Pitti Engineering Limited: Is it on an inflection point?

Pitti Engineering Limited (PEL) formerly Pitti Lamination Limited, started its operations in 1983. It is in the business of producing Sheet Metal, Die-cast Rotors & Assemblies, Stator Core Assemblies, Fabricated Machined Components, Pole Assemblies, and Machined Components for varied industries including industrial drives, freight and passenger rail, mass urban transportation, power generation, aerospace, oil & gas, mining and earth moving equipment, renewable energy and infrastructure projects, amongst others. Company’s products find application in basic capital goods, such as motors and alternators, which are themselves quintessentially used in any process engineering. Marquee clients of the company include many leaders in the electrical equipment manufacturing field.

The expansion plan:

During the quarter ending Dec 2019, the Board approved the expansion plan to enhance its installed capacity from the existing 36,000 MT to 46,000 MT for sheet metal components and from 247,600 hours to 405,600 hours for machining which will be completed in a span of 36 months with a total capex of INR 270 crores. At the end of Q1 FY 21, the Board reiterated its resolve to go ahead with the capacity expansion despite low turnover and loss at the net level in that COVID19 affected quarter. Promoters increased their stake @ 90 per share:

The Company allotted 22,22,222 convertible warrants at a price of INR 90/- each to be converted into 22,22,222 equity shares of 5/- (including a premium of 85/- per share) on preferential basis to the persons belonging to Promoter/ Promoter Group on 14th February 2018. The same were converted into fully paid-up equity shares on 24th June 2019. The Aurangabad Advantage?

PEL has two plants at Hyderabad and one plant at Aurangabad. The Aurangabad plant started its operations in January 2018, after the facilities from Hyderabad were partially shifted to Aurangabad. This shift to Maharashtra brings the Company in proximity to its customers as well as raw material sources. This will supposedly reduce the Company’s logistics and operational cost to a significant extent, making its operations more competitive.

This supposition by the management may be true, as after the start of Aurangabad operations, PEL had two years of improved sales and profitability, as shown in the figure below (curtesy screener.in).

The tailwinds

Capital goods, electric vehicles, data centers, Indian railways, and wind energy are some of the sectors using company’s products, and that are showing uptick in growth momentum. PEL expects substantial order flows from these sectors during coming years.

Apart from increased expectations of growth in these sectors there is increased focus on making industrial goods inside the country through Make in India and Aatmnirbhar Bharat campaigns. These indigenization drives will help PEL in increasing its production. Aiming at 1000 crore annual turnover with shifting goalpost

During FY 2012 PEL increased its capacity to 32000 TPA and aimed at 1000 crore annual turnover during subsequent three years. However, maximum turnover so far that the company could achieve so far is 622 crores during FY 2019. But the latest annual reports continue to reiterate company’s position to become a 1000 crore company. And there has been an uptick in the turnover of the company during last two years. Strong relationship with the customers

PEL boasts of strong long-term relationship with its international customers. The 2015 Annual Report of the company says and the same is reiterated in subsequent annual reports:

“At Pitti Laminations, we are catering to evolving requirements of customers through developing better products and processes, focusing on quality parameters consistently, implementing best-in-class technology and sustaining price competitiveness.

“We are a fully integrated player addressing the needs of a huge customer base. We work with customers as developmental partners, rather than just business affiliates.

“In the laminations segment our domestic clients include ABB, Andritz, Alstom, BHEL, Crompton Greaves, Cummins, L&T MHI, ReGen Powertech, SE Electricals, Siemens, TDPS and Voith, among others. Around 36% of our domestic revenues are derived from existing relationships with long-lasting clients (Crompton and Siemens are with us for over 22 years, whereas Cummins and ABB are our clients for 17 years). The GE Group is the single largest global customer, accounting for a majority of our export in 2014-15. We were awarded with the ‘Certificate of Excellence’ by GE for being the ‘Best Supplier – Quality 2015’.” The Risks

According to the Annual Report of 2020, PEL faces the following risks. Economic risk:

Capital goods sector is inextricably linked with the overall economic, infrastructural and industrial growth of any country/region. Technology risk:

Being in the business of engineered goods with a significantly higher level of customization, the company’s business is susceptible to technological/ product process obsolescence. Concentration risk:

Being overdependent on a particular customer, user segment or country/ region can pose a business risk in case of the said constituent undergoing a business crisis or preferring to shift to another supplier. Competition risk:

Emergence of a large number of competitors vying for the same business can heighten competition risk which often leads to revenue and margin erosion. Liquidity risk:

Capital goods sector continues to be a capital intensive sector involving longer cycle of product development that often includes proof of concept components as well. Safety, health and environment (SHE) risk:

Occupational hazards may endanger the safety of our employees and communities around our manufacturing locations besides adversely affecting the flora, fauna and environment. HR risk:

Any erosion in commitment, competence and compassion of employees towards company’s stated vision of value creation can incapacitate the company’s abilities and reputation. Unforeseen Risk:

The most significant emerging risk is the ongoing COVID-19 pandemic which resulted in a loss of human lives, impacted economic activity across the world and eroded wealth more than what the financial meltdown did. Other risks not listed in AR 2020

Significant portion of PEL’s raw materials are imported and its produce is exported. Therefore, company also faces the risk of adverse foreign exchange fluctuations. Please read the annual report 2020 (pp. 22-23) to know more about the risks that the company faces and what measures it takes to mitigate these risks. Increased focus on domestic sales

For last several years, PEL has been focusing on domestic sales, after witnessing the unpredictability of the export markets. Export sales volume of laminations in FY17 was at 2790 tonne, after its recent peak of ~8000 tonne in FY15, while domestic sales showed a slow but steady rise. This fall in exports was mainly due to the key customer GE witnessing a marked slowdown in the offtake of its products. It was not related to client attrition. Inputs are needed from industry and financial experts

I have tried to understand the journey of PEL during last decade, mainly through company annual reports and research reports of ICICI Direct. In this report, I have tried to describe that journey. Based on my limited understanding, it seems that PEL has become an established name in the electrical lamination industry domestically and worldwide. The company has continuously focused on improving the quality of its products and cost efficiency. The company has also focused on becoming more customer friendly. With increasing demands of the products and increase in value addition and capacities, it is possible that the company is at an inflection point.

