I am fully invested, which also translates to I don’t have any funds to take advantage of the low valuations.

Till now, I have avoided leveraging. ICICIdirect has a facility (so have others, I mention this as I am familiar with this site) of buying shares by pledging shares to get funds available to use as margin. The first mistake I have made is of pledging too many shares. The margin required is 1/3rd or so of the amount required for buying the shares. So, for buing shares of 10 lakh, I would have required approx. ₹3.33 lakh. I have pledged the shares of the entire amount, so in this example, now I have the whole 10 lakh to continue with the example, instead of 3.33 lakh. Thus, I can now buy about 30 lakh worth of shares.

Now, I not only have the shares pledged to secure the margin money, but the shares I bought from that are also pledged.

My condition is like Abhimanyu in this case. I have entered the chakravyuh, but don’t know what happens now. My head is full of questions. ICICIdirect has an FAQ on it, but like most FAQs, it doesn’t give the most needed answers. For example, it doesn’t even tell what the rate of interest is.

I will be so grateful for the answers here. If not possible to give a lengthy reply, kindly give any links available. Any book also will do. Nobody would have bought a book faster than I would do. My questions are very basic.

(i) For how long can the status quo continue, without my having to square the trade?

(ii) Do I pay only the interest every day, or can prepay some of the principal too from time to time?

(iii) Can I take delivery of part of the shares? For example, out of the 100 L&T I have bought, can I take the delivery of 30 in a fortnight, and like that?

(iv) What is the proceedure of getting the pledge on the shares I have pledged to secure the margin amount?

(v) Is it sensible to buy shares by leveraging during a bear market?

I am copying the FAQ from the ICICIdirect. Once complete, I will share a pdf. I have also found another FAQ. ICICIdirect.com

Thanks in advance.

Answers are not in a particular order, pls bear with me sir.

This is called as LRS facility, i personally used it too in Zerodha , where you get 50% on pledging of your particular script.

I can tell in context with Zerodha which is known as Zerodha capital.

We need to maintain 50% of LTV ratio beyond which they have a right to sell our share. You can google what that means. in simple terms your pledge share should not get too much negative post pledging.

Another thing is they charge 11% ROI annually. So suppose i have 22L amount taken from 44L of stocks value, i am paying around - 20150 approx per month.

There is time period until which you need to repay back the loan amount, for me it is 2028, starting this year.

You can pay both interest as well as principal to reduce your interest.

They dont suggest to take use this amount for capital buying. Yet people are smart if you know what i am saying ;)

If you pay more and clear some amount, there is a section in zerodha that will tell you how much amount of shares you can unpledge, considering LTV ratio doesnot go bad.

for point 5th , it is a choice one has to make, as no one know which is the bottom of share, which is stock you need to enter that will keep on following the trend or bounce back from bearish trend.

I hope this will help you to correlate and find sections in ICICIdirect to correlate.

Thank you. So grateful. I have been given upto the March 2027. ICICIdirect is saying it will charge me ₹26.55% per lakh. There are also other extra charges, which I presume may be one time.

This is pure looting. And this is the reason i didnt opened my demat account in ICICIdirect, first you have to buy plan and all.

Mine tenure is Oct 2028, to be precise.

Pls go through this.

Is this different from Margin Trading Facility (MTF)? I am asking because for Zerodha MTF the interest rate is Rs 40 per lakh per day, which comes out to be 14.4% annually.

It is LRS not MTF. Loan against shares. Not Margin giving facility.

FAQ on shares pledged as margin.pdf (859.5 KB)

Icici charges lowest interest 9.8% per annum, 26/day/lk on daily basis, debit happens everyday.

Plz note that MTF and LRS are two different facilities. Zerodha pledges shares in both cases and as mentioned in earlier posts interest rates comes to 14.4 and 11% per year respectively.

For MTF the way it works is you pay only for 1/3rd of the total cost of shares bought. And interest is charged daily and it gets deducted from the balance in your zerodha funds. I guess it also adjusts any shortfalls on daily basis if stock price falls (though I am not completely sure of this)

LRS is like any other loan where stocks are kept as collateral (just like you can take loan against property). Loan given is 45 to 50% of your stock value. Loan duration is 3 yrs and interest is charged monthly. Loan to value (LTV) is calculated on daily basis. In case of shortfall, one can pay back that amount or pledge additional stocks.

