Been researching this business and several others slowly over the last few weeks. Benefits of a bear market that you can actually take your time ![]()

It is interesting to see how Poly Medicure has evolved over the last decade. It looks like it plucked a lot of the low hanging fruit in the IV Cannula business in the initial part of the decade.

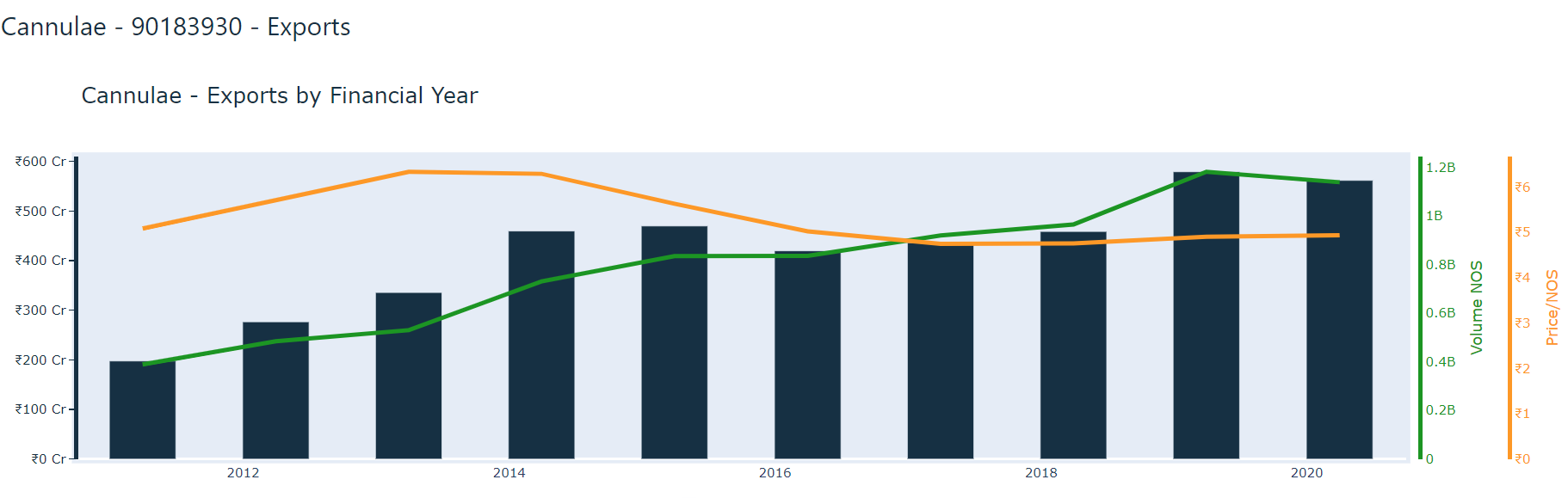

*FY20 Export numbers aren’t complete as Feb/Mar numbers aren’t in yet. There is likely 15-20% growth in FY20.

It looks like Export sales makes up nearly 70% of the business and Europe in that makes up a bulk of it (> 50%?). So it is easy to see why Cannulae exports sort of mirror the fortunes of the company in terms of more than doubling sales in the first half of decade. (IV Cannula made up 45% of sales in FY '11)

In the second half of the decade, Cannulae exports have barely grown until FY19 where there was a spurt (Again reflecting in company’s topline).

One good thing though is that the Company has introduced several other products which has sort of helped it grow at faster rate than IV Cannula (50% topline growth from FY15-FY19 compared to 25% growth in Cannula Exports). This probably came from company diversifying as well as being able to penetrate the market domestically. This though is a lot of hardwork compared to the tailwind in the first half.

One thing to note is that the per unit export price seems to have stayed around Rs.5 for 10 years! Hardly any pricing power here - Its clearly a low cost advantage that we have but even a slight growth in realisations here can drive up Value a lot. This is clearly a repeat volume business with a low-cost advantage.