I am hopeful that this description of the journey would awaken the interest of experts from electrical lamination industry and financial experts, who will be able to cast more light on the prospects of the company. Disclosure: Invested.

Blended EBITDA per metric tonne was 40,695 as against ₹42,521 per metric tonne in the corresponding quarter last year

The minor decrease is attributable to our efforts in reducing DSO (Days sales outstanding ) from 92 days to 54 days from the corresponding quarter

The company continues to be working on reducing the operating cycle. Working capital cycle as on September 30, 2021 stands at 99 days. We have set ourselves a target of reducing this to 75 days within the following year. I believe this will free up sufficient cash to fund the company’s growth without taking on any significant debt in the coming years

In February 2020, we had announced a capex of ₹ 270 Crores. I am happy to report that despite the challenging 18 months that we have faced, we have completed 35% of the envisaged capex and remaining is on track for timely completion

During the last one year our capacity has grown from 36,000 metric tonnes per annum to 41,000 metric tonnes per annum

The increased capacity is fully utilized as on date. Further, as our capacity is modularly expandable any incremental additions that will keep getting added on a quarterly basis shall keep getting utilized as they get commissioned.

At the end of this capex cycle, our capacity will be 72,000 metric tonnes per annum (from existing 36,000 metric tonnes per annum)

With the constant price, the revenue potential at the end of this capex cycle for the company shall be 1,800 Crores (TTM 739 Crores ->143% increase )

In the first half of FY 2022, the company has developed products for applications such as 3.4 megawatt windmill generator for Gamesa, 4 megawatt compact hydro generator for Simens and railway motor for Mitsubishi metro among others. These have a potential of adding 45 Crores of revenue per year going forward. I continue to see buoyant demand from all our key end user segments. The order book and forecast as of September 30, 2021 stands at 984 Crores.

Volume growth we see at this year we should be closing around 40,000 tonnes per annum if all goes well vis-à-vis the current 14,000 tonnes that we have done, but of course

this is subject to addition of capacity which is going on right now. In terms of margin, we

see the margin is stable between ₹ 40,000 to ₹45,000 per tonne EBITDA margin.

The stator and rotor that we supply do find application in EV and we are in active discussion with a couple of end users to develop these products, we should be able to you know state something more explicitly in the next 6 to 8 months.

So competitive landscape, so China has slowly and gradually withdrawn more and more

export incentives that they had and as a result now India and China are having parity in

terms of most of the product that are manufactured and generalizing that statement, as far as

our industry is concerned, we always had better price parities than China so much of our products were indirectly exported back to China, so in terms of competitiveness we have always been competitive, in terms of demand environment, yes, we are seeing a definite

shift wherein now this China Plus One policy at the global sourcing level and more and

more global sourcing is getting diversified to safeguard against any geographical and

political risk. Local demand like I said I am seeing buoyant demand from all our end user

segments, the order book and forecast stands at 984 Crores, which is all time high, we have never seen this kind of demand before and the orders are continuing flow in

41,000 is the annualized capacity as on September 30, 2021 itself, by the end of this

year I think this capacity will grow to about 48,000 to 52,000 tonnes depending on the

arrival of our machine, as I said the capacity is modularly expendable as the machine keep coming in the capacity will keep going up, in terms of utilization of this capacity if you see the capacity which we have commissioned in quarter two is also fully utilized, our capacity utilization is running at 88% including new equipment arrival. By H1 FY2024 we will be 72,000 tonnes capacity.

*Data power systems if you see we have started to give a separate line item in our

presentation, we see huge demand coming from this segment, apart from that the renewable energy space, wind turbines are going well, in terms of new applications for a product they are two very promising fields that we see, one is in terms of de-centralization plant at coal power plant wherein to comply with environmental regulation they need to do carbon capture and diesel emissions so that is one sector that we see maybe in the next 5 years to become big and apart from that obviously the buzz word which is the electric vehicles space.

Today in terms of railways, railways I would say including metros because that is how we

account for it, 28% of our business comes from railways, going forward we see this

business increasing by 25% to 30% in the next two years.

Capex entirely is Brownfield, the facility that we already have in Aurangabad factory, we have

additional land available adjacent to it which is equal to two time the land that is already

being developed so it will be coming up right in the same campus.

Total blended cost of debt is about 8%.

the last 4 to 5 years our blended EBITDA per tonne has gone from

19,000 to 40,000 today and we see this is tracking upwards further.

We do not focus only on doing assemble and value added products. At the end of the day we

also track ROCE, so when we do the lose lamination the amount of capital that we need to

deploy even it is a lower EBITDA margin business, the capital deployed is much lesser, so

we like doing the lose lamination business as well so we have no bias in doing either or,

depending on the opportunity and the kind of return on capital we are seeing in this firstly.

Secondly you said that it gone down from 73% to 70% that is true, but if you see the

volume growth, the volume has come from 5,600 to 8,600 so you cannot always just

increase only high value added and assemble component, if you have to grow you have to

grow across the industry right so this thing will keep varying and in terms of taking new

business, if you see good ROC in lose lamination we will continue to grow that business as

well.

