Hi there, thanks for your kind words! I am glad you found my notes helpful.

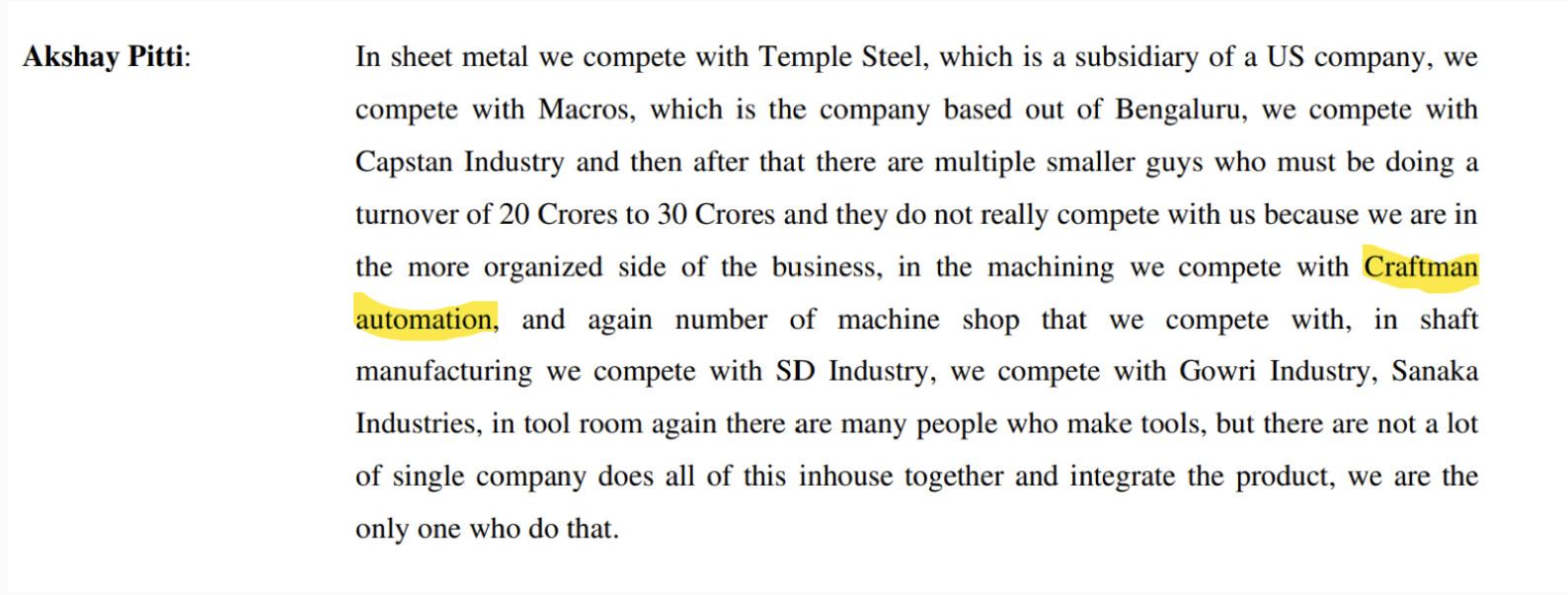

This industry is highly fragmented, but Pitti is indeed a market leader in the organized lamination and machining. Currently, they have 8% market share as the management notified in the last concall, but they aspire to take it to 10-12% in coming years as they add more capacity (72000 tonne max volume, total market size is 500,000 tonne). Pitti competes with a lot of player in a few parts of the value chain (like sheet metal, machining, tool shop), but according to the management, no competitor does the complete value addition. Next competitor is half the size of Pitti. Please refer to the following concall snippet for understanding the competitive landscape.

