The reason for involvement of family member in the company is due to the over age of the promoters at board member. All for promoter brothers (ITJ, ATJ, RTJ and GTJ) are 65+ year age and they need strong succession plan for the future of the company.

The respective sons (Kunal, Bharat and Nikhil) of the three promoters are working in the company, and they not included as part of the Board and the remuneration given to them is reasonable. Given the family oriented business it is good that 3rd generation are introduced for their grooming. I think this is not an issue.

For the EPC business the mgmt clearly indicated that they dont want the EPC business to more than 5-7%. Please note that in the Cable EPC business the supply portion use to be 80-90% and balance 10-20% is erection and commissioning. So later the receivable should come down.

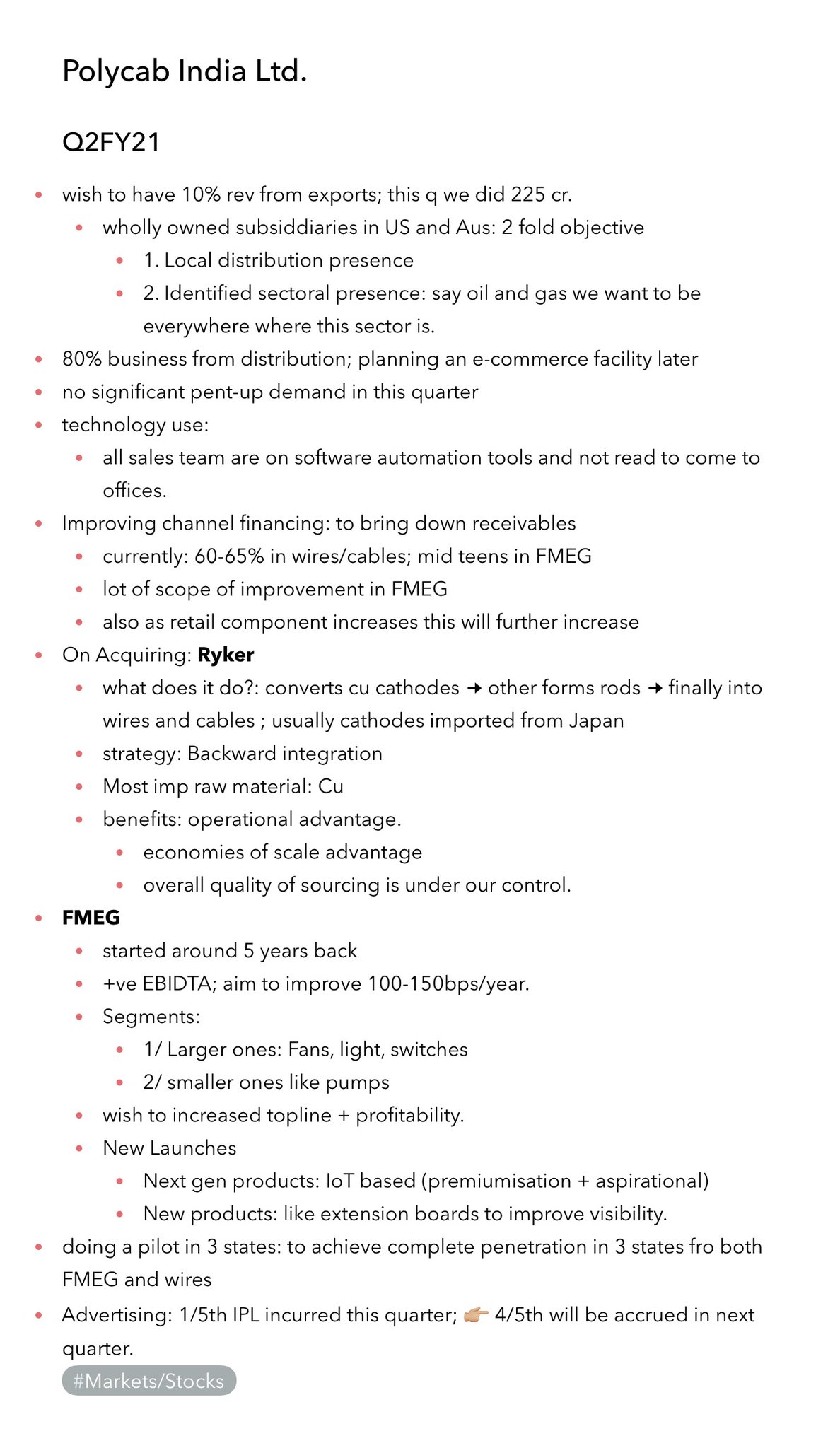

below is my first glance on the Q3 , yet go through concall transcripts …

Wires and Cables business posted 6% YoY growth –

