Sorry i have been unable to find this. Please consider sharing

- The precise report you read.

- Please share your key takeaways if possible so all of us can benefit.

Sorry i have been unable to find this. Please consider sharing

Hi Sahil, you can go through 2019 or 2020 ARs. Below are a few snippets from AR 2020 to answer your questions. In other section of the AR, they also mentioned that the low cost producers in these markets can create significant challenges for them to gain market share in the replacement market. You will have to connect the dots in the AR to understand the whole context of what I said in my previous posts. Apologize in advance, if my interpretation does not match yours.

Regarding the key takeaways from the AR, I have highlighted the doc, but have not taken down notes yet. I will try to do that, and post something here.

@RajeevJ your inputs from time to time have been very helpful. thanks

@vivekchat - i don’t have clear answer as to why the growth was lessor earlier and why high now. I don’t know if they will be able to maintain a higher rate going forward. At a high level they did say that with the current capex etc they can potentially double their business in next 4-5 years and that’s what they are aiming to do. Lets see if the recent changes in business are sustainable going ahead.

@varun86arora - thanks. it was good to meet you at the AGM.

Hi,

I just started reading about PIX of late, and I see a lot of people here who have done quite a bit of research on this company. So, I will post the few questions in my head:

Over the last decade, RM costs % have significantly come down (54% to 27%, Rubber prices have been also slightly low which has helped) - Which probably indicates the company has been taking aggressive price increases over costs. I wanted to understand the durability of this. Where is the price increase coming from? Domestic/Export. What is the price differential with products like Fenner/Gates that still exists and company can bridge. (% export on revenue has not gone up, so it has just been price increases)

Does the company have any sourcing advantages on raw materials, backward integrations which gives it an advantage going forward?

Although the RM costs have come down over the decade, EBITDA margins are more or less flat. Emp Costs as a % of revenue has doubled (12 to 24%). Yes, KMP have taken a pay cut in 2021, but their attitude has been generous and democratic pay to 4/5 key people in the last decade. Here on, can margins go up/likely to only go down with constant KMP salary/Emp cost increases (how much lower can RM costs % or other costs go down further - Any comparisons with other players?)

hello , i had more scuttlebutt one of major textile house with engineers in surat , they were telling top 5 brands includes pix, gates , jk fenner this are majorly used in the v belts , no one had pricing power whichever cheaper and easy availabilty is sold , but pix had brand recognistion , i had already tracking position in this company , i might be avg up also in pix.

disc not sebi regiter.

Thank you for sharing the notes from AGM. Since you and others on this forum have studied the business in detail just wanted to check if you have any views on this - the RoCE is quite low for the kind of margins the company enjoys. From the nos it appears that this is most likely this is on account of high investments required in P&M. While I read your comment that they double business with the curernt capex, they have never in the past achieved sales of more than 1x of the total investment in fixed assets. Any discussion that additional discussion that they you had on the subject which gave comfort that they can achieve this?

A meeting for listing in NSE will be held on 12 Nov ( along with results declaration for Q2 )

Gates 3rd Quarter result

Future Outlook

The Company is maintaining its full-year 2021 outlook for core revenue growth in the range of 20.0% to 22.0%. While the Company continues to experience a robust growth environment, additional inflation, particularly related to freight and logistics, and costs incurred to support the exceptional demand from customers are leading to margin pressure on the business. Although the Company expects the margin impact of these incremental costs to be temporary, it is updating its expectation for full-year Adjusted EBITDA margin to be in the range of 21.0% to 21.5%, compared to the previous range of 22.2% to 22.8%. The Company now expects total capital expenditures to be approximately $100 million, while Free Cash Flow Conversion continues to be expected at greater than 80% of Adjusted Net Income.

Margin Pressure in Pix Transmission will be key thing to watch in coming quarters.

Does Pix transmission hold quarterly concalls because I am not able to find any?

On a side note, the result of this quarter looks decent to me.

