Magma Fincorp AR 2018

Result seems to be very good…

PAT up 75% to Rs 68.1 Crore, Disbursement up by 25%

NIM up by 100 bps, NNPA falls 37% to 4.4%

Not invested

1 Like

Magma press Release on Q1 performance

Revenue flat. Lower provisioning (Y-O-Y) saved the day.

If the disbursement went up, how come the topline is same?

Q1 FY19 Concall summary (source: capital market)

The company has exhibited strong performance on all fronts in Q1FY2019. The company recorded PAT of Rs 68.1 Crore, up 75% over the corresponding period last year.

The company has posted healthy 25% growth in the disbursements to Rs 1840 crore for Q1FY2019. The loan book of the bank has increased to Rs 15966 crore end June 2018 from Rs 15848 crore end June 2017.

The company has targeted the disbursements growth of 25% and loan growth of 16-17% for FY2019.

The net interest margin of the company has improved 100 bps yoy to 8.6% in Q1FY2019, aided by lower cost of funds and higher earning assets. The company expects to maintain NIM at current level in FY2019.

The company expects to contain the operating expense growth at 15% for FY2019.

The company has transitioned to Ind-AS accounting during the quarter. Company’s NNPA (Net Stage 3 Assets under Ind AS) stood at 4.4%, a sharp improvement from the level of 7.0% in the corresponding quarter in the previous year.

The company expects to continue improvement in asset quality and reduce credit cost below 1.5% in FY2019 from 2.7% in FY2018.

The company expects higher loan growth and dip in credit cost to boost RoA to 1.8-2.0% and RoE to 13.5-14.5% in FY2019.

The company has increased provisioning on standard assets under Ind-AS from the earlier mandated 0.40% to 2.65% end June 2018. It is expected to reduce the volatility in future earnings and pave the way for impressive growth in the current and future years.

With the normal monsoon and increased MSP for crops and higher outlay for rural markets by the central government, the company is poised to achieve higher growth in the coming quarters and will take full advantage of the tailwinds.

The disbursements in the asset backed finance (ABF) segment has recorded an impressive 23% improvement to Rs 1348 core in Q1FY2019, driven by growth in Commercial Vehicles Finance (139%) and Used Assets finance (27%).

The company has moved its 61-90 bucket collections for its ABF business from the business team to the collections team, and expects that this change should bring further significant improvement in its collections efficiency, and which shall result in NPAs reducing further during the year.

The Company has significantly transformed its mortgage business and deeply embarked its journey to become national level affordable housing finance company. The company’s home loan disbursements surged 142%, while the direct origination continued with its upward journey which now stands at 67% as compared to 24% in Q1FY18. The overall mortgage and home finance disbursement increased 24% to Rs 160 crore in Q1FY2019.

The Company continues to focus on its SME lending business resulting in 34% increase in SME disbursals to Rs 333 crore in Q1FY2019. It has been one of the most consistent performing biz and the company hopes to build on it further by penetrating deeper in the tier 3 and 4 towns and has planned to open 20 more locations in the coming quarter and extend lending to micro and small enterprises.

In the General Insurance business, Magma HDI registered strong growth of 62% in GWP to Rs 193 crore from Rs 119 crore in corresponding .quarter in the previous year. While Motor continues to be dominant portfolio for the Company comprising 72% of its business, its Commercial business portfolio achieved 81% YoY growth in the quarter. The Company continues to enjoy one of the lowest Own Damage loss ratios in the industry coupled with best in class customer service experience to the customers along with creating building blocks for our Health business.

