Polymed, Weekly - Flag breakout. Not a technical pick for me and the fundamental thesis is in the Polymed thread here and here. The Q3 performance has been good, the product pipeline and R&D spends encouraging. Valuation is fair and not cheap but not as expensive as some storied localized manufacturing/PLI stories like Dixon.

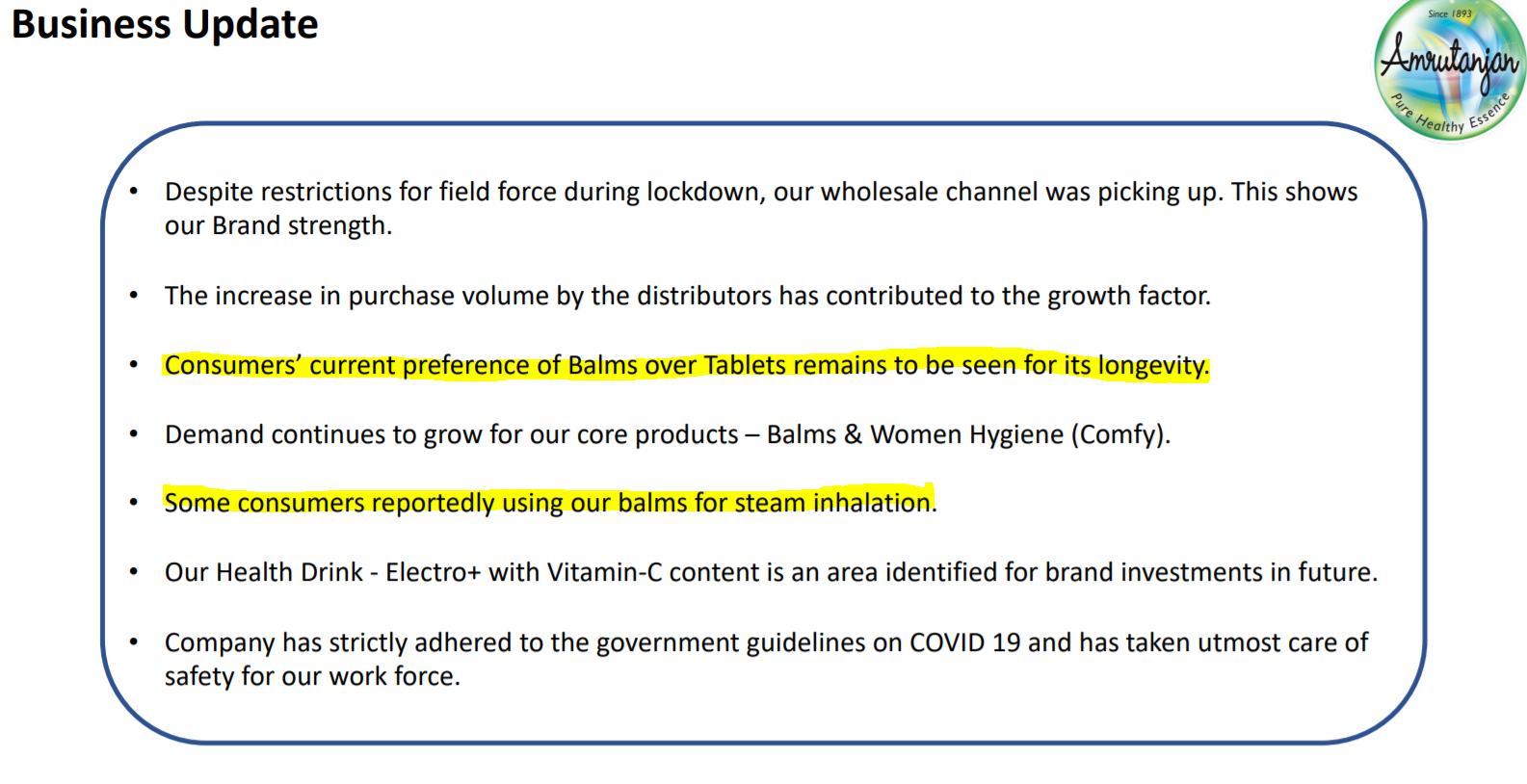

Amrutanjan update from here - Amrutanjan Q3 numbers pretty good. So maybe Q2 wasn’t a one-off? Its still hard to say and the Investor Presentation is as clueless as me.

They are also not sure, clueless or conservative? My guess - Winter started early this year and has lasted longer and coupled with Covid and suppressed Menthol prices, lead to good numbers last couple of quarters. Will know in the coming quarters. Comfy has had a 22% growth as well which is great. Price appears to be breaking out as well with volumes.

SH Kelkar update from here. Good numbers but market reaction has been too tepid for comfort. This was apparent in the earlier business update with the great sales growth reported. Reasons probably are the promoter stake sale (Keva Cons.) around 116 levels and the debt reduction plan probably going to be delayed due to increase in working capital owing to stocking of RM on account of price volatility.

Disc: Holding Polymed from 230 levels. Amrutanjan from 460 levels. Kelkar from 98-108 levels. No transactions in Polymed and Amrutanjan recently. Kelkar reduced allocation recently as story is changing from what I perceived but still continue to hold some.