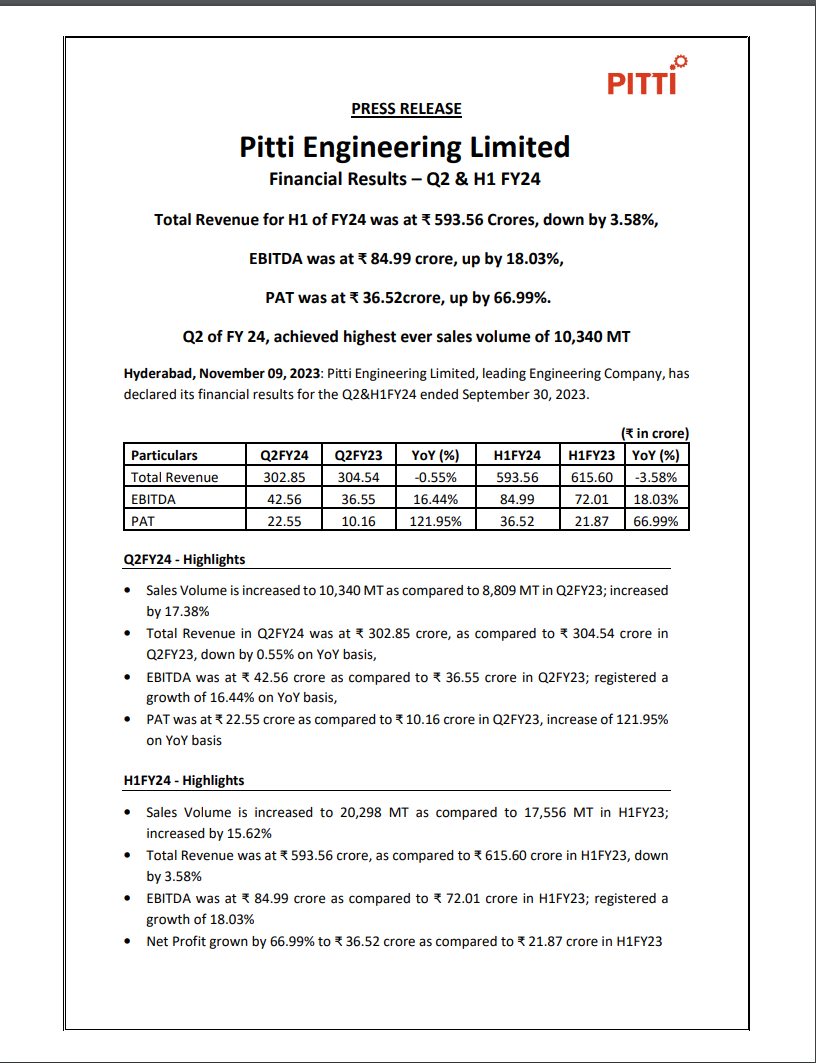

Pitti Engineering Limited, a prominent engineering company, has released its financial results for the second quarter (Q2) and first half (H1) of the fiscal year 2023-24 (FY24) ending on September 30, 2023. The key financial and operational highlights are as follows:

H1 FY24 (First Half of FY24):

Total revenue for H1 FY24 amounted to ₹593.56 Crores, representing a decrease of 3.58% compared to the previous year.

EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortization) stood at ₹84.99 Crores, marking an 18.03% increase.

Profit After Tax (PAT) reached ₹36.52 Crores, showing significant growth of 66.99% compared to the previous year.

Q2 FY24 (Second Quarter of FY24):

Achieved the highest-ever sales volume of 10,340 Metric Tons (MT) during Q2 FY24, signifying a 17.38% increase compared to Q2 FY23.

Total revenue for Q2 FY24 was ₹302.85 Crores, slightly down by 0.55% compared to Q2 FY23.

EBITDA in Q2 FY24 reached ₹42.56 Crores, which is a 16.44% increase from Q2 FY23.

PAT for Q2 FY24 amounted to ₹22.55 Crores, reflecting a substantial growth of 121.95% compared to Q2 FY23.

