At current portfolio level, each month I can add another 5-6% money.

I am a little confused with regards to which stock I should increase allocation to.

I do not wish to hold more than 8 stocks in my portfolio, so if I add another stock, one of these should go out. This rule helps me stay focused and dissuades me from buying anything and everything that looks good.

A little about my portfolio objectives and constraints:

Time horizon ~5 years

I can tolerate up to 50% reduction in value, anything more than that will indeed make me nervous.

Dear PP1, thank you for taking time to advice. However, I beg to differ from you, as explained below. I will be very happy if you could give me some constructive criticism.

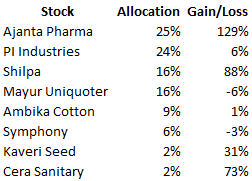

Mayur 32% CAGR revenue growth in last 6 years (until 2014) - current PE 27

Symphony 39% growth CAGR revenue growth in last 6 years (until 2014) current PE 48

Assuming fundamentals have not changed much but both have a mediocre medium term prospect, and margins have roughly normalized, I don’t see a strong reason to exit Mayur and buy Symphony by incurring 2% transaction costs.

Yes, deploying fresh money in Symphony and accumulating it is indeed something I am looking to do at lower levels. I may even start accumulating Mayur if it shrinks as a part of total portfolio.

The stock selection are good. I personally holding Ajanta,Cera and PI too. I had mayur but due to high dilution of equity, i don’t feel confident for 25-30% CAGR for next 5 years. So I exit

As per the current valuation of Ajanta, at 42 pe, u should reduce the exposer and add more Cera or ambika at current level.

PI is good pick but 24% allocation is high risk. U can add Dhanuka at current level if u want to stay with same space

You can also track or add some fmcg players which are consistent performer like Relaxo, Wim, Eicher, Amaraja to make portfolio gain stable and consistent.

I don’t understand the business model of Kaveri so no comments.

I am really impressed with this portfolio. It should give very good returns over the medium to long term. I think you could consider reducing mayur. they may not be able to repeat the past cagr considering the large base now. I dont understand why everyone is after textile stocks these days? (ambika, kpr, welspun etc.). what is the moat here and what has changed in the recent past?. isnt it a pure commodity business?. no offence meant :

Mayur has definitely lost strength recently (technically as well as fundamentally), but somehow I am not so negative on it yet. Can say Gut feeling. Also, as a thumb rule, I don’t sell stocks until they drop at least 20-25% from their lifetime highs, so sticking around.

Ajanta is moderately expensive, but the the traction in growth continues and I am not at all convinced to sell. In fact if it was below 35 PE and NOT 25% of my portfolio, I would buy more.

Cera: I don’t like companies with reduction in margins. Some kind of paranoia.

Ambika looks good as a value buy, but I think I will refrain from increasing exposure until growth starts showing up.

I allocated a large % to PI recently, because I was thinking 6 months in advance when I will have 30% additional cash from savings. And I was worried that PI would run too fast too soon…I did not want to lose the opportunity to buy a large chunk of PI. I am quite impressed with its business and financials.

Eicher, Amara Raja - Terrific companies but too expensive for me to digest. May be a Symphony like correction happens and then I can try to buy into them. Relaxo - well not to comfortable with this.

Its a nice growth stock portfolio constructed which you need to hold for 5 year to get full benefit. I have exited many stocks due to high valuations namely Symphony, Ajanta, Mayur. But slowly adding Symphony back.

But i am slowly looking at Engineering companies; specialized PSU like Engineer India. If Infra & Pvt capex picks up then such companies should benefit a lot.

Mayur is not the same quality business as Symphony

Symphony - No.1 brand in coolers, consumer facing (B2C), under-penetrated market, shift from unorganized to organized, huge opportunity in industrial cooling, strong in product innovation/design

Mayur - Not a brand, B2B, commodity products with slight differentiation, facing difficulties in footwear (which is 50% of sales), strong in product innovation/design

Disc. I am invested in both - but more in Symphony than Mayur. I sometimes consider exiting Mayur.

PE ratios not only depend on growth rates, but also on the longevity of growth… The longevity of growth for Symphony is far more visible than for Mayur.

