I think a new MD& CEO has taken over - Mr. HarDayal Prasad who was the MD of SBI Cards ( when the IPO of SBI Cards was launched) has joined as the new MD & CEO in Early August 2020. this could be one trigger for change of sentiments.

1 Like

Q2-FY21- Key Highlights

Capital Raise Update

PNB Board has decided to infuse capital upto INR 600 crore in PNB Housing Finance Ltd, through Preferential Issue/Rights Issue subject to regulatory approvals.

Board approved capital raise of upto INR 1,800 crore through Preferential Issue/Rights Issue.

Financial performance (Q2 FY20-21 vs Q2 FY19-20)

Total Revenue of INR 2,022 crore vs INR 2,230 crore registered a decline of 9%. The Company had an assignment income on securitized pool of INR 110 crore in Q2 FY19-20. There is a net income on securitized pool of INR 105 crore in Q2 FY20-21 due to fall in buying Banks’ MCLR.

Operating Expenditure is at INR 107 crore vs INR 132 crore registering a decline of 19%. The decline is on account of the cost rationalization measures undertaken by the Company.

Pre provision Operating Profit is maintained at similar levels of INR 575 crore compared to INR 578 crore.

Profit after Tax is at INR 313 crore vs INR 367 crore registering a decline of 15% YoY.

The Net Interest Margin stood at 3.5% as compared to 3.2% YoY.

Gross Margin, net of acquisition cost, stood at 3.5% compared to 3.4% YoY.

Financial performance (H1 FY20-21 vs H1 FY19-20)

Total Revenue at INR 3,894 crore vs INR 4,463 crore registering a decline of 13%.

Operating Expenditure is at INR 211 crore vs INR 273 crore registering a decline of 23%. The decline is on account of the cost rationalization measures undertaken by the Company.

Pre provision Operating Profit decreased by 15% to INR 980 crore from INR 1,156 crore.

Profit after Tax is at INR 570 crore vs INR 651 crore registering a decline of 12% YoY.

The Spread on loans for H1 FY20-21 stood at 2.7% compared to 2.6% for H1 FY19-20. Excluding the net positive impact, the Spread for H1 FY20-21 is 2.5%.

Net Interest Margin stood at 3.1% compared to 3.2% YoY.

Gross Margin, net of acquisition cost, stood at 3.1% compared to 3.4% YoY.

The cumulative ECL provision as on 30th September 2020 is INR 2,004 crore resulting in the total provision to assets ratio at 3.0%. The total provision coverage ratio is at 115%.

Return on Asset is at 1.5% during H1 FY20-21 as compared to 1.6% during H1 FY19-20

Gearing as on 30th September 2020 is 7.8x compared to 8.9x as on 30th September 2019.

Return on Equity of 13.8% for H1 FY20-21 vis a vis 16.7% for H1 FY19-20.

Business Operations

The disbursements stood at INR 2,444 crore during Q2 FY20-21 compared to INR 694 crore during Q1 FY20-21 and INR 4,969 crore during Q2 FY19-20. The disbursements during the quarter witnessed gradual pick up, primarily in the retail segment, and has reached 86% of pre COVID-19 levels.

Asset under Management (AUM) is at INR 81,221 crore as on 30th September 2020 as compared to INR 83,495 crore as on 30th June 2020 and INR 89,471 crore as on 30th September 2019. Retail Loans contribute 82% and Corporate loans are 18% of the AUM.

Loan Assets stood at INR 66,951 crore as on 30th September 2020 from INR 68,009 crore as on 30th June 2020 and INR 74,353 crore as on 30th September 2019.

Distribution and Service Network

As on 30th September 2020 the Company has 96 branches with presence in 64 unique cities and 22 Hubs.

The Company also services the customers through 17 outreach locations.

Asset Quality

Gross Non-Performing Assets (NPA) at an AUM level is at 2.20% while it is 2.59% at Loan Assets as on 30th September 2020. Retail book GNPA stood at 1.23% and Corporate book GNPA stood at 7.60%. The GNPA in corporate book reduced during the quarter owing to the resolution in 4 accounts. Proforma GNPA not considering status quo as per the Honorable Supreme Court order would have been 3.04%.

Net NPA stood at 1.46% of the Loan Assets as on 30th September 2020 against 0.65% as on 30th September 2019.

Borrowings

Total borrowings are at INR 66,237 crore as on 30th September 2020 from INR 71,457 crore as on 30th September 2019 registering a decline of 7%.

