Very Possible … but how come the sales got increased then ? If it will be a top line growth how come the funds get siphoned off ?

One thing that bothers me much is the surprisingly low remuneration of the managing director. He was paid 50000 rupees per month. It’s baffling that the top officer of the company is willing to work for this low a wage. Also, they had appointed a student of CA Final as an independent director. I wonder what the cause of this action was. I’m certain there must be other people better suited for the directorship. Could it be a quid pro quo? When remuneration isn’t consistent with industry averages, it’s likely that there are other ways in which the management is enriching themselves.

I may be totally wrong but these factors don’t give me comfort.

Hi Shreys,

- Low remuneration I don’t think is a issue rather it’s a good sign for the company and share holder since Promoter is not taking the maximum portion of revenue that come out of the company.

- About the 2nd point of the appointment of the CA final year student as an independent director I am not very aware of . Can you please share some more information in this ?

Until and unless the cash of 70cr(if its real) has a proper use/distribution the market wont be valuing the company , thats what I feel.

has a proper use/distribution the market wont be valuing the company , thats what I feel.

Thanks Shreys,

For pointing out this. I have somehow overlooked this fact. I will dig into this and will try to find what is the actual objective behind this decision.

@KC1986

I’m happy to help. Would request you to share your findings with us. It really helps.

Yes this is a definite concern. The nature of cash equivalent is also a question.