What is the logic behind saying its overvalued? Could you give 5-10 pointer? I see PE mean for last 15+ years is 12.8 and current PE is 13.6, ROCE 27, ROE 28%, OPM 26+%, D/E is 0.32 that is manageable. Sales growth decent and profit growth for last 5 years are 58%.

How it is overvalued?

World and market are convinced about electric vehicle can be the next trend. I checked for pix portfolio and found they have some products to offer for EV.

Need to understand if demand pick up how pix can increase products and capatilise in mega trend.

https://www.pixtrans.com/products/automotive-belts/more-auto-voy-belts.php

Disclosure: Invested

Pix is at the business end of the year. The second half is the busy season for the Co. The expansion is likely to be completed by the end of the current fiscal. The Co. for 2022-23 hopes to do increased sales of about 600 crs. At current levels of profitability it should do profits of about 105-110 crs for the full year without factoring in increased margins due to operating leverage.

The current market cap of about 1017 crs makes the valuations rather attractive. The stock seems to be at an inflection point. With the Co. enjoying such high operating margins, growth in sales results in a disproportionate increase in profits. Such companies usually tend to enjoy multiples in excess of 20.

The mgt is on record about getting its shares listed on the NSE shortly, making the cost of transactions much lower going forward. All indications of better days ahead!

Sir i agree in general on valuation. Another observation for me has been that if & when management opens up about biz in any way: investor presentation, concalls, that proves to be huge valuation unlocker too. I hope pix can start doing concalls/IPs as soon as possible.

Yes, I agree. I think concalls, investor presentation etc. should start within the next twelve months or so & the Co. should engage the services of an IR firm. Once Companies taste the joys of market cap, they want more of it! In Pix’s case, it will be well deserved as well!!

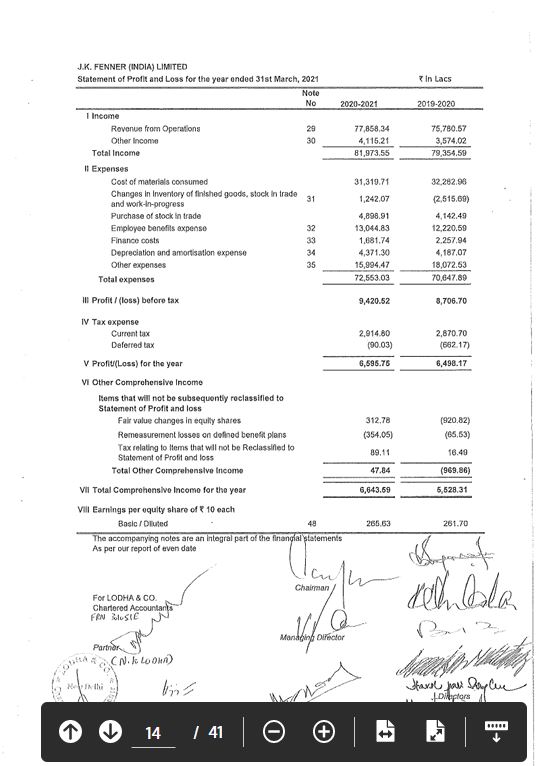

I just did a check on the financials of JK Fenner.

According to this both the PAT and Revenues of JK Fenner have remained flat. On the other hand, Pix’s PAT and Revenue both have grown quite a lot. Does this indicate a continuous market share grab by Pix?

Disc: have a 1% allocation to it. (new to investing, hence a little conservative when it comes to microcaps)

Need details of segment results and overlapping categories for both the companies to conclude the above. Flatness in revenue may be due to revenue drop in the non-overlapping segments such as supply to 4W OEM (New Car Mfg.).

Is Fenner listed as I could not locate? Else, what’s the way to get Fenner’s AR?

No, not a listed company. It is owned by Bengal & Assam co. that is listed. So, got it from their website. It’s AR was not available for this year.

Not much to add on fundamentals with excellent data points in thread above from @RajeevJ @sahil_vi. And fellow VPers.