With regards to floods in Kerala, the company has exposure of below 5% of loan portfolio in Kerala state. The company has employee base of 400 employees in Kerala with 14 branches. Product wise, the company has presence mostly in passenger vehicle and commercial vehicle segment, while the presence in SME, tractors and construction equipment is in significant

11 Likes

Magma Fincorp Ltd

Highlights of Q1 FY19 results

- Key Initiatives

o Rebuilding product mix in ABF , Focus on Affordable Housing, Building Highly profitable SME book and High performance Insurance business, Looking in investing in a strong customer service platform and making significant investments in people at MD level.

o Collection efficiency to maintain the portfolio quality . Company have dedicated collection team for Tractor , Housing and SME . Company also have dedicated team with 60+ TPD. And the NPA portfolio across all products. Business is done in AWMI and CPMI indices . Branch and zone grading benchmark has been introduces and reward link to portfolio quality are being placed this has resulted in Non-Performing Portfolio declining substantially and result in a healthy growth across business.

o In EVF company has decided to focus on higher weightage of commercial vehicle and used efforts with the reduction in the company tractor portfolio to ensure that company portfolio quality continuous to drag better that will continue to deliver healthy NIMS.

o In Housing company decided to build its portfolio from its own channel and reduce the dependence on LAP and DSA business.

o SME was the best performing portfolio for the company where company is focused on lower tier locations like location number 11 in huarache in terms of business potential for company to build on a existing product and reach.

o In General Insurance business company was able to build strong OEM relationships maintain leadership in motor business with the best OD loss ratio in the industry with best in class service with the customers and creating building blocks for company health business. Most investing is done in human capital . Company business like Insurance and Mortgage are lead by fully powerful CEO and their business team are fully geared to achieve their business plan.

o Company has made substantial investment in skill development system from the top level to the front line member of the team to ensure that company have a full team running in synergy and perfect collaboration to achieve the financial goals.

o Company have transition the IND-AS in the quarter , Biggest change was provision for ECL which will significant influence on how company will do business. The industry will need to upfront the expected credit loss as it response any deteriorate in portfolio quality at immediate .

o Changes happen due to IND-AS

On Asset quality company had made higher credit loss provisioning under ECL regime . Stage3 asset equivalent to NNPA has significantly reduced and now stands at 4.4 % compare to 7 % last year same quarter

Company PCR for stage-3 asset stands at 56 %

Early warning indicators shown improvement of 25 % yoy and containable portfolio EMI which reduced by 43 % YOY.

Disbursal has grown healthy by 25 % with a marginal growth in loan book and company is now at the high lend of underwriting and it will reflect in loan book growth of 17-18 %. Therefore company see improvement in the stage three ratios in coming quarters. - AVF business

o Disbursal grew by 24 % YOY this was inline with projection and led by commercial vehicles with 139 % followed by used asset growth at 27 % . Focus is on customer satisfaction and consistent approach to direct customer led in growth of direct disbursal to 40 % compare to 33 % in same quarter last year.

o Productivity levels has quite improve significantly over the previous year as the number of cases on an average at 3.22 units as compare to 2.38 units same quarter last year.

o In current quarter company have moved to 90 collection from 60 collection team. Company expect further improvement in the disbursal and operating efficiency with this move - Mortgage business

o Company has transformed it to become the national level of affordable housing finance company

o Company HL disbursal grown by healthy 142 % yoy with the average annual ticket size of 10 lakh . LAP disbursal were down by 14 % YOY. Direct contribution continue and now stood at 67 % compare to 24 % same quarter last year. Company now have 316 people for business origination and 247 dedicated to collections. - Unsecured SME

o It remains to be an excellent business for company with 34 % increase in SME disbursal this was in back of Christ focus in country locations and tier-2 and tier-3 cities. Company had launch product for informal segment of customers and intend to expand products starting with pre-approved offers for large existing customer base . Company is working to provide Fin-tech base solution for micro and small enterprises in this vertical. - General Insurance Business

o Company registered steady growth of 62 % in terms of gross premium . Combine ratio of premium collection and Volume together increase by 7.8 % over the same quarter last year which was 117.8.

o Motor continues to be the dominant portfolio for insurance business. Contirbution mix remain at 72 % compare to 76 % last year. Company enjoy one of the lowest domination loss ratio in the industry. Company has added new corporate client in the quarter to achieve 81 % growth in the business over last year.