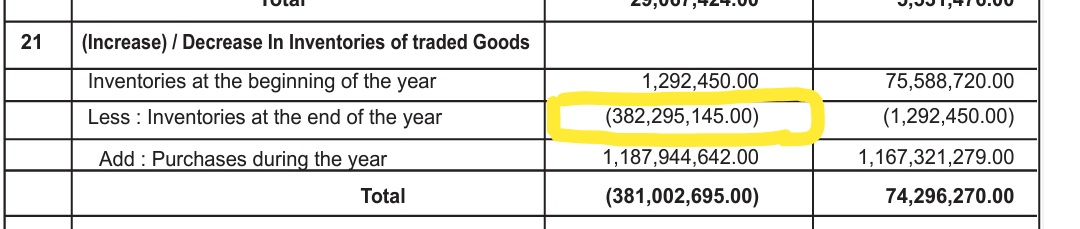

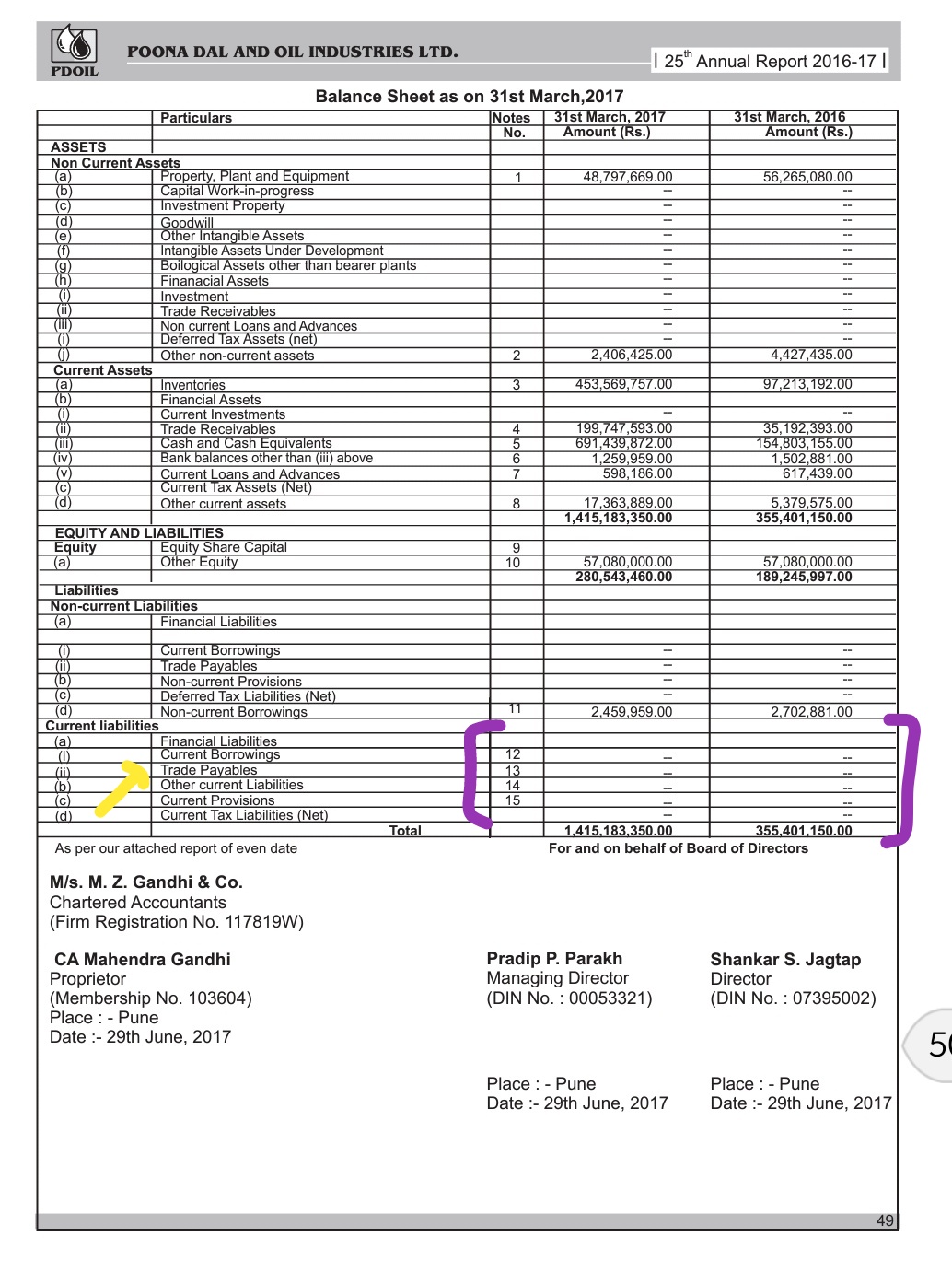

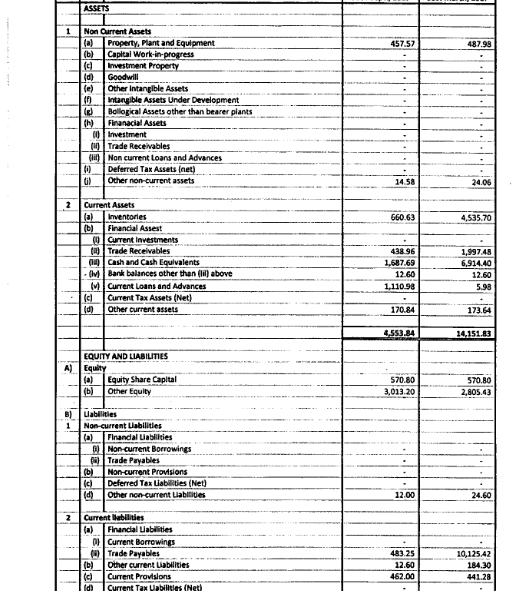

From 2017 Annual report - Only 3 heads have changed drastically in BS - 1. receivables have gone up significantly, 2. Inventory has gone up significantly, 3. Cash has gone up significantly.

If one notices the operating cash flows, it is up significantly due to lower working capital.

If one sees the energy consumption expenses, the numbers have reduced, which means there is no “extra” production. Numbers suggests there has been much more trading activity rather than processing. (i am not following this company so am not sure how this functions).