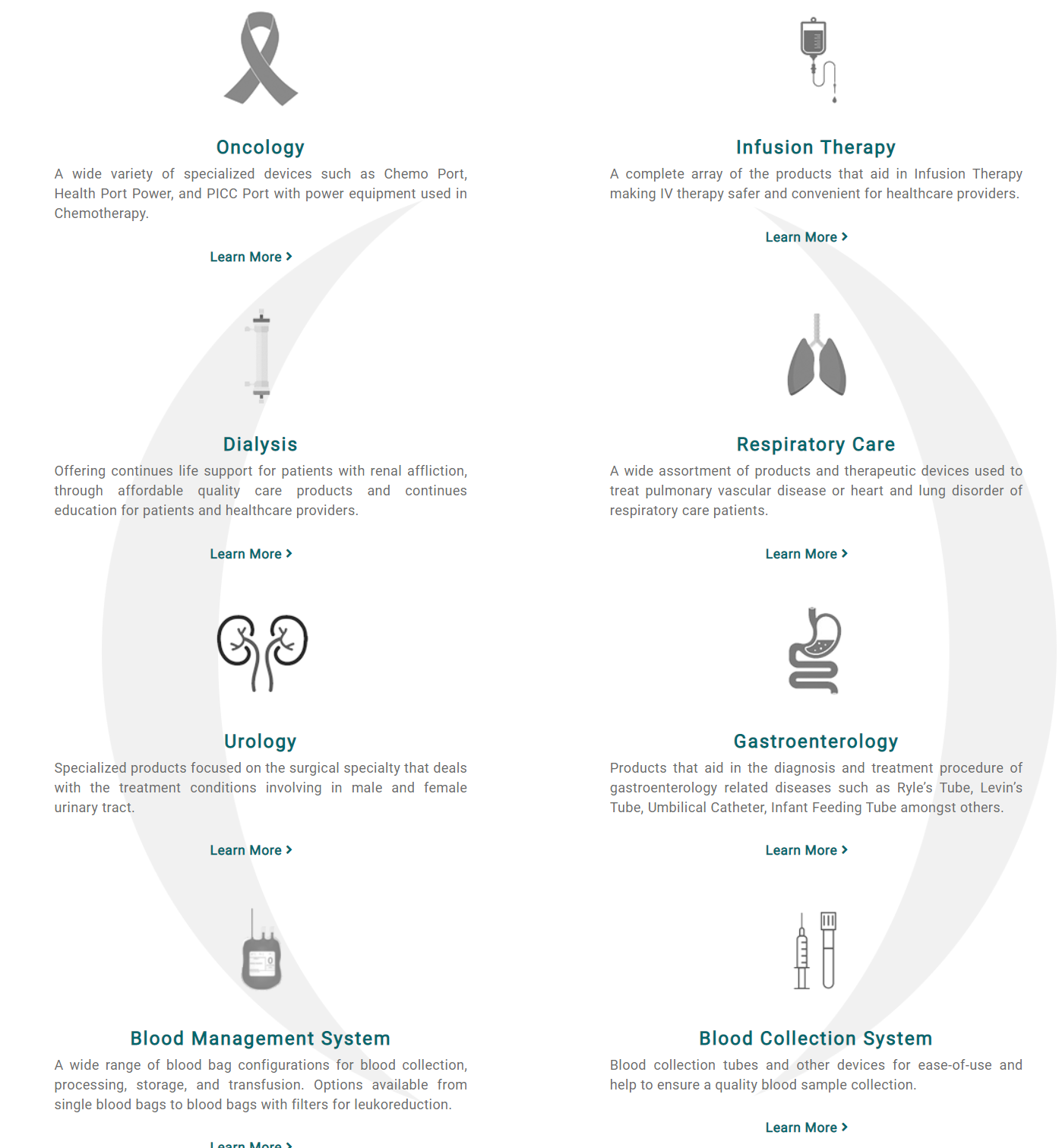

Am not sure how many products the company had back in FY '11 - FY '15 but the product catalog and therapy areas seem pretty wide, though most of them may be small contributors as of now.

Infusion Therapy is probably the one driving bulk of the Sales (nearly 70% of Sales) as of FY19. Blood Management, though the company has put in a lot of effort has not been able to grow to compensate for reduction in growth in IV Cannula business. Dialysis and Respiratory Care are relatively newer therapy areas which are probably yet to contribute in a big way. Blood Collection - Looks like company was selling 25 million tubes in FY10 - Not sure how this segment has grown since, especially given the growth in diagnostic business.

The latest Italy acquisition Plan1Health appears to be in complementary areas of Vascular Access in the Oncology therapy area. The site is in Italian, so if you want an English version - Try this Google translated version. It gives a fair idea of the competency and areas of business. Looking at the recent dispatch to the exchanges in Feb in terms of setting up a subsidiary in India of the same name, I think the company probably plans to manufacture Plan1Health’s products here in India for cheap and export it. I might be wrong. This may give a good foothold into the ageing European market for the company, which is a big positive if executed well.

Overall, it seems to be a reasonable bet - Price hasn’t moved anywhere in 5 years probably due to big optimism built into it in the first half of the decade. The business hasn’t done badly but definitely not done as well as it did in the first half when it had tailwinds. After that it has had to work hard at it but it has not sat back clearly. The consistent 20%+ operating margins over the entire decade shows that the company definitely has some sort of moat in its line of business. It may only be a matter of being aggressive in getting into markets and keep introducing new product lines. Since these are all low cost/high volume products probably sold via the same distribution channels to the same end users, there can probably be lot of leverage over time.

Not sure if the business had any advantages due to Covid-19. Probably the Blood sample collection, IV Cannula and the respiratory care products could have seen more demand than usual. Looks like 50% of the facilities were functioning during the lockdown as well.

Disc: Been buying around 230 levels.