Rights issue soon

5dd9a48b-8bce-4f09-8b58-cb7c96023dc0.pdf (671.1 KB)

Wow, another googly. What will be the price for this 50, 75 ?

Also, for those hoping for debt levels to go down (like me), nice dreaming, not happening soon.

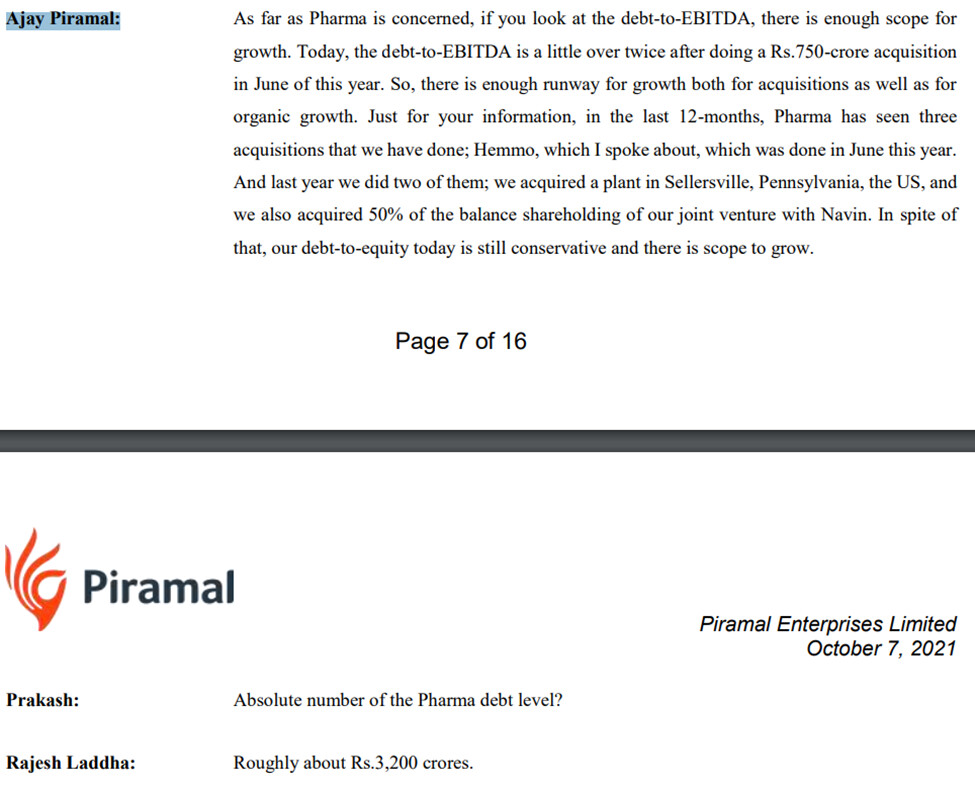

Excerpt from last and only concall:

Sumit Gupta: Last question is if you can provide an outlook on the net debt levels and the interest cost?

Vivek Valsaraj: So, as we’ve guided, Sumit, earlier that our debt levels that we’re looking at about is four to four

and a half times EBITDA, and that’s the level that we should be comfortable standing by.

Sumit Gupta: So this is for FY’23 and '24 or '24 will be less?

Vivek Valsaraj: For FY’24 as well. As we’ve already guided that we’ll be having some growth investments that

we are going to do, so it would be on similar lines, the criteria would apply for FY’24 as well.

Another one:

Ranvir Singh: What level of debt we can expect by the end of FY’23?

Vivek Valsaraj: So, as I said earlier, the max debt that we’re looking for is in the range of four to four and a half

times of EBITDA. That’s where we see ourselves.

Ranvir Singh: In absolute term, currently Rs.4,300 crores debt that we have, so what’s your debt repayment

obligation in next six months?

Vivek Valsaraj: It’s like this, our debt repayment obligations are fairly well diversified, if that’s where your

question is heading towards and it takes into consideration whatever our investment

requirements as well, and our debt levels would be about four to four and a half times EBITDA

that’s where will be.

Seems like the above issue is both for capex and debt servicing ??