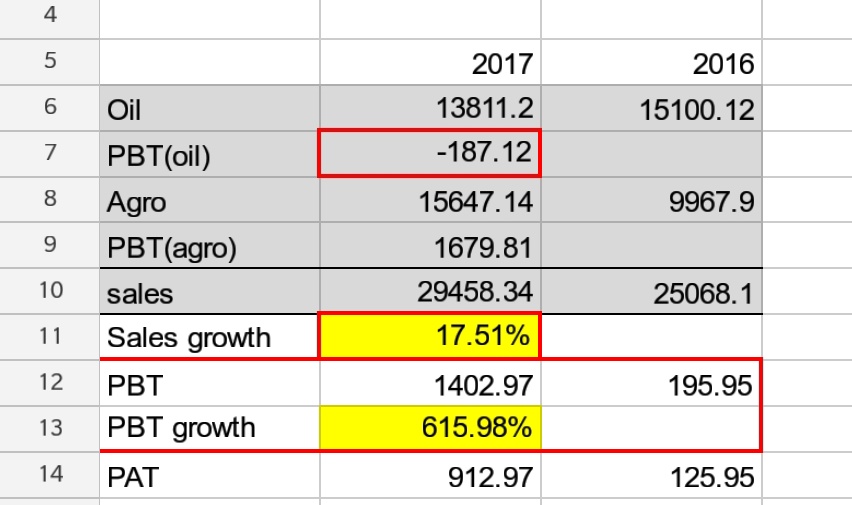

Annual report doesn’t have any mention of any special case (special order or something) as to why profitability and cash flows have suddenly improved. They just mention a few lines on the two verticals - The year under review witnessed a growth in the Indian economy which had positive impact on agro industries. Company has achieved commendable Growth in Sales for the year under review and increased overall profits for the Company.

On one hand they say -

On the other hand, they say -

Disclaimer: Neither invested nor interested.

3 Likes

Thanks @Mridul ,

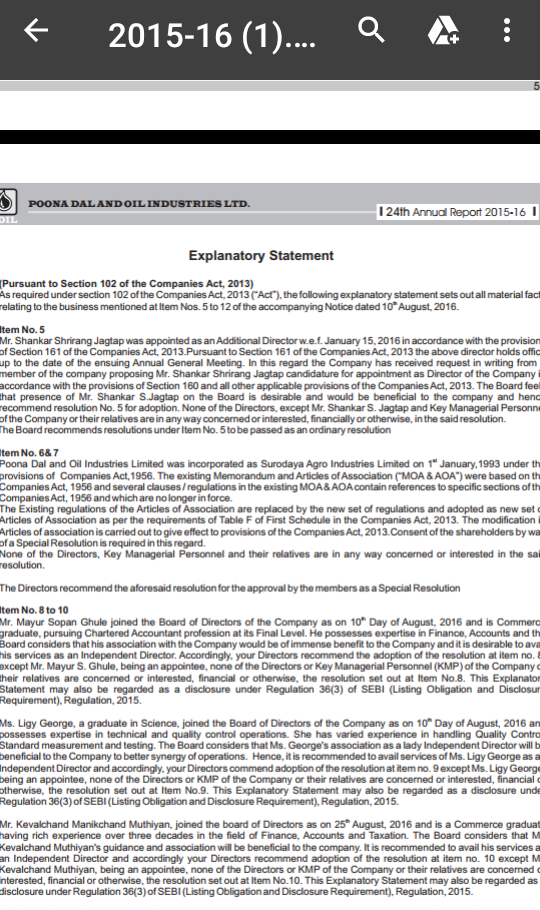

The explanation is really nice. About the business operation the Company mentioned that “The oil division consists of extraction & refinery process & the agro division consists of manufacturing of dal & processing of flour.” So they haven’t mentioned any trading activity rather they have stressed upon “state of art refinery having capacity of 300 MT per day” and “The group is selling all its products under its own brand name viz HIRA, TIGER, SURAJ & MOTI”. So I am not sure how the trading activity they will apply since they are selling own branded product but considering the number you given from AR as a reason for exponential sales growth a trading activity can not be ruled out rather only solidify the case. So we might need more information at ground level from Pune nearby location [requesting to all the VP members if anyone stays at the nearby location of the company {E 2, Kurkumbh MIDC, Kurkumbh, Tal. Daund, Dist. Pune - 413801}]

