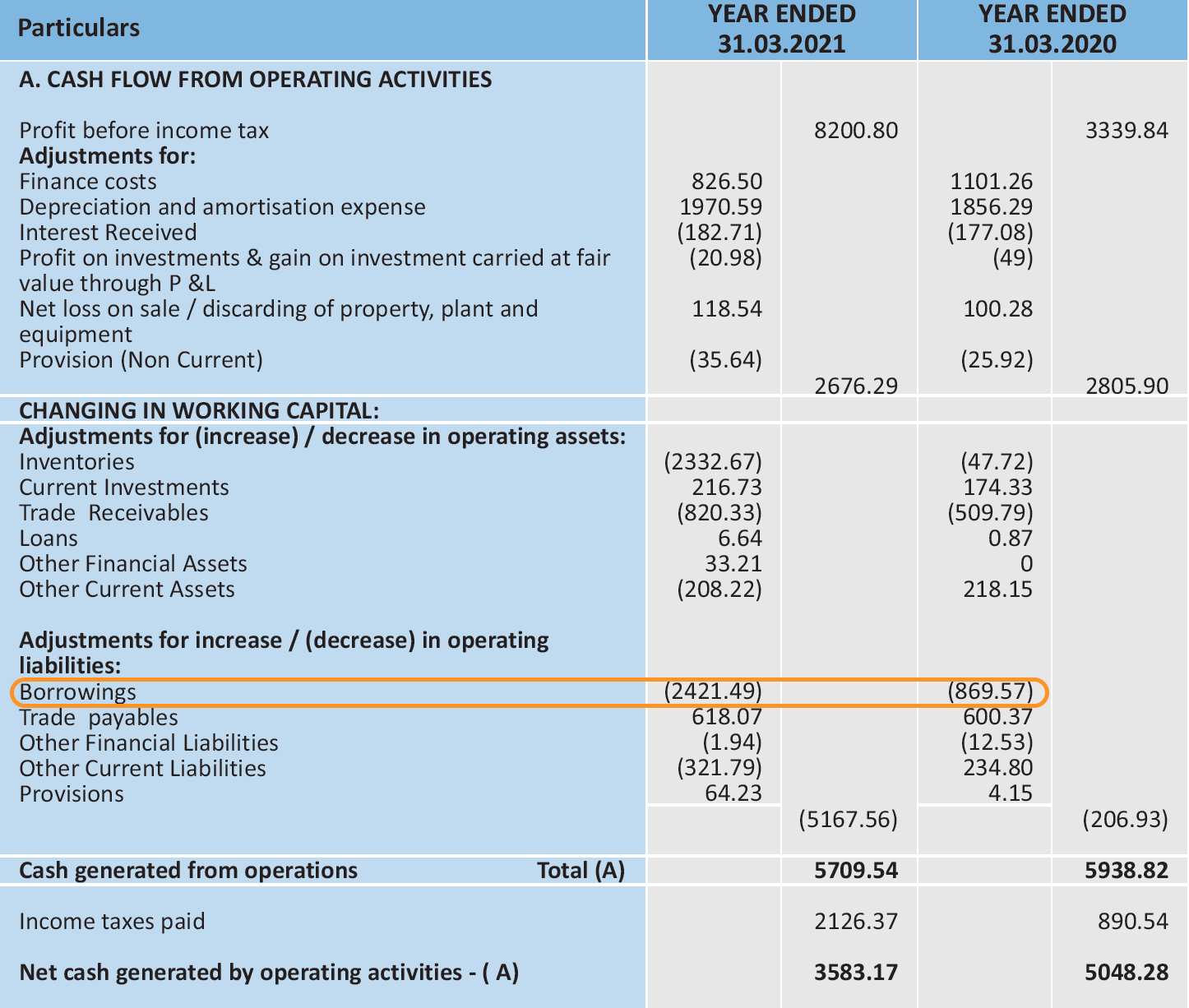

Not sure why a change in borrowing (whether short term or long term) should be part of cash flow from operations and not finance.

Pls share the names of some other companies where this is being done.

Regards,

Vivek

Not sure why a change in borrowing (whether short term or long term) should be part of cash flow from operations and not finance.

Pls share the names of some other companies where this is being done.

Regards,

Vivek

You are right. CFO calculation seems incorrect in the Annual report as well as in the Q4 result release. I have already shared the same with the CFO couple of times over email but there has been no response from the company.

D: Invested. 3% weight.

Hi Vivek, If you are talking about this line item as shown below, then yes, it seems like they are subtracting cash due to short term borrowings from CFO. I am not sure if it’s a standard practice and I am not an expert on the cash flow statements either, but my limited understanding suggests that if we add it back to the CFO, wouldn’t that increase the cash generated from operation?

Not able to understand, why would a company want to report lower CFO, although it would have no effect on free cash flow?