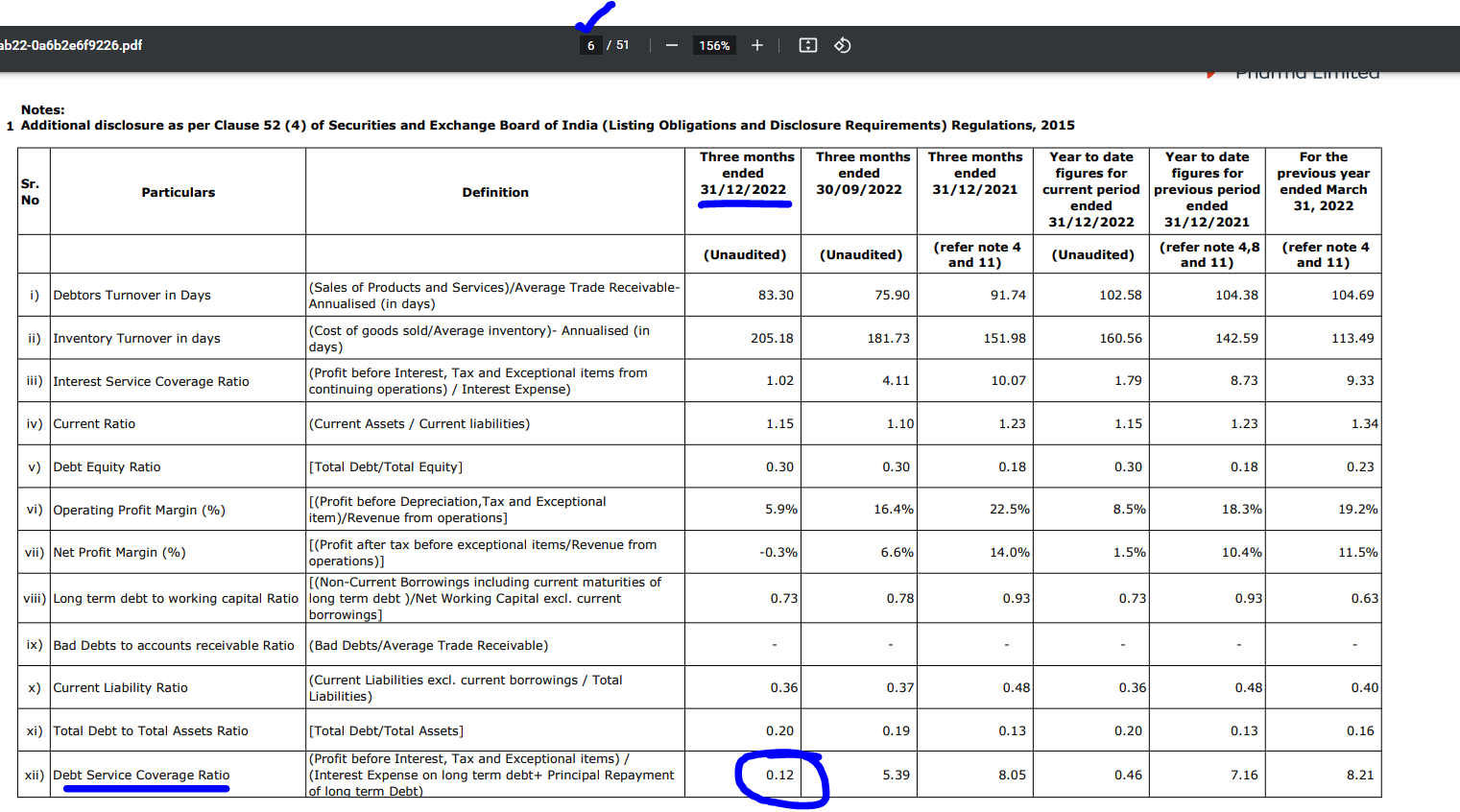

Hitesh Agarwal: If we look at the net debt-to-EBITDA ratio, it is around 4.5 times as mentioned, and you have

guided a CAPEX of around Rs.1,200 crores in the next 18 to 24 months. So, I wanted to know

like, if you could throw more color, how we’ll be able to fund this CAPEX? And second question,

could you elaborate more on the CAPEX spending across different segments?

Vivek Valsaraj: I think in a way responded to the query earlier. As I said, our overall debt schedule which we

have today is fairly well diversified. It does take into consideration of whatever our investment

needs, and also over a period of time internal accruals should be able to be sufficient for

repayment of debt as and when they fall due for repayment. So all of this has been taken into

consideration. My only request is, if you look at the net debt-to-EBITDA ratio as it stands

today… I understand where you’re coming from, but you need to understand that here obviously

has seen some impact. Going forward, we obviously expect these ratios to improve. And

accordingly, the ability to service debt go through a mix of internal accruals as well as being

able to raise debt for the ones that we’ve already retired. That should help take care of the overall

requirements of CAPEX.

LOL.

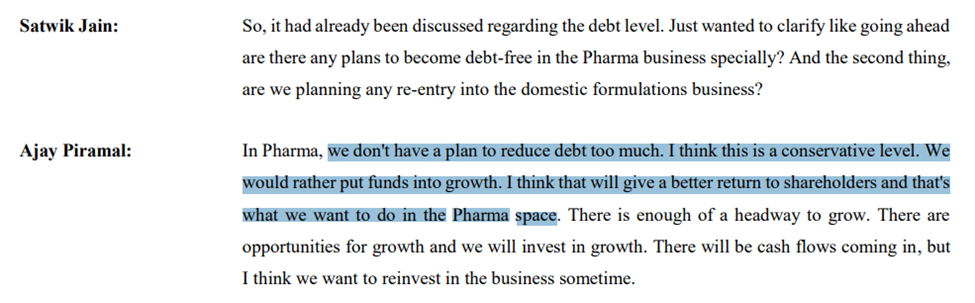

Prakash Agarwal: My question is related to the kind of debt we have today. But, is there a plan to raise further

private equity fund or something like that?

Nandini Piramal: I think right now we’re quite happy that we feel our internal accruals will pay off the debt that

we have and we don’t need to raise additional funds at the moment.