o Business is doing good with OEM and Banca tie-ups and looking continuously for new partnership and new product to diversify the portfolio. - Financials under IND-AS

o Disbursal grew by 25 % from 1473 Cr to 1840 Cr YOY

o AUM grew by 15,894 Cr to 15,966 Cr YOY

o NIMS grew by 100 bps from 7.6 to 8.6 YOY on the back of lower cost of funds ,raise of fresh capital and product mix

o OPEX to AUM is at 4.2 against 3.6 previous year. It has grew by 15 % YOY on absolute amount while disbursal amount has grew by 25 %

o NPA in three stages had decreased from 7 % to 4.4 % on a like to like comparision company PCR significantly improve to 56 % . ECL provisioning at stage-1 and stage-2 stands at 2.7 % compare to 3 % last year.

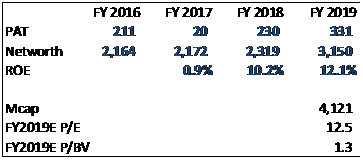

o PAT on consolidated basis grew by 75 % increase to 68 Cr compare to 39 Cr compare to last year same quarter.

o ROA has improved from 1 % to 1.7 %.

o ROE has improved from 8.9 % to 12.2 %.

Q&A - What would be the going forward trajectory under PCR ? Going forward will the percentage would reduce in tractor loan and mortgage or it will remain same ? Is the profit under Insurance business will be sustainable going forward ?

o Under IND-AS company has to make a provision not only for the NPA but also for the standard assets and it is not per minimum mandatory 40 basis points but based on the historical performance of the portfolio of the company. So company has look past 7 year performance and geography and than evolve at what is the stage-1 and stage-2 for the standard asset provisioning that company want to do and what is the stage-3 which is the NPA provisioning that company need to do. The provisioning that made by company will result in absolute consistent performance going forward. After adopting the new business method from December 2015 80% of the standard assets numbers improves under EWI and the CPMI by 30 % and 45 % respectively so the credit cost in future will come down substantially .

o Under Insurance business company has constantly adopted a policy that company will follow a profitable growth path and result of that company have earned least amount of capital than any private insurance company under 20 Cr. Company has to grow quickly but not at the cost of profits therefore company don’t expect to get any hit from the insurance business into the P&L account of parent company.

o Company want to increase the weightage under mortgage and reduce the weightage under LAP and want to increase the weightage of home loan and within home loan company want to increase direct sourcing compare to DSA to reduce the minutes of foreclosure because they keep shopping around and take the customer to other HFC. About a year ago less than 30 % of company sourcing was direct and now it is more than 60 % in the first quarter of current year and within that again in the month of June it has cross 70 %. So company is ahead of plant for the year where company wanted to reach 70 % for the direct sourcing. So Mortgage business will grow in terms of PIE of company AUM.

o Company is going to a product re-alignment with profitable growth strategy in the AVF business well . There company find that tractor business is largely depend on Vivaries of monsoon and company give loan for an average period of 4.5 year and it has been typically seen that in the block of 5 year at least one or two drought come and hit due to deficiency of monsoon and that does impact the ability of the customer to pay the installments, Therefore company decided that company would like to reduce the tractor loan business and move to LCHV to maintain the growth of 17-18 %. Going forward tractor on overall basis will carry a low weightage. Company don’t see impact on OEM on increase on impact of capacity. - Did company see any impact of the flood that is going on in Kerala in the general insurance business ?

o Significant part of portfolio is reinsured and therefore anyone can get the claims under re-insurance although company has to take care of the people who has been impacted by the natural calamity but one will get the money back from re-insurance . All the insurance companies make a provision of one-two such events every year and therefore company has made it for the same so it is unfortunate that in India there is one or other natural calamity impacting one or the other state but company keeps the sufficient provisioning for the same. Company exposure is largely in north followed by west and than eastern than south. - On ATF vertical company have tenure of 40-45 month so that show that 25 % of the book must be repaid during the year and it forms the majority chunk of the overall portfolio so how company is planning to scale up the overall loan book ?

