My understanding of Free Cash Flows (FCF) is CFOA minus maintenance capex i.e. the capex required to maintain the current earnings and not the growth capex. FY19

CFOA is Rs. 107 cr. Total Capex is Rs. 77.99 cr in which the maintenance capex must be much less. So FCF positive in FY19. FY18

CFOA is Rs. 75 cr. Total Capex is Rs. 82 cr in which the maintenance capex must be much less. So in FY18 also the FCF is positive.

Request you to re-check the numbers/ratio you have mentioned. Debt Equity ratio is at a very comfortable level of 0.33 and not 2.11. Further, one needs to look at the reason for increase in debt levels. In case of Polymed the debt has been used for building capacity and we should appreciate the fact that Fixed assets have also doubled in these 5 years.

Polymed being a manufacturing company it is only logical that to increase sales it has to put in money in building up capacities and capabilities. After all, there is a limit to asset turns and it is unreasonable to expect them to clock 5-6-7 times asset turns. We need to keep in mind the industry and the business the company is involved in and then judge it on its performance based on those industry standards. For example, we can’t say HDFC has a Debt-equity of 7 and so it is bad, because that is how the banking industry works. Similarly, if in the healthcare/medical equipment business the asset turns are 2-2.5 then the company in order to grow will have to invest in Capex once it reaches that limit.

Therefore, it is important that as analysts/investor we look at various financial parameters in relative terms and not just get influenced by absolute numbers.

Finally as clarified by @harshitgoel Sir as well, Polymed has not diluted equity in past. The increase in equity share capital is on the back of bonus issue (no money comes in or goes out, its a mere book entry).