On a funny note , from the movie 3 idiots. Chatur to you: " Hai Himmat toh average down karke dikhao"

Disc: invested since pre demerger and added some in between

5 Likes

The management clearly did not answer the many debt related questions convincingly. For example, as you have pointed out above, even when the questioner specifically asked about absolute debt levels, the management continued with their debt-to-EBIDTA answer. The questions became more and more direct as the call progressed. Eventually, Prakash Agarwal asked if there is a plan to raise further equity funding, Ms. Nandini Piramal said no. After he finished his questions, she quickly called out “…last question please!” even though the allotted one hour was hardly getting over (this is captured in the audio recording around 58th minute but omitted from the written transcript). I found this surprising since at least in the first call after the company got listed as an independent entity, one would expect the management to spend more time than usual answering investor questions and not be so rigid. I had taken a tracking position on the listing day and luckily exited with a small loss after the call. The glossy presentation uploaded in January also is silent on debt, borrowings or funding. But looking at the price fall from Rs.200 to Rs.100, obviously the market knew something like this was coming.

22 Likes

The conference call was on 9th Nov. After that ~3 months have passed. Management has Q3 results and might have already sensed the trajectory for Q4 results.

EBITDA accrual might be way lesser than management’s expectation due to ongoing downward pricing pressure, which was confirmed by Divi’s and Alembic Pharma’s management for the Q3 results, in the US market.

EBITDA/Debt ratio was already stretched. Now, this might be on the verge of violating debt conditions. Hence, the need of additional equity.

In the upcoming call, above is the rationale I expect to hear from the management.

Disc: No investment.

6 Likes

Thanks @Chandragupta @Surender Sir. In all honesty, all I want to hear is why the investors were not told about the debts pre-demerger. Piramal are known to be minor shareholder friendly like the capital distribution strategy incidents of sales etc. but this was really a bummer. I can try to digest the poor performance but not the current behaviour.

Also, above rationale is the only way to raise debt without going to banks but even hearing this from current mgmt would be slightly better.

5 Likes

One of the conference call had details for the same. However, they could have been more explicit in presentations.

Just wondering, how a precise figure of debt would have helped an investor in his/her decision making. IMO, managements thinking on debt keeping EBITDA as reference should be good enough to judge their plan of action.

Debt Amount details:

**No intention to be debt free | IMO, to earn a better ROE on the major business line (CDMO) that is asset intensive.

8 Likes

Results out for Q3 (Link).

Basis management’s view in previous conference call, H2 was expected to be better than H1. However, Q3 of FY23 is worse than Q3 of FY22. All the costs increased more than the revenue increase in % terms.

Brief synopsis:

| Dec-22 | Dec-21 | % Change | |

|---|---|---|---|

| Rev. | 1716 | 1539 | 11.5% |

| Mat. Exp. | 625 | 547 | 14% |

| GPM | 63.5% | 64.5% | |

| Emp. | 492 | 396 | 24% |

| Other | 511 | 370 | 38% |

| EBITDA | 87 | 226 | -62% |

| OPM | 5.1% | 14.7% | |

| Fin. | 95 | 50 | 90% |

| D & A | 164 | 147 | 11.8% |

| Oth. Income | 83 | 161 | -49% |

| Profit of associates | 16 | 9 | 70% |

| PBT | -74 | 199 | -137% |

Confirmation from the Q3 results:

However, chairperson expects investor to believe in the below highlighted reasoning:

Update: 09-Feb-2023 - Conference call Takeaway

- Most questions - about Planned Capex, Growth potential, anticipated performance for Q4 - blocked stating that can not make forward looking statement.

- Why higher other expenses? Includes one time impact (not quantified) due to delay on collection of receivables by few of the CDMO customers.

- Initiative taken to improve revenue growth and various cost items. A very generic answer provided in boilerplate language when probed to share the specifics.

6 Likes

Thanks for sharing above results and key points Sir. As evident from latest ratios, I might have refrained from investing in this if this info was shared earlier. I am still upbeat on the business but balance sheets need to be clean considering this business was not a small scale/newly formed business. I’m yet to go through results (or avoiding at night to limit the day’s frustation ![]() ). Hope we can move on to another kind of discussion other than debt/balance sheet related discussion.

). Hope we can move on to another kind of discussion other than debt/balance sheet related discussion.

2 Likes

The Q3 con call looked very dismal. Management’s most frequent answer was, “We do not want to make a forward-looking statement”. I think the investor community bruises them on call as well on the stock market. I think they were shielded from investors/analysts under PEL inefficacies, and they were free to say whatever they could as there was nothing else to challenge them.

PPL has three business lines- CDMO, India Business, and Complex Hospital Generic. Indian business consists of JV with Allergen, which gives me approx 100 cr PAT per annum. So if PPL report losses on a consolidated basis, that means their core business is not only reporting their profit but also taking profit from JV.

Complex Hospital Generic- It had a good problem (problem, nevertheless). They had some supply chain issues as a result, they could not fulfil the demand. This shall revert in Q4, which is good for the business. So this business shall report good numbers in Q4./ But PPL does not share separate profitability for their different segment, so we will not know the true state until management chooses to say so. But this part of the business seems to be going well.

India’s business is also growing, and they are investing heavily in it. It shall hit 900 cr revenue in FY23 and 1000cr+ revenue in FY24. Management indicated that they would keep investing until the business crosses the 1000cr run rate. It means Fy24- if one wants to trust and believe what management is saying- this segment shall report some tiny profit (currently, it is EBITA positive).

