Poona Dal and Oil Industries Ltd. is an India-based company. The Company is engaged in the oil and food grains industry. The Company operates in two divisions: oil division and agro division. Oil division includes oil, by products and others. Agro division includes pulses, processed pulses, processed pulses flour and others. The Company had a licensed and installed capacity of 135,000 metric tons of Refinery, 90,000 metric tons of solvent, 30,000 metric tons of vanaspati and 45,625 metric tons of pulses.

SEGMENT

The operations of the Company falls into two segments viz. oil division & agro division. The oil division consists of extraction & refinery process & the agro division consists of manufacturing of dal & processing of flour.

PRODUCTS

The group is selling all its products under its own brand name viz HIRA, TIGER, SURAJ & MOTI. The brand name is very popular in the state of Maharashtra and other neighboring states. The group is enjoying excellent relations and is commanding a prestigious reputation with the banks with whom the group companies are banking. The group is also enjoying excellent reputation in the market of Maharashtra and neighboring states.

LOCATION OF PLANTS AND ITS MANUFACTURING CAPACITY

The factories of the Company are located at E 2, Kurkumbh MIDC, Kurkumbh, Tal. Daund, Dist. Pune - 413801

With the state of art refinery having capacity of 300 MT per day and with efforts of sound technical staff Employees and Workers who are able to create their own brand image of products in the market vis.

• HIRA Refined Sunflower SOYA OIL

• TIGER and SURAJ in Refined Soyabean OIL

• MOTI in RBD Palm OIL

• 111 super Palm Oil and,These products are mainly available in two main segments one Bulk Pack having pack size of 15kg, 15ltr in Tins and Jars

• Consumer Packs available in 500 ml Poly pack, 500 ml Bottle 1000 ml Poly pack and Bottles and 5 litres jar and in this segment our products are distributed through strong network of distributors in a state of Maharashtra and Neighboring state

• TIGER is our most popular and trusted brand in soyabean oil in various pack sizes 1 ltr and 500 ml poly pack and jar 2 ltr jars

• RBD palm Oil Is available in Brand name MOTI available 1,15 kg and 15 ltr

• 111- is a super refined palm oil which is specially manufactured in our refinery in short span of time it has gained brand image because of it quality this is sold in loose form along with refined soyabean oil in tankers

• The products which are well reputed in the market for their consistent good quality and competitive pricing. The brand name enjoys a premium in the markets and well known among the masses.

CONSUMPTION AND IMPORT STATS of EDIBLE OIL

Between 2008/09 to 2015/16 the domestic production decreased by 8% whereas consumption increased by 48% and to cater that import increase by 78%. So the domestic edible oil producer are in sweet spot with the rising effort from the govt in the food processing and agro sector. It has been estimated that a mere 4% increase in the per capita consumption adds around 0.8 million tonnes of demand each year.

FINANCIAL

A Debt Free Company with 35 Cr Market Cap having 70 Cr Cash in account is a big plus in this sector where lot of other it’s peers are struggling with high debt. ROE and ROCE stands at 31% and 46% respectively . Receivable days at 14-15 at average is very good with Free Cash Flow stand at 52 Cr. Although high Working Capital Cycle (27-30 days) is a cause of concern for this industry but from the industry segment perspective it is very normal with Inventory Turn Over days at 10.

RISK

- For the oil year 2017-18, there is scarcity in sowing and crop damage due to flooding has increased in the major growing regions. These factors have contributed towards a reduction in Soybean crop size. As compared to the last year, when the Soyabean oil output was 12 million tonnes, this year it is forecast at below 9 million tonnes. So we can see input cost will be on the higher side which will impact the margin. Also any unfavourable weather condition will impact this industry adversely.

- If the Govt will raise the MSP then it will be a cause of concern which is very much on the card.

- With the raising input cost and due to heavy domestic consumption it will be tough for the Govt to impose a high import duty on edible oil hence no protection can be given to the domestic industry. Although in the last quarter the Center has hiked the import duty on imported oil to protect the farmer so if this will be the trend then we can expect some good future for this segment.

- Another concern is the management push/aggression behind the growth of this company. Since I found no major capex done after FY15 hence it will be hard to determine their growth strategy behind the business. Pradip Poonamchand Parakh the MD of the company not much is known apart from is very conservative attitude towards the business. [Urging any senior VP member to shed some light on this ]

- Also the Promoter Group is into Real Estate business [Pdbm-poona Developers Private Limited] which is a diversified one and can be most closely compared with it’s peer like BCL. So not very sure about their intention .