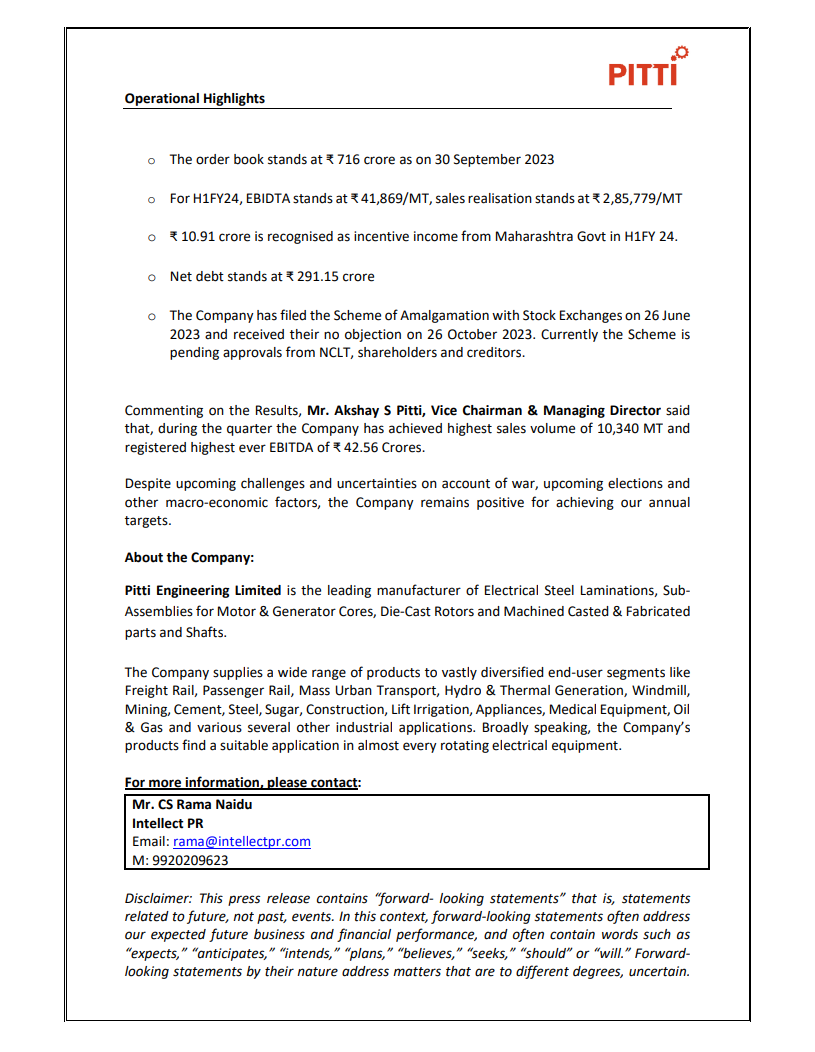

Operational Highlights:

The order book as of September 30, 2023, stands at ₹716 Crores.

In H1 FY24, the company’s EBIDTA reached ₹41,869/MT, and the sales realization was ₹2,85,779/MT.

The company recognized ₹10.91 Crores as incentive income from the Maharashtra Government in H1 FY24.

The net debt of the company stands at ₹291.15 Crores.

The company has filed a Scheme of Amalgamation with stock exchanges on June 26, 2023, and received no objections from them on October 26, 2023. The scheme is currently awaiting approvals from the National Company Law Tribunal (NCLT), shareholders, and creditors.

Management Commentary

The company achieved several milestones during the quarter, including the highest sales volume of 10,340 MT and the highest-ever EBITDA of ₹42.56 Crores. Despite upcoming challenges and uncertainties related to factors such as war, elections, and macroeconomic conditions, the company remains optimistic about achieving its annual targets.

Shareholding Pattern for Q ending Dec 23

The retail holding has become less. FII and DII have increased their stake. JR Seamless Private Limited now also have 1 per cent stake. Overall the shareholding pattern seems to have become stronger. Number of shareholders is at all time high. That to me seems to indicate increased awareness and hope.

1-No impact on margin if raw material price increase or decrease. It is due to some contracts with customers.

2-Growth driven by railway, renewable energy and power sector.

3-Order book increased by 25-30% QoQ.

Q3 Order book is 898cr. Good order book visibility ahead.

