If anyone can help me understand this - it will be very helpful for me. Thank you

Ex:

FOCO (Franchise Owned Company Operated): Franchise - PNG & Sons, Company- Gargi

1st Jan: PNG & Sons: Inventory - 1Cr

31 March : PNG & Sons: Inventory - Inventory: 1.1Cr

Inventory Transfer from Gargi from 1st Jan to 31st March - 20 Lac

Sales accounted by Gargi = 1Cr + 20 Lac - 1.1Cr = 10 Lac

This inventory of 1.1cr on 31st March goes to Gargi Books as Assets

FOFO (Franchise Owned & Franchise Operated)

1st Jan: Inventory of 1Cr moves from Gargi Books to PNG & Sons Books

Sales Accounted For Quarter by Gargi now is 1cr + 20 Lac = 1.2 Cr

Sales for the period is inflated because of 1 time inventory Transfer

But this is only 1 quarter phenomenon, going forward PNG & Sons will only replinish inventory which is being sold to end customer

Hope this helps

4 Likes

Recently company announced launch of 9 carat plain gold jewellery under Gargi brand. Its an interesting segment to enter in current high gold price scenario. This will provide another growth avenue for the company. With stronger balance sheet due to its recent preferential issue ( Rs 970/share) and systematic store expansion beyond Maharashtra , company is ready to begin next phase of its growth. Main board listing in early 2026 would take away SME tag making stock rerating a real possibility.

Disclosure - Invested as part of my core PF. Adding more on every drop. Not a buy or sell recommendation.

5 Likes

Expect PNGS Reva Diamond IPO (whenever that happens) to have rub off effect on PNGS Gargi stock price. Also expect good quarter this time, aided by inventory gains due to rising silver prices (which can get partly offset if they are not able to raise prices fast enough)

PS added post Q results : great results, which means company is able to pass on silver price rise to its customers. This is much better news than the results itself

Bingo!!!. Your prediction for results are 100% right. Congratulations!!!