o Company is coming to the end of the higher growth which was in FY15. From last three years company disbursal growth has slow down and now it started growing and result of that the run off of the older portfolio is still higher due to which the AUM growth is marginal related to the growth in the disbursal. In AVF if one has 25 % growth in the disbursals than company AUM should grow in the range of 16-17 % and that will be seen in case of all peers and which is what company expect that AUM growth will be 15-16 %a and disbursal growth will be 25 %. - How do the company see profitability increasing going forward because of rate hike coming forward ?

o Cost of fund of company will only increase by 10-15 basis point. Last year company cost of fund was on a declining trend so where company has started with high and end up with low therefore the rate of interest for last year same quarter is higher and cost of fund is largely likely to be stable . Company is going to get a increase in AUM and that will give company additional net income margin at the rate of 8.6 % of cost.

o NIM is adjusted for the originated income which is amortized , Brokerage and commission are also amortized. NIM will be in range of 8.5 % for the year. Credit cost will be decrease sharply from the level where it is right now because company 90 plus assets have decline over year and the decline continues also today . Company old portfolio which was originated before Nov-15 in that portfolio company NPA has been back by almost 15 month and there after the NPA has been declining. Company new portfolio is substantially better . Company NNPA which is 4.4 % will see substantial reduction going forward in coming quarters. These factors together will bring down company cost of fund below 1.5 %. - In AVF segment company has given maximum loan in Vehicle segment like two wheel or four wheel so now by increasing crude oil price and rate hike in interest what will be the impact going forward ?

o Interest rate rely on customer and yes these are the two headwinds but company is optimistic on the sector going forward. - How is the South region loan book doing as there is flood in Kerala ?

o Right now company is just praying and working for safety of company own employees over 400 employees working in the state of Kerala . Company don’t have SME present there too much and company business in AVF is largely on the passenger vehicle under LHCV and company don’t have any tractor loan there and in term of construction equipment. In terms of the weightage the overall portfolio of the Kerala is below 5 % in overall portfolio on national basis. So whatever impact come company will absorb it and evaluate it. - What is the reason for the EWI increase on qoq basis ?

o Must look it on YOY basis and very good tracking of EWI is seen and it is growing substantially and it is completely under control.

o EWI is 0 plus at the end of one quarter while CPMI is an average of CPMI 1-2-3-4 so CPMI is a longer duration index and CPMI has been trending well and even in the current quarter it is decreasing . Now overall in EWI the number is zero plus and in this industry the first quarter is the worst quarter in terms of collections. So company don’t give too much weightage from march to June because this was expected and quite usual and compare it with the last year . Last year it was 10 and now it is 8 so there is a 20 % improvement and this trend will improve going forward. - Why company GNPA has increase from 1000 Cr in last year same quarter compare to 1600 Cr in Q1 FY19 ?

o Last year company was having PTC securities book completely outside and therefore if there was anything in 90 + DPD it would be completely outside . Credit cost comes through a method of Accept Interest rates . If some installments has gone in zero plus company will receive lesser interest rates so that was the treatment so this 90 plus was securitized and the number was not included. However after IND-AS come in the securitize portfolio has come into book and whatever 90 plus was residing that is added to current portfolio. So that number is in range of about 100 Cr.

o Earlier company was not paying interest on 90 plus but after IND-AS company have to first provide interest and then make provisioning. So that amount of GNPA has also come in due to which there is an 70 Cr difference. As per I-GAP company GNPA was 1117 and as per IND-AS it is 1422 Cr . - What led to change in the AUM growth as there is an addition of 800 Cr because earlier it was 50,000 Cr and now it moved to 50,800 Cr ?

o Additions are

Interest on NPA assets getting added

Brokerage and commission which earlier was come as a separate item now it is adjusted with the AUM

Origination cost which effort is actually reduces. - At what point company will get stagnant in terms of OPEX ? Give some brief on drivers for operating leverage ? There is an impact of 154 Cr on effective interest rates so what is going into that number ?