The Deposit portfolio stood at INR 16,600 crore as on 30th September 2020 from INR 17,179 crore as on 30th September 2019 with expanding retail penetration.

Total assigned loans outstanding as on 30th September 2020 is at INR 14,270 crore.

Capital to Risk Asset Ratio (CRAR)

The Company’s CRAR based on IGAAP stood at 18.66% as on 30th September 2020, of which Tier I capital was 16.13% and Tier II capital was 2.53% compared to 15.67% with Tier I at 12.69% and Tier II at 2.98% as on 30th September 2019.

The risk-weighted assets as on 30th September 2020 stood at INR 50,297 crore.

Commenting on the performance Mr. Hardayal Prasad, Managing Director & CEO said:

“With the opening of the economy we are witnessing an increasing trend in retail disbursement and have reached 88% of the pre COVID-19 numbers. The measures undertaken by the Company around provisioning and retail business led to a robust balance sheet with total provision to total asset at 2.99%, CRAR at 18.66% and gearing at sub 8 times. The Company would continue to focus on disbursing lower risk weighted retail assets, enhance recovery and cost rationalisation to create value for its stakeholders”

Anyone who could help with meaning of “Assignment income on securitized pool of INR 110 crore”, please?

Capital raise of roughly 4000 crore lead by Carlyle group announced. However the silver lining is the following disclosure “As part of this transaction, Salisbury Investments Pvt. Ltd., the family investment vehicle of Aditya Puri, Senior Advisor for Carlyle in Asia and the former CEO & Managing Director of HDFC Bank, will also invest in the capital raise. Aditya Puri is expected to be nominated to the PNB Housing Finance Board as a Carlyle nominee Director in due course.”

Read the press release here.

Edit 1: Stock is on upper circuit and the news is likely to result in significant rerating. FYI - During November 2016 when this got listed the OFS was priced at 775 per share.

Edit 2: Capital infusion has resulted in an open offer at Rs. 403.22 per share. Note that post the issue of shares and conversion of warrants the new group will hold little less than 45% in the company. Offer document can be found here.

AJ

4 Likes

Carlyle group was already invested in PNB housing with 33% stake and was looking to exit the business sometime back. Below is the link for the same. They didnt get the valuation to exit and now they have increased their holdings and bought in Aditya Puri and market participants got excited.

Disc - Not invested.

This is 2018 article.

Since the HFC market is expected to revive in this decade Carlyle can stay back for few years & make many times over, of what they were expecting in 2018. It makes perfect sense to capitalize the Bull run of last year to build on the valuation just by using Aditya Puri & their own brand power before exiting at crazy valuation in few years down the line.

One thing is sure that PNBHF will be reformed big time due to the mgmnt change may prove beneficial in long term even if Carlyle exits after few years.