Promoters continues to increase share holding every quarter - albeit smaller pace

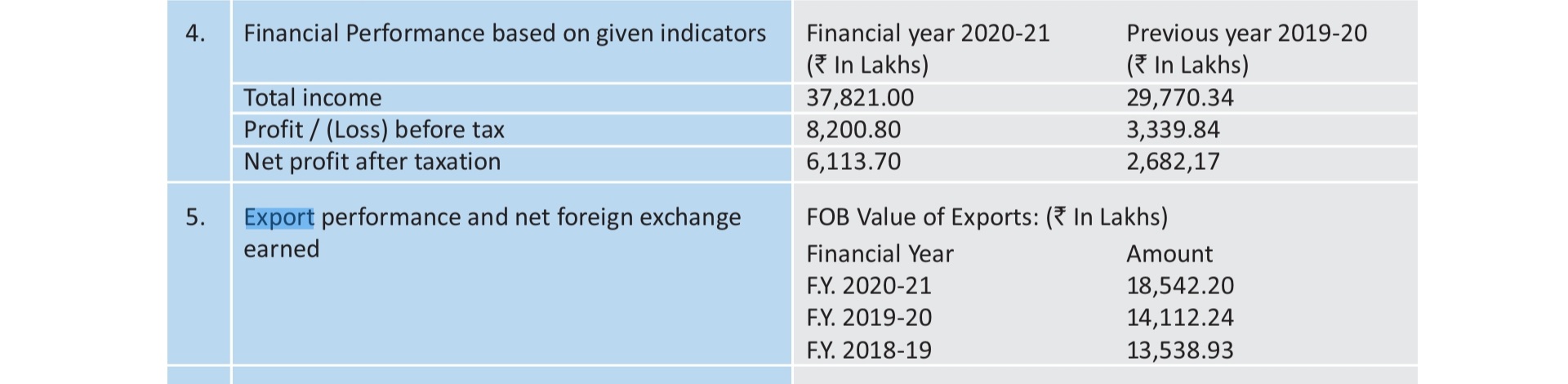

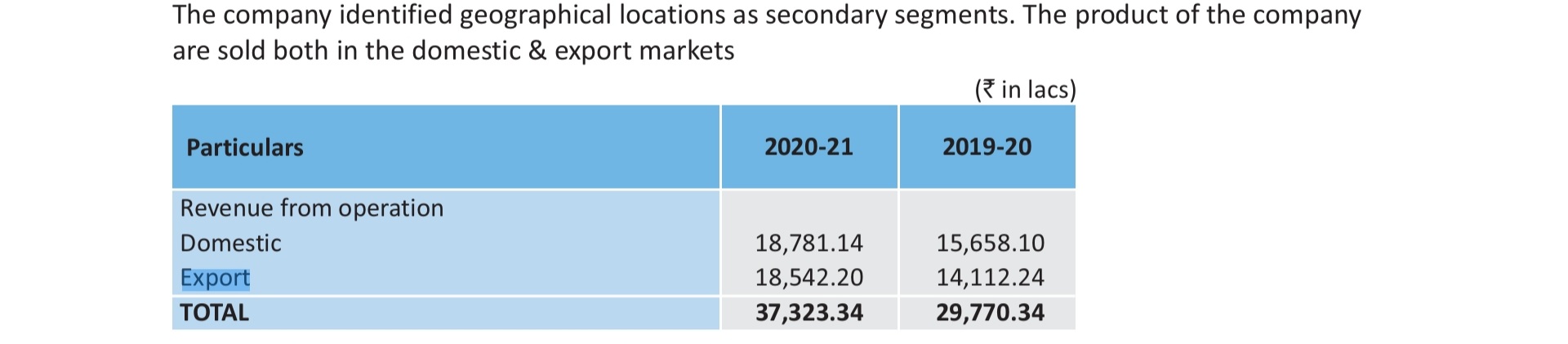

Higher Export mix seem to be reason behind margin expansion, faster export growth than domestic - small data set from AR but seems logical explanation of margins expansion in a tough year, besides Op leverage and pricing power. Also export seem to be on FOB basis thus no impact of global shipping turmoil.( FOB - FREE ON BOARD)