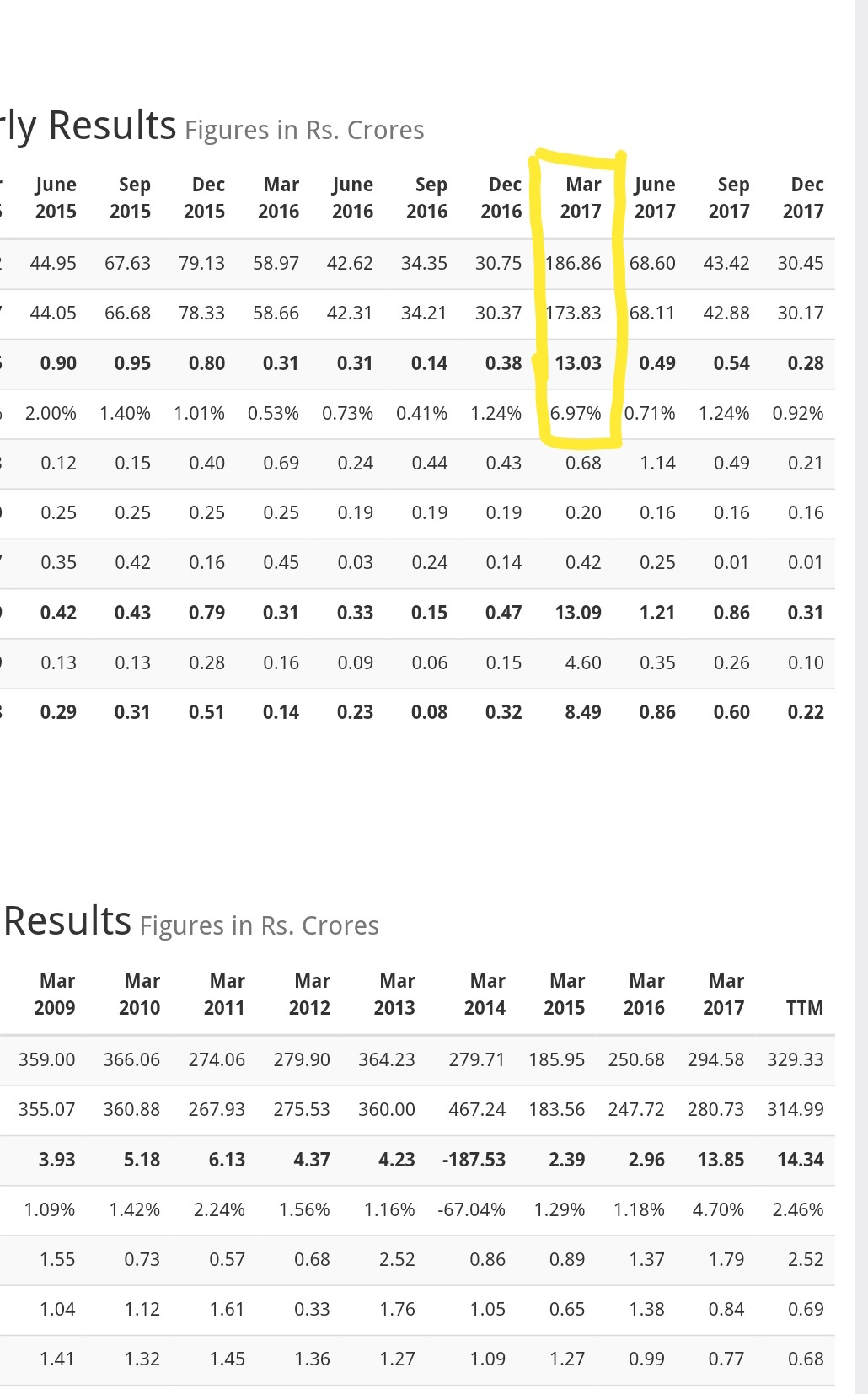

Attaching the Financial ration analysis data sheet[source screener data.]Poona Dal & Oil.xlsx (131.9 KB)

[Discloser :- Invested with a tracking position so views might be biased.]