There is a huge entry barrier, if what we talk of high level numbers if we go to the micro level we are more than 5,000 different products developed all of which are active for the client, to compete with me some new entrant had to develop all the 5,000 products in one shot which is practically impossible which is the development of the last 30 years of products so to this we are developing inventory of 5,000 products and every year we add at least 5 to 10 new products to our library.

in most of the products that we make which are

intermediatory products which go into the final product that our customer make, we are soul

suppler in most of the places that we operate, secondly the kind of product we operate it is

very difficult for a new entrant to come in, we compete with three different industries, we

have a combination of three different industries, we have changed the way our end

customers do business so we started our traditional sheet metal company hence we always

talk in per tonne basis or per tonne capacity, but we have moved well beyond that, we have

a fabrication facilities, we have our own tool room, we have our own machine shop, we

have our own shaft manufacturing facility to replace us in the supply chain, first and

foremost my competitor needs to find three to four different companies each in a different

field and then find someone to integrate the product, assemble and supply it as a ready to

use unit, so in terms of capabilities we have a unique process that we have created over the

last 5 years. In terms of cyclicality of the industry each end segment has a cycle if you take

consumer durable ceiling fans or AC motors they have a seasonality, winter have a

seasonality, we could not install winter winds on monsoon period, but apart from that rest of

the industry segment that we cater to typically do not have any seasonality.

in total we will be eligible to get more 400 Crores of incentive for Maharashtra

government once our entire capex is done, this will be spread over a total of 13 years. Starting from FY2018, so what you have to seen us book is what we have booked in

FY2018-FY2019 and FY2019-FY2020 till now, so 2 years are done, another 11 years are

pending, the rest of the amount we will get in these 11 years.

Top five would contribute about 60% to 65% of revenue.They would be Siemens, Wabtec, they would be ABB, they would be Cummins and the fifth number keeps changing on and off sometimes it is Toshiba, sometimes it is Crompton, so the fifth number keeps changing but top four always remain constant, Siemens, ABB, Cummins and Wabtec.

=Metro, Freight and Passenger Rail segments continue to grow significantly. We are seeing strong

demand continuing from the wind energy segment. Encouraging progress is visible in Electric

vehicle and Automotive segments as well.

=We have healthy business visibility and an order book

of Rs. 1,078 crores as of 31 March 2022.

=Renewable energy, especially windmill is currently projected to grow very strongly based on our interactions with our customers. We are seeing tremendous growth coming from

there.

=Traction motor, railway and metro will grow.

=EV and the automotive will start

contributing significantly and special purpose motors will also grow.

=Predominantly in consumer durables, although they contribute less than 1% of our revenue, that’s

the only place where I am seeing de-growth or pressure on some demand side.

= Apart from that, all of the other sectors are also growing, but not at 30% obviously. Mining, oil, and gas are the other one, which are going to grow significantly because of the off-highway vehicles and price

in oil going up.

2…Capex

A=On the CAPEX front, we have spent Rs. 137 crores out of the Rs. 270 crores planned CAPEX,

and the residual entire capex is on track for completion by FY23 itself.

B=The Company has also recently decided to invest an additional Rs. 197 crores for FY24 and

FY25. This incremental investment is towards replacement of old equipment and modernizing of the Hyderabad facilities, further automate the Aurangabad facility and enhancing of

machining capabilities and capacities.

= The Hyderabad facility is aged. It was set up in 2004 and 2005 and with this automation, we should be able to see EBITDA increase to Rs. 48,000 per ton, once CAPEX is

done.

=This CAPEX will start not before FY24 and out of the Rs. 197 crores and I am just giving you broad numbers, around -Rs. 70 crores is for replacement of the existing lamination facility in

Hyderabad, about

Rs. 55 crores is towards the additional machining hours from 600,000 to 648,000 and the

remaining is towards automation and general CAPEX that we would require to upgrade the infrastructure in Hyderabad and Aurangabad to accommodate this new CAPEX

3…Debt

=Peak debt at the peak of the implementation of CAPEX cycle will not exceed Rs. 360 crore

=Will be debt free after about 5 to 6 years from now.

4…Current quarter Q1 of FY23, we have the strongest and healthiest order book that we’ve ever had in the history of the Company.

5…Domestic@80%

=We are not losing any clients in exports. We see the domestic market growing disproportionately

vis-à-vis the export market. Exports also have grown. If you see, we have exported Rs. 296 crore

of sales, which is again much higher than the previous year, but the domestic customers are

growing at a faster rate than our exports, which is why we see that going forward domestic will

become close to about 80% of the total revenue mix.

6…EV capacity

=There is no separate capacity for EV. It is the same product as far as we are concerned whether

it goes in the electric scooter, it goes in electric bus or in the traction motor, the process is the

same. So, you can, in one way, say that the entire capacity is for EV.

7…In our industry, about 80% of the average capacity utilization that you can expect.

8…Shifting

=We are not shifting machining facility from Aurangabad to Hyderabad, we are shifting the

lamination from Hyderabad to Aurangabad and focusing on machining in Hyderabad. So, the

existing facilities, which are required for the lamination related operations of machining, like

shaft, will continue in Aurangabad. Where the lamination is required for machining, that will

come to Hyderabad. So, the shaft we wound not be transferring it from Aurangabad to

Hyderabad. Only the lamination, which is required in machining will get transferred from

Aurangabad to Hyderabad.

9…Working capital

=we are continuing to improve our working capital cycles and

we have already got it down to 96 days for the full year and we expect this to continue to go

downwards towards 75 days and even eventually further down to 60 days.

=This is driven from both the debtor days reduction as well as inventory days reduction. As we

continue to reduce our dependency on imported materials, we will be able to reduce our

inventory days as well. So, there you will not actually see any hit on margins.

10…Margin improvement

A=Value added products

If you take the products of the company, the simplest product that you make is a loose sheet

metal lamination. Now, obviously over there, your margins are going to be much lower and the

most value-added product that you make is a fully core-dropped stator frame and a fully

assembled ready-to-use rotor where the shaft is attached, the copper is put in by us. So, the value

add on the final, I am just giving you the two extremes. So, as you improve the product mix,

from just plain vanilla laminations to assembled and then in assembled also more value add as

you keep doing, your margin per ton will keep on increasing.

…The demand is for the more value-added kind of products.

B= Economy of scale

Second reason where your

margins will improve is that you have invested for 72,000 tons of capacity and you have scaled

up your operations as such. So, once your utilization factors go to 80% on 72,000 tons,

obviously, economies of scale kick in.

