I couldn’t find the right thread, but feel free to redirect me if there’s anything specific to Punjab National Bank.

Interestingly, I noticed there’s no dedicated thread on this, even though the bank has consistently reported over 100% profit growth quarter-on-quarter since March 2022.

What’s even more surprising is that despite posting over 100% PAT growth in the last two quarters, the stock price remains reasonably priced. Due to overall market conditions.

Note: I am invested in the stock, so my views may be biased. This is not a buy/sell recommendation.

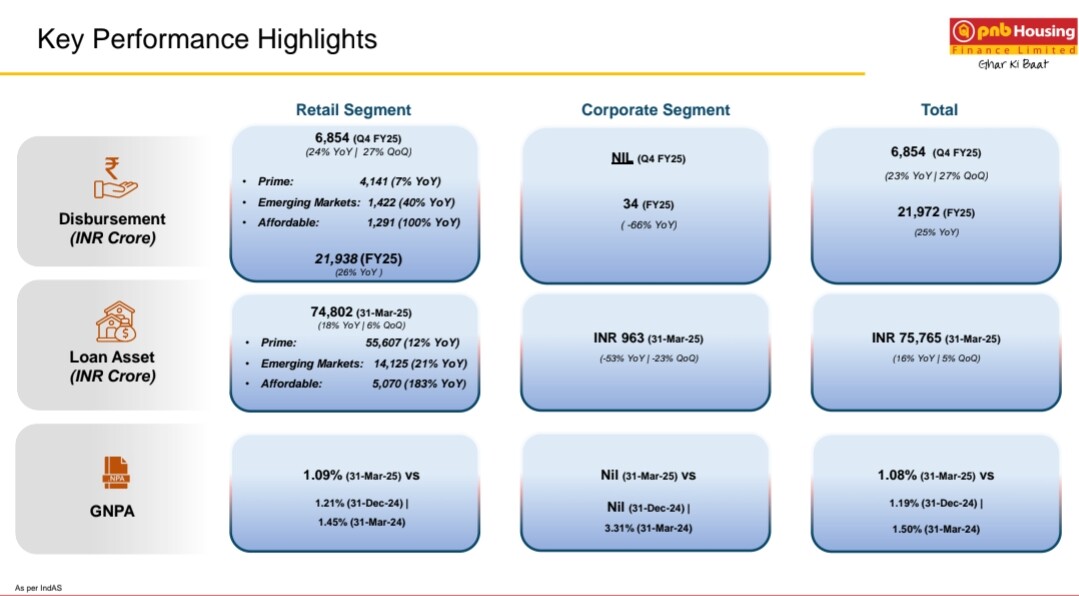

While PNBHF will continue to grow the AUM and increase the share of Affordable, need to closely monitor asset quality, especially as they start to age.

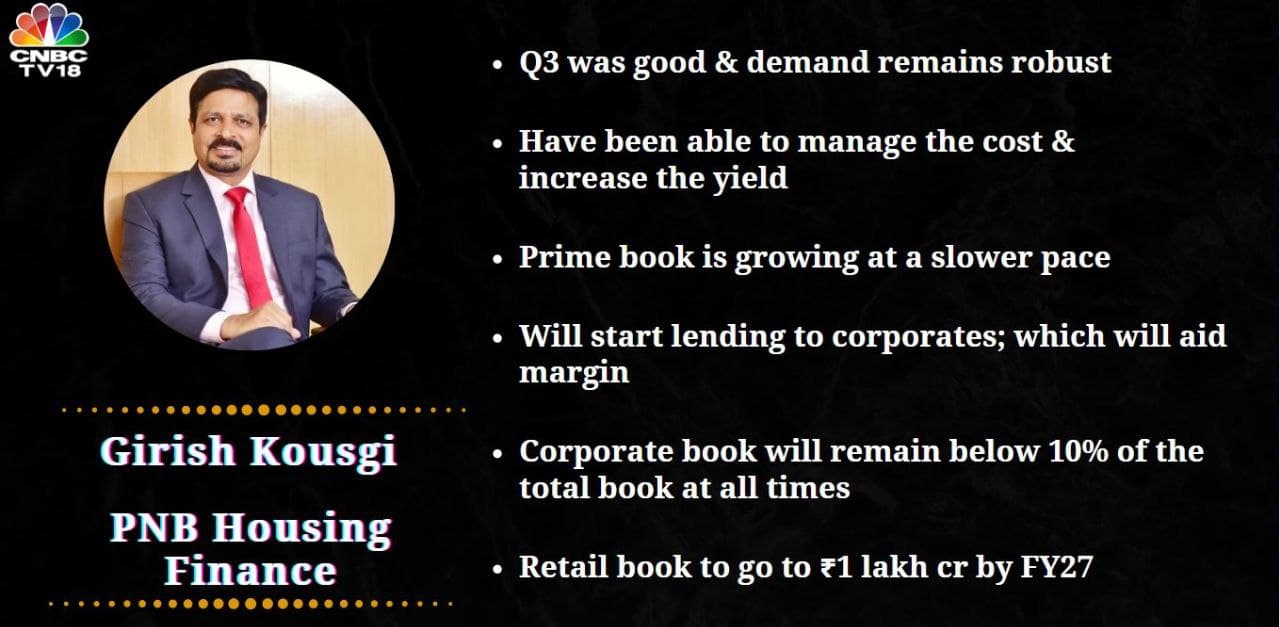

A couple of things from the con call-

To increase the yield in falling interest rates environment, they will need to disburse to riskier class of customers. Management indicated this will happen. They will also increase LAP which is inherently risker than home loans. In Affordable, they have a high transfer-in (20-22%), which again indicates higher risk or lower pricing.

CEO said the bounce rate in affordable is about 11% and they expect to increase to closer to 15% as they increase lending to high risk customers, which is industry standard (per CEO).

For FY26 and FY27, they will be cushioned by recoveries. Beyond that they will need to increase NIM in order to maintain similar ROA.

At the current P/B, these risks seem priced in. But needs close monitoring on quality - as recoveries dry, if the aged loans start turning to NPA, it will be a double whammy.

Any inputs post CEO resignation, generally, what comes to mind if the CEO, who is in the highest position, resigned, SCAM comes into the picture first. Hope that is not the resaon

CEO left only bcoz of much better opportunity. Company is confident of providing continued performance and respective substitute will be replaced in coming time.