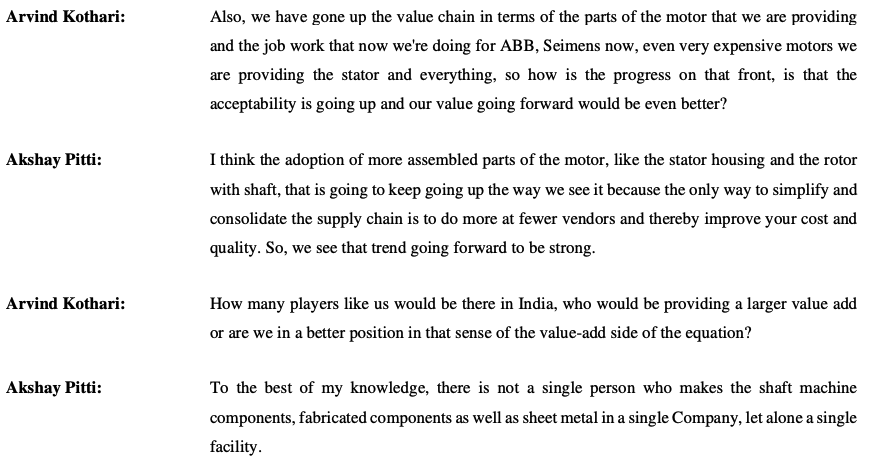

Management also claims that is there is not a single facility in India that makes shaft machine components, fabricated components and sheet metal (value chain of the motor assy). Trend is customers are moving towards suppliers that are moving up the value chain like Pitti because they want to simplify and consolidate the supply chain.

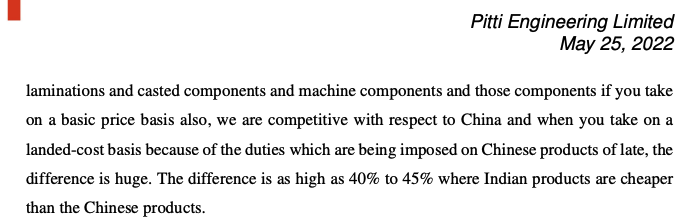

Management also says that lamination and casted components used in motors made in India are 40-45% cheaper than China

Tempel Steel: Second largest in India (18000 tons current capacity in FY23)

Magcore, Capston: All in the range of 8000-10000 tons.

As far as the moats are concerned, Pitti management claims to have the following competitive advantages:

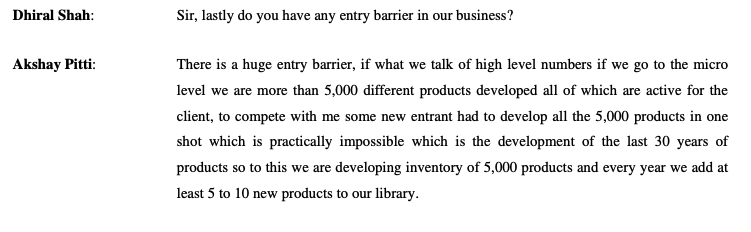

High library of products used in the value chain. Company claims to have 5000 products active for the clients and adding 5-10 new products every year. Any new entrant has to develop 5000 or more products to keep up.

Company has their own tool shop, their machine shop, mfg facility. One stop shop for all the operations to create finished goods. This helps in achieving good quality, better cost, less issues with dealing multiple vendors for the clients. A new player has to do all the value chain operations under one roof which is quite cost intensive.

Economies of scale: All other players are pretty small in terms of volume. Second player is at 18k tons capacity while Pitti is at 32000, planning to go to 58k (80% of 72k tonne volume)

Hope this helps!

Disc: Invested, so I have vested interest in this company.

One of the cap good stock that has not gone insane in valuation in this bull market , even though have appreciated a lot …

it is a tier 3 company, [but a market leader in its segment] with absolutely no pricing power …

Till the time cap goods sector grows ( siemens, abb etc) , this should grow fine… Fy25 should be a big one in earnings considering capex completion in fy24… but not sure on way forward beyond that

being a cyclical … i cannot invest beyond 10% … When to get rid of this (AT the peak) is the real challenge