Now coming to ICICI, they also provide LRS at around 10-11 percent. So not sure about this 26% interest. Not sure if MTF is at 26%.

Sir, I think we have mixed up 3 different concepts here. Let me just capture in brief what they are:

- Shares As Margin (SAM): You have shares that you bought in cash lying in your demat account. You pledge them to avail a SAM limit. With this limit, you can either trade in F&O, or put up initial contribution for MTF. You cannot buy shares in cash for delivery with this SAM.

- Margin Trading Facility (MTF): Here, you put up 25%-50% of the share value upfront, either as Cash or funded through SAM availed in previous step. The balance amount is lent to you by ICICI. They charge interest on the amount they have lent you (typically 9.75%-17%). IN case you used SAM to fund the initial margin, you pay interest on both SAM + amount lent by ICICI.

- Loan Against Shares (LAS): You have shares that you bought in cash lying in your demat account. You pledge them to avail a LAS loan. Typically you get 50% of the equity value as direct cash disbursement in your bank a/c (just like any personal loan, home loan etc). Rates of interest are lower here. When availed from a bank, the loan is like an Overdraft (OD) i.e. you dont need to pay the principal back, only the monthly interest amount. You are charged interest only on the amount drawn from OD, and you can deposit money and withdraw multiple times as per your will. The LAS limit gets renewed each year, so your principal repayment effectively rolls over.

In terms of riskiness, MTF is riskier than LAS. This is because a) your leverage is higher (typical MTF you can get 2.5-3.5 x leverage); b) your MTF is getting marked-to-market daily, and you dont have any buffer.

Eg. I put up 10k upfront, take 20K as MTF and buy a stock worth 30K. If the stock now goes down by 10%, I need to put up the shortfall back in my MTF (3K or 10% of 30K).

In LAS, a) your leverage is lower - typically capped at 0.5x for equity collateral, and b) you can build in a buffer as well

Eg. I have shares worth 20K in my demat account. I pledge all of them, get a cash disbursement of 10K against the same. Now either I use entire 10K to buy stock (max. leverage of 0.5x), or use only part of it - lets say 8K to buy the stock. Here there is no impact on my loan amount due to fluctuation in value of the share i bought using LAS.

The fluctuation in loan amount is only due to MTM of shares pledged as collateral for LAS. Let’s say value of pledged 20K shares goes down by 10%. Hence, my loan limit now reduces to only 50% of 18K, i.e. 9K. So, if i withdrew the entire 10K earlier, i need to top up by 1K. But, if I built a buffer and used only 8K earlier, I still have a buffer of 1K left (9K new LAS limit minus 8K LAS availed).

To compensate adequately for this risk, ICICI charges much higher interest on MTF than on LAS.

Where does your Chakravyuh come in?

You seem to have taken SAM (the first one). You bought shares for cash, pledged all of them to get a SAM limit.

Now what you do with SAM actually determines whether you are Abhimanyu or Arjun/Krishna (who knew how to break out)

You can use SAM to get limits for Intraday trading or F&O trading (leverage on top of leverage). You can use SAM to fund your cash contribution for MTF (leverage on top of leverage).

Both of these strategies are extremely high risk! Even in a bear market. Nobody knows the bottom. Stocks can continue to trend downward for no reason, despite them being hugely undervalued even after a prolonged bear market.

Sensible thing is to avoid leverage, or use only a controlled version of it through LAS. There is good leverage (the low cost, controlled LAS kind) and bad leverage (high cost, daily MTM, uncontrolled MTF kind). Be very mindful of what risk you are building in whether it is bull market or a bear market.

That said, there are examples of successful investors who have used controlled leverage to build enormous wealth (google “Davis Double Play with leverage”).

You might have entered the Chakravyuh, but you need not be Abhimanyu. You can be a Krishna or an Arjun too based on what you chose to do!

They are charging me 26.55 per lakh, per day.

So well explained. Its members like you who enable me to feel I am not fighting a lone battle in the share market. Really grateful. ![]()

![]()

Hi Sir,

I have been using ICICI for quite a while. This seems to be the SAM + MTF position you have taken.

Let me try to answer them in line:

- If you hold them just like your normal demat shares, the interest component will bleed money. MTF is mainly for Inraday/ Highly short term trades. Avoid this at all costs.

