Any news here Stock up 15% with very high volumes…

4 Likes

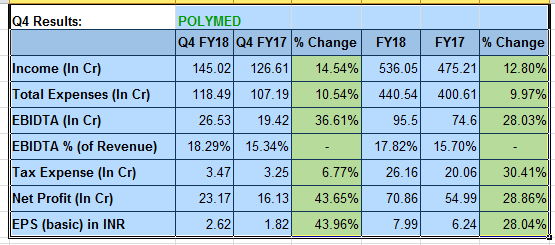

4Q was particularly strong 18%% sales growth, higher margins and 42% PAT growth. FY18 EPS at Rs8. Stock at trailing 32x P/E

Disclosure: Invested

In India, we have Romsons and Medikit as other dominant players in medical disposables industry. How can we get the revenue and profitability metrices for these two players? Any other serious competitors?

I was researching this company and asked my father about this. My father is in pharma business. He told me that in Kapurthala and Jalandhar side, Romsons is the market leader and he hadn’t heard much about Poly Medicure. As per him, market is growing at a good pace of 15-20% every year.

2 Likes

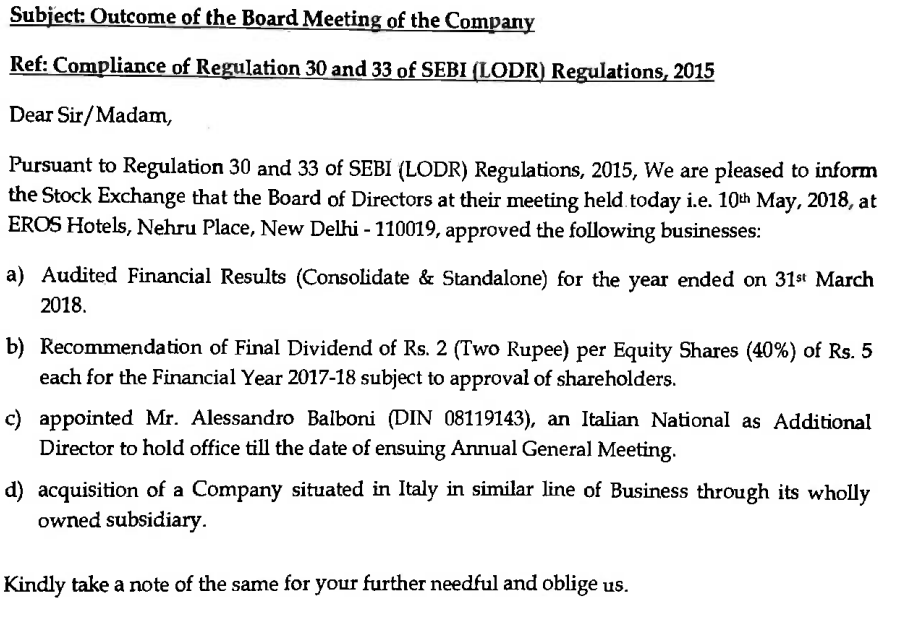

Probably this is the reason Stock reacted so much today…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/f3e07028-0cea-4da5-ba0a-ea2b826a255b.pdf

1 Like

Romsons or Hindustan medical device product quality is sub standard but polymed product are of superior quality like BD (world top brand in medical disposable)

Just found the company and gone through all the discussions to understand the business !

Definitely , the business looks great with immense possibility and scope.

The numbers too are great and consistent margins are impressive !

Read the link about Vadra Deal (Old news which was discussed here) and the integrity of Management.

Some Points that i have observed and found out !

In AR 2015-16 , the highest shareholding excluding promoters entities was with Allgeny Finlese (14.01%) which it sold entirely to Ezekiel Global Solutions as per AR 2016-17. Both these firms have a common director (Mr. Anuradha Bafna) , though not much details about any links between Promoter Company and these two entities .