The biggest drain in CDMO. The US’s slow decision-making and funding issue due to the stock market rout is taking a toll. A good portion of PPL CDMO business is contributed from venture-backed start-ups (emerging biopharma), and they are facing increased security from their investor due to market corrections. This, in turn, shall be affecting what they are working on, indirectly impacting players like PPL.

Management commentary looks like the situation will take time to be corrected. When asked, management expects this situation to improve in the next 2 quarters; until then, CDMO will be impacted. It looks like CDMO is taking PPL downhill at the moment.

An additional $42 million Capex has gone live in Q4, which means it’s interest and other expenses, as well as depreciation, will hit Q4. As this is a new Capex, they are unlikely to have a corresponding increase in revenue. So the net effect will be negative on the P&L for Q4 unless PPL perform a miracle.

Although PPL is reporting P&L losses, they would have a good operating cash flow as they report huge amortisation due to their expensive acquisitions. So FY23 depreciation and amortisation amount will be around 650 cr. A good chunk of it will be towards amortisation, which means they will have 400-500 cr (my wild guess) operating cash available toward repayment even though they are reporting losses. Maybe that is the reason PPL is not too concerned about debt (or does not seems to be concerned to me). Management wants to raise money from rights issues for growth Capex as well as for debt repayment, but it may take Q2 to complete (by Sept end).

Overall, stock pricing (CMP 90) is at an attractive level, but the business is at a difficult position or going through a rough patch. One who understands the business well & high conviction may be rewarded well from this position, but there is some inherent risk. Many investors would prefer to look at one/two stable quarters before committing capital; until then, PPL may well trade in this choppy water.

Note: Invested for some time.

28 Likes

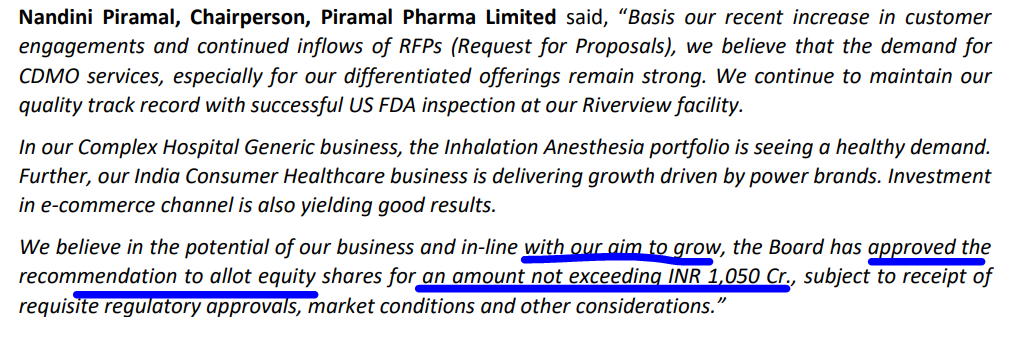

Heard the Q3 concall of Piramal Pharma. They r planning a fundraise of 1050 cr. The stock price is at a rock bottom.

The fund raise completion tgt is Q2 FY 24.

Question - Are they reasonably confident of a good Q4, Q1 which bumps their stock price before their fund raise. Can’t think of any other scenario where in the company wants to do a fund raise at depressed valuations ![]()

Its just a conjecture. Is it a valid one… time will tell.

Lets hope for the best !!!

Disc : invested, biased.

4 Likes

Or may be the company is not confident about its performance for upcoming quarters, hence under the ploy of being in the fund raise mode, they will duck all the uncomfortable questions terming them futuristic, as was done on a number of questions during current con call. Else when the fund raise was to be completed by Q2 FY 24, why was it announced just before the results and con call ? It could well have been considered after that and the investor should have been shown clear road map for subsequent quarters.

Disc : Invested at higher levels.

1 Like

I know right.

I cannot give this management the benefit of the doubt or any credit for potential capital allocation skills (or business operator skills either for that matter)

The concall was honestly painful - no direct questions answered straight. It felt like the no forward guidance was an excuse to give investors no visibility (because the management doesn’t have any?)

Honestly, the investors had very silly questions as well - e.g. why are Ajay and Swati Piramal not on the board. Like they’ll somehow magically increase margins and sales by attending board meetings.

That said the stock is at 3x EV/Sales (not fond of the metric but there’s no sustainable profits/cash flows to speak of)

They were at 25% EBITDA Margins in 2020.

If you double sales in 5yrs while getting back to 20% margin levels by 2028 - you get 2000cr EBITDA against 15000cr in EV today.

So 7.5x EV/EBITDA and 1.5x EV/Sales on 2028 numbers, hopefully they cut the debt in half and you have 1x debt/EBITDA.

Maybe the combination is worth 15x EBITDA, so you get 2028 EV of 30000cr. Reduce balance debt of 2500 and you get a market cap 27500, current market cap is around 11000k. So you get 20% IRR

But you get diluted with a right issue at silly valuations - so maybe 15-17% IRR (conservatively)

That looks inexpensive and not unachievable (assuming management executes differently from how they’ve behaved so far)

That said I’m not keen to average down just yet.