C=Automation

And the third one is automation. So, we are heavily focused

on automation. I would invite you to our Aurangabad facility to have a look at the kind of automation that we have already done, that will simplify and explain to you what kind of margin

improvement can take place due to automation. Just to put in perspective

11…Market size

=firstly let’s take the market size and opportunity in India. The stated market size for this

product in India is about 500,000 tons. We are at mere 32,000 tons. We are not even 10% of the

market. We are the largest, but we are not anywhere close to even 10% of the current demand.

As India grows, this product demand and requirement will increase. As you adopt EV, as you

adopt green power, the requirement for these products will increase and we see that even if we

can target to maintain our existing market share or even improve it slightly, we have great

opportunities of growth in the existing products.

12…Unorganised segment

I think about half the market is still coming from the

unorganized segment and as more and more people start buying from the organized, it will

definitely lead to more opportunities for us.

=Company’s products find application in basic capital goods, such as motors and alternators, which are themselves quintessentially used in any process engineering.

=It is in the business of producing A…Sheet Metal(electrical steel laminations)

B…Die-cast Rotors & Assemblies, C…Stator Core Assemblies,

D…press tools

E… Machined Components for varied industries including

F…Fabricated Machined Components,

2…Industrial

=steel,cement,sugar

(Special-Purpose Motors, which can be deemed as a proxy for

steel, cement, sugar, and other infrastructure related business, )

=pumps

3…Power generation

(hydro,thermal,wind)

4…DG set(Generator) for ups

=Data centre

=5G

=hodpitals

=Residential and commercial spaces

5…Appliances

Products

1 …Sheet metal

2…Machining

3…Tooling

4…Shaft manufact.

…HIGH PRECISION MACHINING OF LARGE METAL COMPONENTS

2…2018@Aurangabad@226 cr @Machining and laminations

… The mega plant at

Aurangabad is proposed to be completed in two phases- Phase 1 and Phase 2

… Phase 1 has been successfully completed with a

total cost of Rs. 226.00 crore.

= PEL is eligible for receiving a re-imbursement in the form of subsidy from Government of

Maharashtra for its Aurangabad plant for investment towards Phase 1 over a period of 7 years and has received Rs. 16.54 crore

in the form of investment subsidy in FY21.

3…220 cr capex @will completed by 2024 @machining and laminations

=Under this expansion plan, we will

A… integrate our existing supply chain by setting up additional facilities for those components/processes which are currently being outsourced.

B…We are also going to add dedicated manufacturing lines/units for new applications segments

where we have made significant

inroads and are expecting sizeable

future business.

= These include

…railway undercarriages

…components for EV

(Electric Vehicle) motors,

…drivetrain systems, gear cases

, …unique engineered product solutions for wind turbine

applications,

…and medium and heavy

fabricated machined components

C… Post expansion, we would have added new technologies/ engineering applications such as

… high pressure green sand moulding,

…medium and heavy fabrication,

…very large five axis machining

capabilities and assembly facilities

for various unique products that find

applications in power generation, drive systems, motors, off highway vehicles among others.

=2022

we have completed 35% of the envisaged capex and remaining is on track for timely completion

=During the last one year our capacity has grown from 36,000 metric tonnes per annum to 41,000 metric tonnes per annum

=At the end of this capex cycle, our capacity will be 72,000 metric tonnes per annum (from existing 36,000 metric tonnes per annum

=At the end of FY24,

the machining capacity would double from its existing 350,000

machine hours to 700,000 machine hours.

=With the constant price, the revenue potential at the end of this capex cycle for the company shall be 1,800 Crores

=Capex Entirely is Brownfield, the facility that we already have in Aurangabad factory, we have

additional land available adjacent to it which is equal to two time the land that is already being developed so it will be coming up right in the same campus.

…

MOAT

1…ECONOMY OF SCALE

=With expanded capacity ,we have lower cost of manufacturing because of fix cost of sallary and asset

…India’s largest laminations manufacturer

…One of the few suppliers in the

world with tooling, laminations,

casting and machining

capabilities under one roof

…Largest exporter of electrical

laminations from India

…Leading supplier to to all motor

manufacturers in India

…Pioneer & Market Leader of assemblies for large

alternators & motors in india

…Pioneer

.The company is a pioneer in

the manufacture of traction motor sub-assemblies in India

2…ENTRY BARRIER-5000 different products

.

=There is a huge entry barrier, if what we talk of high level numbers if we go to the micro level we are more than 5,000 different products developed all of which are active for the

client, to compete with me some new entrant had to develop all the 5,000 products in one shot which is practically impossible which is the development of the last 30 years of

products so to this we are developing inventory of 5,000 products and every year we add at least 5 to 10 new products to our library.

3…ENTRY BARRIER-.FORWARD AND BACKWARD INTEGRATION

(Three different industries)

=It is one of the few suppliers with tooling, laminations,

casting and machining, all under one roof

=We are India’s only end-to-end product and service provider in the electrical laminations segment with strong presence in

tooling, casting, lamination and machining.

=The integrated presence helps us maintain

A…complete control of the product quality,

B…ensure value at all stages of production and

C…provide great comfort to our clients in terms of

dealing with multiple suppliers.

D… This integrated presence helps our customers depend on us

=The kind of product we operate it is

very difficult for a new entrant to come in, we compete with three different industries, we

have a combination of three different industries, we have changed the way our end customers do business

A…Traditional sheet metal

.so we started our traditional sheet metal company hence we always

talk in per tonne basis or per tonne capacity,

B… .Fabrication

but we have moved well beyond that, we have a fabrication facilities,

C…Tooling and machining

=we have our own tool room, we have our own machine shop,

D…Shaft

we have our own shaft manufacturing facility

= To replace us in the supply chain, first and foremost my competitor needs to find three to four different companies each in a different

field and then find someone to integrate the product, assemble and supply it as a ready to

use unit, so in terms of capabilities we have a unique product

=Competition risk: Emergence of a large number of competitors trying

for the same business can heighten competition risk which often leads

to revenue and margin erosion.