The other entity whose name arose in land dealing was Sanchiya Enterprise which holds 3.49% Stake in 2016 but no stakes in 2017 as it transferred entire stakes to SCG and Co. Ltd. Interestingly both the Companies , Sanchiya and SCG have again a common Director (Mr. Manju Lata). More importantly , the Promoter Entity “Jai Polypan” has the same Email address “bhandarinitin@hotmail” which is of Non Promoter Entity SCG.

Another 10% Non Promoter holding as per AR 2016 is with B.S Trade Pvt ltd which again sold almost entire Stakes to Zetta Matrix as per AR 2017, both having a Common Director Kulvansh Singh. Do Note , he is the same person who has signed deal of behalf of VCB Trading (which is a promoter group of Polymed). Another promoter of Zetta is Mr. Anuj Janardan who is also a director in Agrasen Service Pvt Ltd which again has similar id “bhandrinitin@hotmail” and similar Address “Bais Godam” which is of Promoter entity Jay Polypan. Tried searching for this person “Nitin” but unable to find any details yet.

Though it can not be said as a fraud or illegal but there is a possibility that these companies may get insider details of the results and business.

I am very new to investing and can be wrong in my interpretations ! Seniors member can guide much better about these transfer of shares and common Email and address thing.

@ayushmit @Donald

Regards

Bharat

6 Likes

Went to a blood donation camp organised here at IIM Lucknow. Ram Manohar Lohia hospital also uses Poly Medicare blood collection bag. I asked the people who were collecting blood that since when they are using it and they said from quite a while now.

Has anyone observed the use in other hospitals?

3 Likes

Interesting. It looks to me like these shareholders who are classified as ‘public’ are actually promoter entities. So the actual promoter share holding may be close to 50%

1 Like

This is a wonderfully curated thread. Some points from my end -

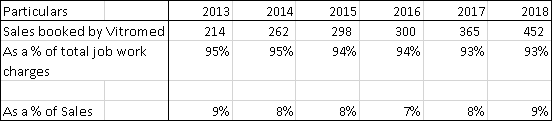

- Transactions with Vitromed

Vitromed is a partnership firm with all the Polymed promoters as partners. This firm is also in the business of making medical devices and is the contract manufacturer of polymed. Almost 55% of vitromed’s revenues come from polymed. These revenues flow as job work charges in polymed’s books and are as follows –

It could be a case of the value moving out of the company or it could not. However, the listed company has stable margins since last 10 years and the returns are above cost of capital. Company has earmarked 75 crores and 90 crores of job work for vitromed in 2019 and 2020.

What is quite surprising about vitromed is that non polymed revenues are all exports and are in the biotech segment. They are currently making losses in non polymed business since its newly started. This could as per me, be a red flag since a new venture was not started in the listed company (vitromed website also lists renal care and anaesthesia products that polymed would be starting now). Despite the losses, Vitromed’s RoCE is 15%, which indicates that poly med business is quite profitable for vitromed.

Also, as per the ICRA report of vitromed (attached) “The firm has stable working-capital intensity, primarily due to comfortable receivable terms with Polymed”

https://www.icra.in/Rationale/…/69239~Vitromed%20Healthcare-R-06042018.pdf

- Patent Victories

Their patent victories over B. Braun are possibly one of the strongest points with respect to their business. However, till now they have won in India and Germany and lost in Aus and Spain, and in even in India, they prevailed since there was a procedural error in B Braun (also some foul play, no doubt since the patent officer was suspended).

However, their India sales have been declining over last 2 years, reasons for which I could not locate. Based on the competitor’s list and the tender from AIIMS, Jodhpur, the industry is fairly consolidated with few players working with top institutions (since bulk of their India business is tender based). Also, in the blood bags segment, the largest player in Asia is an Indian MNC called Terumo Penpol. Surprisingly, all the companies manufacturing blood bags in India use licenced technology from NRDC – (https://www.nrdcindia.com/english/index.php/success-stories/78-disposable-blood-bag-system). So was wondering how strong their IP is in their IV business.