But I feel the raise is more likely due to Raw material cost pass – Volume would not have grown

FMEG – 41% YoY – good growth

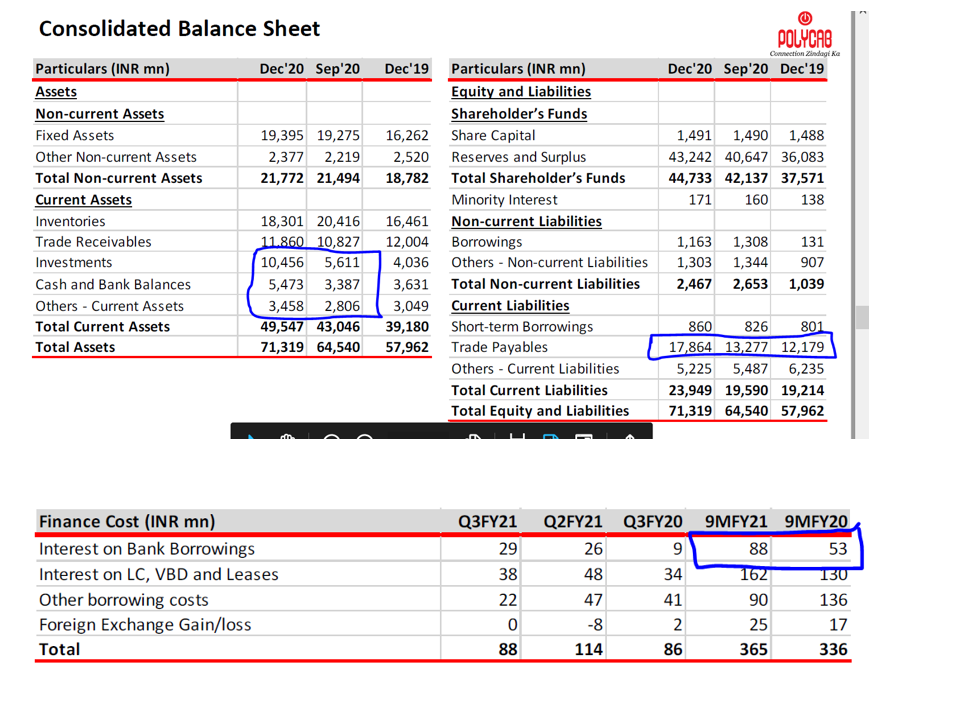

Cash increased , but good amount of that is due Trade acceptances

not sure why the company is paying for trade acceptances when the have cash on hand …

due to above action company would have payed 20-30 cr additionally for interest on bank Borrowing

Kindly listen from 19:50 onwards to understand trade acceptances part.

Overall decent management commentary.

There is a lot of scope of improvement in the numbers with improved working capital and increased channel financing and management seems well aware and is working on it.

Online presence, new ventures and new geographies needs to be tracked further and finally the growth in Wires/Cables needs to be monitored as well.

There trade acceptances are kind of debt. The company does pay an interest on these trade acceptances. Its only because of certain RBI guidelines it is treated as trade payables. Actually they are not trade payables but are debt.