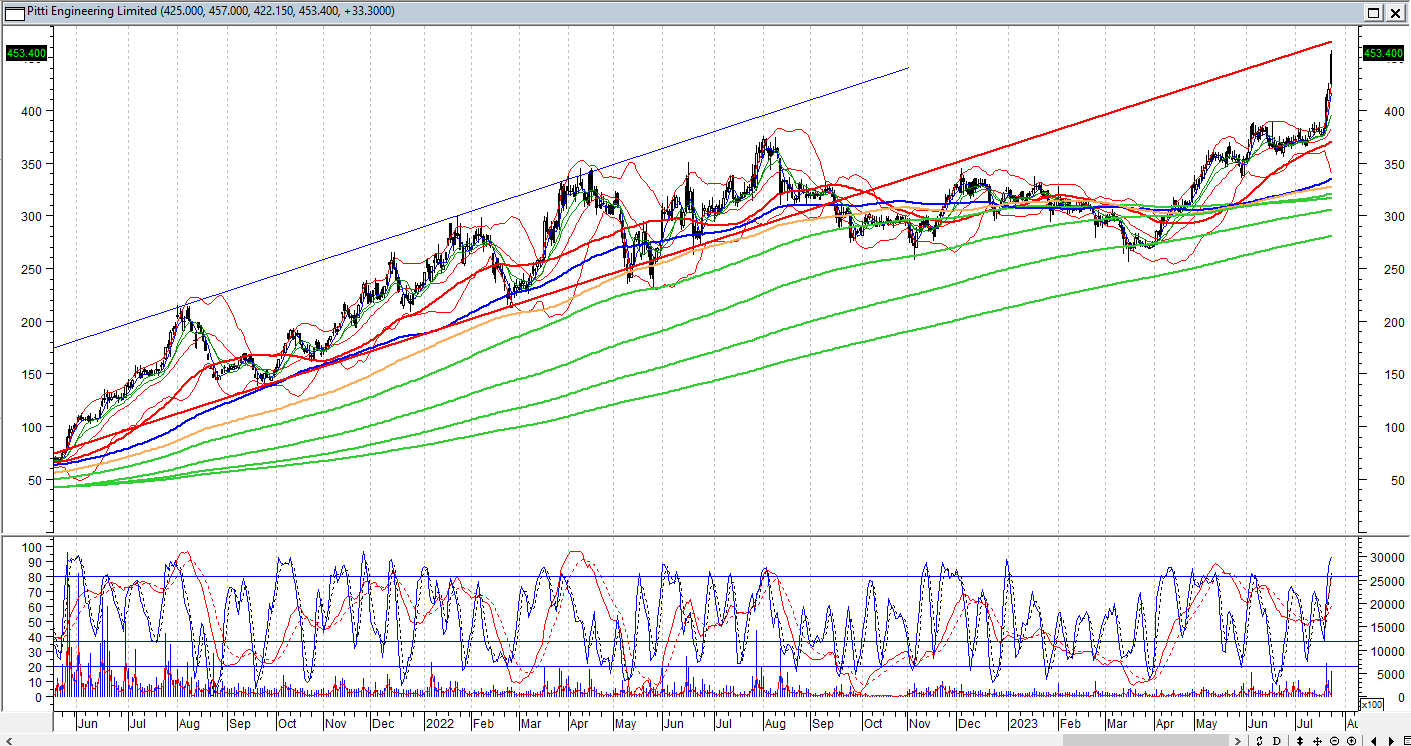

Two-year NSE daily chart of Pitti Engineering Limited.

From May 2021 to Aug 2022, the price moved in an upward channel. Now the lower band of that channel (if extended) will act as resistance. So the current rise is likely to face resistance at 460-470 levels. If that level is breached from below, the price may again move in the same channel. Real rise will come, if the upper band is also breached.

One thing that I have noticed in Pitti’s concalls is that Chairman Mr. Sharad Pitti is never present in concalls and VC Akshay Pitti answers all the questions. Other senior management personnel are there just sitting, and nothing else. I have very strong opinions about this and feel the company is insulting those senior management leaders by not letting them speak and using them like a showpiece. Would like to get opinions of other members here.

Disclaimer - Invested and re-evaluating the business

Q1 FY24 concall :.

Shouldn’t look at revenue for the Co, as it depends on raw material prices

Ebidta / ton is moving upwards with more share of assembled products

80% of 72000 ton capacity to be used up by FY26

Co. Doesn’t want to make full motor. But looking for opportunities in contract manufacturing

Current Co. Tonnage is 10k ton, q2 would be 11k and there onwards adding 500-600 ton for remaining 2 quarters

Export for renewable to start in q2.

Pitti casting merger to be completed by q1 next FY (fy 25)

Net debt is aroung 280cr, and Working capital is around 70 days

Opportunity for direct export to EU is opening up. Potential of 150-200 cr in next 2 yeras.

Disc : Invested

Not a comprehensive coverage of the concall. Please refer to concall record on company website

The company passes on increase /reduction in raw material prices to customers. So, revenue is Lowe when the raw material price is lower. But Ebidta / ton stays same, irrespective of the Raw material price

Does this imply they don’t have pricing power? Even if they are getting raw material cheap , they can give to clients at constant price. Will improve margins?

Please correct me if I am wrong

This is in fact good. Margins doesn’t fluctuate much, unlike commodity businesses. Anyway company is increasing Ebidta/ ton as the revenue mix changes to more assembled products and also ramping up of Europe revenue in next 2 years

Contract manufacturers do not have pricing power. A case in point is Dixon Technologies Limited. It is a contract manufacturer of televisions, washing machines, smartphones, LED bulbs, battens, downlighters and CCTV security systems for companies such as Samsung, Xiaomi, Panasonic and Philips. It has 17 manufacturing units in India. The PE of the company is over 100.