About the other stocks - Have very little knowledge of Pharma - so no comments there…

Cera - not a great stock for the next 3-5 years due to slowdown in real estate (which in my opinion is here to stay for a while)

Kaveri - I have doubts on management, after they came up with the story of investing 1500 crores into exotic vegetables business… such a large investment into such a wierd business - most likely cock-and-bull story…Also, falling cotton prices is a headwind for the business…

Ambika cotton - Nowadays, textile stocks are in fashion… But this has nothing to do with the long-term fundamentals of textile business… Some short-term/medium-term stuff like low cotton prices, govt incentives,etc are playing out - but these could turn the other way around without warning… Lot of herd mentality at play here among investors…

First disclosures. I used to own Mayur till some 10 days back for almost 3 years. Completely exited. I own Symphony now.

I feel Symphony is a much better business. Mayur is almost like a commodity business. Domestic OEMs and footwear manufactures will squeeze margins and you can see it is difficult even to keep maintaining 19-20% OPM even if raw material cost comes down.

A bet on Mayur for the next 4-5 years would be that per meter realization is north of Rs 300, growing 5-10% every year with revenue mix of say: 25% - B2C businesses, 30% - Export and Export OEMs, 20% - Domestic OEMs and 25% - Footwear.

I feel this is difficult and not much revenue clarity is present than when com[pared to Symphony where Mr M discounts Symphony’s current valuations that it will grow at CAGR 22-25% for the next ten years.

When we see the two scenarios, Symphony is a better bet with revenue clarity present and a B2C model.

Thanks @PP1, @drgrudge. Yours comments on Mayur is very helpful. Yes, B2B and commodity type businesses cannot demand high valuation But, isn’t Mayur’s moat is on quality product that even other country leading car manufactures are also bought into ?

I was assuming Mayur will continue its run next few years for

(1) Export & Export OMEs will go up

(2) Domestic automobile, especially 4 wheelers market will steadily go up

(3) Foray into high margin sofas & chair furnishing. Waiting for this B2C initiative results.

@PP1, you are correct about the allocation. However, I did not give a more clear picture I suppose.

My current portfolio is about 14 months savings, hence in another 12 months I am going to almost double up my portfolio (assuming there is no significant movement in my current portfolio)

Exposure to Mayur will definitely come down, may be approx 10% or less. I am not in a hurry to sell as I hate to churn my portfolio too much and I took the exposure to Mayur in the last 6 months.

Somehow I am not convinced FRESH BUYing Symphony at PE 45+, even after the recent correction. Doesn’t “large base” problem apply to Symphony as well ? Shouldn’t we rather concentrate on smaller base and fast growing companies to get 35% CAGR for next 5 yrs ?

Look at 1 year forward PE, assuming earnings growth of 35%. Then the 1 year forward PE is about 35 (for Symphony @1750). That is a PEG ratio of 1, which is a fair valuation.

I don’t know about Mayur… But, Symphony doesn’t have a large base problem.

The domestic cooling total market (organized+unorganized) is itself growing at 20% (replacement of fans / buy a cooler for home as it works on inverter during power breakdown and the AC doesnt). Also, only 20% of the market is organized, the rest is unorganized - so extra growth opportunity.

The industrial cooling market is very nascent, and is a huge opportunity to be tapped (probably - we have to wait and see how it takes off)…

Export markets potential is also huge…

Should you look at smaller-cap instead of Symphony - Well, if Warren Buffet thought so, he wouldn’t have invested in Coca Cola. Retail investors have some sort of obsession for small-caps - but it is often not a healthy thing.

Example. Difficult for 100 billion company to grow at 30%, but not so difficult for a good small company to grow at 30%. So, easier to grow on a small base.

Example: Company A has 65% market share, in a slow-growing market. Then, difficult to grow @30%, because of large base.

I am thinking of deploying the 30% cash sitting in my account as it is painful to see cash sitting idle. However, a little nervous with the valuation of most companies. Thinking of adding some Banks and HFCs like Repco, Karur Vysya.

Please note that I have been adding Ajanta, PI and Shilpa on dips, hence the total returns have come down from the last time I shared my portfolio. Also, all the 3 shares have under-performed since last 4-6 months.