o OPEX has grown by 15 % in absolutes terms in the first quarter on the back of the disbursal growth of 45 %. So operating leverage has already started kicking in from the initiative company was working from past 10 years and now it is coming down. Company entire focus is on improve productivity in which company have moved in by 2.5 % basis point per month to about 3.2 % per month compare to same quarter last year. The lag effect that company was use to have until FY15 is now at the tail end because it is total to 44 -45 . So from now onward the disbursal growth of 25% yield to a AUM growth of 16-17 % and from the time when OPEX growth will be less than AUM growth than company will start generating the operating leverage. On top of that there are several initiatives and efforts made by the leadership team across business to improve the productivity . So that will be the next level of operating leverage that comes in and that company expect on the next year. So this year company have a AUM growth of 16-17 % and OPEX growth of 14-15 %.

o Effective interest rates affect on financial assets and financial liability of 54 Cr negative number is what company is referring to and effective interest rates under IND-AS in the interest income one has to include amortized upfront income and exclude amortize brokerage and commission which company has pay on origination cost. In past company use to amortized subvention income which company use to receive from OEM. However company use to upfront any income which received on account of management fees as company adjust the loan cost also related to origination. The origination expense which company use to pay as brokerage that company use to amortize. Under IND-AS everything has to be amortized. - What is the attrition rate for the employee in the company ?

o 25 % at the absolute level , 15 % at the first supervisor level and low single digit in the senior management. - What would be difference in NPA between IND-GAP and IND-AS ?

o The two largest item on IND-AS is

Recognition of the Interest income on the NPA account which get added under the IND-AS but it is not added into the IND-GAP

NPA on the BTC issuance under securitization which is treated as off book under IND-GAP and treated as On-book under IND-AS - The run rate which company has guided is it the exit credit cost or the average credit cost ?

o It is average cost for the year. - Is there any cost to AUM target that company have in next 1-2 year ?

o This year company is aiming toward 15 % growth in the OPEX but 16-17 % growth in the AUM and that is where company will start getting operating leverage but that is work in progress. So over next year as company get better productivity in the AVF business on the topline and even in the mortgage where company have field team of around 600 people of which 350 people are in the sales function and out of those 350 people 200 has come on board from last 6 months . So there must be some optimum productivity. So all will do well and give operating leverage. It is all about building quality portfolio with productivity where company had talk about new origination from Dec-15 onwards which is 80 % of the total portfolio where servicing cost would be lower because that cost is substantially sitting in the stage-1 assets. So combination of all these factor resulting into operating leverage. - What will be the ROE , ROA target for next two-three year ?

o Company is targeting ROA of 1.8-2 which will convert ROE of 14.5 % for the current year. In next 3 quarter company will work to achieve 15 % ROE and once company achieve that than further guidance will be provided.

8 Likes

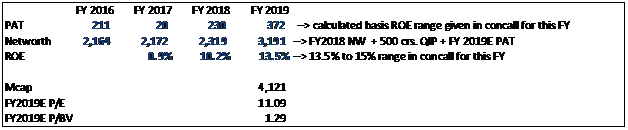

For 13.5% to 15% ROE range estimate for this FY, implied PAT is Rs. 372 crore!

Even if I take 12% ROE estimate, implied PAT is Rs. 330 crores!

In either case, earnings are expected to see at least 35-40% growth this FY.

2 Likes

Poor results and stock is down by about 50% in a matter of 4-5 weeks…With the positive numbers provided by management on Disbursement, I am not sure if the business is likely to perform better…Views would be appreciatedMAGMA_01082019125810_IntimationtoSEswrtInvestorPPT010819_142.pdf (1.9 MB)

Is the earnings call transcript available anywhere?

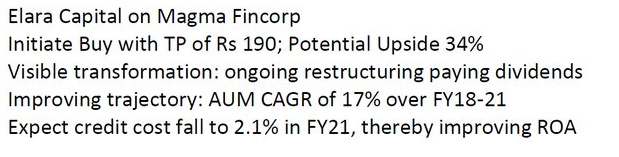

Magma fincorp

Key takeaways

Growth and outlook

While the overall economic environment remains subdued, the company is

confident of closing the year with AUM levels similar to FY19. This growth will be

led by focused products (affordable housing, SME, used assets).