One of the best core stocks that I own, this company has a tremendous growth opportunity and I love how the management has grown the FMEG business while also reducing the debt on its books. Their foray into passive networking solutions is also positive and i like how the management if expanding into related businesses and executing them with great efficiencies.

Polycab came out with good Q4 results:

Revenue increased by 43% to 3037cr in Q4 ( flat for Fy21)

EBITDA up 43% to 422 Cr and PAT increased by 32% YOY.

EBITDA margins at 13.9% for the quarter and 13.1% for FY.

Exports revenue in Q4 at 1.3bn(4.5% of sales) FMEG business growth at 89% yoy in Q4 and EBIT margins increased to 7%.

(overall good results even after considering the low base of Q4FY20 due to lockdown and recent surge in copper price)

YoY growths should be read taking into account that most of the march’20 was impacted by total lockdown.

What are the company’s expansion plans given the excess cash it has?

I will look into what the current capacity utilization is over this weekend.

Surge in the Copper Price would amplify the growth because Polycab usually pass on the increase in raw material cost to customer which increases the revenue.

better parameter to check in this industry is volumes…

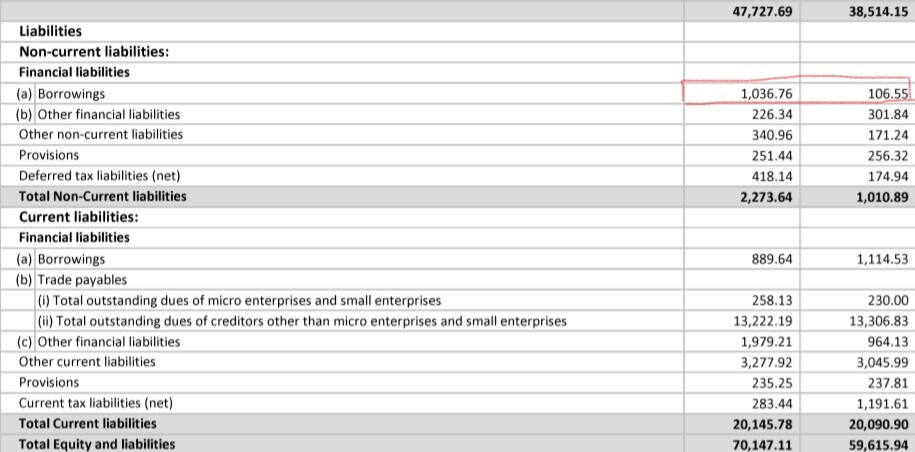

Thanks!! I was thinking about why have borrowings(sum of short-term and long-term) increased, while they have made net repayment of around 100 cr. However, then I realized that there was around 250 cr of debt of Ryker which got consolidated after making it their wholly-owned subsidiary.

Polycab Ltd, conducted their conference call on 7th June 2021.

" Target to attain more then Rs 200 Bn sales by Fy2026 "

Here are the key takeaways-

Company has generated positive growth this period as well.

They now command about 20-22% share of organized wires and cables market of India.

There is a strong momentum around housing wires.

They still have strong B2B scale-up.

With upcoming position in B2C strong business is expected.

Company has increased its focus to leveraging digital to transform business model.

Distribution levels and retail has reached a good scale to 17% and 32%.

New concept are been planned and worked upon.

Employees are been provided all types of knowledge and professional support to grow and help business attain it’s multi year transformation.

They will keep adding value for business growth.

Companies wire and cables business delivered a strong growth on qoq scale due to healthy pickup of infra and other industrial project’s.

International business was hit hard but has shown decent sign of recovery.

Under FMCG, There was a huge jump in the revenue and EBIT margins on both yoy and QoQ scale.

This was due to healthy customer demand, distribution and strong execution.

In it, light growth segment got almost doubled. Their Switches and Switchgears grew by almost 2.5x.

There is further improvement in the product mix and other initiatives are been taken by them to be more profitable.