I think the private sector banks get you that IRR with better certainty. Even ITC probably gets you closer to 15% IRR with 10% sales growth + op leverage+ dividends. Maybe some of the better managements in the pharma space get you that IRR.

FYI - Peter DeYoung(CEO) is married to Nandini Piramal (Chair)

7 Likes

In fact, quite the opposite.

It was a direct comment saying: “If you lot don’t know how to do your job, get the veterans back. We’re fed up with you.” I felt it was the best question without actually insulting the mgmt directly.

The timing of the rights issue couldn’t be any better for them. An easy excuse to divulge from the pathetic performance and absolute inability of mgmt to steer the business properly during headwinds. Fools running a great business always go down together.

Will delete in few hours.

Disc: Invested pre demerge

7 Likes

One of the unasked questions in the call was :

Will the Carlyle participate in the right issue

This alone would give the intent of the current management team

A rights issue at this price is a great opportunity for them to increase their stake at a low price. Lot of frustrated investors may not subscribe to the rights

I was scratching my head last quarter when they gave a dividend of 30 rupees per share before the demerger when they had just provisioned a large amount against bad loans.

Maybe that dividend will come in handy now

7 Likes

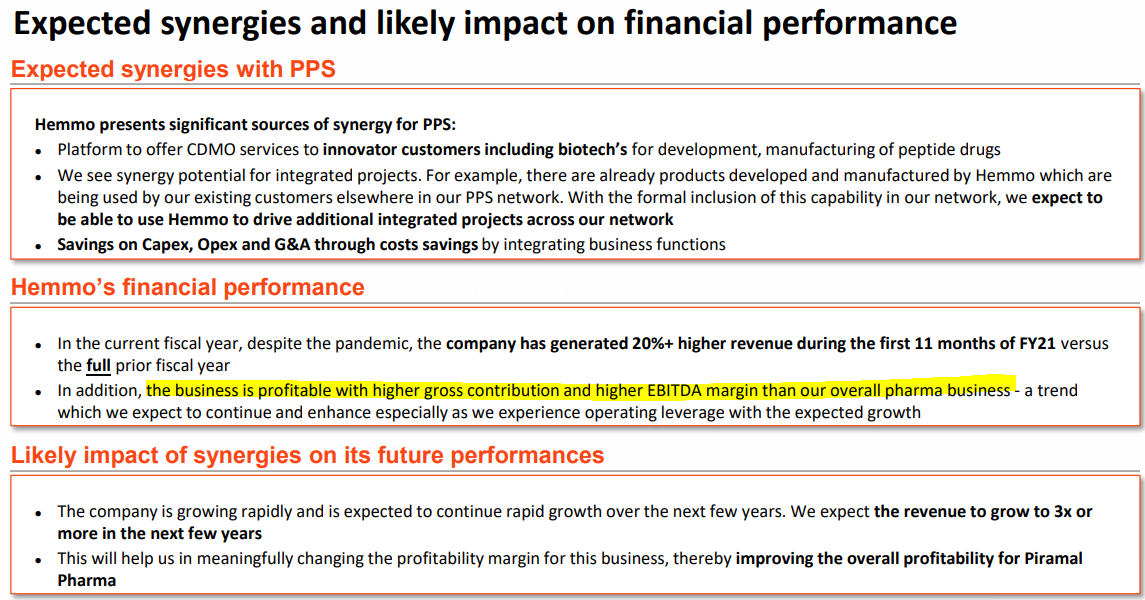

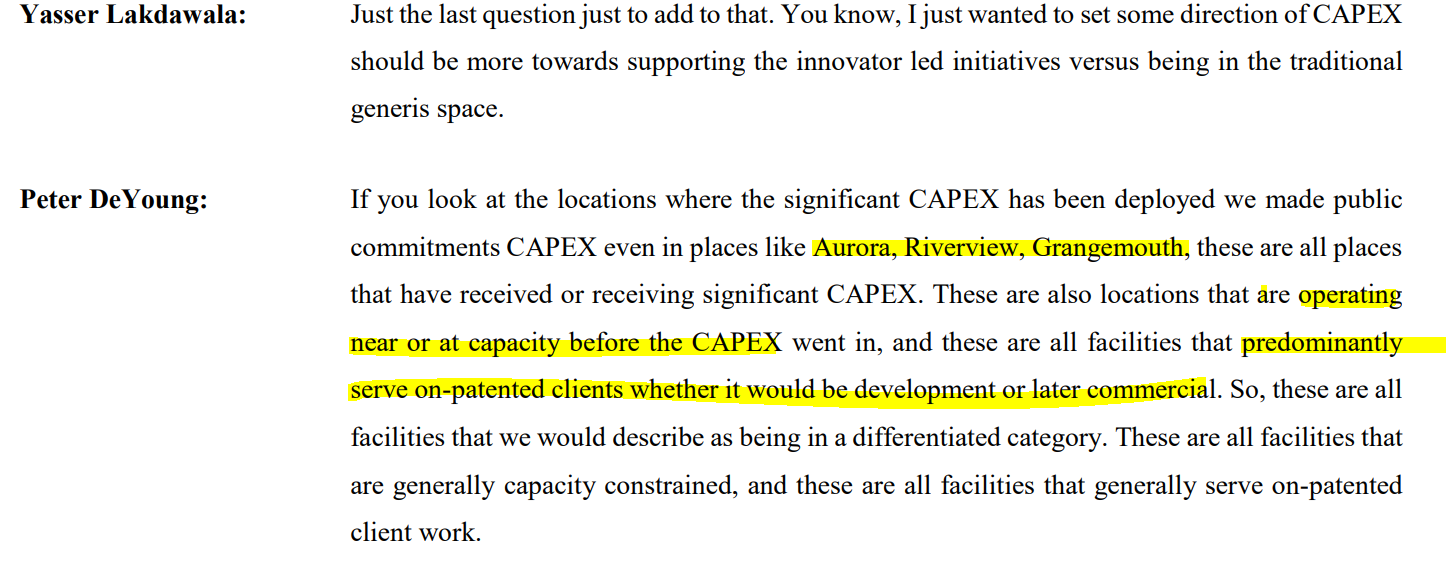

I re-read the transcript to understand their innovative CDMO business, Capex, better. Most of the Capex they are doing is going towards expanding existing high-margin businesses or targeting new innovative businesses, or expanding capacities where current capacities are running at full capabilities (Turbhe, Riverview, Sellsville).