So although the overall financials of the company are very good, their newer forays would (which would bring the incremental revenue) would be difficult to figure out.

7 Likes

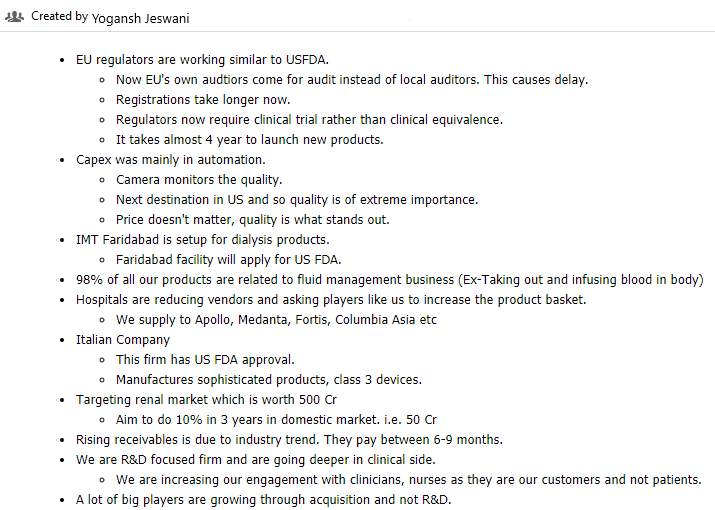

Hi All,

Sharing my notes from AGM 2018.

Regards,

Yogansh Jeswani

Disclosure: Tracking

Please Note: These are my personal running notes of the AGM and can possibly have error in listening, writing or interpreting while preparing these, please do your own due-diligence.

18 Likes

Few points based on scuttlebutt with regional manager of company(there may be few mistakes while noting down point):

Polymed is 3rd largest manufacturer of medical devices in India/?world.

We are exporting to 105 countries having offices at Germany,Egypt and China.

Agents are appointed at other countries who sell and manage our products. We get better margins/payment terms with exports.

Plants are European Union approved.?one US FDA approved plant.

Innovations driven company. Introducing many new products. IV cannula with safety features to prevent needle stick injuries, iv set with photosensitive protectors.

Launching 40 new products soon.

We are selling directly to most of corporate hospitals like Narayana,Apollo,Columbia Asia,HCG…etc. some business with ESI / govt hospitals is through govt tenders.

Continuous training for staff/doctors about our products.

Many hospitals once they use our products are asking again us to supply.

Dialysis products launched 6 months back. Our dialyser cost less than 50% of existing player products, still our margins will be around 40%. Dialysis machines are from Fresenius company due to which we are facing bit reluctance from Fresenius people to use our products.

Poly med has all catheters/ cannula required for dialysis.

Central catheters:Poly med catheters better than B Braun.Guidewire is most important in catheters which is manufactured by single player throughout world. Even B Braun imports guidewire from same player.

Selling 5000 incentive spirometer/ month but our market share is less.

Vacuum suction/ drains we have products. These are dominated by Romovac/Ramson from many years. We are trying get market share.

Super distributors: have fixed margins of 4 to 5%. They will pay advance money irrespective of stock level with them.

Distributors: will get supply from super distributors and their margins vary.

Promoters have started focusing on domestic market now. Our customers in other countries are asking us why we are not selling much in India. Management has increased domestic sales manager strength to more than 250. Our domestic has grown by 100% in last 6 months.

