SECTOR BACKGROUND

Awarding activity in road sector has picked up pace in the past two years and is expected to remain firm in the next 2-3 years. In FY16, the government awarded 10000 km of road projects and in the current financial year, it targets to award over 25000 km or Rs 3 trillion of road projects. This trend is expected to continue in the coming years.

COMPANY BACKGROUND

• PNC Infra Ltd (PNC) is a north-based EPC/BOT contractor (www.pncinfratech.com)

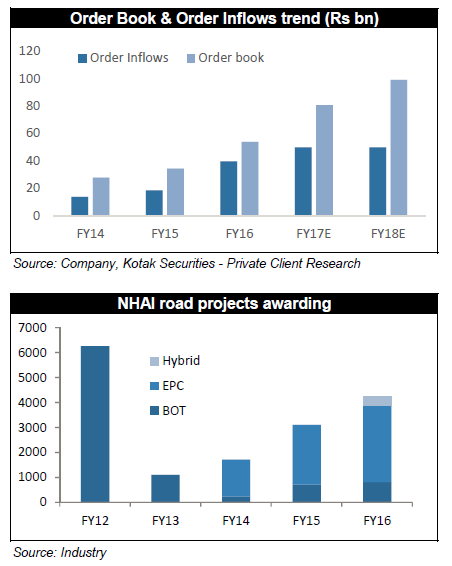

• Strong order book visibility: PNC has an order book of ~ Rs 5100 crores (2.5x FY16 EPC revenues). Further, PNC has won Rs 1374 crores worth of orders won from April 2016 till date, financial closures of which are expected to be achieved by October 2016.

• Strong execution track record: PNC has a proven track record of early completion of projects in a sector marred by inordinate delays. It has the distinction of being among the first few to receive an early completion bonus from NHAI.

• Multiple operating efficiencies: PNC’s four pronged strategy:

a. conservative bidding

b. operating in a core geographic cluster

c. ‘No subcontracting’ policy in critical construction activity and

d. a large equipment bank, have enabled the company expand its EBITDA margin 500 bps during FY13-FY16 to ~17%.

• In FY16, PNC enjoyed a 11% market share of the NHAI’s Rs 48,100 crore EPC order book, second only to the infrastructure behemoth, L&T (12% share).

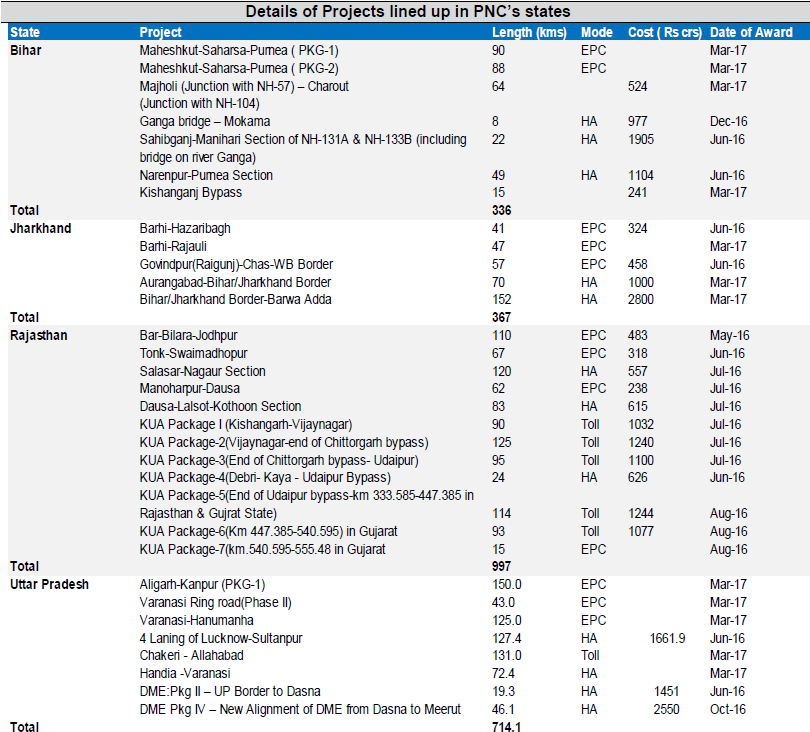

• PNC has executed ~75-80% of its road projects in UP, Jharkhand, Bihar and Rajasthan. These states have a robust pipeline of road EPC projects over 2016-17 – 4 states alone account for 36% of the 6631 kms of road projects that NHAI intends to award in FY16.

