What is total acquisition cost is it 10+8= 18 crs??

For the last two or three weeks many employees and especially Shyam lal Bajaj (Director) selling there shares… Also two of the promoter director transferring there shares to a few trust…can anyone give a approximate idea what’s going on in this regard

1 Like

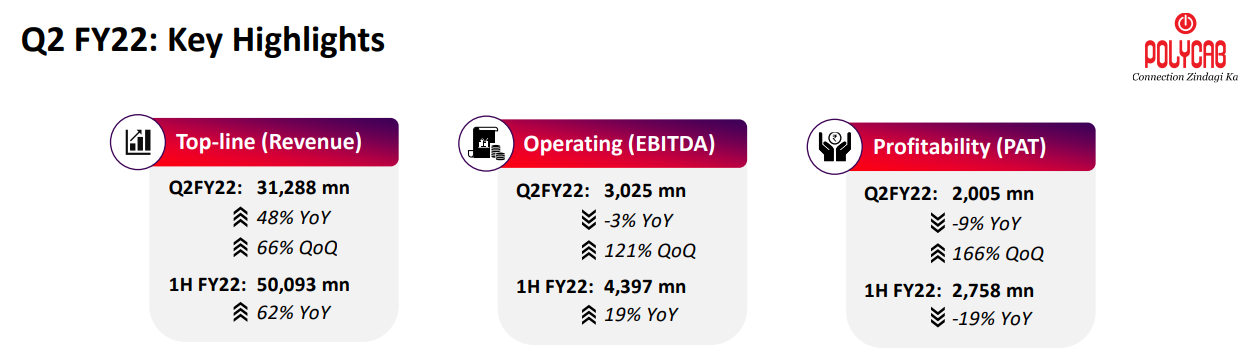

From 2014 to 2021 - 7 years - Polycab’s

Revenue growth - 3986 to 8927 (12 % Cagr)

Operating Profit - 299 to 1167 (21.5 % Cagr)

Net profit - 89 to 882 - 10X (38.5 % Cagr)

Other income - 8 to 138 - 17X (50 % Cagr)

Income Smoothing ? Or something Completely different?

a 15% compounder is the story we can see for at least few years

No it is likely going to be more than that solely because FMEG is growing at 40% and wires and cable is not stagnant.

For FMEG it is mostly about brand building. Right now they are only focusing on topline growth without compromising quality with wires and cable backing any capital requirement. At one point in time they will be able to raise the price and increase the margin which would meaningfully increase the bottomline.

This is how i can explain the jump in Polycabs P/E.

Disc: invested.

3 Likes

Has the company disclosed any information related to their revenue breakdown in wrt tier1/2 cities in any of the presentations or concalls?

Is there any information about this available in any public domain for all the FMEG players?

expecting pressure on Margin because of inflation.

2 Likes

YOY If there is no increase in market share, I think the extra cash burnt for increasing revenue is a waste as there is no increase in profits!

Too much competition?

1 Like

they aren’t looking at qoq but 3-5yr play for the overall business, esp. FMEG… they need to maintain certain top of mind recall so reasonable investment in a&p is justified in my view… as asian paints management said you can’t switch off and on a&p budget… but need consistency…

Discl: invested…

3 Likes

Further company has been making strategic bets (eg. silvan acquisition) + induction of Mr. Sharma, new Deputy M&D, is aligned with their Project Leap…

5 Likes

Polycab announces 100% sale of Ryker (Copper RM unit). In many of the previous concalls, management asserted how important Ryker was to the company as it gave it better quality and timely supply of RM. Infact, they called it a major advantage over their peers.

Puzzled by company’s decision to fully divest.

5 Likes

Multi year tolling arrangement to protect Polycab’s supply chain dynamics - Don’t think this would have been an easy decision to take. We would know the extent once the specifics of the formula are made known.

And that too, when copper and value addition to it is going through the roof in pricing and China hoarding it all. Having backward integration to a key ingredient to your wires, why sell it?

1 Like

Its a low ROCE business and operating at sub par utilization. Wire rod making is not their core competency and such a business would be better off with a company like hindalco.

5 Likes

You can’t say this as backward integration. Any copper price fluctuations still has same impact with or without Ryker. If it’s not giving good yield for business, it’s better to sell it off.

We can take some positive here, even though they were hoping high on Ryker business, the moment they feel it’s not working, they sold the business rather than keeping it under them and pumping money

Disc: Invested

3 Likes

Seems like a good move… Outsource non-core competency and secure long-term arrangement… it will be margin and roce accretive also as Ryker is commodity play…

2 Likes

When Ryker JV was announced and also when they acquired 100% stake, the Management was very confident and talked about the backward integration and how this would bring a difference in their products.

Selling it that too around within a year of acquisition definitely doesn’t increase my confidence in the management.

disc: invested, considering reducing the bet size.

3 Likes

After selling Ryker, now Polycab incorporated the new Subsidiary called "Steel Matrix Private Limited (‘SMPL’) "

Industry : Manufacturing of Steel drums and bobbins for cables and wires

Authorised capital: Rs.1.00 crore

Size / Turnover: N.A

Objective : To secure dependable supply of quality packing materials, improving control over the supply chain and increase the overall operating efficiencies. SMPL will also help to strengthen the backward integration of the Company’s manufacturing process.

% of shareholding : 75%

4 Likes

Disc: invested

5 Likes