Business Overview:

PNB HFL are the fifth largest HFC in India by loan portfolio as of September 30, 2015 with the second largest amount of public deposits in an HFC in India as of March 31, 2015, according to the IMaCS Report. Parent and Promoter is Punjab National Bank (“PNB”), one of the largest nationalized banks in India. Over the previous five years, PNB HFL have implemented a business process transformation and re-engineering (“BPR”) programmed, which has contributed to them becoming the fastest growing HFC among the leading HFCs in India as of March 31, 2015, according to the IMaCS Report. In 2009, PNB sold 26% stake to Destimoney Enterprises (now a Carlyle Group entity). In 2012, Destimoney Enterprises increased its stake to 49% (Before IPO). Loan portfolio grew at a CAGR of 61.76% from ₹39B as of March 31, 2012 to ₹271B as of March 31, 2016.

Product Offered:

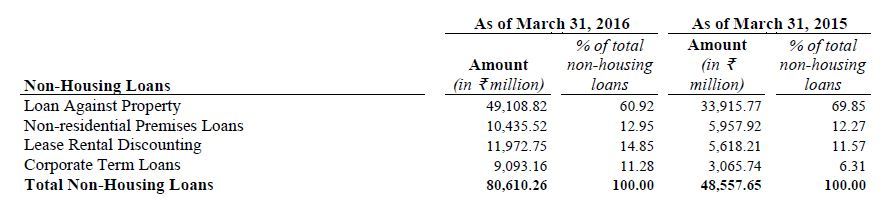

PNB HFL offer customers “housing loans” (71%) for the purchase, construction, extension or improvement of residential properties or for the purchase of residential plots, and “non-housing loans” (29%) in the form of

- loans against property(“LAP”) to property-owning customers through mortgages over their existing property and any additional security, if required;

- Non-residential premises loans (“NRPL”) for the purchase or construction of non-residential premises;

- lease rental discounting (“LRD”) loans offered against rental receipts derived from lease contracts with commercial tenants;

- Corporate term loans (“CTL”) which are general purpose loans to developers and/or corporate for purposes of on-going projects or business needs.

As of March 31, 2016, Among the Housing Loan Book , retail housing loans constituted 87.10% of total housing loan portfolio i.e 61 %. The average loan size (at origination) of retail housing loans as of March 31, 2016 was ₹3.20 million, with a weighted average loan-to-value ratio (“LTV ratio”) (at origination) of 65.92%. As of March 31, 2016, Among 29% of Non Housing Loan , retail non-housing loans accounted for 23% .

The average loan size (at origination) of retail non-housing loans as of March 31, 2016 was ₹5.58 million, with an LTV ratio (at origination) of 46.25%.

A Different Operational Model

PNB HFL conduct operations through an operating model which, as of March 31, 2016, included 47 branches across the northern (40%), western(30%) and southern (30%)regions of India and 16 processing hubs (which include three co-located zonal offices) and our central support office (“CSO”) in New Delhi. PNB HFL branches act as the primary point of sale and assist with the origination of loans, various collection processes, sourcing deposits and enhancing customer service, while their processing hubs and zonal offices provide support functions, such as loan processing, credit appraisal and monitoring, and their CSO supervises PNB HFL’s operations nationally. PNF HFL’s enterprise system solution (“ESS”) integrates all activities and functions their organization under a single technology and data platform, bringing efficiencies to our back-end processes and enabling them to focus their resources on delivering quality services to their customers. Their branches, processing hubs, zonal offices and CSO are supported by their centralized operations (“COPS”) and central processing centre (“CPC”), which provide centralized and standardized backend and administrative activities, payments and processing for their business, relying in turn on their ESS. PNB HFL’s distribution network included over 5,000 channel partners across different locations in India as of March 31, 2016, including their in-house sales team as well as external direct marketing associates (the “DMAs”), deposit brokers and national aggregator relationships with reputed brands.

Stable Margin with Diversified Loan Sourcing :

Given the diversified loan portfolio with significant share of non-retail loans and self employed customers, PNB HF has enjoyed high loan yields. While it currently earns~10.5% yield on home loans, it earns around 100-300bp more on LAP. In addition,self-employed customers are charged 75-150bp more on housing loans due to the inherent volatility of their cash flows. At the same time, the company has worked to diversify its liability profile.