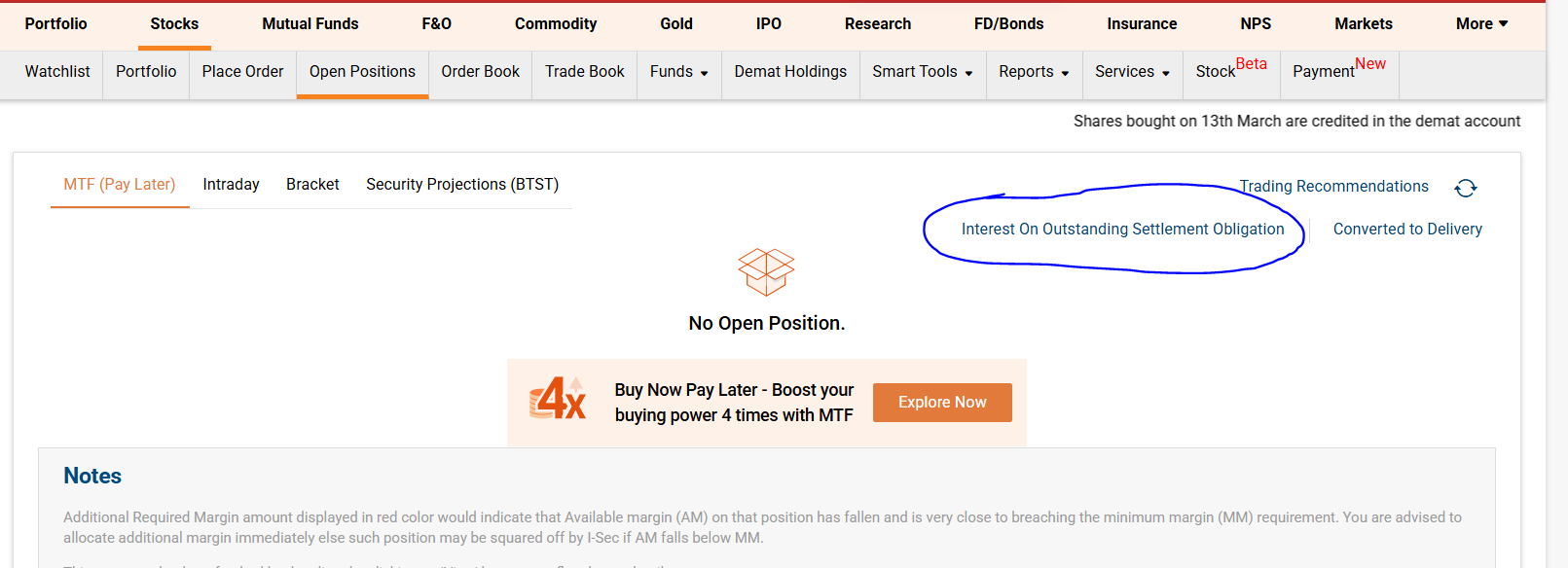

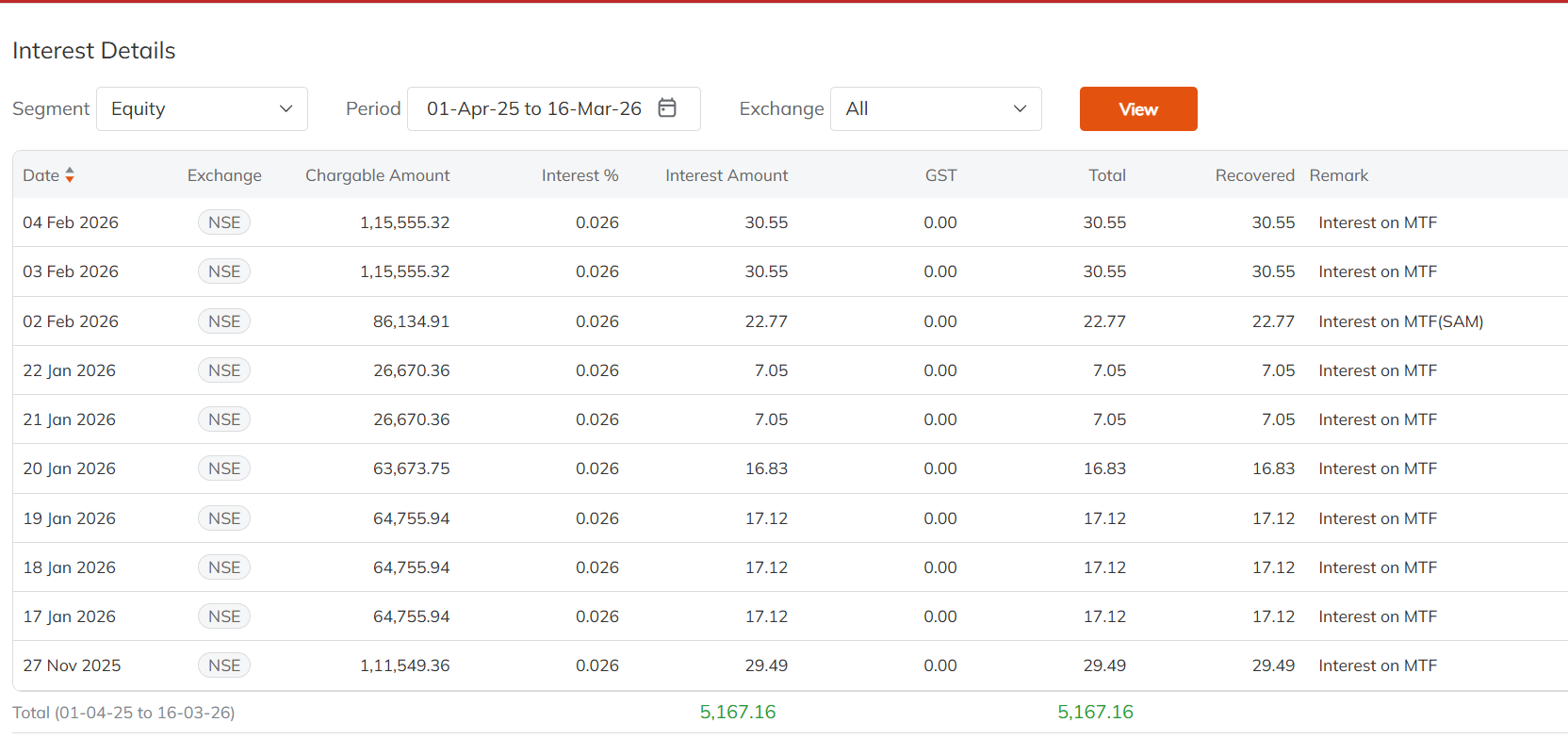

- Yes, you pay interest daily. You can check interest statement here:

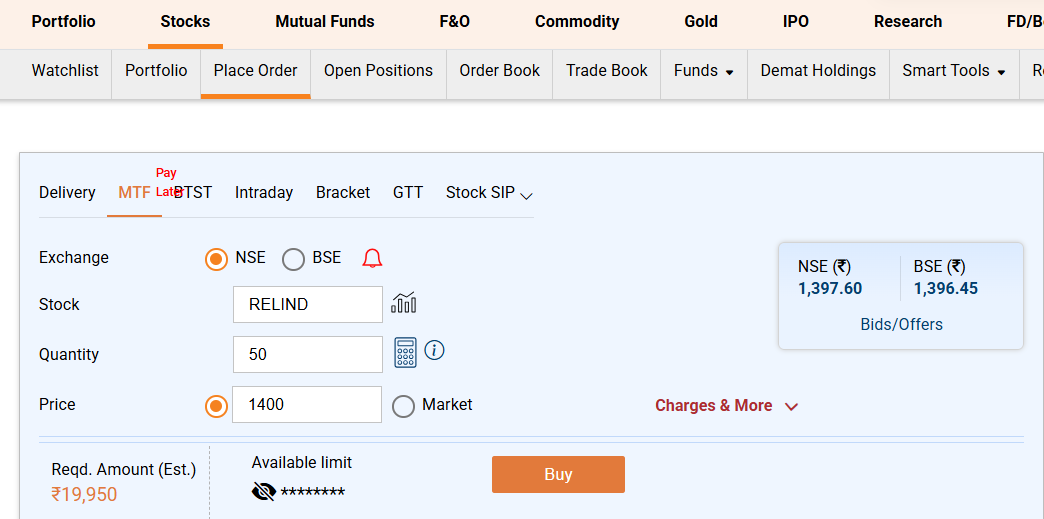

- Yes, you can take delivery of the MTF shares whenever you wish. Simply go to MTF section and select: Convert to delivery. You will have to keep adequate balance to pay full cash for the converted shares.