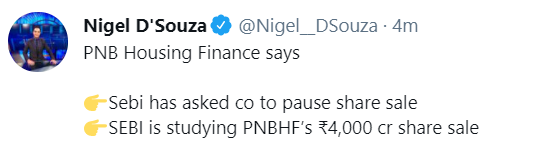

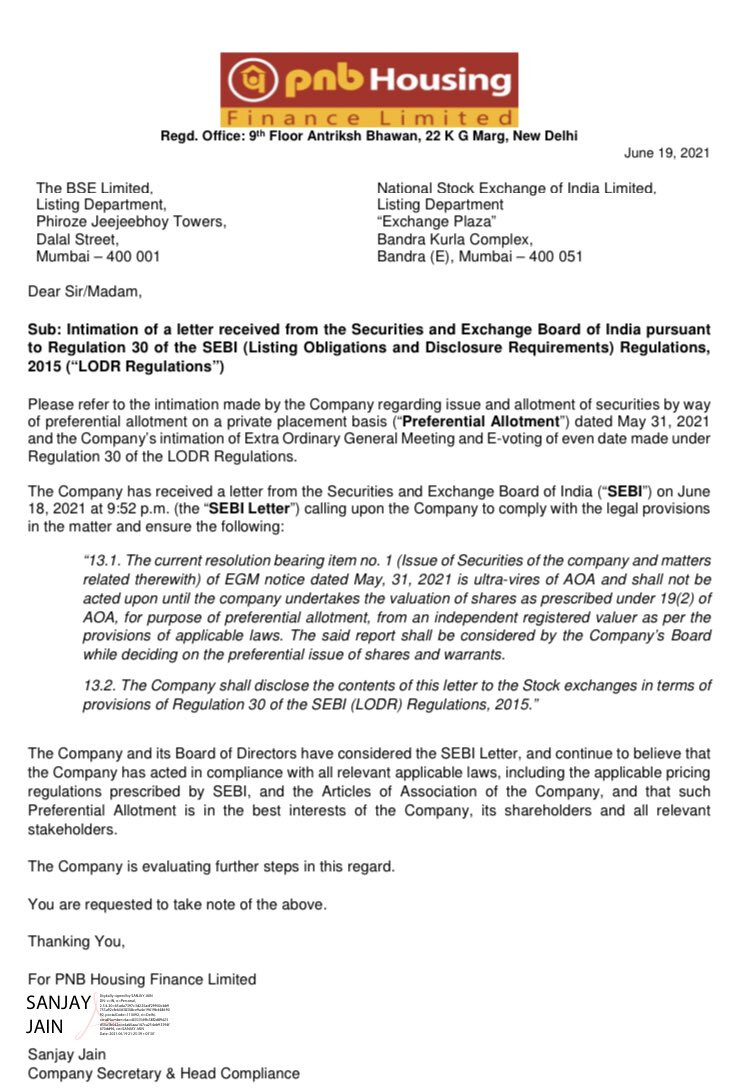

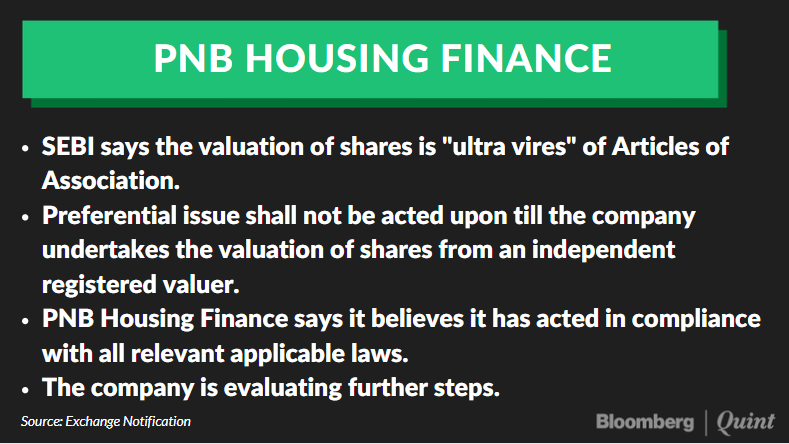

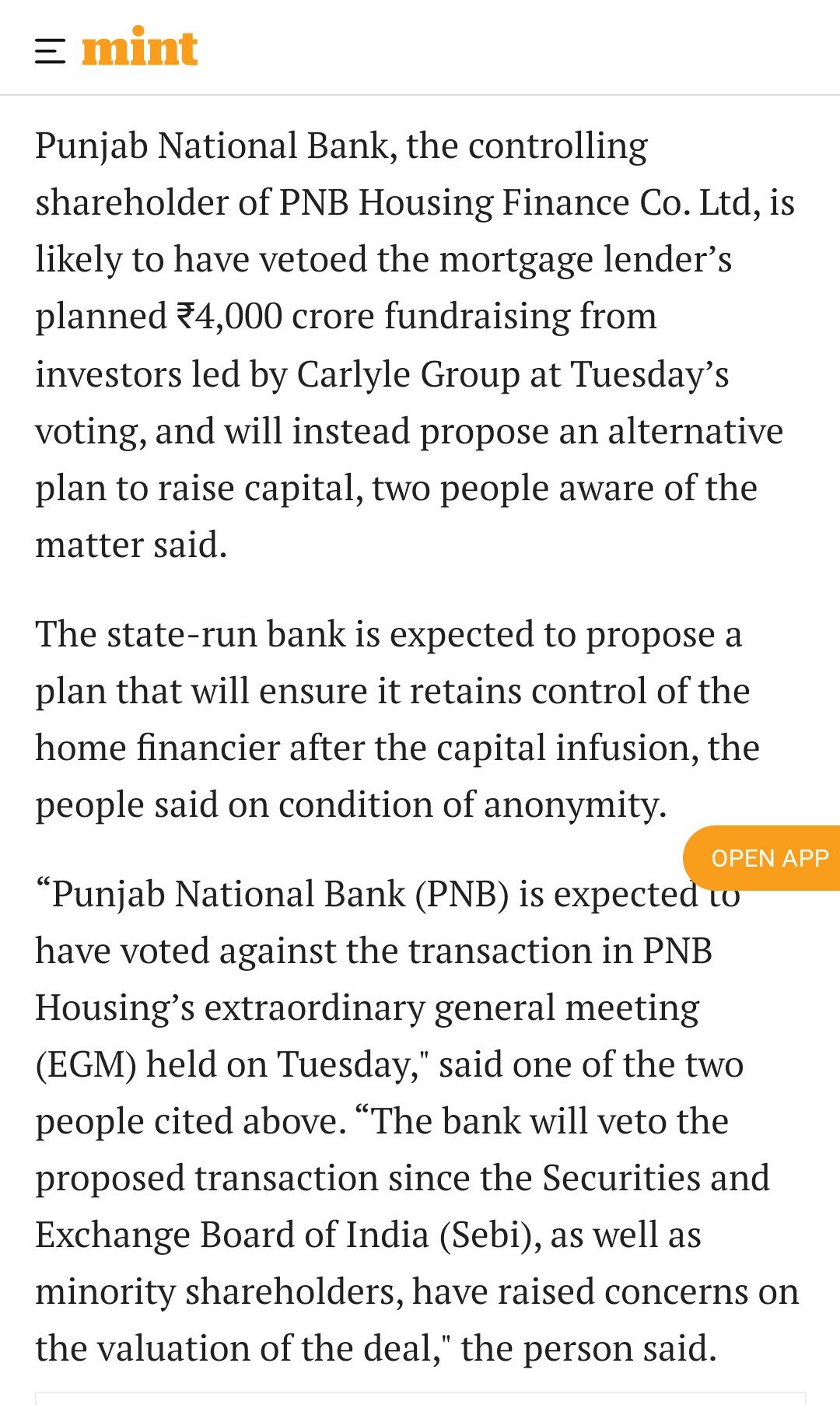

Deal with Carlyle terminated. Well done SEBI!

1 Like

How is that a good move? The HF needs growth capital for fresh loans and remain in competition. It might not be fair to which I agree but minority shareholders are not going to pay 1 times the book value to raise 4000 crores.

The verdict was not out, Carlyle called it off in the best interest. They could not even appoint a 3rd judge. It’s really bad. Such slow legal system.

1 Like

Q2Fy23 concall highlights:

- out of 52000cr retail book, 3000 cr affordable book. want to grow it. Affordable has good yield with low delinquency.

- Non affordable to affordable ratio in retail to be 75:25 in future.

- Have been able to arrest BT out on a sequential basis. Bt out q1 1350 n 1100 cr in q2.

- Increase in provisooning: 243 cr. has 4 components. 80 cr actual.

- credit cost of q2 on annualized basis: 1.54% it’s more compared to 0.94 in H1. for whole year it’s expected to be 1%.

- Mr. Girish Kousigi Your priority for this company: aggressive on growth. To be seen in next few quarters. Getting into affordable segment in big way. Focus on bringing down GNPAs. To ensure profitability.

- Answer to Omkara capital: Growth in book to comeback. because disbursement is already up. book will catch up. working to bring down gnpa. Plan for resolution on corporate book. There will be improvement going ahead qoq.