In Q3, PPL went live with $42 million of Capex. This is mainly in Peptides, ADC, and in-vitro (within the glass) research facilities ((PDS Ahmedabad).

It is a high-margin business (although management said it is a high growth, it had revenue of of 121 cr with PBT of 35.5 cr in FY22, so I wonder if it will make a significant dent).

.. this is from April 2021 ppt at the time of acquisition.

PPL is undergoing major capex at various sites across the work.

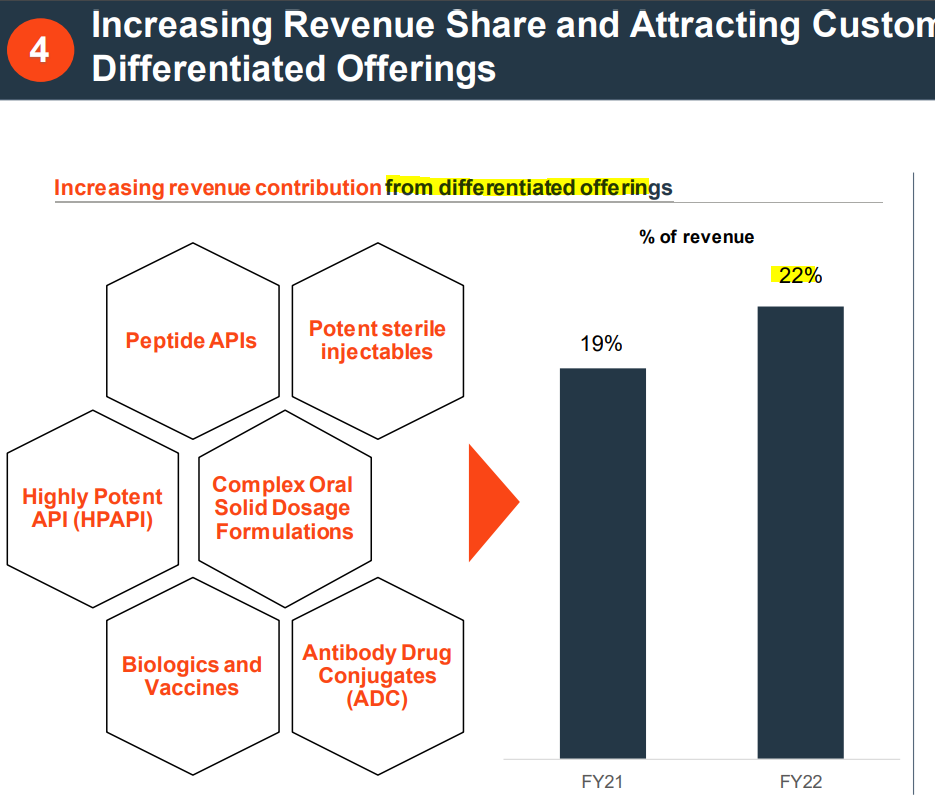

Another thing to track is how their differentiated offering is progressing. Although only some things here are patented, like peptides/ADC, these products have less competition and high margins even if they are generics.

As per management, most of the capex is to serve onshore clients for their innovative molecule. So once the capex goes live (whenever ), the portion of innovative molecules will increase rapidly. In FY22, $56 million (450 cr out of 3960 cr CDMO) was Innovative business, which is 11.38% of CDMO business. I think it could increase significantly in the next few years if one believes what they are saying.

Note- Invested

10 Likes

When is the rights issue coming out?

It’s been more than a month they declared…

(Waiting, waiting…)

1 Like

I think it will be in first half FY24, they have mentioned somewhere during concall. Thanks!

2 Likes

Common sense says, they would come up with rights issue under favorable valuations for the promoters not investors.

Hence if market valuations rise in 2023, only then they would else FY2024.

4 Likes

This is to inform you that the US FDA conducted a Good Manufacturing Practices (GMP) Inspection of Piramal Pharma Limited’s Digwal facility from 27th March, 2023 to 31st March, 2023. The inspection was completed successfully with Zero Form - 483 observations. The Company remains committed to maintain the highest standards of compliance.