Management of Pitti Engineering Limited have also consciously decided to keep their margins low and stable. The rise in earnings will be through increase in volume. This is good for the health of the company.

Hi sir,

Is this you?

Just started tracking from my side and found this in shareholding pattern.

The levels you mentioned in this post and the name and levels in SHP are similar. So asking.

Higher machining utilization results in a more value-added product mix, leading to increased EBITDA per tonne.

2. Automation and Labor Efficiency

New capacities are highly automated, reducing labor requirements.

Enhanced automation contributes to EBITDA expansion.

3. Economies of Scale

As the company grows, costs spread over higher tonnage, driving EBITDA expansion.

4. Product Mix Projection

Trending towards more assembled products.

Anticipates assembled products constituting over 80% of sales in the next 2 to 3 years (currently 70-75%).

5. Future of Lamination Business

Loose laminations will remain in the product mix.

Some applications require on-site assembly, and customer preferences also influence the mix.

6. Business Development in EV and Renewable Energy

Engaging with clients for European and North American renewable energy requirements.

Focusing on exports in the renewable energy sector.

Collaboration with automotive clients like Varroc and Dana for ICE and EV components.

Involvement in electric bus, two-wheeler, and three-wheeler components.

7. Merger with Pitti Castings

Papers submitted to stock exchanges and SEBI & Awaiting regulatory approval.

Timeline for completion expected towards the end of the current fiscal year or Q1 FY25.

Components Business Growth Outlook

Post-merger, the company anticipates a top-line revenue of approximately Rs. 300 crore from the components business

This growth target is expected to be achieved by FY25.

Competition and Imports

India typically doesn’t import laminations; however, it imports raw materials, such as electrical steel, from countries like China, Korea, and Japan.

The trend in India is shifting towards localized manufacturing of electrical steel.

Shift Towards Fully Assembled Products

The company envisions moving towards fully assembled products like motors or alternators.

Currently, there are no plans to start such products under the company’s brand, but contract manufacturing opportunities might be explored in the future.

Domestic and Export Mix

Initially expected domestic growth to outpace exports.

Recent order wins in the European market have balanced export sales growth with domestic.

Reduction in raw material prices expected to release working capital despite lower sales in rupees.

Volume Breakup between Aurangabad and Hyderabad

In the current quarter, they expect around 10,500 tonnes.

The distribution between Aurangabad and Hyderabad is expected to remain similar to the previous quarter.

Emerging Market Trends

European market opening up for larger assemblies.

Growth expected in the railway and non-railway machine components business.

Export Opportunities

Predominant opportunities in the marine and wind power sectors.

Indian companies gaining traction as European companies seek alternatives to China.

Potential to ramp up this business to approximately Rs. 150 crores within the next 2 years.

Market Size

Domestic European market size for laminations exceeds 400,000 to 500,000 tonnes per annum.

Exact volume sourced from China not disclosed.

Key segments in the European market include automotive, railways, and electric vehicles (EVs).

Both Indian and Chinese competitors are actively targeting the European market, seeking to provide laminations for various applications.

Current Market Share

Estimated to be approximately 10% of the total Indian market for electrical-motor and generator-related laminations.

Anticipating an increase to around 15% after the completion of CAPEX.

Total steel consumption for electrical-motor and generator-related laminations in India is around 700,000 metric tons.

Company’s consumption accounts for about 70,000 tonnes, or roughly 10% of the market.

Current Market Dynamics

Laminations are utilized across a wide range of applications in Europe, from off-the-shelf motors to specialized industrial components.

Established European brands like CG Power and Bharat Bijlee are presently comfortable importing laminations.

Company’s Strength

The company specializes in traction motor railways and industrial/commercial motors, which are not widely imported into Europe at present.

Initial inroads have been made in power generation and marine applications within the European market.

Competition and Scale

Multiple lamination manufacturers in India are vying for a share of the European market, with differences primarily in terms of scale.

Smaller manufacturers often focus on serving smaller customers and specialized applications, including special-purpose motors and renewables.

Growth Strategy

The company is strategically expanding its focus to encompass smaller industrial consumer applications within Europe.

Recent opportunities within the European market have yielded higher EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) per tonne compared to the company’s overall average.

The company aims to further extend its presence within the European industrial/commercial laminations market, capitalizing on the growing demand.

Value Addition

Current opportunities in Europe involve highly assembled components that incorporate shaft integration and various other machining processes, leading to an elevated EBITDA per tonne.

EBITDA per tonne for these opportunities surpasses the company’s average.

As the company expands into the industrial/commercial laminations market in Europe, it anticipates maintaining a favorable EBITDA per tonne relative to the Indian equivalent.