• The govt is now acquiring 80-90% of the land before announcing the date for commencement for construction

• Gathered enough qualification credentials to independently bid for a single project to a tune of over Rs. 3,000

• Currently co is executing 16 projects in roads & airport runway sector

• Currently we have 7 operational BOT projects of which 5 are Road BOT projects, 1 is Road OMT project and 1 is Industrial Development project

• Our consolidated net worth as on June 30, 2016 is Rs. 1,364 crores whereas total debt is Rs. 1,722 crores. Net debt to equity comes at consolidated basis comes at 1.13 times.

• There are 17 new EPC orders worth Rs 15,000 cr that will be up for bidding

• Toll Revenues - Gwalior - Etawah MP Highway is Rs. 15.5 crores; Kanpur - Ayodhya is Rs. 69.8 crores; Kanpur Highway is Rs. 24.7 crores and Bareilly - Almora was Rs. 9.6 crores; Ghaziabad - Aligarh is 37 - 38

lakhs per day

• PNC has long history in the roads sector with over 15 years of experience in executing NHAI projects. PNC has track record of timely and before schedule completion of projects and received early completion bonus.

• PNC is focused on the northern region and is expected to be a strong contender for grabbing future opportunity in road construction from poll bound states like UP and Punjab.

• PNC has robust current order book of Rs 64.7 bn and further targets to add another ~Rs 40 bn of orders in the rest of the year based on robust pipeline of orders specifically in road space. This gives high revenue growth visibility for the next 2-3 years.

