Q2 FY20

Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/44ae370f-1cf4-4756-be87-80a7b4cbf354.pdf

Q2 FY20

Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/44ae370f-1cf4-4756-be87-80a7b4cbf354.pdf

One basic question.

What’s the difference between spread on loans and net interest margin?

Check last slide - Formulas- in the Investor Presentation

Motilal Oswal view - Given the challenging macroeconomic environment,coupled with high leverage, PNBHF has taken a cautious stance on disbursements. Disbursements are likely to remain muted until equity capital is raised. We thus expect AUM to grow at 10-12% in FY20 and beyond. PNBHF is focused on resolution of the five accounts in the watch list - this remains a key monitorable. We cut our FY20/21 EPS estimates by 3-5% to factor in lower growth and higher credit costs.Buy with a TP of INR630 (1.0xSep’21E BVPS).

The scrip is being hammered down. The underlying story does not seem to have changed overall. Is there more infos known to members that is not clearly visible to all ? Appreciate if members could provide their views on this.

Impact of Coronavirus lockdown on real estate sector

True. Media and most of us give too much important to these so-called “experts” who sound all logical and confident but are mostly talking their books. We should not be surprised if they come now and say they sold off their Bajaj Finance in January (in-fact shorted it) and moved to pharma sector ![]()

Any sign of trouble they keep advising/criticising/praying to the Government for some relief. They all talk of spending time in the market and not timing the market but are all short-term/medium-term oriented and can be best termed as momentum investors. We should listen to them only for their thought process but not get excited by any sector/stocks discussed. All of them have to sound confident and optimistic in public. There are very few people like Howard Marks who is candid enough to say that he does not know what will happen. All those who proclaim that they are 100% in equity always are actually failing the first rule of personal finance - asset allocation.

Also in the context of this thread, we have to be extra careful when there is a PE fund invested in a company and looking to exit. They generally try to force the company to take extra risks for short term profits which will show its impact in the future. With PNBHF it could be earlier loans to developers to show good growth numbers which will start showing its impact. SBI Cards is another example where the number of cards issues, lending etc drastically went up few years before the planned IPO. They generally dress up the company and try to extract maximum returns. For a majority promoter driven company looking to IPO, we can be somewhat assured that the promoter will have some skin in the game post the IPO and have his interests aligned with the minority shareholders. Of course there are fraud promoters mostly in SME IPOs who do the same dressing up and we need to keep away from them.

He is handling Bm PMS …if he discloses every thing on news channel than why any one will give him funds to manege and pms fees.also he has to follow all sebi rules

We always respect PMS secracy of their holding. However, when he himself disclose his pms holding and advocate more about company earnings and future growth to balloon the stock price to dump it thereafter creates unfair condition. (sometimes even company promoter doesn’t know such earnings forcast!!!)

I am not advocating him but stock was nearly in pms holding for more than year. They exited after private equity holder were not able to deal for buy out.

PNB’s NCDs and Tier 2 bonds downgraded due to weakening asset quality of wholesale loan portfolio.