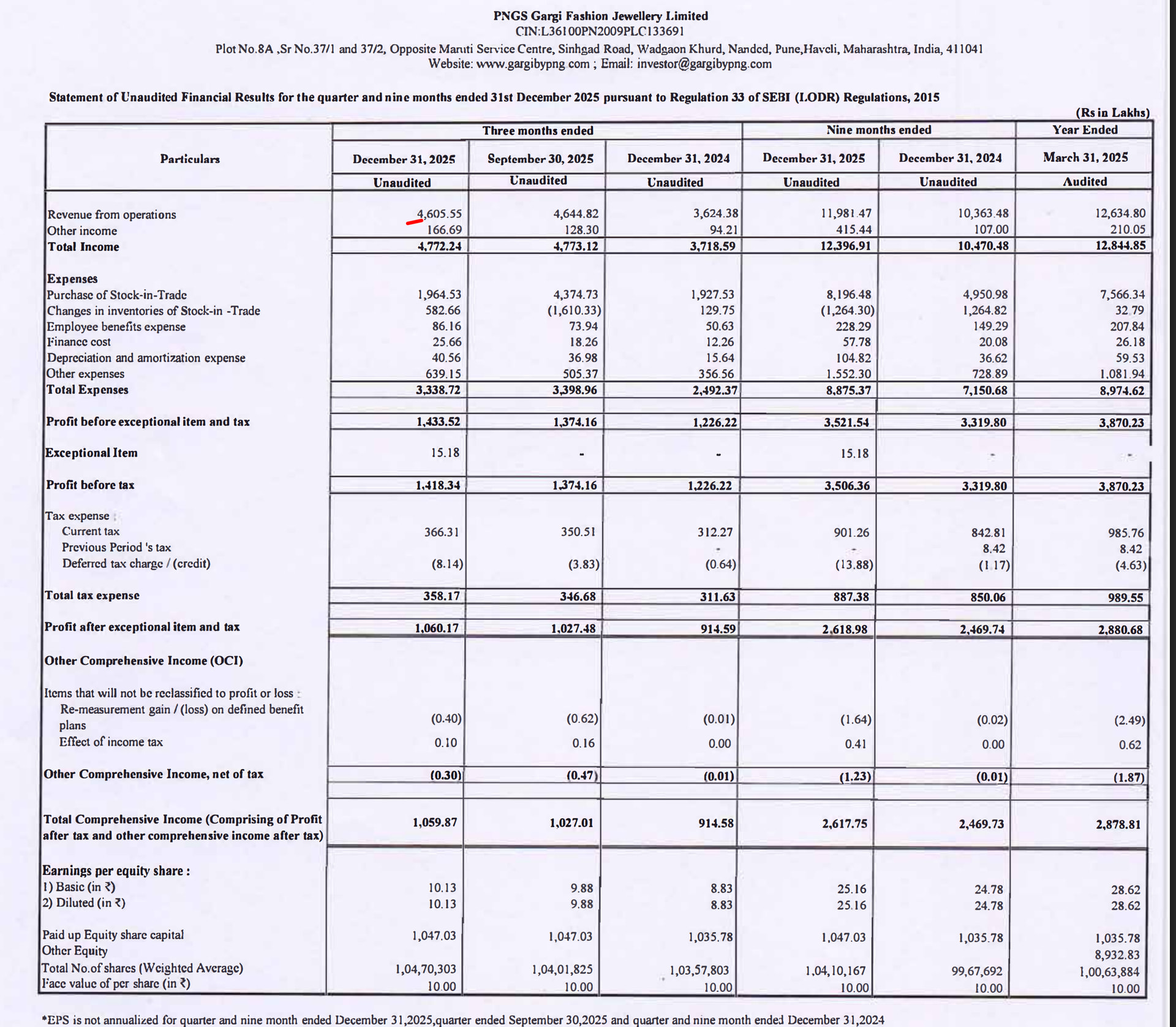

Great Results of Q2 FY 26. Revenue and profit doubled.

1 Like

Gargi posted good set of numbers today.

| Metric | Q2 FY26 (₹ lakh) | Q2 FY25 (₹ lakh) | YoY Change |

|---|---|---|---|

| Revenue from operations | 4,644.82 | 2,295.10 | +102 % |

| Total income | 4,773.12 | 2,305.67 | +107 % |

| Profit before tax | 1,374.16 | 690.97 | +99 % |

| Profit after tax | 1,027.48 | 509.35 | +102 % |

| EPS (₹) | 9.88 | 5.14 | +92 % |

Thanks to Gold prices surging, it moves some consumers to fashion jewellery.

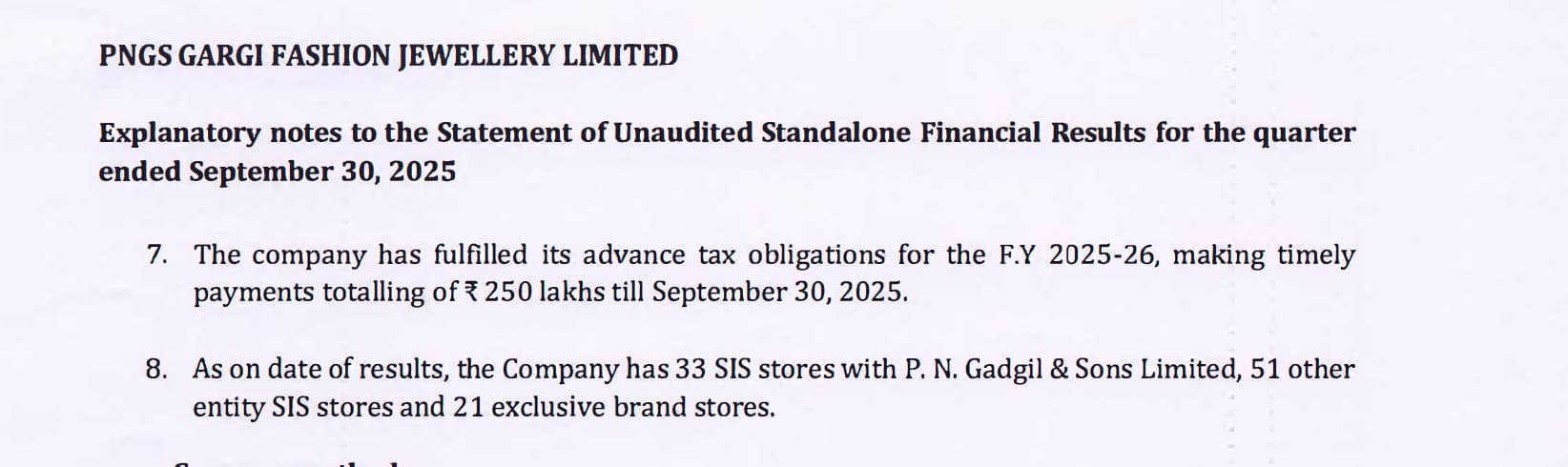

As on date of results, the Company has 33 SIS stores with P. N. Gadgil & Sons Limited, 51 other entity SIS stores and 21 exclusive brand stores.

Store count is 105 as of this results, they had 84 stores as of my post in feb 2025. So their target of 118+ can be achieved by march 2026.