8 Likes

PPL published draft letter for rights issues. It is a good read about the company. Some of the snippets from the draft.

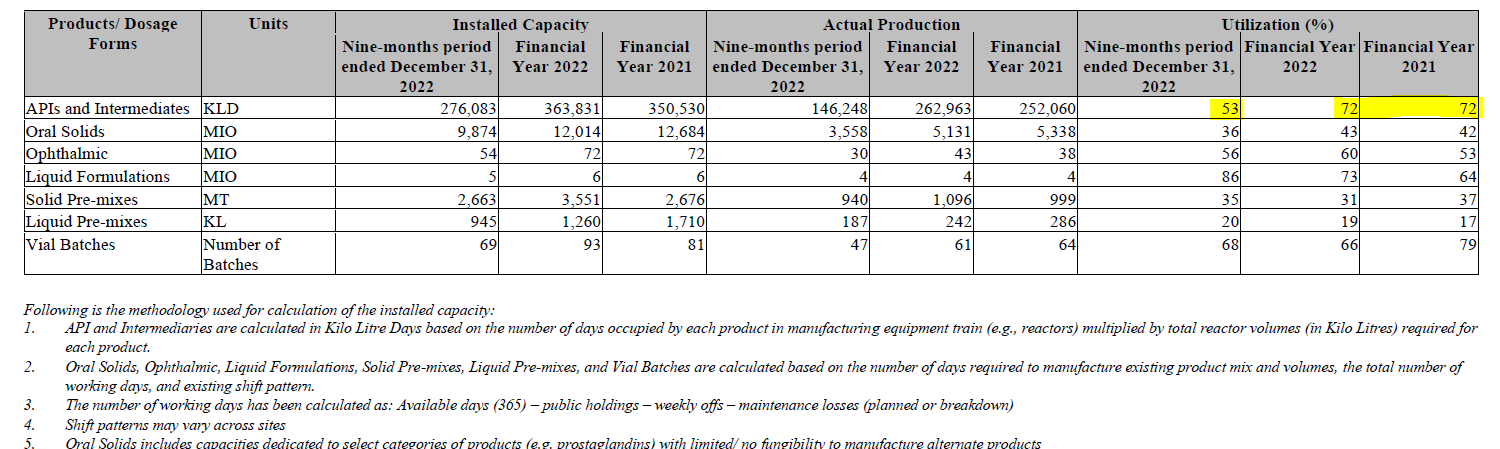

Getting meaningful information from management other than what they publish is very difficult. The below data shows what causes the sudden drop in profitability.

Few observations:

API capacities are underutilised- only 52% utilisation. Other dosages form also underutilised, but API seems to be a big daddy impacting profit.

ICH

This is a high ROCE business as PPL does not invest in manufacturing facilities, instead uses third-party suppliers to manufacture and focus on brand building and distribution. In 3 to 4 years time, this business could be a high ROCE business.

“Further, for our ICH business, our key products like baby diapers, baby wipes, medicated soap, lacto lotions and antacid liquids are manufactured by third parties.”

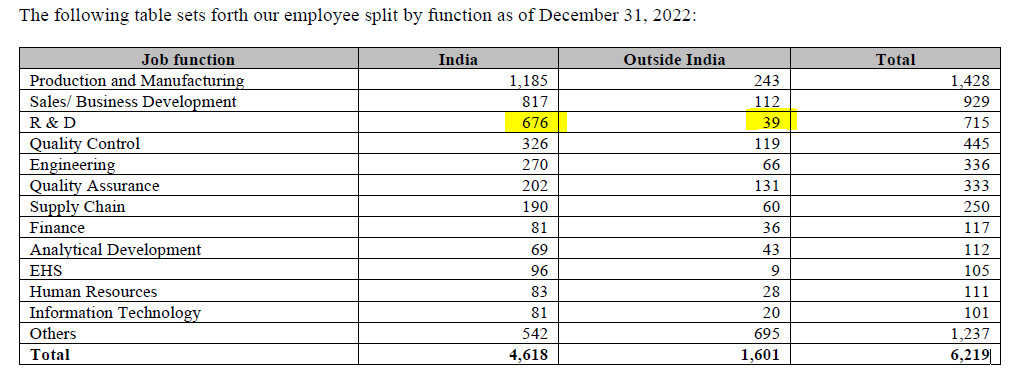

Employees

Most of the R&D is based out of India (95%), which augurs well from a cost point of view. The same is the story with Sales/Business Development. Looking at this, most of the employees are based in India, and 25% of employees are based outside India. Management said they faced increased employees cost abroad and faced difficulty in hiring. Not sure which job function they is related to. This is “This was primarily due to the impact of increments, higher average headcount and weakening of the INR versus key currencies.”

