The Ken did a story on Poonawalla Fincorp last week. It’s behind a paywall, but here are the four key summary points.

Poonawalla Fincorp, born out of a merger between Poonawalla Finance and Magma Fincorp, recently registered its best-ever quarter. And the credit goes to a makeover.

The company has taken Magma Fincorp apart brick by brick to rebuild it with a retail and digital product suite and a new set of urban, more credit-worthy customers.

Instead of investing its energy and monies in collections—as Magma Fincorp did—Poonawalla Fincorp has created a tight entry barrier for its customers. But in the process, it has been leaking old hands.

Throughout 2022 and early 2023, the company witnessed heavy attrition. So much so that there are only a handful of senior Magma employees left in the company. Mid-level Poonawalla employees are quitting too.

Multiple startups are co-loaned by Poonawala Fincorp, according to the market. I need assistance finding a list of startups that Poonawala co-lends to.

It is interesting to observe that if they materialize the guidance,

They have guided 30 to 35% growth of profit for at least 7 years.

(Armaan finance guided same for coming 3 years)

Next 3 years of no capital raise.

They are leveraged less than 2.

Operation costs are on steep decline as from 300+ branches to reduced till 89 due to tech Focus.

Valuation wise available at Price to book value of less than 4.

MSME has the Highest Yields compared overall with Other NBFCs (Armaan Financial is having yield of 36.1% & NNPA =0.4, with Poonawalas Cost of Capital at 8% NIM stands at 28% if success like Arman is replicated)

For point 6 No claim that Poonawala can make 36% yield, but NIM can be much high is the point I am trying to make.

What inferences can be drawn here?

Nothing wrong came out regarding the company. So I don t think there is much to worry here. A person can express his desire to move out of operations and that s what the erstwhile MD did. It should recover unless he got more shares to get rid of. He might require funds for his next venture which he thinks would be more profitable than sticking to poonawalla. From investors perspective what matters is to see if there are better and equally reliable alternatives. If not, better to stick, else take a calculated risk and move. The fall has been more than anyone anticipated perhaps, but all is not lost either. I didn t see any red flag yet.