- cost of borrowing: 7.32 % now. once we start to grow and asset quality improves our cost of borrowing will come down due to rating upgrade. but in the immediate quarters it should increase by 0.5-0.6%.But we are going to focus more on affordable segment where there is less competetion with higher yeild. so won’t be a problem to maintain the spreads. there is not much difference in terms of asset quality in affordable vs non affordable.

- update on corporate book resolution: might take sime. working on it. 3-4 quarters we should see something. Corporate account resolution takes some time. Which is not the case in retail.

- Retail book normalised credit cost from next year.

- 2.6% spread is sustainable.2.2 % is threshold. it could be higher.

- provisioning on corporate book gnpa: gnpa 1734 cr. 50% pcr on corporate gnpa. we are adequately covered in terms of provision.

- Normalised credit cost on retail: 40-50 bps

- ROA&ROE in normal conditions: 2.2 spread, nim of 3.2, ROE should also improve going ahead.

- Going ahead we will be retail lending company only.

- capital raising update: filing for rights issue to be done before ending 2022 around 2500 cr.once rights issue is done rating upgrade will happen. then we’ll get better rates.rights issue to be completed within q1fy24.

- steps to take cost of fund down: it will come down. once our asset quality improves we’ll get better rates. so focus is on growth, asset quality and profitability. Cost of fund will automatically come down bcz of better rate once we reach there.

- growth guidance: our book should grow by 10% this year. next year about 18%.