14 Likes

6 Likes

1 Like

With silver prices at elevated levels, how does this impact Gargi’s margin profile and sales volumes? In their DRHP, they clearly stated that volatility in silver prices can affect profitability and demand including scenarios where higher silver costs could reduce sales volume and compress margins if price increases cannot be fully passed on to customers.

Given the current price environment and Gargi’s heavy exposure to 92.5% sterling silver products, do we have any insights on whether the company uses hedging or other risk-mitigation strategies for raw material price fluctuations? The DRHP doesn’t mention hedging arrangements, and I’ve not seen disclosures on this in earnings calls or reports.

Additionally, any views on the Silvery jewellery sale trend in general in December and also impact on gross and EBITDA margins in the near term given recent commentary that rising silver prices have already weighed on gross margins due to timing of label price adjustments?

Not hedging is not a risk for this time. Since the silver price went up it’ll result in inventory gain (silver price went up after they bought it ).

1 Like

Volatility in silver price was much higher in January, so Q4 will be the real test of company’s operational resilience. In Q3, while topline growth was strong, profitability didn’t increase at the same pace which caught me by surprise as I was expecting operating leverage to come into play. Is it due to relatively new expansion of exclusive stores which takes more time to get mature and hence profitability expected to remain subdued in coming quarters?

Invested and added recently, average buy price is 1000

Quick analysis of this quarter’s results as compared to last quarter as well as last year shows expense increased mainly in 4 areas

- Other expenses - 6.39Cr (5.50Cr Q2 FY 26, 3.57 Cr Q3FY25)

- Employee Benefits - 86Lacs (74Lacs Q2 FY 26, 54 Lacs Q3 FY25)

- Finance Cost - 26 Lacs (18Lacs Q2 FY26, 12 Lacs Q3 FY25)

- Depreciation - 41 Lacs (37 Lacs Q2 FY26, 16Lacs Q3 FY 25)

One time hit of 15 Lacs due to new labour code.

As you can see, item no. 2, 3 and 4 are due to new store expansions. But major increase happened in other expenses which include marketing expenses. Company in its last concall mentioned that they are planning to spend around 7Cr this financial year. (4 CR in FY 25)

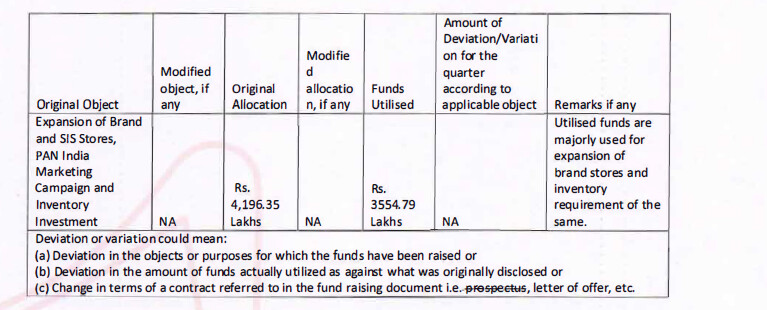

This is also reflected in the preferential issue fund utilization declaration to the stock exchanges wherein they mentioned using Rs 266.64 Lakh in last 3 months for marketing and promotional expenses for this quarter.

So results were in line with expectations.

5 Likes

Q3 FY 26 Performance & highlights

1. 27% YoY topline growth; however excluding the one time sale of 25 cr due to change of model to FOFO last FY; YoY revenue growth is ~ 53%

Outperforming the market on growth.

2. Category dynamics

Indian fashion jewellery market 10,000 cr likely to grow to 30,000 cr by 2030 ; share of organized retail is < 10% ; huge headroom for growth. Fashion jewellery growing @ 11.5% CAGR

3. Financial Metrics

-

Gargi operating at 31% EBITDA margin and 22% PAT margin

-

Zero debt company

-

FOFO model, superior unit economics

-

Asset light model; delivered 130 cr topline from 4.7 cr fixed assets

-

Currently at miniscule mkt share of 0.15% , signifying headroom for growth

Only player with 20+% PAT margin; with PAN India reach, good corporate guv. and strong legacy.

4. Benchmarking with other peers

- Gargi operating at 31% EBITDA margin and 22% PAT margin. Superior margin profile than peers

- Largest competitor in fashion jewellery at 6% EBITDA and 2.7% PAT margin

- Apple to apple sized peer, is loss-making @ 58 cr loss. (likely to be Giva)

- Global brand operating at 11% PAT margin and 18% EBITDA margin

5. Store locations and launch

- Had indicated 12 locations to be opened in last call. Opened 16 locations. Surpassed the guidance given on store launch

- 121 points of sale across India, as on date.