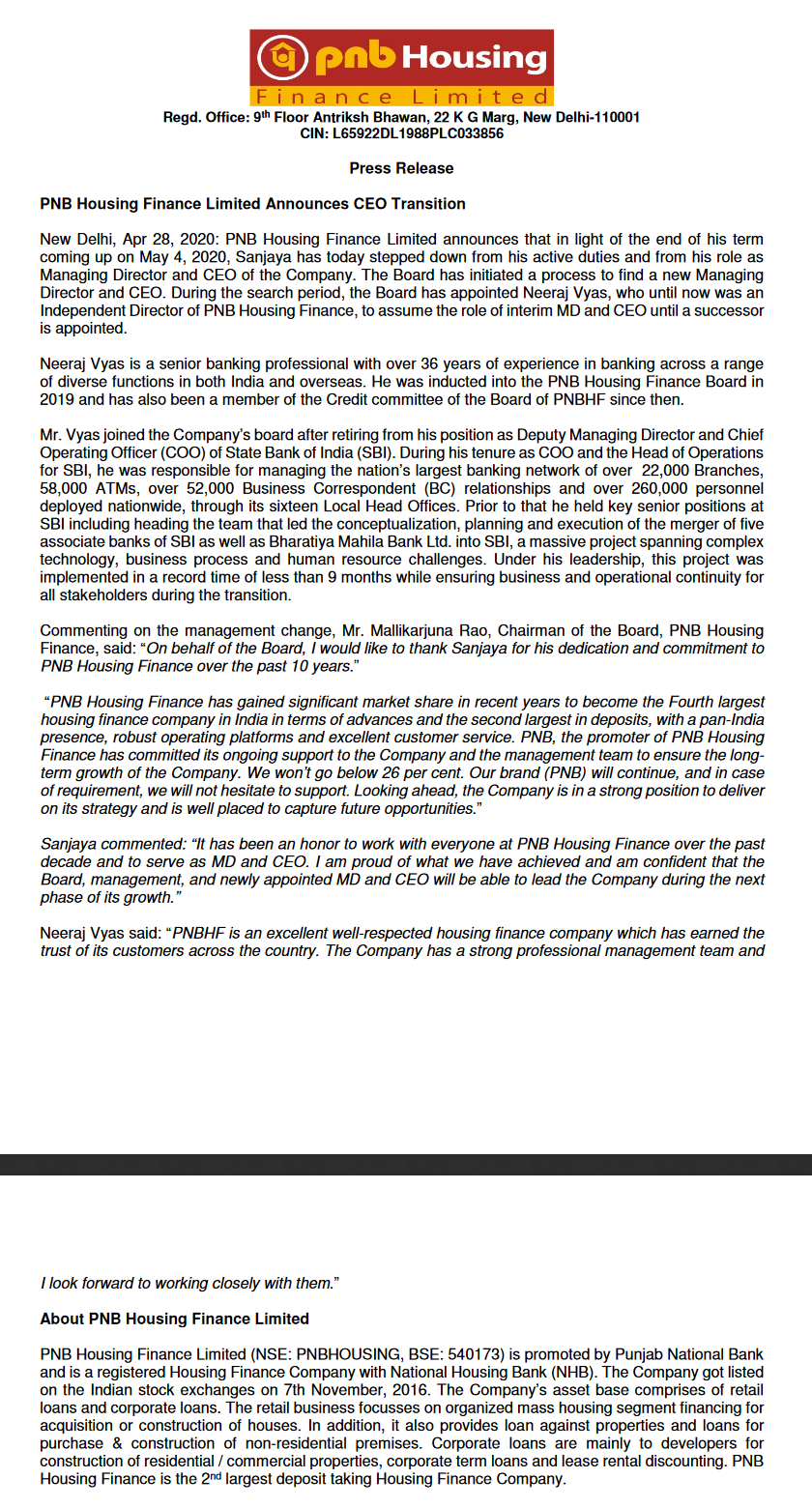

PNB Housing Finance has appointed a new interim CEO after Sanjaya Gupta’s stepped down a week before his term ends as MD and CEO,don’t know what happens to their capital raising plans now,stock is well below book value and any dilution will be extremely value destructive but they may be compelled to dilute for survival.

Their release seems very lackadaisical about finding a new CEO,when they knew Mr. Gupta’s term is ending why did they not initiate this process a year ago?,especially given the challenges the company is facing given the turbulence in the real estate sector and their own issues regarding stake sale etc in the past.

I am feeling afraid this will become bankrupt. Too much debt.

They make ~2k crore revenue every qtr and pay 1.5k cr in interest and another 300 cr in other expenses.

They have a ~80k crore loan book. 5% NPA => 4k crore write-off… They have no equity. Equity is just some 8k crore. So company might collapse.

Request some knowledgeable folks to post and help. I am considering exiting with whatever I have left in this stock…

Hi Alexander,

Can you share the source of your data. B’coz as per their financial presentation of Jan, 2020

Their NPA is 1.75% in Jan,2020 and moreover their spread is around 3% which can easily take care of their opex.

PNB is planning to raise 1700 Crore funds and Carlyle Group is participating in it- I think that’s a positive sign.

Looking forward to hear the views of other Investors.

This is an old news of 3rd March 2020 when sanjaya Gupta was CEO and it was pretty Covid. Things have changed drastically since then and sous the share price and situation in HFC in general and in PNBHF too.

Hi there,

Can anyone help me understand who has pledged this share because when I look at their financials, they show that no shares are pledged and there is also no change in the promoter holding.

What am I missing over here?

Change of business plan ;

2b40b64a-01bb-4064-953e-57891fa2e947.pdf (329.3 KB)

They want to sell most of their developer financing business and focus on retail low ticket housing loans. In q4 concall also their new interim ceo was stating the same thing.

Any idea, why Sanjaya Gupta stepped down after 8 years or he was asked to. After that change of business plan as well. Anyways I always thought he was overconfident about developer loans and that was quite visible in his tone.

Good results in current environment

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b4e376ce-3106-46f7-b195-aaf02ebb8b24.pdf

Hello All, would anyone have inputs on why the stock has shot up in recent weeks?