Within used assets, used cars have higher share and portfolio is behaving well.

In order to support growth, the company aims to increase distribution network.

Q4FY20 disbursements are expected to be more than INR20bn.

Housing finance

It continues to remain a strong business with growth, asset quality and

profitability being intact. Focus is on affordable housing with an aim to be a top-5

player.

With disbursements of ~INR1.5bn per month, it is targeting AUM of INR15bn in

FY20 and ~INR20bn by FY21.

With 25-30% growth and presence in 10 states, the focus will be to achieve scale

and may consider an IPO in two-three years.

Liquidity/borrowings/margin:

Liquidity situation has been easing and has a robust pipeline of funding sanctions

and undrawn credit lines (six-seven new banks added recently).

Cost of borrowing is expected to decline starting Q1FY21 (9.2-9.5% now due to risk

premia). For FY21, the costs are expected to be lower by 30-50bps.

Asset quality:

Asset quality is expected to improve in Q4FY20 as collections have been good in

Jan 2020 (100% after a long time).

The pain in CV segment is significant given the stretched cash flows of borrowers,

which is preventing the roll back from stage 3 to stage 1/2.

Credit costs have peaked out overall and claw back of NPA is expected.

2 Likes

The only consolation in this counter is the sound management. Business is expected to revive after 2-3 quarters

I had looked at Magma two years ago. Price has crashed form 52wh of 67 to 17 today. Can any existing investor please outline the kind of impact this Corona situation may have on different parts of Magma’s business?

Today Manish Jaiswal clarified on et now that the collections began to pick up in March but this lockdown is a serious situation. The real impact will be seen in the second week when funds with businesses start drying up and depending on how well banks support.

Only after a couple of weeks will better info be available on the impact.

I received interest on magma ncd today(on time)

1 Like

The sun has finally risen here after a long dark night,much needed huge equity infusion(Rs 3456 Crores) coming in to the company, by Rising Sun Holdings, a company from the Poonawalla group(Serum Institute of India).

1 Like

Magma Fincorp’s (MFL) ownership and management has undergone a change after the Poonawalla group bought a 60% stake in the company. It is now a subsidiary of Rising Sun Holdings Pvt Ltd (owned and controlled by Mr Adar Poonawalla), subsequent to raising of equity funds of Rs 3,456cr on 06 May 2021. Since then, it has realigned strategy to exit stressed businesses like used CV/CE and tractor loans and is entering product lines like professional loans, consumer durable loans, home loans, and medical equipment loans, all of which are high growth products.

Post the capital infusion, MFL has one of the strongest balance sheets (CAR of 69.8%) in the industry, but the worst leverage at 1.3x. It has ample room to grow its AUMs without diluting further equity. The management intends to grow AUMs 3x by FY25, mainly driven by reduction in cost of funds and expansion of product offerings and customer base. Also, the company aims to control net NPAs below 1% level.

MFL has also infused Rs 500cr in its subsidiary Magma Housing Finance (post infusion, net worth is Rs 1,000cr; Tier 1 capital ~53%), which has grown its AUM at 17% CAGR over FY18-FY21 with its share in consolidated AUMs increasing from 18% in FY19 to 31% in FY21. With a strong group backing it and a cleaner balance sheet, the company’s credit rating would improve and cost of funds would moderate, going forward, which would drive profitability and return ratios.

The credit loss buffer built by the company and cumulative provision of Rs 1,192cr should be adequate to counter any COVID-related impact on profitability in the future. Rationalisation of its existing network of 297 branches and expansion to new locations should improve branch-level profitability. Also, greater reliance on electronic modes of collection and lending could bring down costs and enhance distribution capabilities for the revised product suite.

1 Like

news share :

2 Likes