- Planning to launch not less than 20 stores (25 to 30 likely locations) in next FY. Mostly in North India where fashion jewellery is popular. Franchise model stores need capex of 25 to 30 lakh (silver jewellery). Own stores need higher investment of 1 cr capex

6. Expansion

- Pune currently has 16-17 stores; has potential for 40 stores

- With fashion jewellery, allows the agility to quickly expand to other locations in adjacent region after launching in 1 city.. Concern of varying preferences mainly in Plain gold jewellery– different preference in Maharashtra vs South vs Gujarat. But not in fashion jewellery.

7. Brand Awareness

Fund raise of 10 cr – with promoter participating. Utilizing funds for a Brand awareness campaign across India

- Transforming from regional to PAN India marketing in next 24 months

- Marketing spends 3.6 cr in 9M in last year; vs 6.5 cr spends in this FY.

- Focusing mostly social media marketing. PIN code wise marketing and time band wise marketing

- Mithila Palkar– eliciting good response/ acceptance among North customers too

8. Product wise specifics

-

Share of silver jewellery – 38% diamond jewellery and 57% silver. Likely to move to 45% and 55% by H1 next year.

-

Recently added 9 carat gold

o Avoiding in 33 PN Gadgil store locations. To avoid conflict of interest. Selling in exclusive Gargi stores

9. Store performance

- Laxmi Road, Pune (standalone) store crossed 2.25 cr in 1st year of operations.

- Very good response in non-Maharashtra markets (Lucknow, Amritsar, etc) as well. Helped by SIS strategy with Shoppers Stop pan India.

10. Guidance of 20 to 22% PAT margin going forward

11. Aditya Modak (next gen) was also present in the call

12. Migration to Mainboard exchange

- Some revision in criteria. Min 15 cr Operating Profit for 3 years. In 1st year company didn’t meet criteria

- On completing FY 26 – will meet criteria. So migration likely by Q2 or Q3

Disc: Invested

3 Likes

Highlights from Q3 FY 2026 Gargi Con-call:

- Successfully opened 16 stores, the goal set was for 12.For fy 27 guidance of 20-25 new stores opening.

- As of date having 121 stores in total.

- Pune capacity is 40 stores, right now 15 stores present.

- Zero debt with 70 cash cash balance.

- Can fund 25 new stores with current cash pool, not planning to take up any debt or equity fund raise for another 2 years.

- Main board listing around sept 2026.

- Sold 1 kg on a gross weight basis of their 9-karat gold jewelry in the first 3 months itself.

- Committed to grow 35% cagr for next 4 years at topline without compromising on profits, PAT levels to sustain at 20-22%.

- Marketing spend 8-10 crore range, not expecting ROI on this as its not quantifiable.

| Item | Reported Number | Target H1 next year |

|---|---|---|

| Product Mix (Revenue) | 57% Silver / 38% Diamond | 55% Silver / 45% Diamond |

| Same Store Growth (SSG) | Not less than 25% |

| Store Unit economics: | |||

|---|---|---|---|

| Item | Number | ||

| Standalone Shop Revenue (Pune) | ₹1.5 crore – ₹2.5 crore per annum | ||

| Kiosk Monthly Sales | ₹3.5 lakh – ₹4 lakh | ||

| Gura Elante Mall Monthly Sales | > ₹5 lakh | ||

| Franchisee Investment (Silver) | ₹25 lakh – ₹30 lakh | ||

| Franchisee Investment (+Diamond) | ₹50 lakh – ₹60 lakh | ||

| Company-Owned Store Investment | ₹1 crore (Capex + Inventory) | ||

| ROI (Owned Store) | 20% – 25% (within 2 years) |

| Product info : |

|---|

| Gross Margin (Silver) - 55% |

| Gross Margin (Diamond) -45% |

| Avg Ticket Price (Diamond) 15k-25k |

| High-End Ticket Price - 1.25 Lakh |

Industry and competition data :

- Indian Fashion Jewelry Market : Market size is ₹10,000 cr and will grow 2x to ₹30,000 cr by 2030. Gargi has 0.15% share as of now. Organized market share is only 10% now.

| Entity | PAT Margin | EBITDA Margin | |

|---|---|---|---|

| Gargi Fashion Jewellery | 22.8% | 31.3% | |

| Large Competitor | 2.7% | 5.5% | |

| Global Brand | 11.8% | 18.3% | |

| Direct Peer | Loss-making (₹58 cr loss) | N/A | |

| Other Industry Brands | N/A | 12% – 15% |

5 Likes

On your last comment - Do you mean Industry will grow 3x by 2030 and not 2x (typo)?

Also, how come Gargi has 0.15% market share? Annual revenue close to 150cr, overall market is 10kcr, so market share is 1.5% and not 0.15%!

Lets focus on absolute numbers on what management stated in the call. We can find it in page 3-5 on what was discussed.

2 Likes