@yogansh Did you get any update from management about their focus on increasing domestic sales during AGM. Their domestic revenue has not shown any improvement last year.

| FY | 18 | 17 |

|---|---|---|

| domestic(in Crs) | 127 | 134 |

| exports | 370 | 304 |

21 Likes

1 Like

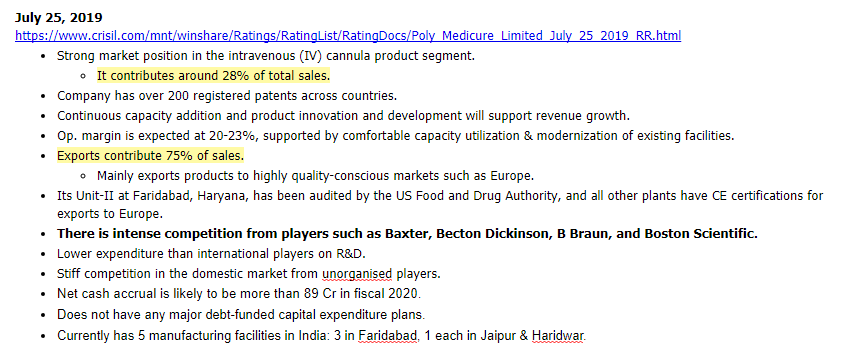

Hi All,

Sharing my notes from the credit rating report.

Regards,

Yogansh Jeswani

Disclosure: Tracking.

10 Likes

Q1 results:

Standalone revenues 152.35 crs 16% up, PBT 28.1 crs 26% up, PAT 20.18 crs 48% up

Consolidated revenues 161.58 crs 21% up, PBT 27.72 crs 26% up, PAT 19.8 crs 49% up

Good set of numbers with decent growth in sales & operating profit. Higher PAT growth vs EBIDTA due to lower taxes compared to last year

Disclosure: Holding. Not an investment advisor and Investors are advised to do their own due diligence.

3 Likes

The company continued its growth phase with a solid business performance in the first quarter.The company acknowledges the Government of India’s initiative to promote Make in India products and also thanks Government of India for reducing custom duty on parts /raw materials to make dialyser (artificial kidney) used in dialysis treatment. This initiative will help in reduction of manufacturing cost for dialysers (artificial kidney) and in turn reduce cost of dialysis treatment to patients. The company is expanding its reach in tier 2 and tier 3 cities where demand is set to grow multifold due to implementation of Ayushman Bharat programme (PMJAY).

The company is also setting up a new plant in Mahindra SEZ zone near Jaipur for expansion of manufacturing activities and expand its reach in Europe and Asia.

1 Like

Poly Medicure AR 2019 notes

Company’s 2019 AR is a good read. After the proposed regulation on medical devices sector by the government, investors were skeptical about the profitability growth of medical devices company. Management on the contrary is quite optimistic in the annual report about the growth opportunity presented by various Govt. measures for medical device industry (Ayushman Bharat scheme, Natioanl Medical Device Promotion Council). Also 70% of sales of the company are from exports so any adverse effect, if any on medical devices manufactured by the company, will be limited to domestic sales only. Company is targeting to grow by both organically and through acquisitions (Did an acquisition in Italy during the year). In export market market company competes on price and in domestic market it competes on technology.

Notes from AR

- Company has been recognized as the “Indian Medical Devices Company of the Year 2018” by Department of Pharmaceuticals, Ministry of Chemicals and Fertilizers, Government of India on 18th February, 2019. Biggest recognition and Achievement since inception of the company. The award was conferred based on Company’s export performance, R&D efforts and New Product launches.

- Company has achieved net sales of Rs. 610.83 Crores as against the net sales of Rs. 521.68 Crores in the previous financial year, which has registered a growth of 17.08%. EBITDA has increased to

149.12 Crores as from135.96 Crores in the preceding year. Profit after tax of ` 65.40 crore. - Some of the key products are: • Short PIVC’s (Peripheral IV Cannula) • Mini MID Lines • MID Lines • CVC (Central Venous Catheters) • PICC (Peripherally Inserted Central Venous Catheters) • PICC Ports

- Top exporter of medical devices in past 6 years.

- A new manufacturing plant will come up in Mahindra SEZ, Jaipur by early next year.

- Turnover

Infusion Therapy Products: 68.60%

Blood Management: 11.48% - Remuneration of KMP is Rs. 8.75 cr.

- This year Company is introducing new products in VASCULAR ACCESS / INFUSION THERAPY.