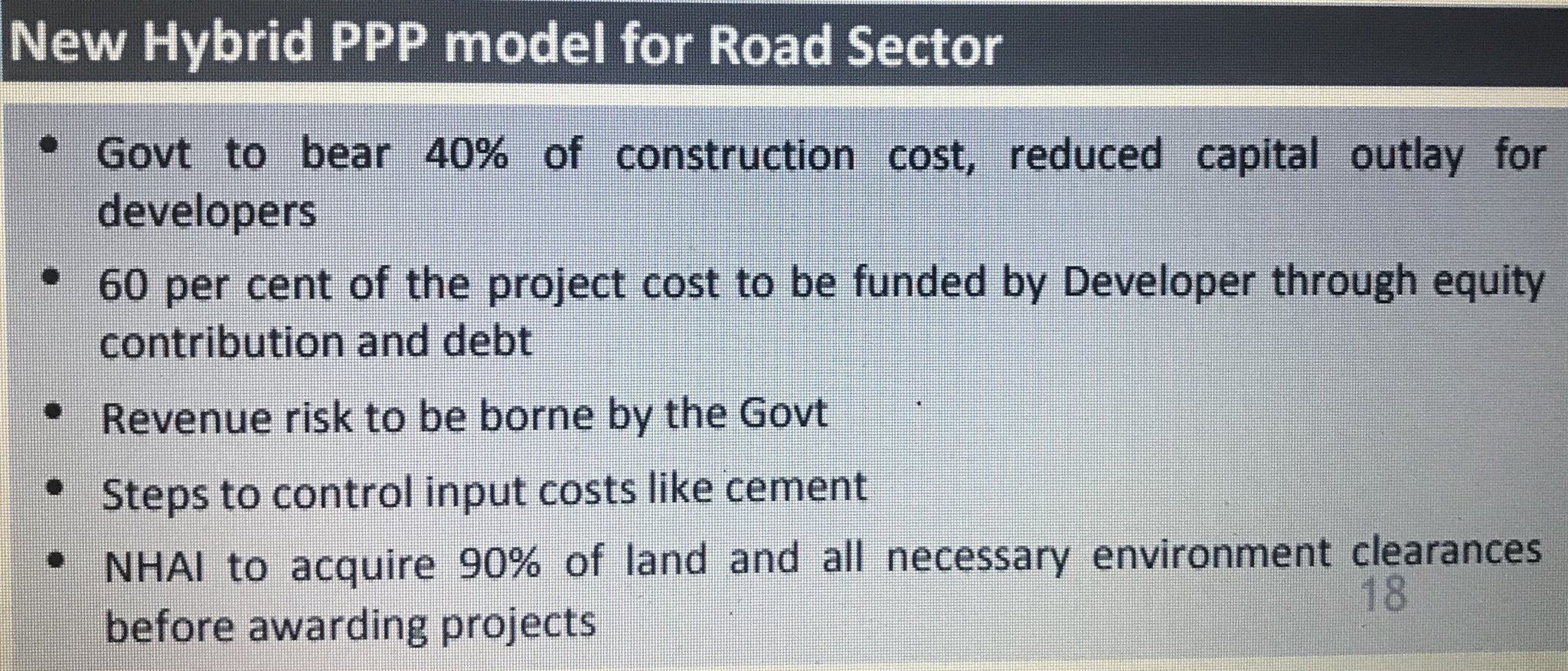

Understanding the Hybrid Model of Road Development

Funding - The government will contribute 40% of the project cost in the first five years through annual payments (annuity); developer to raise remaining 60% through debt or equity. Semi-annual annuity payments will be paid to the developer for the balance 60% of the project cost

Disbursement

Government’s 40% contribution will be disbursed in accordance with the project completion milestones (24%, 40%, 60%, 75%, and 90%)

Revenue Collection -

i) Responsibility of NHAI

ii) The Government / NHAI will collect the toll and pay the developer annuity payments over 15 years along with interest thereon at bank rate + 3%. The developer will also receive O&M payments bi-annually along with annuity payments.

iii) All project payments will be inflation indexed.

RISKS & CONCERNS

• Slowdown in road sector

• Aggressive bidding of projects

• Inflows of large size BOT projects

Disclosure: I am invested in the stock and my views are likely to be biased. Please do your own due diligence or consult a SEBI registered investment analyst.

Thanks Abhishek for the post. Road sector has definitely seen momentum in the last few quarters and continue to do so. Its a new business for me, would request your inputs to understand it more. They do two types of businesses - EPC and BOT/annuities.

As i understand EPC is purely services business and is working capital heavy. A) What kind of EBITDA margins do they expect to do in this vertical? Their margins shrank by ~50 bps in FY16 to 14%. B) Any idea on whats the the quantum of performance guarantee fees that the client retains with it and for how long? C) How much worth orders can PNC execute an one year?

BOT - A) What kind of IRR do they expect to make in BOT projects? B) Are they adding BOT projects going forward, my understanding is, please correct me if that’s wrong, BOT projects are capital intensive and tend to result in poor returns.C) As per your info, 5 BOT projects’ yearly revenues come to ~250Cr, what’s PNC’s share in this cash flow stream and how much of that flows to bottom line (PBT and PAT level, whats the opex and tax costs)? D) Is PNC secured in case govt decides to stop charging passengers for toll like it happened in gurgaon and at few places in Maharashtra some time back?

Historically, free cash flow in this business has been very poor. While this is the case for most of the companies in their growth phase, what is your expectation on by when PNC can be expected to start generating some FCF?

Based on FY16 numbers, it made ROCE of ~11%, do you think this business can inherently generate ROCE of 15%+?

Any idea on whats this line item called ‘Concession rights’ (under intangible assets) worth ~2,100Cr (huge addition in FY16)?

How do you assess and get comfort around corporate governance of PNC, given most or all of the players are marred with CG issues in this sector?

they have changed their revenue recognition, would request you to comment on what do you think whether is it a conservative or an aggressive accounting move?

PNC Infratech operates in two segments EPC and BOT.