Other segment product, like EPC business were hit very hard by covid and had delivered poor yearly performance.

But There is a strong receive on QOQ basis.

Copper backward integration has helped Company to maintain their margins.

Company do its best in terms of change in prices to avoid any reduction in our margin levels.

This Strong opportunity came from private sector.

Financials and Investments

On Yearly scale, PAT levels have seen a huge jump of about 16%.

Revenue and EBITDA grew by about 9% & 12% on QOQ basis. It was due to improving share in B2C business and availing leverage benefits along with cost savings.

Business didn’t grew much due to Covid-19 impact on yearly scale.

Companies expense on advertisement has reduced a lot compared to previous year and it has does impacted their sales.

Capex expenditure in Fy21 was around 700 cr and as looking recovery this will increase.

Currently Company has an increasing net working capital on yearly scale.

The Company has increased its dividend % this year.

And The management has seen shift in its members as well.

They are bullish on their cash conversion cycle and will take inorganic growth later.

They have a Capex plans of around 300 cr for new period. This will majorly go to FMCG and rest in cable and wires

Their cost optimization project udaan has done well as they have been able to save about 200 points in cost and expect further.

To attain their 200billion rs mark in next 5 years, Company has a broad picture but they don’t have specifics right now, but this information will definately come by next quarter.

(copied from @tycoonmindset05)

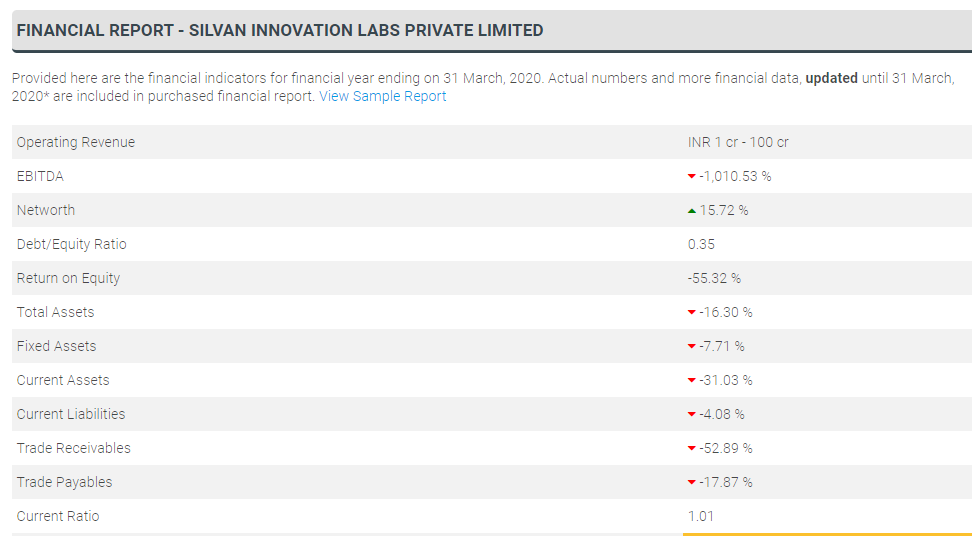

Polycab to acquire Silvan Innovation Labs Private Limited

Key points-

It was founded in 2008 by four electronics and embedded systems domain veterans possessing a cumulative experience of 120 years in reputed companies like Texas Instruments and Lucent Technologies. The company has 17 patents, including filed and provisional.

The cost of acquisition is around Rs102mn for shares and around Rs 80mn as additional funds infusion to discharge certain outstanding liabilities.

Revenue:

FY20: Rs 34.4 million

FY19: Rs 92.4 million

FY18: Rs 81.7 million

Has a sizeable order pipeline of over Rs 1bn however the pandemic has significantly constrained the business from achieving its true

potential.

Looks interesting and future focused acquisition for Polycab. Definitely its going to increase the exposure in nextgen FMEG products.

I don’t find any historical PNL related information of Silvan. If its cash burning, we need to watch that too. I just found the below information from internet,