4- Capex for Aurangabad facility coming live in H1FY25.

5-42000 metric tons to 50000 metric tons after capex in FY25.

6-Pitti Castings amalgamation will improve margin significantly and EBITDA will be increased. 70% sales of Pitti Castings is derived from procurement of Pitti Eng. So common revenue will consolidate and margin will improve.

7- Tax will be lower in FY25(after amalgamation) due to unabsorbed losses in Pitti Castings. Unabsorbed loss is 80cr. It will help in high EPS.

8-Debt under control.

9- After Amalgamation sales of value added products related to machining will increase. It will increase margin significantly.

10- Peak utilisation will be reached in FY26 . After that further capex will be planned depending on market requirement.

11- This year got 13.09cr incentive income.

32.42 cr more incentive income expected in Q4 FY24 for Aurangabad facility.

1-Current capacity of BCIL is 14000 tons. Peak capacity can be reached is 18000 which will be reached in FY26.

In FY25 they will reach 16000 tons.

2- In FY25 BCIL will do EBITDA of 30cr.

(EBITDA of FY23 was 14cr)

3- Current debt is around 450cr. No more debt now.

Very Big news is they are planning to be debt free by FY26.

200cr Cashflow will be generated by Pitti annually.

20cr EBITDA by Pitti Castings and 30cr by BCIL in FY25 possible.

4- Benefit of this acquisition is that Logistics cost will he improved vastly. Though currently numbers of BCIL show less EBITDA margins but after acquisition it will improve as raw material cost will go down (it will be supplied from Pitti Only)

5 - This facility is in Bangalore where lot of clients are located. Logistics cost will be reduced.

6- Current order book 120cr for BCIL

7- FY25 consolidated EBITDA margin would be 17% and EBITDA around 295cr and approx 1700cr Topline.

8- FY26 → 360cr EBITDA+35cr incentive income by government.

9- 70% production capacity is automated. They are more inclined towards Industry 5.0 standards.

Subject: Update on industrial incentive – Disclosure under regulation 30 SEBI (listing Obligations

and disclosure requirements) Regulations, 2015

Further to our letter dated 20th May 2023 providing an update on the industrial incentives and

benefits under the Package Scheme of Incentives (PSI) 2013. We are to inform you that the

Directorate of Industries, Government of Maharashtra (GOM) has its letter dated 2nd May 2024

amended the Eligibility Certificate under the Package Scheme of Incentive Policy (PSI) 2013

pursuant to the application made by the Company for additional investment made at its

Aurangabad facility for the period 1st January 2019 to 31st January 2022.

The GOM vide the above stated letter has amended the Eligibility Certificate under the PSI 2013 and

revised the Industrial Promotion Subsidy (IPS) to Rs.16865.05 lakhs from the existing Rs. 10360.52 lakhs.

This is I think the total amount of subside that the company will receive over the years. Please correct me if I am wrong.

Q4 Results and FY 24 results on Wednesday 15th May. Dividend declaration possible. The company is also thinking of raising money through preferential allotment.

Hi, is anyone still tracking the company? Could someone shed light on how the recent announcemt of “NCLT approves amalgamation of Pitti companies” benefits the company from a quantitive perspective? What is the combined revenue?

Revenue Growth: The combined revenue of Pitti Engineering Ltd is expected to grow significantly post-amalgamation, with projections showing an increase from INR 12,016 million in FY24 to INR 20,356 million in FY25 and further reaching INR 23,768 million by FY27.

Efficiency Gains: The merger with entities such as Bagadia Chaitra Industries and Dakshin Foundry enables expanded capacity and cost efficiencies. Pitti’s expanded Aurangabad facility, along with new copper winding capabilities, is anticipated to improve margins and customer acquisition.

Broader Market Reach: The acquisitions extend Pitti’s geographic footprint, unlocking new markets and enhancing its role in high-growth sectors like renewables and railways.

I have been incredibally lucky to have invested in Pitti Engineering around 60 levels. Even through the blood bath in 2025, stock has been above 1000 levels. Recent promotor sell around 1400+ has reduced my confidence (who are we mere mortals to know more than promotors). Any view from boarders here if there will be continued EPS growth?