Pitti Engineering, by successful pursuit of a number of forward and backward linkages, has emerged as a highly unique vertically integrated player in significantly higher value added solutions. Consequently, the company has not only insulated it from standalone competitors across the highly staggered value chain, but also, in the process, developed such stickiness that even fiercely competing customers would come to it, directly or indirectly, for its impeccable

customer value proposition.

=The competitive advantage provided by in house facility for integrated

end to end manufacturing processes including machining, assembly,

fabrication, casting along with an established large supply chain for

procurement of massive list of components required for assembly and sub assembly purposes, imparts higher value addition to the products.

This one stop shop characteristic of PITTI makes it invincible for its

downstream customers for their supply chain requirements.

4…PRODUCT DIVERSIFICATION

=Leveraging our strong engineering skillset, we have expanded into more value-added product lines which provide us with a new

revenue stream and decreases the impact of business cyclicality.

A=Our operations range from tooling and laminations to castings and

machining, leading to extensive value addition and providing one-stop

customer solutions.

B=Our wide range of products from 50 mm to 1,250 mm single piece electrical steel laminations allows us to cater to niche customer requirements – diversifying revenue streams and de-risking the business from single product dependence

6…INCUBATION PERIOD @4 to 5 yrs for one product

=.It will take 4 to 5 yrs for single product from vendor regestration to ready to use product for any new competitior…

=Most of our customers will take at least two years to get a vendor for registration done, post that

development of one single product would take at least a year-and-a-half at the supplier end, then

the approval of the product supply to the customer it will go to a life cycle which would typically

take 6 to 9 months and then you would have the first pilot of supply and then the commercial

supply, so I would say about 4 to 5 year timeline for anyone to come in and then after that only the

other products would be offered to a competitor, and then again the similar timeline would be

there to develop the rest of the product portfolio.

7…Strong relationship

It is due to

=timely supply of

=Quality products at

=competitive price

=Crompton and Siemens are with us for over 22 years, whereas Cummins and ABB are our clients for 17 years

=.At Pitti Laminations, we are catering to evolving requirements of customers through developing better products and processes, focusing on quality parameters consistently, implementing best-in-class technology and sustaining price competitiveness.

=Relationship that we have with them is more like a partner rather than a supplier so we are very happy doing this for them, if they want us to

further go up the value chain and give them a ready motors we have more than willing to do

that, but going and competing with them is something that I would not want to do.

8…Margin

=Margin improvement

A=Value added products

If you take the products of the company, the simplest product that you make is a loose sheet

metal lamination. Now, obviously over there, your margins are going to be much lower and the

most value-added product that you make is a fully core-dropped stator frame and a fully

assembled ready-to-use rotor where the shaft is attached, the copper is put in by us. So, the value

add on the final, I am just giving you the two extremes. So, as you improve the product mix,

from just plain vanilla laminations to assembled and then in assembled also more value add as

you keep doing, your margin per ton will keep on increasing.

…The demand is for the more value-added kind of products.

B= Economy of scale

Second reason where your

margins will improve is that you have invested for 72,000 tons of capacity and you have scaled

up your operations as such. So, once your utilization factors go to 80% on 72,000 tons,

obviously, economies of scale kick in.

C=Automation

And the third one is automation. So, we are heavily focused

on automation. I would invite you to our Aurangabad facility to have a look at the kind of automation that we have already done, that will simplify and explain to you what kind of margin

improvement can take place due to automation.

=Our margins will not improve because commodities have

moved, either up or down. They do not improved or deteriorate

because of that. Both raw material as well as scrap, so the net raw material cost increase or decrease in the raw material cost is completely passed on to the customer, increase or decrease.

= We are chasing both the lower EBITDA margin per ton business as

well as the higher EBITDA margin per ton business. It’s not like we are

only focused on the higher ones. So, the lower ones would be your

consumer durables, EV because there the value add and the scales are

very different. So, the EV would be more like an auto ancillary kind of

business, not like a discrete engineering manufacturing kind of

business. We are also targeting increases in Indian Railways as well as other locomotive and Metro related businesses, which typically come

at a significantly better EBITDA margin per tonne. So, when you go to

60,000, the above impact of high and low EBIDTA contributing

products should even out and we should see around 42,000 EBITDA

per tonne.

9…Sole supplier

…In most of the products that we make which are intermediatory products which go into the final

product that our customers make, we are sole suppler in most of the places that we operate

10…BUSINESS GROWTH STRATEGY

Our twin-focus remains on

A… higher value addition in our products and

B…diversification of application

segments and geographies by developing new products. We

are intensifying our new product

development activities through

prototyping, pilot batching and

subsequent scale up

=Operating margin expansion and sales realization from higher value addition and new product development

=As part of our larger vision, we continue to focus on remodelling our strategic framework that focuses on building a differentiated product by understanding the needs of the customers and adding value to our product thus creating a new market for the same

C…Not pricing power

Our customers are solely dependent on us, but we are also depending on them right, in the industry

they are the giants, there is GE, there is Simens etc then we will have a comment you cannot

name a fixed customers so in this industry if I have a monopolistic position or a pricing

power if I exercise it I am going to start firing relation so you know it is more of a partnership, these clients are be with us for 30 years and we have grown with them, so you

know using the word monopolistic is not good with these kind of relationship.

11…CYCLICITY

Leveraging our strong engineering skillset, we have expanded into more value-added product lines which provide us diversification with a new

revenue stream and decreases the impact of business cyclicality.

=As new segments /industries are added,we are less dependant on perticular industry

and so less vilnerable to cyclicity

Diversification is due to

X=Our operations range from tooling and laminations to castings and

machining, leading to extensive value addition and providing one-stop

customer solutions.

Y=Our wide range of products from 50 mm to 1,250 mm single piece electrical steel laminations allows us to cater to niche customer requirements – diversifying revenue streams and de-risking the business from single product dependence

…

Negative

1…Customer concentration

=Top five would contribute about 60% to 65% of revenue.They would be Siemens, Wabtec, they would be ABB, they would be Cummins and the fifth number keeps changing on and off sometimes it is Toshiba, sometimes it is Crompton, so the fifth number keeps changing but top four always remain constant, Siemens, ABB, Cummins and Wabtec.