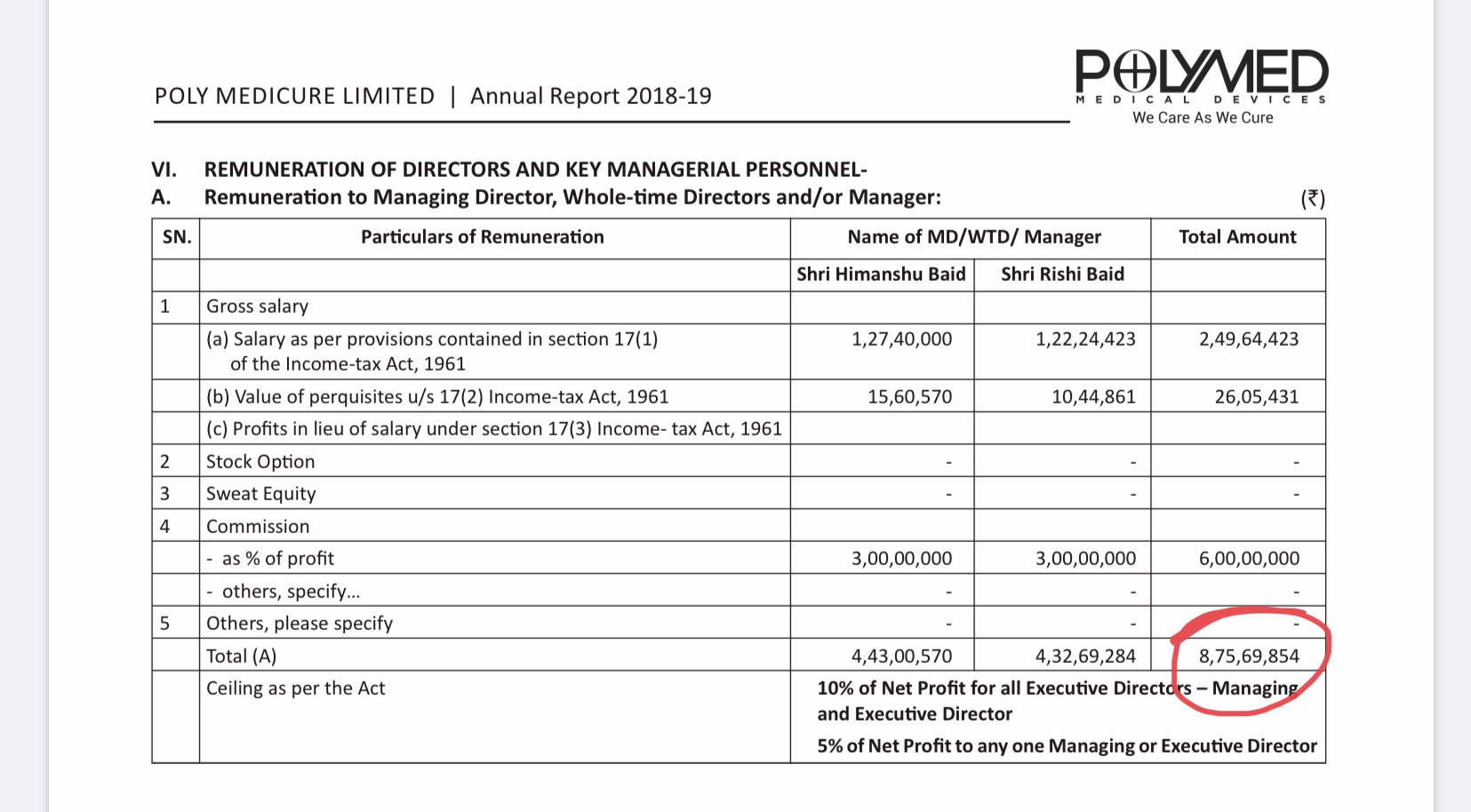

Poly Medicure AR 2019 notes

(Excluded points already covered by @harshitgoel in earlier post)

Strengthened Vascular Access & Infusion devices portfolio through SRL Italy acquisition and offering a complete range of Vascular Access Devices in Oncology space (cancer care treatment)

More focus on Clinical Trainings to enhance POLYMED’s brand recognition in the Healthcare industry

Expanding product basket in all business verticals and making new investments for increasing capacity for domestic as well export business and developing new products

Invested in automating the manufacturing processes and production lines to the core by deploying artificial intelligence and robotics

India: 25 super distributors, 10+ authorised agents, 1300+ dealers and 250+ persons in Sales, Marketing and Product Management

Exports: Have Dedicated Sales Network and Tie-up with 200+ key distributors in 105+ countries

Key RM: plastic granules, PVC sheets, boxes, medical paper and film

In case of the drastic price rise of RM during the year, the Company makes appropriate changes in the prices of Finished Products after due discussions with the customers. The prices of Finished Goods are generally reviewed every year and appropriate changes in prices are made to offset the increase in cost

How has the industry reacted to the government move?

The industry has so far reacted positively, though doubts remain about the ability of the Central Drugs and Standards Control Organisation (CDSCO) to effectively regulate both drugs and medical devices.

Himanshu Baid, Chairman, CII Medical Technology Division and Managing Director, Polymedicure, said, “CII Medical Technology Division welcomes this move, as this will ensure that all medical devices available will be safe and effective. The temporary registration application for devices that are currently unregulated will require basic administrative documents and basic product information. The registration process carries no government processing fees and does not expire till the manufacturer/importer obtain the import/manufacturing licence within a period of 36 and 42 months for class A, B and C, D devices respectively, the temporary registration may be cancelled or suspended by the CDSCO for product safety concerns, or when superseded by an Import/ Manufacturing License. Once registered the local registration holder will be required to notify the CDSCO and Materiovigilance Programme of India (MvPi) of Serious Adverse Events (SEA) occurring in India.”

“The small to medium players will get impacted due to coronavirus as they are dependent on China for raw materials, components and packaging materials. Most companies have one-two months of stock. We may see some disruption in the coming weeks. Already domestic raw material suppliers have started increasing prices,” said Himanshu Baid, MD of Poly Medicure. The company is engaged in IV catheters, blood bags and dialyzers. Baid added the company is not impacted as it has minimal imports from China.

I dont see a plant closure notice for Covid-19 in the exchange dispatches. Are the plants still functioning? Do they perhaps have exemption like Pharma?

I think the plant is operational. I came to know thru the Twitter where Himanshu baid is discussing with Dr trehan on health along with the polymed team. He was sitting in the plant itself. Pls see the attached video