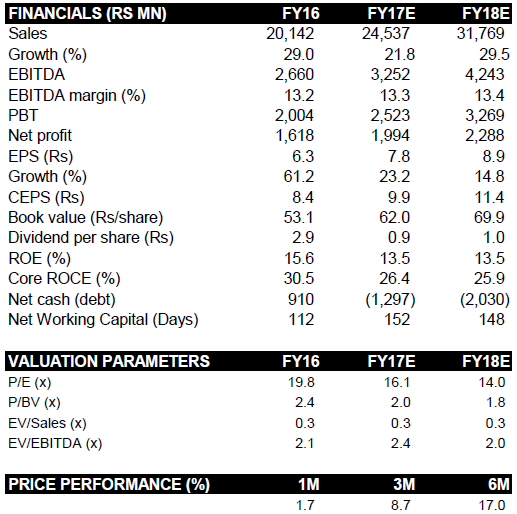

EPC segment is expeted to deliver strong EPS of INR 7.5 & INR 8.0 and RoCE ~18% over the years FY17E & FY18E based on strong order backlog given above. PNC has strong execution track record that results into good EBUTDA margins led to higher RoCE. EPC business could get multiple from 12x-15x.

BOT (7 projects) are not expected to perform well in upcoming quarters due to slowdown in industrial activities (as suggested by most of BOT players) led by demonetization impact. BOT Toll projects, difficult to generate RoCE. This will be hangover for this company either they don’t think to divest them. Asset light companies like KNR are getting higher valuations due to this reason.

My two pence:

I am not covering positives as these are already covered and known.

Enterprise Value is around 5200Crs is not cheap. The margin of safety is not very high. Also, their expanding in power sector is not a welcome thing. They have listed two projects on the site. I am not sure about the current power projects in hand and their focus on the sector. If they are pursuing this, I would like to be cautious about it.

Also, I am not too sure about the success of Hybrid Model of Road Development and how it is going to further stretch the balance sheet of the company. Remaining points about the BOT covered in other reply are applicable.

PNC states that going ahead they expect EPC contracts pie to shrink and instead HAM model to be the mainstay

Under HAM

There is no toll right for the developer. Revenue collection would be the responsibility of the National Highways Authority of India (NHAI) - The developer is insulated from revenue/traffic risk and the inflation risk, which are not within its control.

Advantage of HAM is that it gives enough liquidity to the developer and the financial risk is shared by the government. While the private partner continues to bear the construction and maintenance risks as in the case of BOT (toll) model, he is required only to partly bear the financing risk.

Government’s policy is that the HAM will be used in stalled projects where other models are not applicable.

Regarding Intangible - Concession Rights

Thats the right in Toll Share that PNC has earned. So typically in a BOT Model the operator has a contractual right to charge users . So he recognises an intangible asset at the fair value to the extent that it has a contractual right to receive - This is amortized over the period in which it is expected to be available for use by the operator.

I am an investor in PNC infra. Good to see post on PNC on this forum.

I have invested considering some of the rationale mentioned by @basumallick.

Some additional points:

Recently inaugurated Agra - Lucknow highway has PNC as one of the four players. It was expected to get PNC a bonus due to early completion. This forms significant part of current executed project (Rs 16.4 bn). Any update on this project. Last con call they have intimated it would be in Q4FY16.

My key variable for investments - track record of before time execution, asset ownership and sector tailwinds providing revenue and profit visiblity, valuation comfort vs peers probably due to state in which company operates which I believe should not be there considering most NHAI projects are getting awarded in these states.