2…D/E RATIO

2021@1.27

2020@1.09

2019 @1.29

2018@1.53

=It will come down because we will

have the repayments of the previous debts. So, close to Rs. 40 crore

debt is up for repayment in the next 12 months. Whereas, if you see, I

said that we are going to add about Rs. 120 crore to 150 crore of

CAPEX, over the next year, with 1:2 debt equity. So, about Rs. 80 crore

of total debt will get added, Rs. 40 crore will get repaid. So, the net

position will be about Rs. 40 crore. Then for the subsequent year we

have Rs. 70 crore of CAPEX for FY24, again at 1:2 debt equity you

know, you are adding maybe over Rs. 25 crore or Rs. 30 crore of debt.

And again you will have a huge repayment. So, your debt will peak

out. It is only to tide over the timing.

3…pledge(20% of promo holding )

=Pledge is to the bankers of Pitti Engineering, and not something I would have like to do, it is

stipulation(order) from the bank, SBI have the stipulation that a percentage of the promoter holding

is pledged to it and I am only complying with the covenants of the loan agreements, if you

become debt free, yes, definitely all the pledges will be removed

…High working capital days

=The company continues to be working on reducing the operating cycle. Working capital cycle as on September 30, 2021 stands at 99 days.

=We have set ourselves a target of reducing this to 75 days within the following year.

=it’s already down to from 97 to 92, so some improvement is there,

when I say stable it is still some improvement. And we are working on

it. And it will take time, see it will not happen overnight. So, we are

fully committed to bringing it down.

=Our long term target is to have debtor days down to 45 and the total working capital down

to 60 days.

5…Economic risk:

Capital goods sector is inextricably linked with the overall economic, infrastructural and industrial growth of any country/region.

6…RPT

=The relationship with Pitti Casting is that we buy these castings

that are used in our machining business as well as the value add

business from them. They are the approved supplier from our end

clientele for many of the parts that we machine and sell. As far as

merging these two companies are concerned, subject to Board

approval I am pretty much open to merging it subject to regulatory

permission and Board clearance.

=Pitti Electrical Equipment and Components are our holding

company, promoter holding companies. So, I don’t see any merger

possibility with them

=only entity which has other business is Pitti Castings

…

FUTURE GROWTH

1…Aurangabad plant

PEL has two plants at Hyderabad and one plant at Aurangabad. The Aurangabad plant started its operations in January 2018, after the facilities from Hyderabad were partially shifted to Aurangabad. This shift to Maharashtra brings the Company in proximity to its customers as well as raw material sources.

=The reason that we have setup the facility in Aurangabad is

A… highest concentration

of our domestic client based is Maharashtra

So reduced logistic cost

B…Near to raw material supplier

So reduced operating cost

C…Besides, advanced manufacturing features like robotics, automation and IoT, integrated sheet metal, machining and assembly operations have helped improve efficiency and remove redundancies

=Plant shifting will supposedly reduce the Company’s logistics and operational cost to a significant extent, making its operations more competitive.

2 …Last 5 yrs(2016/2020)Growth strategy with capex of 230cr

=Last 5 yrs change in business from commodity to value added

=Major chunk of our output comes from a fully assembled and ready to use product rather than loose laminations so that is the change that we have driven in the past 5 years which makes us indispensable as well as increases our margins.

=2017-18 was a transition year, in which we streamlined and strengthened our portfolio and operations(2018 AR)

A– Exit

=Exited our labour-intensive facility in Plant 1, Hyderabad

B–Aurangabad plant

=Commenced operations at fully

owned state-of-the-art Aurangabad

facility with automation and robotics with reduced operating and logistic cost

C– Hyderabad plant 4

=Commenced commercial production at new facility in Hyderabad for

high‑precision machining on large

metal components. The expanded

machine shop will also help in meeting GE and Alstom railway orders

D– Integration

=Progressed in terms of developing as an integrated player

=Having successfully brought together such a compelling combination – tooling, lamination, machining, assembly – we started exploring the new applications segments and customers that would like to benefit from our vertically integrated capabilities.

E–New segments and new customers

=We reached out to more

than a dozen new application segments, showcasing our capabilities and learning the pain points of these newly engaged customers.

3…New products

=Going forward the product profile will increase and go towards more high value added products.

A=Fabrication

=With the objective of increasing product portfolio for its existing customers,

the Company has capitalised on its capex additions to enter into fabrication of Truck Frames, which is the under carriage of railway engines, to supply for the domestic operations of one of its prestigious international customers.

The success in this new product is expected to unlock new market

opportunities in International and domestic markets as there exists huge

untapped opportunities with Indian Railways for the product.

B=Shaft

=22.50 crore Investment in new

product line- shaft manufacturing

=In line with the strategy to move high up along the procurement value chain

of its downstream customers, the company has begun supplying shaft inserted rotors by manufacturing shaft in house, thereby facilitating unique

positioning of PITTI in the supply chain of this product for its customers.

4…New promising sectors(>50%rev)

= It is encouraging to see emerging

segments like

=power systems for data farms,

= electric vehicles,

=Railway n metro for mass

urban transit systems,

= renewable energy

segments starting to make sizeable

contributions to our order book now.

=Appliances

=Till about a decade ago, all our

supplies were headed towards

DG sets and various industrial

drives.

=Thanks to our thoughtful expansion of business offerings and

diversification of user segments,

more than 50% of our revenues come

from newer segments today

4.A…EV

=The stator and rotor that we supply do find application in EV and we are in active discussion with a couple of end users to develop these products, we should be able to you

know state something more explicitly in the next 6 to 8 months.

=It’s more of an

exploratory product that we are developing for a very reputed two wheeler manufacturer, for their EV application. If successful, it has a

tremendous revenue potential, which I cannot quantify as of now.

= All these applications put together have a revenue potential to add about 45 Crores of top-line per year going forward

=• The Company has received LOI for supply of stator and rotors

from two reputed customers manufacturing for e-bicycles and

2 wheelers in the EV space.