Ex: You bought Reliance 100qty at 1400rs via MTF. If you wish to convert 50% of it, you will need Rs.70,000 cash.

- To use the pledged margin (SAM), go to place order and select MTF.

See the benefit of MTF, you just need 19,950rs margin instead of 70,000.

- Use MTF only for super short term (2 weeks max) as your interest is charged all 7 days

Regarding your charges, there are multiple plans to choose from:

I have taken the 4999 plan. The charges on your first plan are fully reversed in terms of brokerage (They won’t debit brokerage till 4,999rs). So do check with your RM if you can avail it.

Feel free to reach out to me for further queries.

Happy investing!

Really so wonderful. You have really answered all my questions.

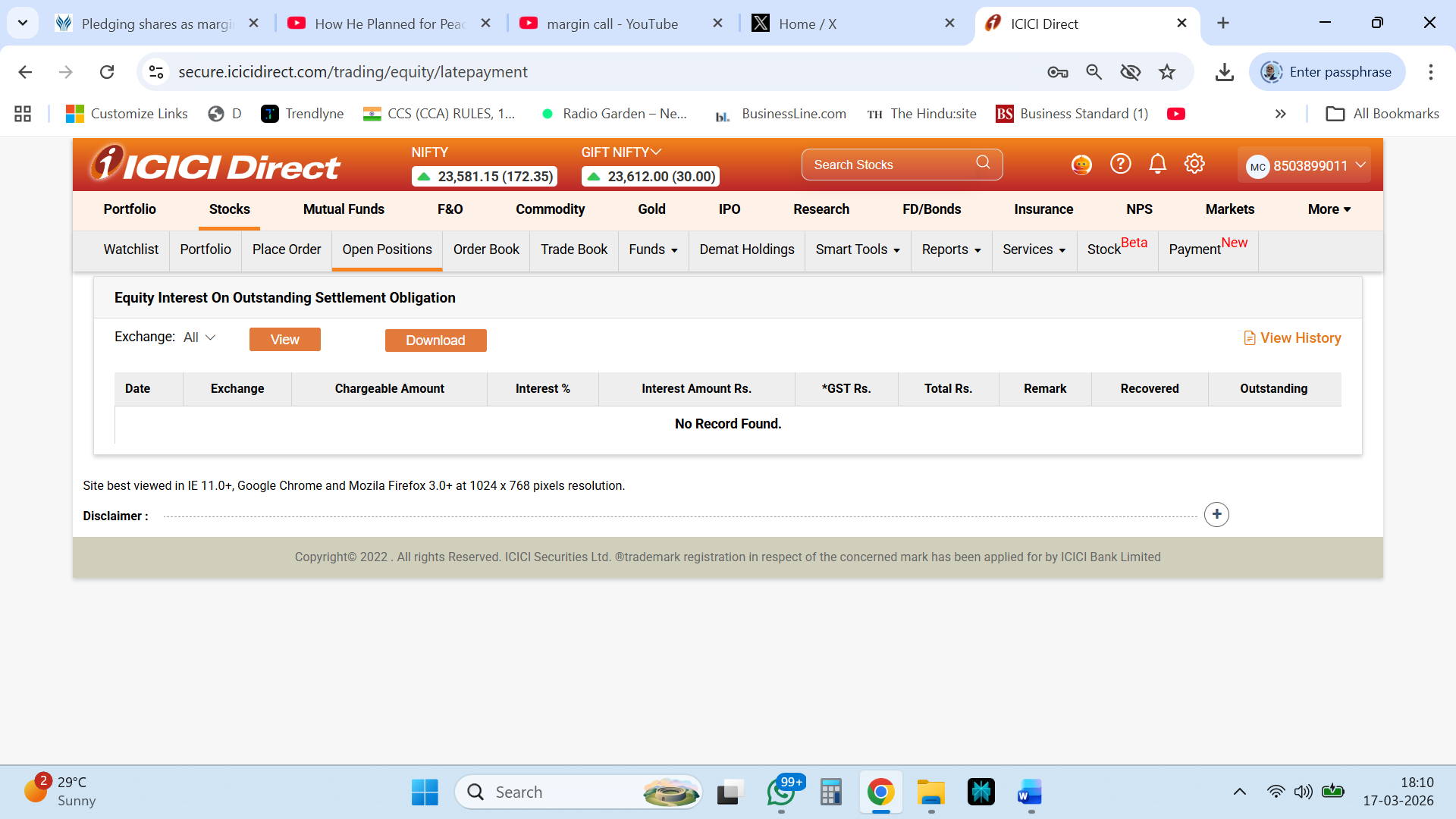

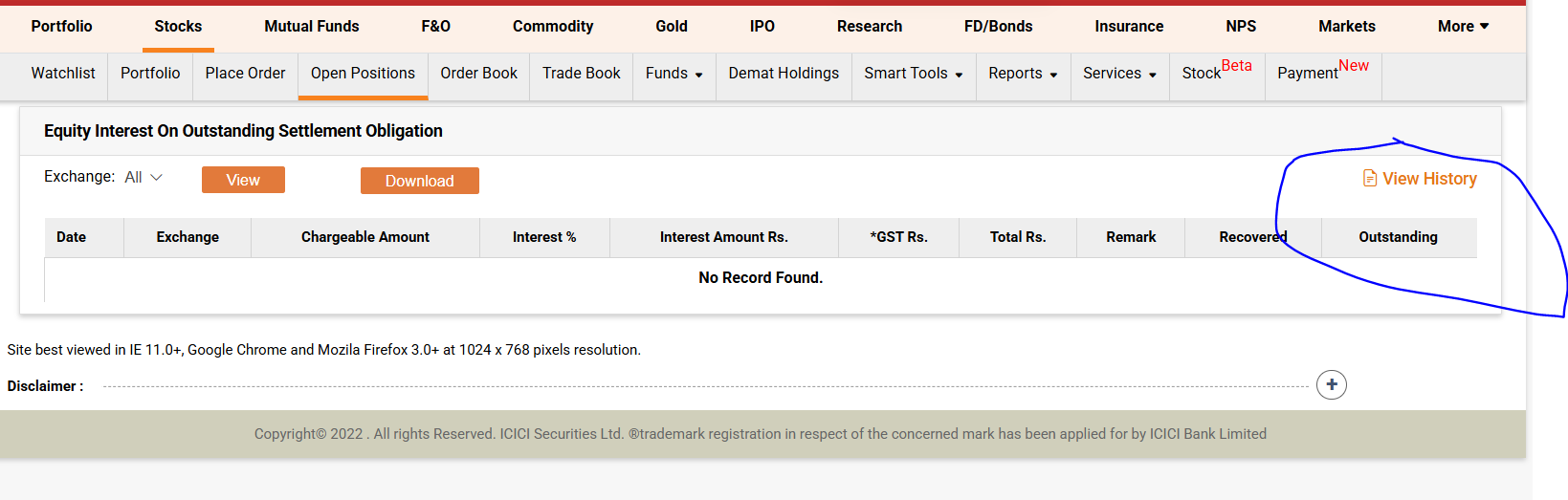

I am however, unable to view the interest they are charging. The screen says, “No record found”.

I have the PRIME 9999 plan.

PS: Everything is hunky-dory till now as the account is showing profit. Keeping my fingers crossed.

Select View history, it will take you to another tab “iReports”.

Select the time period and you should be able to see.

Thanks again. I have really no words to express the relief.

It seems like there is no interest yet. Let me check again tomorrow.

Once I have the opportunity, I can ask you: what has been your experience with leverage (stocks as margin)?

You buy shares in MTF or delivery, how the stock would know if you are holding asset in delivery or MTF? It all depends what price you have paid for your position, only issue with MTF is you need to control your greed and discipline your exposure. I have kept a rule of 20% levered portfolio at any time with extention to 40% in special situations. Its boon when you are in bear markets and turn to bull markets. Its a curse when you buy stocks and market corrects very sharply as cutting losses is depressive as your pledged holdings are also sold. I am using it for last 8 years. MTF sponsored my two trips abroad in 2018 and 2025. 2020 till Sept 2025 it was good experience, Oct till now i am paying back due to sharp drawdown, booked losses in some positions which are large. So use it very carefully. Buy small and treat as holding for 6-7 months, or large with ultra short term with strict stoploss, maximum 4-5 days.

Very good advice. Thanks. I am thinking of holding for a few months to a year.

This quote by @aditya.lathe deserves highlight for others who arrive here out of curiosity or contemplation to do something similar.

![]()

![]() Debt destroys staying power.

Debt destroys staying power. ![]()

![]()

Its both sides, bear markets offer assets very cheap so leverage can play a large alpha as well if timing is right.