berry is answering that or not.Example-In FY21-Q2 result ,I found that short term borrowings are increased significantly than the previous year.But ,In the conf call Mr. Varun Berry mentioned that ,the raw materials prices were decreased so they bought the full year’s raw materials with short term borrowing.

CDSL

Huge Organic Growth opportunities are there/Zero Debt Company/Low Market Cap/Entry Barrier is there/Only one competitor/Lots of free cash flow.

I checked the conference calls.The management is acting like Govt organisations.They are avoiding questions on competition,eating growth opportunities etc.For checking future growth of CDSL, I checked what demat account the new broker PayTM Money is offering.And I found that by default they are offering CDSL’s demat account

Mr. Nehal Vora is playing very conservatively.Personally I think CDSL is not using technology efficiently like ZERODHA to eat the market oppertunities. Check its platforms like Easi ,Easiest etc.From the apps you can get a light picture of Management’s vision.I am not saying to involve in competition with NSDL.What am I saying is that ,if only 4% market share is eaten and rest is left,then why not going aggressively.Indirectly Mr. Nithin kamath of ZERODHA has lots of contribution in the growth of CDSL.

Still I am unable to understand what % of its total revenue and margin CDSL earns whe we sell shares.

HDFCLIFE

Good Management/Organic Growth is there/Shifting of Market share from LIC is also there.

HINDUNILVR

Market Leader/Zero Debt Company/Free cash flow/The company will remain there for next 100 years/Brand Loyalty is there to create entry barriers.

IDFC

Bought it on recommendation and holding it as I bought it on low prices

IDFCFIRSTB

The bank is becoming retail oriented.And is running on the vision of Mr. V. Vaidyanathan. But still investing at present means “investing in hope”

I am checking the quarterly results of the since last 1 year.The bank is posting profits since last 2 quartes .But what I am tracking that what Mr. V. Vaidyanathan is saying ,is he doing that or not ? And I am satisfied with that. For checking more about the bank ,I opened an account with it.I checked its app/net banking ,it is super easy to use.It means who ever is handling the technology segment in the company has the vision about ,what customer want from apps.In comparison with other Pvt banks platforms,Federal banks platform is pathetic .IDFC first banks platform is way better than Federal Bank and Bandhan’s.I went to electronics retailers shops and saw IDFC first bank’s advertisement s there ,but not found Federal bank,Bandhan Bank,SBI Kotak there.It means IDFC bank is working with brand marketing with consumer electronics like HDFC bank.

INFY

Market Leader/Tons of free cash flow

ITC

Buying from Rs.300 level.I am still holding it as a victim of behavioural finace crisis.Otherwise no reason to hold.

Lots of problems with the company.I mean simple fundamental to think ,who burns free cash flow to make hotels,as if net profit from hotels will double every 2 year.One good talented man created the business in Itc,and the management is eating it.I visited the kirana stores to inquire about the ITC’s products.They told that ITC’s products are awesome and customer demand it.But the company is not providing the quantity what they demand.It means ITC has distribution problems in its FMCG business.ITC has lots of heads of business i.e. Cigarettee business head,Dairy and biscuit Head,Personal care product head etc etc. It is more interested in creating cadres than business. ITC’s management is not focused at all.

.

LALPATHLAB

.Market Leader/Low Debt /Free Cash flow /Shifting of market share from unorganized to organized sector/organic growth/brand loyalty/entry barrier

I am checking the quarterly results and conf calls since last 2 quarters and satisfied with the vision and honesty of the management.

PIDILITIND

Market Leader/Low Debt /Free Cash flow / organic growth/brand loyalty/entry barrier/Zero competition

RELAXO

Market Leader/ organic growth/brand loyalty/entry barrier/Shifting of market share from unorganized to organized sector

TATACONSUM

Added to keep track of the business

TCS

Market Leader/Tons of free cash flow

MARICO

Market leader in its core products like Hair oils,Sunflower oil etc.Settled business in growing economies like Bangladesh,Vietnam etc/Zero debt/ Company is fully focused and excellent capital allocator. Management is transparent and honest.

checking the conf calls and satisfied with the strategies,vision and honesty of Mr. Sugat Gupta.

we are either in a situation like 2009 where markets topped 20k and then fell for years or we are in late 2002 when the big bull run started .

we are either in a situation like 2009 where markets topped 20k and then fell for years or we are in late 2002 when the big bull run started .