On technical seems to be in narrowing triangle pattern with 5+ months consolidation, currently near breakout point - stable in last few sessions volatility

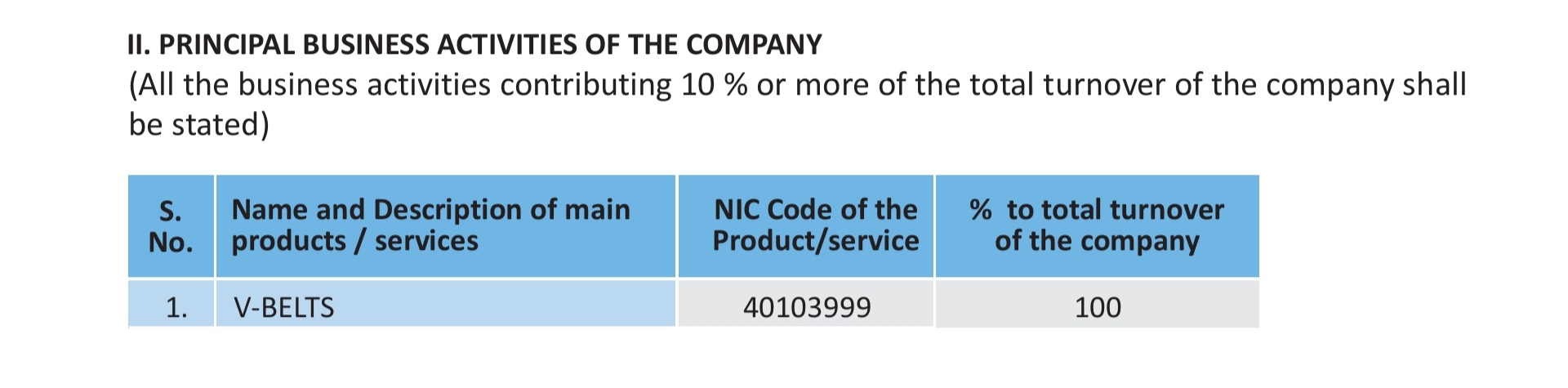

Company may be eligible for MEIS credits, scheme is being replaced with RodTEP and can help boost bottomline as transition to new scheme seems WIP - applicable to all exporters. ( basis NIC code)

All in all a good Capex cycle play with large opportunity size relatively to Pix current size n scale. Being a microcap, rerating has been swift in last few quarters, runway for growth and potential to rerate further as long as they deliver.

Besides numbers it’s a good business model with customers stickiness resulting from customization reqmt for each customers, Opex play from customers lens thus consumable with repeat business, requiring large no of SKUs with growing customers base ( to some extent reminds of BKT model - Balkrishna tyres).

Added in recent correction.

Pix auditor note of 2016 and same in AR 2020

I did not audit the financial statement of subsidiaries & Joint Venture Company as at 31st March 2016. Thesefinancial statements audited by other auditors whose reports have not been furnished to us by the Management and our opinion on the consolidated financial statements, in so far as it relates to the amounts and disclosures included in respect of these subsidiaries, and our report in terms of sub section (3) and (11) of section 143 of the

Act, in so far as it relates to the aforesaid subsidiaries is based solely on Management accounts certified by the Management.

Lets take example of other company

L t foods auditor note

We have audited the accompanying Consolidated financial statements of LT Foods Limited (hereinafter referred to as the “Holding Company”) and its subsidiaries (Holding Company

and its subsidiaries together referred to as “the Group”), its associates and a joint venture

As mentioned by Dr vijay malik sir ,it seems to be clear red flag. Company has definately good growth prospects but few points keep me confusing for investment

1…Subsidery audition

2…High renumeration

3…High % of RPT@24%

2021

Rpt@16 cr

Pat@ 65 cr

4…I think RPT in previous yrs may be very high due to lower PAT