1)Yes!!when we see yearly sales growth it’s normal…but profit growth isn’t normal.Profit has spiked much.And,it seems to be due to Increased inventory of traded goods which suggest that company has purchased and retained lot of traded goods.This may be interpreted as either decrease in orders/demands of products or company is optimistic about utilisation of all it’s inventory ahead.

2)To support decrease in demands of products,company’s energy consumption can be logged in I guess.Although increase in rate/unit of electricity there is decrease in its use from previous year.(n.b-however,this can’t be sure sign)

3)Oil part of company is in loss.It has reduced sales from previous year as well as expenses for operations of oil is more that it’s revenue.

4) Although company has Good bank balance,no debt,good asset at present;to maintain this goodness it needs to strengthen its demand-supply.It seems like well designed beautiful car with damaged engine.

(N.b-Just my views.Suggestions are welcomed)

1 Like

Thanks @jvpatel87

For the explanation . So let me categorize the concern at a high level.

- Exceptional Sales in One Quarter mainly due to trading activity and how much sustainable is it?

– How this sales growth will span out we have to look for next 2 quarter to understand the strategy behind the company. - Since Oil division is loss making one hence there are concern about the demand of this product ?

– Well this has been a story for domestic oil producer last year unless they have a strong brand or distribution network. And perhaps that is why most of them have more focused into other agro division as well and PD Oil is no difference than this. - Agro division has seen a spike in growth and what will be the future of it?

– Consumer staples demand in a country like india is always sustainable . - Strengthening it’s demand-supply dynamics and how this can be achieved ?

– This is a definite concern for all of us and I am trying to a lot of scuttlebutt from few of my friends in Pune region to get know the details of this. since no information is available in public.Will update them once I have any information about it.

At this level I feel this company is a safe bet since it is available at a throwaway valuation, debt free and high cash with a lot of inventory. Although we have to be rest assured about the concerns raised in this thread itself and have to has a good watch at the coming quarter and any strategic decision they take.

[N.B. :- I am holding a tracking position in this company and will wait for any further investment till I get any better information about the points raised ]

1 Like

I think this company is not good for long run.Oil division is in loss since many years.Management doesn’t look much active.AR doesn’t have much informations .They are much of copy-paste.No any expansion and future plans ever seen in there any old ARs too.

Well @jvpatel87,

If you notice the last two quarter result. Their Oil division is making profit. Sales ware down driven by lower revenue from Agro segment. The stock in trade purchase is also very low compare to cost of material consumed. Also the in the last nine month both the segment is making profit.

Hi @jvpatel87,

Thanks for your observation. But the document you are referring is the AR I guess. Sometimes I have found many AR used missed out details items rather it just mentioned the Notes section to refer for details. In this case it has also been the same. Also if you go by the total sum liability it is getting exactly matched so I found no issue.

Better you refer to the FY17 result declare on BSE for the numbers.

Did you get any response to mails you sent to company?