Regarding R&D…

In the AR 2017-18, in chairman’s letter, Mr. Amarpal Seth seems cognizant of the fact that R&D is required in his business to be ahead of the competition…

He says “… The global scenario is changing day by day with cut throat competition and constrained margin is hampering product marketability. The products are marketable if it is innovative… The product research and development and quality control will only save us in grave situation …”

However, since the above statemen is said in 2018, there is no R&D expense seen in any of th subsequent years… why ?

Someone pointed out above how the belts are bieng replaced by electronics / computer panels etc…

In light of such technology already being in us, can the company lag behind in R&D ?

Do read this previous post for context on Gates.

A quick update on this with Gates’ Q2CY21 performance.

Sources:

GTES-Q2-2021-Earnings-Release-Presentation-Final.pdf (2.3 MB)

GTES-Q2-2021-Earnings-Transcript.pdf (358.5 KB)

Disc: Invested, biased

Good results

Pix appoints M/s MSKA & Associates as joint auditors. Hopefully this improves auditors quality.

Came across one company “International Conveyors Ltd” , manufactures of PVC Conveyer (mix of PVC and Fabrics ) belts similar to what is being manufactured by Pix and interestingly Cresta Fund is one of the Investors. Attaching link to their presentation

Anyone attending AGM tomorrow? Would be great to collate questions if anyone here is attending. I will be happy to share my list of questions. Thanks

I have given the suggestion to company to conduct online AGMs in future.

D: Invested

https://www.amazon.com/Pix-399-A36K-Blue-Kevlar-V-Belt/product-reviews/B004MRI1IU

Reviews on Amazon for their V-Belts

Thanks for adding. this is very useful. Having worked extensively on reviews, one thing i do want to caution investors about is not to take each amazon review at face value. Some/all of these could be fake reviews.

Annual Report - JK Fenner - 2019-20

Don’t know if it will add value though

In our industry (textile) we have personally always used fenner belts (now jk fenner) or gates (imported) ….I have personally never used a Pix belt…but yes i agree…these teeth/timing belts r an important element of the machine…and we use to keep atleast one spare for each machine always…(there usually was a shortage)

Pix Transmissions - Initiating Coverage - 270821.pdf (998.3 KB)

HDFC Securities initiates a buy on Pix Transmission with a target of 882 (in bull case)

Hi,

I did attend the AGM recently. Some of the points in brief:

Cheers,

Ayush

Disc: Invested in family and client acs.

Thanks for this insight, Ayush. I read Gates’ annual report and they mentioned in the belts business, aftermarket and replacement belts is a huge opportunity, but in emerging markets, they have not gained traction in this segment due to the presence of local players like Pix and Fenner. So that’s a good news.

While I think this is great business due to high SKUs, and R&D focused customized solution, the only thing concerns me is the high level of inventory and trade receivables, resulting in high cash conversion and working capital days. Cash flows have not compounded at all in the last decade. I am not sure if the management commented on this in the AGM.

Disc: Invested, with a tracking position.

I think high inventory is normal in this business and perhaps the key reason for high margins…as one has to keep different SKUs. When someone buys a belt for replacement, he wants availability to restore the machine and perhaps that’s where these cos command good price. Mgmt said that this year inventory was higher to avoid raw material sourcing disruption/problem and also get good prices as the same were increasing rapidly.

Debtor days looks ok inline with past trend so didn’t ask.

Thanks a ton Ayush for sharing your thoughts about the developments at the AGM & more importantly your insights on the working of the company. Pix AGM is a more demanding experience as it entails an overnight stay in Nagpur.

The Pix story is still in the process of getting recognized. Finally, a big broking house has covered the Company. HDFC Securities has come out with a report on Pix, though their targets are highly conservative. Expect upgrades from them on target price as we go along!

Pix Transmissions - Initiating Coverage - 270821.pdf (998.3 KB)

Hi Ayush,

Did the management give any guidance/road map in terms of growth in sales, profits and capital required over the next few years?

The company has grown at only single digits prior to FY21 and wanted to understand if this recent growth is sustainable.

Regards,

Vivek

While your question is directed to Ayush, I will attempt to answer this. I had a chance to ask this question. The response from the company was that it takes time to build brand and distribution. Both take lot of time. At the same time, while doing business they had to keep working capital in check which by nature of business is on higher side. Company seems more optimistic as the brand, quality of products and distribution have been established. The same is also evident in capacity expansion plan. Some part of sluggish growth may have to do with capex cycle. Good part is that while sales growth prior to FY21 was not high, it exhibited less volatility and cyclicality, probably a function of them focusing on replacement market.

Going by outlook given by Gates, capacity expansion plan of Pix, growth rate in recent quarters, the fact that company is looking for warehouse, possible pick up in domestic manufacturing all these point towards better growth run rate than shown prior to FY21.

Regards