=My view on the sector would be that it’s an emerging sector. So, any

potential number is always thought with little bit of risk. But also, at

the same time, I would say that this is a fast growing sector. So, any

numbers that we are seeing today can increase exponentially in year’s time as well. It all depends on how quickly the country adopts

and accepts electric vehicles and E-mobility

4B…Renewable energy

=I am pleased to report that the company is gradually making its foray in sunrise sectors such as the renewable energy space.

=We have collaborated with a Germany based wind firm for the supply of windmill

pedestals and bearing flange for its project in India.

=Along with it, we have received new

orders for steam turbines and hydel pump parts for hydro power generation.(Govt has apptoved hydro power as renewanle energy)

4C…Data centre and dg sets

=Data power systems if you see we have started to give a separate line item in our presentation, we see huge demand coming from this segment, apart from that the

=Data centres have become reality in the last two to three years with a current capacity at 600 megawatt and plans are a foot to add another 2,500 megawatt by FY26, which is a fourfold increase from the current capacity.

=Pitti Engineering is in the manufacturing of components for generator sets for data centres and have been supplying to Cummins India for the last three years and the company is witnessing cumulative volumes of orders on a month on month basis.

=Data centers require 24x7 power availability and must therefore employ backup generators and multiple data routes to ensure Uninterrupted Power Supply (UPS). This is true no matter the physical location of the center, but is especially the case when the data center is located in a country or area where power supply is known to be unreliable.

=For Pitti Engineering’s generator set segment is going to contribute a large chunk of business as the demand is increasing to provide access of uninterrupted power supply for crucial applications like data centers, hospitals, 5G Network, high rise residential and commercial complexes

4D…5G and dg set

=Cummins management and analysts believe that the 5G networks require generators to sustain base stations and towers which CIL can produce and export in large numbers. The fact that China and Japan do not produce the kind of generators needed to power these towers means CIL has the potential to win large orders, they say.Cuminis is customer of pitti

=We estimate the additional 5G opportunity at Rs 200 crore per annum for Cummins India on an annual basis and growing over the next five years

4E…Hospital and dg set

The importance of uninterrupted power supply in hospitals

can be gauged from the potential cost measured not just in

economic terms but higher cost of patient well-being. The

potential demand for quality DG sets in hospital industry can be

estimated by considering the hospital beds in India

4F…Railways and metro

=With the implementation of the National Railway Plan, the Railway sector also presents significant scope for growth.

=Today in terms of railways, railways I would say including metros because that is how we

account for it, 28% of our business comes from railways, going forward we see this

business increasing by 25% to 30% in the next two years.

4G…pump

New infrastructure development has also created new demands in the

pump industry along with replacement demand. The company has

proactively increased capex to boost its capabilities to cater to the rising

demand even as the Company is prepared for adapting to the changing

efficiency norms.

=Industrial pumps are witnessing a high demand from cement, steel, oil & gas, water & wastewater sectors

4H…Appliances market

=A small, yet key addition to our

user segment was consumer

electricals - where we started

supplying lamination assemblies

for fans.

=The Company’s capacity expansion program to modernise its press

shop with high-speed presses is in line with the objective to enter the

high-volume appliance market, which is transitioning towards organised

sector for fulfilling its procurement requirements. The shift, driven partly

by withdrawal of many players from the unorganised sector in the post

pandemic scenario along with changing efficiency norms and rising quality awareness amongst the end consumers, is forcing appliance manufacturers

to source components from established players in the industry.

5…China plus

=we always had better price parities than China so much of our

products were indirectly exported back to China, so in terms of competitiveness we have

always been competitive,

= in terms of demand environment, yes, we are seeing a definite

shift wherein now this China Plus One policy at the global sourcing level and more and

more global sourcing is getting diversified to safeguard against any geographical and

political risk.

…

POSITIVES

1…Promoters increased their stake @ 90 per share:

=The Company allotted 22,22,222 convertible warrants at a price of INR 90/- on preferential basis to the persons belonging to Promoter/ Promoter Group on 14th February 2018. The same were converted into fully paid-up equity shares on 24th June 2019

2…Started its operations in 1983

Experienced promoters

3…Reputed clienteles

=Top five would contribute about 60% to 65% of revenue.They would be Siemens, Wabtec, they would be ABB, they would be Cummins and the fifth number keeps changing on and off sometimes it is Toshiba, sometimes it is Crompton, so the fifth number keeps changing but top four always remain constant, Siemens, ABB, Cummins and Wabtec.

=In the laminations segment our domestic clients include ABB, Andritz, Alstom, BHEL, Crompton Greaves, Cummins, L&T MHI, ReGen Powertech, SE Electricals, Siemens, TDPS and Voith, among others. Around 36% of our domestic revenues are derived from existing relationships with long-lasting clients (Crompton and Siemens are with us for over 22 years, whereas Cummins and ABB are our clients for 17 years

If raw material cost stabilize, co aims for an approx 1800 crore revenue (based on the assumption of 50000 tonne capacity with a blended sale utilization of the current Rs 3.55L per tonne).

Cash discounts provided to improve WC cycle and thereby increasing the ROCE. Expect WC cycle days to come down to 70 this fiscal and eventually to 60. Current WC days around high 90s.

With CAPEX planned, peak debt to be around 360 crores. Railways is the key customer.

EBITDA per tonne would be around Rs.40000 but expect to improve to Rs.45000

At a current EBITDA multiple of around 9, would be interesting to watch the company’s execution plans

That is some significant forward looking growth in revenue! They closed out FY22 with ~ 950 cr.

I am of the view that the electrical steel laminations space in India is highly fragmented, and there’s a huge opportunity available for a company with great capital allocation and execution skills to grow rapidly, both organically or through M&A.

• Though anecdotal, while travelling through the industrial belt of Tamil Nadu and Karnataka, I have noticed many small industrial units that sell electrical steel laminations.