With the book cleaning going on and growth coming back this looks a rerating candidate. out of 3600 cr gnpa 1700 cr is corporate gnpa. if the corporate gnpa gets under resolution plus some write off then the gnpa will come down to 1900 cr gnpa of retail. presently provision is 2160 cr. so assuming the resolution of corporate gnpa happens with some write off the GNPA and NNPA profile can look very different few quarters down the line from now. Mr Girish Kousigi from Can Fin homes joined the company. He has very good track record with can fin homes which has excellent npa numbers. If he can make PNBHF half of what canfin homes is rerating is on the cards. Even if we completely exclude the corporate gnpa from 10000 cr book value of the company we have 8300 cr which is still higher than the mcap of the company. So I believe it’s undervalued.

One observation: The stock was highly discussed about in this forum 1-2 years after IPO when it was very richly valued. 600 out of 692 posts of this thread were made before covid. The thread became inactive as price tanked in 2019 and finally went below book value post covid and then the npa numbers surfaced due to aggressive growth happened post IPO. Everyone stopped talking about the company when the stock price tanked. Now that stock seems undervalued and might be a rerating candidate nobody is talking about it.

Disclosure: Invested

9 Likes

2022-10-29T18:30:00Z→2022-10-30T18:30:00Z Aptly said…After going through the results and PPT, i joined this topic and was about to write… You mentioned more in detail than I thought…Thnx …

1 Like

I wrote a detailed thread on PNB Housing Finance

https://twitter.com/PalSouresh/status/1586649233431490561?s=19

Also a thread on how the PSU Housing Finance companies look as Technically and Fundamentally here

https://twitter.com/PalSouresh/status/1603430383386624000?s=19

Disclosure: invested in PNB Housing Finance. No buy and sell reccomandation.

3 Likes

PNB Housing Finance, an arm of state-owned Punjab National Bank (PNB), has received capital markets regulator Sebi’s go ahead to raise up to ~2,500 crore through rights issue of shares.

The housing finance firm, which had filed draft papers with Sebi in December 2022 regarding the rights issue, obtained its ‘observations’ on March 6, an update with the markets regulator showed on Monday. Going by the draft papers, PNB Housing will issue fully paid-up equity shares of the company by way of a rights issue to its existing shareholders for an amount not exceeding ~2,500 crore.

4 Likes

This would be capital for growth …

Q2FY24 Quick Notes:

Asset Quality: NPAs reduced Substantially during this quarter. In next 3,4 quarters, our NPAs will be one of the best in the HFC industry.

Corporate – We have reduced the loan book substantially. Now we will again restart in 2-3 quarters frow now. But we will focus only on Strategic Construction Finance which will also help in growth of the retail Loans. Yield will be higher than retail loan book and it will be similar to Affordable financing yield. But, corporate mix will be less than 10% of the overall book.

Increasing the focus on Salaried segment.

Login and sanctions are very good in Half year.

Increasing our share in the south as we are focusing more in this area (37.5%). South concentration helps in increasing Salaried loan customers. In salary segment, we are focusing more on affordable side, so that our yield will be higher.

Affordable Housing just started before 8 months- Growing very fast. Near term target 1000 crores to be achieved very soon.

Credit Cost Guidance this year is 0.6%. From next year it will be 0.4%

Opex to remain stable.

Credit Ratings also updated to Positive from Stable.

Sourcing Mix- not concentrated from any particular source like DSA channel .

Focus on higher yielding products like Affordable housing Finance.

Cost of Funds presently at 7.99% will not increase and remain stable.

RoA presently at 2.24%

Gearings: Looking for 6 to 6.5% in the next 2-3 years.

Affordable Housing incremental yield: 11.5%

Overall Incremental yield: 9.5%

Retail Loan Growth 22% guidance on disbursements during this year and 17-18% book growth for this year. Overall growth will also be similar because retail forms 97% of the book.

4 Likes

Q4FY24 Con-call Notes:

Loan Book and Disbursements

Q4’24 & FY24 performance

• Company continues its stated objective of growing its retail book and running down its corporate book.

• As of 31st March 2024, retail loans form 97% of loan book (balance 3% being corporate).