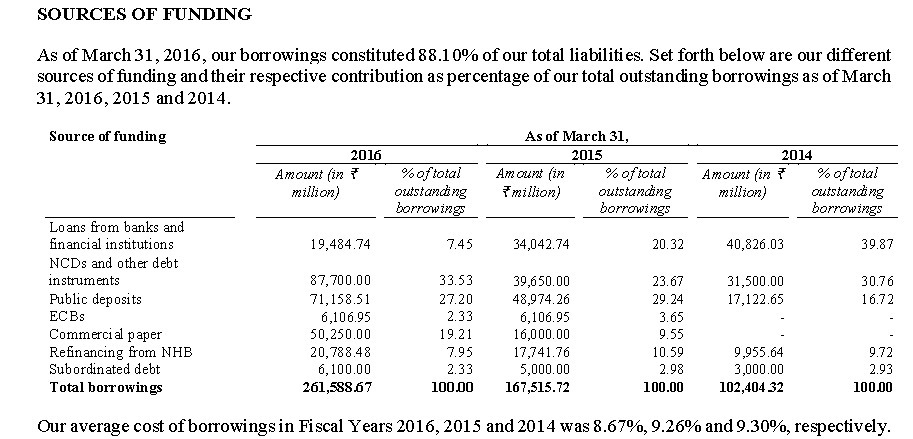

Over the past four years, the company significantly reduced share of bank borrowings from 34% in FY14 to 6% in FY16. The company is a deposit-accepting HFC, and retail deposits comprise ~30% of its total borrowings. With the reduction in share of bank borrowings and the corresponding increase in share of market borrowings, the company has managed to reduce its cost of funds significantly. As of and for the Fiscal Year ended March 31, 2016, total borrowings PNB HFL are ₹261B and average cost of borrowings was 8.67%. PNB HFL have access to diverse sources of liquidity, such as term loans from banks and financial institutions, non-convertible debentures (“NCDs”) and other debt instruments, public deposits, external commercial borrowings (“ECBs”), commercial paper, refinancing from the NHB and unsecured, subordinated debt, to facilitate flexibility in meeting funding requirements. As of March 31, 2016, PNB HFL’s operations are principally funded by borrowings from banks and financial institutions, domestic debt markets, public deposits and the NHB, which accounted for 9.78%, 55.07%, 27.20% and 7.95%, respectively, of their outstanding borrowings. In addition, due to short-term and long-term credit ratings, PNB HFL have access to certain fund raising opportunities in the capital markets. PNB HFL also offer a broad range of public deposit products of different tenures with various interest rate options.

NPA

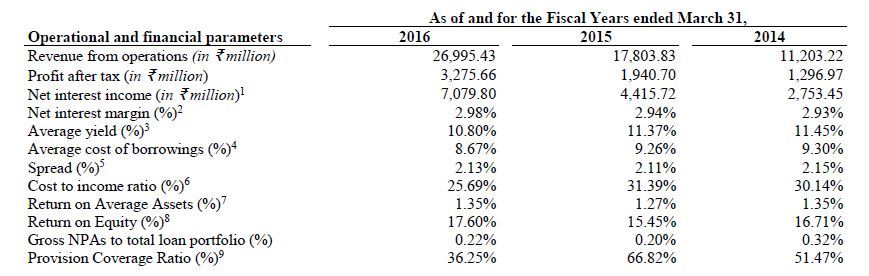

PNB HFL’s gross NPAs, as a percentage of total loan portfolio, are 0.20% as of March 31, 2015, which was the lowest among the leading HFCs in India, according to the IMaCS Report, and 0.22% as of March 31, 2016. As of March 31, 2016, 2015 and 2014, provision coverage ratio (i.e., the proportion of gross NPAs for which provisions had been made) was 36.25%, 66.82% and 51.47%, respectively. PCR decreased in Fiscal Year 2016 primarily because PNB HFL decreased provisions for NPAs to the minimum requirement under the NHB Directions.

Key Performance Metrics

We should Keep in Mind that after recent IPO, High leverage will be corrected so ROA,NIM will improve.

Key risks:

- Loan portfolio is largely unseasoned .The company enjoys a superior GNPA of 0.2%. However, this is also due to the fact that it has grown very fast in the past two years. As a result, the portfolio is not fully seasoned to reflect true asset quality. My understanding is It has been observed that housing finance sector itself generates very low NPA and tested Business Model in past many years, so this risk may not be alarming but please do your own due diligence

- Before doing IPO PNB HFL was ‘Highly leveraged’ (It was highly leveraged @ 15 times so there was fall in CRAR which triggered NHB inspection in 2015)so the ROA was remained compressed by 75 basis point . But after this 3000 cr Large IPO , the Leverage is corrected and Margin,ROA will improve significantly. As per MD Sanjay Gupta “Going forward, we will maintain the business at the usual leverage of 9-10, and at 12 times we will raise capital in future. This is the management philosophy.

Valuation : In current Price company is valued at ~2.5x FY17 H1BV (Post IPO current BVPS is 325), which is still cheaper than HDFC (around 4.5).

Future Focus Area

PNB Housing has launched a special scheme - ‘Unnati Home Loans’ targeted at customers from lower and middle income segment to enable them realise their dream of owning a home at affordable Equated Monthly Instalments (EMIs). Sanjaya Gupta, Managing Director, PNB Housing said, “Unnati is a focused Endeavour to reach out to employees of indigenous establishments and smaller SMEs. We are committed to help in bringing their dream of owning a home closer to them by providing such customized credit schemes. At PNB Housing, we extensively support the government’s vision of ‘Housing for All by 2022’ and ‘Unnati’ supports the low income groups. We are eager to be a partner in the development of aspiring Indians and firmly believe that similar initiatives will be an important contributor to nation building.”

The beneficiaries of ‘Unnati’ Loan Scheme will be individuals residing in peripheries of Tier I cities as well as those in living in Tier II and III cities. ‘Unnati’ home loans can be availed by the salaried and self-employed professionals for a loan amount of up to INR 25 lacs.

Discl: Invested and Biased.Data taken from DRHP.

. To make this thread more informative we need to research more on this company and will exchange our views .

. To make this thread more informative we need to research more on this company and will exchange our views .