• As this domain becomes more consolidated, there are going to be a lot of eyeballs on it, and Pitti Engineering (which I am assuming is the only listed player) has the opportunity to benefit greatly from this.

Thank you so much @Pragnesh for your detailed thesis on this company, as well as the concall notes.

I really like how the company is leaning increasingly towards fully assembled/value-added products, instead of supplying “raw” electric steel laminations. It’s a significant forward integration and margin expansion opportunity.

Additionally, I like how the company is eligible for and is receiving multiple government incentives.

Finally, it’s no small feat to set up another company like this in India. The barriers to entry are significant.

During the September quarter, the public shareholding has gone down (39.8 to 37.77%), as LIC large and Midcap mutual fund has picked up 1.99 percent stake.

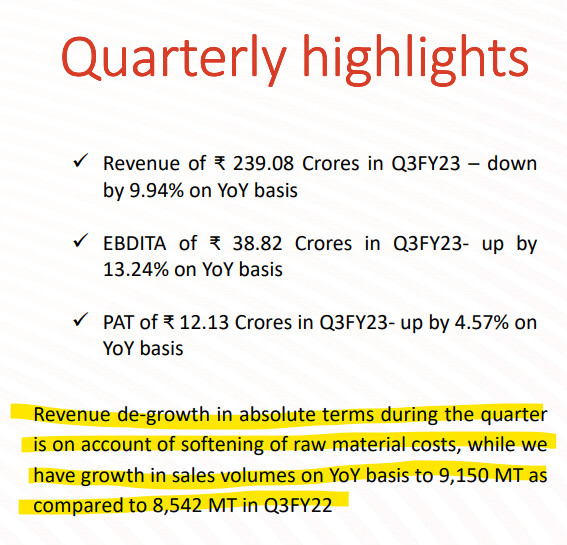

Annual results for FY 23 are as per expectations. Q4 of FY 23 has been good, with quarterly EPS of 7.75 rupees. Final dividend of Rs 1.2 has been declared by the company. AGM is scheduled for 18th of August. Better times seem to be ahead for the company.

Pitti Engineering: Q4FY23 Concall Notes:

• Capacity Utilisation - 74%, industry std is 80% because machines need maintenance and if you push beyond 80%, machines deteriorate rapidly.

• Blended EBITDA/tonne - INR 42,290

• Net Debt - 225cr earlier 290cr

• Guidance: EBITDA/Tonne to be 45k in coming quarters at full utilization after capex or machine setup is done (not mentioned the quarter)

• Working capital days may not improve any more here on. About 75days. Debtors and Payable days will be same.

• Traction motor and railway components business will outperform in FY24. Power gen and renewable energy will see very good growth.

• Installation of new machines is expected to be done in Q3 and completion will be done by year end.

• Capex: Hyderabad is going through modernization capex and the lamination facility will be moved from there to Aurangabad and machining capacity will be installed there. After that there will be a pause on capex.

• Export: North and South America are the two leading regions and contribute 75-80% of exports sale. Remaining 20-25% goes to central Asia.

• Debt: Net debt should rise modestly after the capex is done, but after that it will come down significantly over the next two years.

• Order book: Order books are created for two quarters as steel prices changes frequently. Out of the total order book, 200cr is executable beyond 1 year. Order book fluctuates as customers don’t give orders beyond 2 quarters except for some indstries like Power Gen, windmill, exports where order book is for 6-9 months. Also, steel pricing volatility fluctuates the order book value.

• Capacities are and will be setup based on the customer forecast for next 2 years.

• Top 5 clients contribute 60% of the sales.

• Export order book is booming. Never seen this kind of traction in the exports. Majority of our exports go towards North and South American railways and mining. Both of these segments in those regions are going through transformation, modernisation, and upgradation. So for the next few years, we see quite strong order flows from our export lines.

• Export products are very high value added products and more machined, so exports contributes disproportionately to profitability.

• 1800cr of topline can be achieved at full capacity utilisation after new capacity comes online (this fig may change based on the steel price, so 72000tons (58000 at 80% capacity) will be the max volume. It should max out by FY25-26. For machining, where margins are high, 6.5lakh hours are max capacity and this should be maxed out by FY25.

Future Business Growth Triggers from different sectors: Vande Bharat:

○ Getting orders from 6-7 players who supply to Vande Bharat as well. In the final stages of approvals to supply machine components. Commercial supply is coming from only one players as of now, as rest others are in proto and development phase.

○ Each train requires 32 motors and each motor needs half a ton of lamination. So total 16 ton of lamination for each train. For machining, there is a whole variety of components where they are getting approved. Windmill:

○ In Windmill, Pitti makes the generator part where stator and rotor is needed. Main customer is Siemens Gamesa. Pitti also does the machine components like pedestals, to keep the fan rotor and gen rotor aligned.

• Pump Hydro:

○ Two projects going on here. Greenko and JSW. EV:

○ EV related products are in commercial supply with a couple of customers, rest are in the development phase.

○ This line of business can grow 25-30x in next 2-3 years because the base is so low. Last year company did, 1-2 crs for this segment and can do 25-30cr of revenue from here alone on one order, if they get two orders, it would be 40-50crs. This will happen when customers start making their own motors rather than importing it.

Opportunities in Future/Growth drivers

• Machine components business including fabricated, cast parts.

• Growth and modernization of the railways in India and North and South America. There are adjacencies here as well.

• Capex cycle

This should drive growth for next 3-5 years

• Pitti has 8% of the market share and the industry is currently fragmented. Next competitor is half the size of Pitti.

• Vision is to become a integrated player for all the motor related components such as lamination, machining, shafts.

• Company aims to grow revenue 7-8x in next 10years

After this proposed transaction promoter holding will go up to 61.89 from 59.29.

2.6 % equity dilution for a 13 cr EBITA company

Looks like merger is very attractive

please share your views

@Meet_kus. thanks for the great analysis. You have invested lot of time to do the research. can you tell me, what is Pittis position among competitors. It is not a market leader, and what is the moat for Pitti? What makes pitti a good investment over its competitors in your opinion.