• Recent performance w.r.t. disbursement and loans is as below: -

| Disbursements(value & growth) | ||||

|---|---|---|---|---|

| Q4 '24 | QoQ (seq.) growth | FY 24 | YoY Growth | |

| Retail Disbursements (A) | 5541 Cr | 35% | 17483 Cr | 18.50% |

| Corpoarte Disbursements (B) | 33 Cr | 1% | 100 Cr | -54% |

| Total (A+B) | 5574 Cr | 35% | 17853 Cr | 17.5% |

| Loan Book (value & growth) | |||

|---|---|---|---|

| As on 31st March 2024 | QoQ (seq.) growth | YoY Growth | |

| Retail Loan Book (A) | 63306 Cr | 5% | 14.1% |

| Corpoarte Loan book (B) | 2052 Cr | -7% | -46% |

| Total (A+B) | 65358 Cr | 5% | 10.3% |

• Retail segment now consist of 3 verticals:

(a) Prime: Currently 97% of retail loan book; grew at 4% QoQ; Avg ticket size = 35Lakhs; targets 9-10% yield

(b) Affordable: Currently 3% of retail loan book; grew at 56% QoQ; contributed to 12% of total retail disbursements in Q4’24; Avg ticket size = 15Lakhs; targets 11-13% yield, 1/3rd customers new to credit.

(c) Emerging: Business to start from Q1’25, focus on high yielding (10-11%) part of Prime business in Tier 2/Tier 3 cities

Guidance on growth

• Around 17% growth projected on retail loan book for FY 25.

• One of the key factors driving growth will be the additional 100 branches opened between Dec ‘23-Mar ’24 (60 in affordable vertical, 22 in emerging & 18 in prime).

• As per management the FY24 business was practically from 200 branches, while FY 25 will be from 300 branches.

• Each of these verticals will have there own credit, sales & collection teams.

• As to why can’t growth be higher (esp. since currently leverage is quite low), management says it wants to maintain the asset quality and NIM levels.

• 40-45% of retail business in FY25 is likely to be from affordable & emerging verticals (which are relatively higher yield)

• Plan to start re-growing corporate lending business from H2’FY25 (the plan is to keep it in single digits as a % of overall loan book)

Profitability related

PAT

• Q4’24 PAT is 439 Cr vs Q3’24 PAT of 338 cores - QoQ sequential jump of 30%

• For full FY24 PAT is 1,508 Cr vs FY23 PAT of 1,046 Cr (these are ex. one off nos.) – jump of 44%.

ROA, ROE & NIM guidance

• FY24 ROA = 2.2% vs FY23 ROA = 1.6%

• ROA guidance for FY25 is 2.1% plus.

• FY24 ROE = 10.9%. Management expects ROE to go back to “reasonable” levels in next 3 years as more and more leverage is added (Note: while they didn’t say what is meant by reasonable level, if one were to guess it probably means 15% to higher teens kind of level)

• NIM guidance for FY25 = 3.5%

Yields and cost of borrowing

• Q4’24 yield = 10.08% vs Q3’24 yield = 10.19%. This drop in yield is due to depletion in Prime loan book, caused by bank transfers etc. due to heavy competition.

• Management expects to improve the yield in FY25 (compared to Q4’24) due to increased focus on Affordable & Emerging verticals.

• The yield from Affordable segments is expected to go up 100 bps from 11.5% to 12.5% in FY25.

• Average Cost of borrowing for FY24 was 8.01%. The management expects it to come down somewhat as they now have been upgraded to AA+ by India Ratings, ICRA & CARE.

Impact of additional branches on Opex

• As per mgmt., there will be “some impact” of opening 100 additional branches, but the higher yields justify it. Opex to ATA was 0.93% in FY24, which might move to 0.95% to 1% in FY25.

• An average branch in the Affordable vertical breaks even in around 8 months.

Asset quality related

• The GNPA trend over the last 12 months has been as follows: -

| GNPA% | |||

|---|---|---|---|

| 31-Mar-24 | 31-Dec-23 | 31-Mar-23 | |

| Retail | 1.45% | 1.67% | 2.57% |

| Corpoarte | 3.31% | 3.35% | 22.25% |

| Overall | 1.50% | 1.73% | 3.8% |

• A corporate account with a current outstanding loan value of 126 cores moved into stage 2 in Q4’24. The management currently believes that it will remain there or come back to stage 1.

• Management was able to write back Rs.99 crores from the write-off pool in FY 24 (out of which 49 crores came in Q4’24 – this is why credit cost was just 0.04% in this quarter).

• The current write-off pool is 1700 crores (retail) and 500 crores (corporate). As an approximate guidance, management expects 50 crores of write back every quarter for FY25.

• Credit cost guidance for FY 25 is 0.30%. This doesn’t include any write backs that might happen.

(Disclosure: invested with a small tracking position)

4 Likes