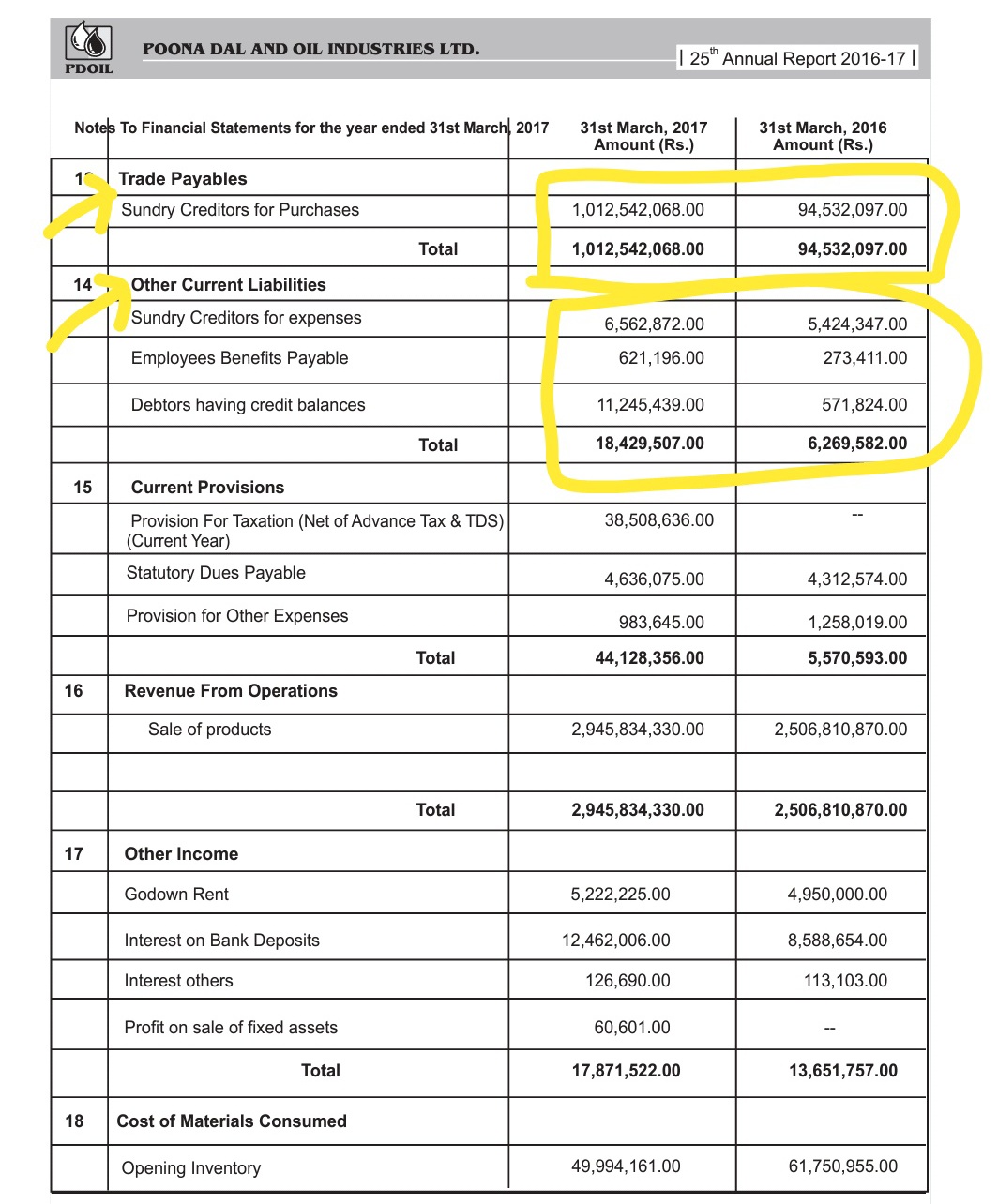

Even trade payables are so huge as compared to trade receivables…

(Disclaimer-have sold all of it today)

The Reply was not very concrete . And as you have rightly pointed out trade parables is really huge as compared to trade receivables but this in-turn also prove the credit quality of the company since they are purchasing on credit and selling on cash.

1 Like

Not sure if you have checked September quarter filing. Company does not have 70crs cash. This was the money given as advance for the orders. Money has been used to payoff the trade creditors and cash position as on Sep stands at 16crs.

Discl: Not invested. not tracking

Yeah I can see that. It will be much clear when FY18-19 report will come out.