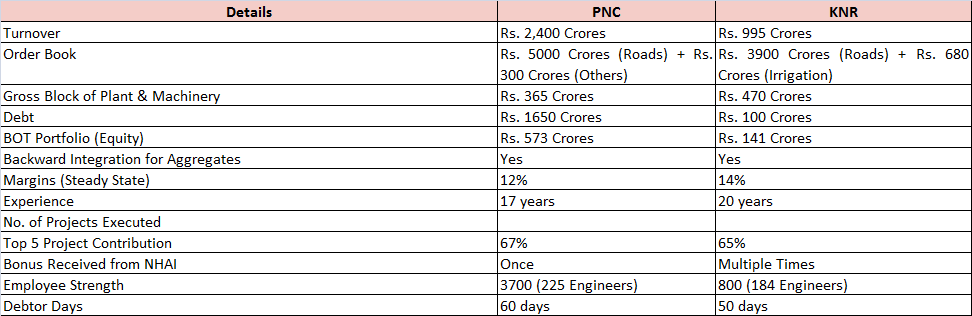

Hi Ashwini, though i have not analysed any of the companies but going by the comp table KNR looks more attractive. KNR falters on just one metric - low asset turns (could that be because they own lot of equipment which helps them complete work faster and make higher margins?? #just guessing). However on host of other metrics from the table, KNR seems to be doing better than PNC mentioned below -

better BS and P&L metrics - low debt, low WC, higher margins for KNR. I think better balance sheet management could be the only reason why market values KNR more than PNC.

high order book of >4.5x revenues vs PNC’s at ~2x

if this bonus thing points to timely execution then that speaks of the track record of management where KNR seems to be doing much better

Given i really have no idea about the businesses and I have gathered my thoughts solely based on the table, my interpretation could be completely wrong.

many thanks Ashwini. This is very helpful piece of info

Is it correct to interpret that private builder bears 2 major risks 1) construction costs under-estimated 2) interest rate risks on the borrowing (i assumed this is what you mean by financial risk)

As for private builder’s cash flows - are they fixed in advance by the govt irrespective of the traffic? If that’s the case then only risks to their IRR would the ones mentioned above or anything else is also there?

Spark Capital in its report has said that such delays are visible in the pace of execution in all the companies. PNC Infratech is the worst hit with 80 percent of road projects awarded since FY16 are delayed.

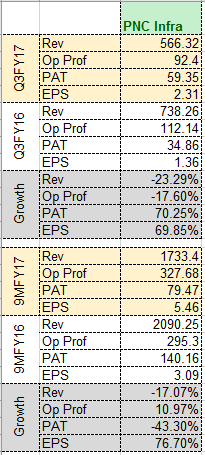

YoY quarterly profit is up 70℅ but operating profit is down by 17.6℅. They had a tax return of 28crs that helped them generate PAT. Is this sustainable, if not we should not call it as a good growth in profits. We should see PBT. It’s flat. In fact PBT growth should have been negative instead of positive. But lower interest cost and higher other income helped. Their interest cost fluctuate every quarter and we need to understand the reasons for it. We need to also answer if higher other income and lower interest cost are sustainable?

The Company being declared the L1 (lowest) bidder in the following two hybrid annuity highway projects of NHAI for an aggregate Bid Project Cost (BPC) of Rs. 2720.0 crore.

Four laning Jhansi-Khajuraho section of NH 75/76 (Package I) from km 0.00 to km 76.30 in the states of UP & MP under NHDP III to be executed on Hybrid Annuity Mode for a Bid Project Cost of Rs. 1410.0 crores.

Five firms participated in the bidding and the price bids were opened on Thursday, March 23, 2017, with PNC’s bid being the lowest (L1).

Four laning Jhansi-Khajuraho section of NH 75/76 (Package II) from km 76.30 to km 161.70 in the states of UP & MP under NHDP III to be executed on Hybrid Annuity Mode for a Bid Project Cost of Rs. 1310.0 crores. Six firms participated in the bidding and the price bids were opened on Thursday, March 23, 2017, with PNC’s bid being the lowest (L1).

What we need to monitor is the financial closure of the projects won, because that is where the current set of problems are cropping up from.

The receivables and interest outgo is much concern for the company as it is comparable to reported profit and has increased tremendously in FY 16. Debt is increasing year on year on consolidated basis which also is a major concern and which I think led the company to opt for IPO.

Somewhere in AR16 I have read that loans has been given to RPs at zero interest rate. Please confirm if anybody else found that.