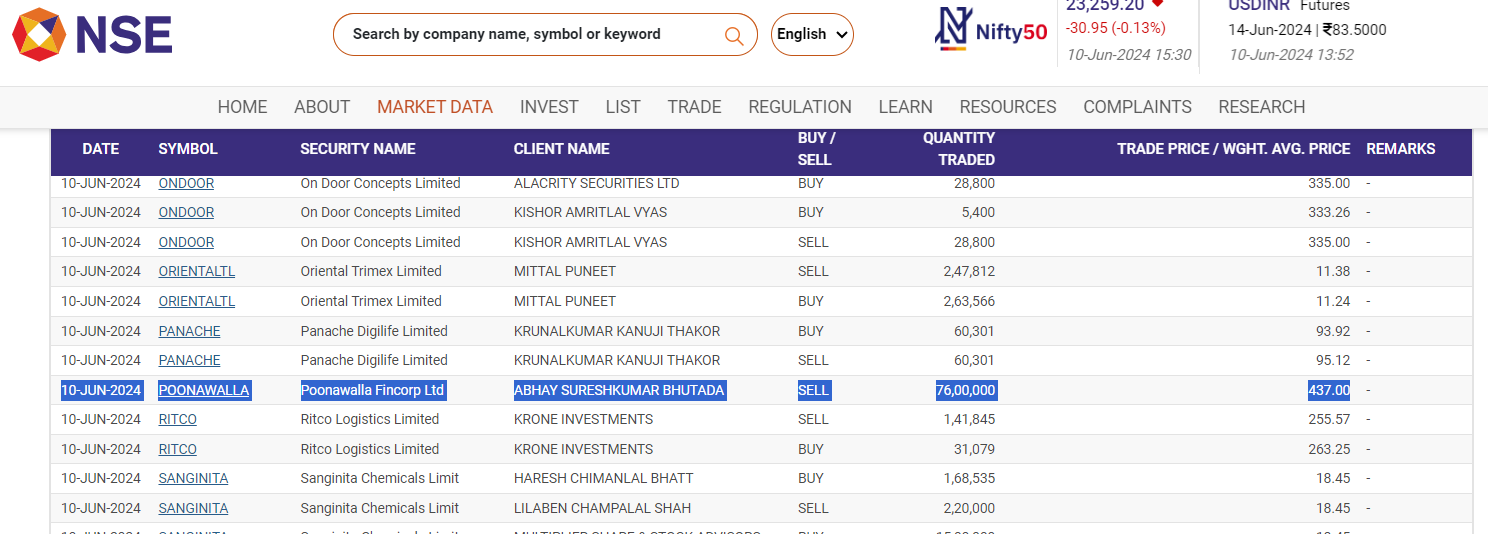

Promoting Abhay Bhutada to group level is not a promotion but a way to shunt him out. And that’s clear from the way he sold a big quantity. He of course said in the latest concall that he was never interested in managing day to day operations since he is a serial entrepreneur. He would focus in his next start up, whatever that be.

As far as I remember, in the interview Mr Abhay said that he himself wanted to be promoted and the poonawalla group was not with him on this and he had to convince them for the same

True I have also heard that in concall also, but being in this industry so far I understood that this is a technique used by most of the people from corporates to save their image.Companies also use it to save thier reputation!

Arvind Kapil seems to be new MD &CEO … Currently, Kapil is serving as the group head of mortgage banking business at HDFC Bank and manages a book of over Rs 7 trillion. He also handled the merger of HDFC and HDFC Bank. Looks the Poonawala is in safe and experienced hands. Any views ?

Poonawalla Fincorp Ltd. reported a 45.6% rise in its net profit for the first quarter of this financial year.

Revenue increased by 40% year-on-year for the three months ended June, reaching Rs 996 crore.

Assets under management for the company grew by 52% to Rs 26,970 crore for the April-June quarter, the investor presentation said. The net interest income rose 42% year-on-year to Rs 676 crore.

The gross non-performing asset was recorded at 0.67%, down 75 bps during the same period last year, while the net NPA fell 44 bps to 0.32% during the quarter.

I want to know what are the reasons for recent fall in the stock prices if any despite good results and excellent asset quality. I understand recent changes in management on a large scale are also one of the reasons of the fall but i believe the new management is also of high standards. They have shown their ability in HDFC and are not just any random guys. So want to understand what is the market fearing about!.

They also gave a five year vision for the company.

Another thing i want to share, if its the rejig in management then we should look at a similar case that happened in birlasoft(though a completely different industry). Mr Dharmendra kapoor who was the MD was removed after he scaled the company and was replced by Angan Guha who is a Wipro veteran(he headed americas division for wipro and was responsible for more than 30% of its total revenue). Since Mr Guha took over, the company did remarkably well and we can see it was followed by share price too which went from 250-270 to 850. I know its not the same but there is a possibility of similar thing happening in a few years if the management walks the talk.

As per my understanding the fall in share price is because the perception of the street changed as the earlier management guided for low OPEX and no expansion in branches for next 4-5 years. And the new management is emphasizing on more branches which will increase their OPEX cost. I think the Pedigree of the new management is much better if not same than the earlier management and as they walk their talk the market will again rerate this stock. I am very confident that this stock should start performing from here as the Interest rate cut is around the corner. If one is looking to play the NBFC theme this is one stock to look out for!

In my view fall in stock price could be due to one or more of the following factors:

1- Technical- If you look at stock price movement over the last 3 years, it tends to correct 20-25% after making new ath. This time around, the correction has been the steepest at 30%.

2- Insider selling- Heavy insiders exits in the last 2-3 years have been an overhang which has been disrupting stock price momentum so there might have been anticipatory profit booking after the last rally.

3- Valuations- Before Q1 results, stock was trading at almost 5 times books which might have also contributed to the correction.

4- RBI action- Credit squeeze engineered by RBI has created some uncertainty over NBFC’s earnings.

Poonawalla reported a loss of Rs 6.3B due to one-time provisioning of almost similar amount against its stpl portfolio. Came out of nowhere, without any warning in the previous quarters.