- Approximately 70% of our total revenues come from exports.

Export Sales: 403.67 cr

Sales to Related foreign Subsidiaris: Rs. 23.35 cr

Domestic Sales: 163.97 cr

Forex Earned Rs. 387 cr (Rs. 344 cr in FY18)

Forex used Rs. 155 cr (Rs. 145 cr in FY18) - Capex of Rs. 49 cr.

- Borrowings on March 2019 at Rs. 160 cr ( Rs. 133 cr in FY18)

- Research and development expenses increased from

1004.78 lacs in fiscal 2018 to1014.90 lacs in fiscal 2019, primarily on account of increase in employee benefits expenses for research and development. As a percentage of total revenue, R&D expenses decreased from 1.87% in fiscal 2018 to 1.61 % in fiscal 2019. - Liquid assets (Cash, Bank and MF Investment) of Rs. 75 cr approx.

- The subsidiary companies performed as follows:

- Poly Medicure (Laiyang) Co. Ltd, China - The wholly owned subsidiary Company has achieved a turnover of

1,098.90 lacs for the year ending 31st March, 2019 against1,421.71 lacs in the previous year. The Performance during the year was impacted by low order book. - US Safety Syringes Co., LLC, USA – The Company has been shut down and dissolved on 10th June, 2019.

- Poly Medicure B.V., Amsterdam, Netherlands - During the year under review the Company has incorporated a 100% subsidiary company in Amsterdam, Netherlands in the name of Poly Medicure B.V. for global operations, further it will be used for expanding business organically and inorganically. Investment of Rs. 34.17 cr. Poly Medicure BV, Netherlands invested Rs. 3348.36 lacs in Plan 1 Health Italy,. Goodwill amounting to ` 2858.11 Lacs have been created on consolidation.

- Plan1 Health s.r.l., Italy, a step-down Subsidiary – During the year under review, the Company has acquired a 100% step-down subsidiary i.e. Plan 1 Health s.r.l., Italy.

- The Company has one Associate in Egypt, viz. Ultra for Medical Products Company (ULTRA MED), Egypt – The Associate has achieved sales of

7,532.73 lacs during the year end December 2018, against6,183.26 lacs in the previous year. Share of profit Rs. 1.39 cr ( Rs. 1.24 cr in FY18).

- Poly Medicure (Laiyang) Co. Ltd, China - The wholly owned subsidiary Company has achieved a turnover of

- Future growth opportunities

- Higher Medical Devices consumption expected in India due to implementation of Aayushman Bharat. This Universal Healthcare Insurance Scheme in India will be a big game changer for the Medical Devices industry.

- Higher Private Insurance penetration driving the consumption of medical devices

- Higher growth expected in Renal Care & Diagnostic industry

- National Medical Device Promotion Council - Under Ministry of Commerce & Industry, Department of Industry Policy & Promotion (DIPP): The setting-up of the Council will boost domestic manufacturing as it will act as a facilitating promotional & developmental body for the Indian Medical Devices Industry.

- The sector at present growing around 12-15% Compound Annual Growth Rate (“CAGR”). A significant percentage of purchasers of medical devices are private medical institutions and hospitals. Due to increased competition in Tier I cities, private enterprises have started to focus on Tier II and Tier III cities, a market which is until now untapped in India. As private enterprises expand in lesser explored markets, the demand for medical devices will expand proportionally.

Regards

Harshit

Disclosure: Tracking

13 Likes

Hi Amit.

-

There was no equity dilution (no funds raised) in 2014 and 2017. Company issued bonus shares in both the cases.

-

What do you mean by “generating free cash”? Operating cash flows or Free Operating cash flows after maintenance capex? Both are positive for last two years.

-

Yes the debt has doubled in the past 5 years but so has the sales. Debt to Equity at 0.5 times and Interest Coverage Ratio at 11 times are pretty comfortable ratios. Company has cash of around Rs. 75 cr also.

Regards

Harshit

3 Likes