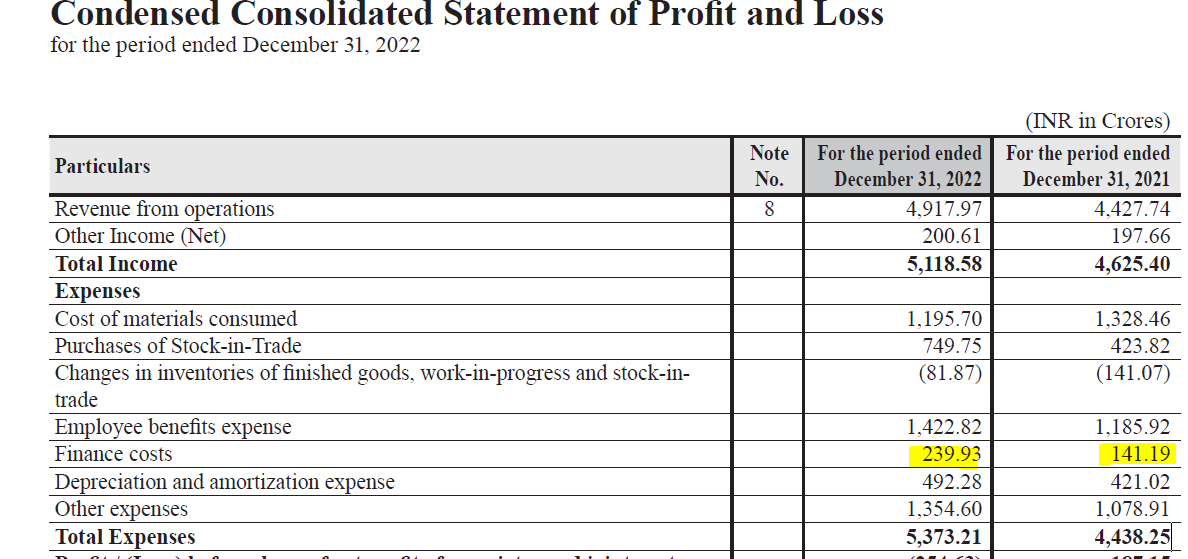

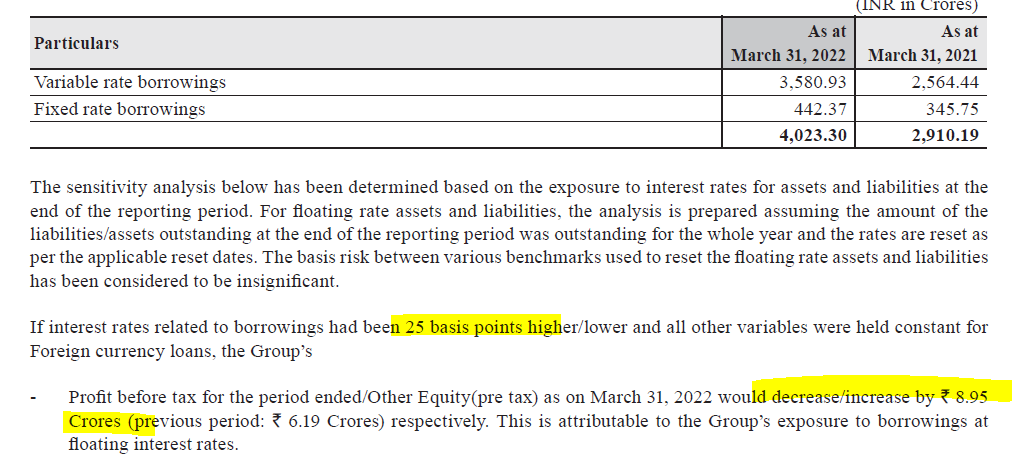

PPL has huge exposure to variable rate borrowing, as 89% of lending as on March 2022 is variable. This would have increased in 9 months to Dec 2022. Also, every 25-point increase impact PBT by 9 cr. The higher interest rate environment has severely impacted PPL. This has caused a 70 % increase in the interest cost in 9M.

…this is due to exposure to variable interest rate

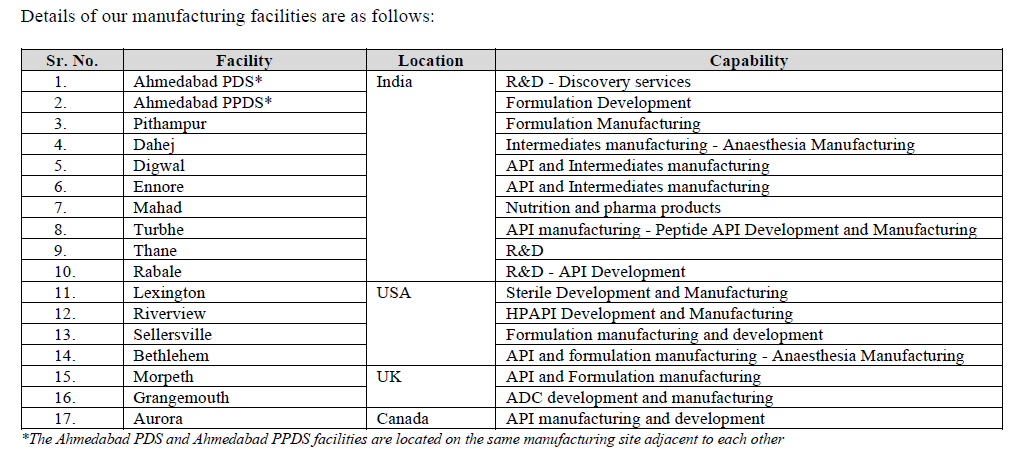

Number and location of manufacturing facilities across the globe

Purpose of issue is to repay debt. However Q3 con-call, management said it is rights issues is mainly for funding growth capex.

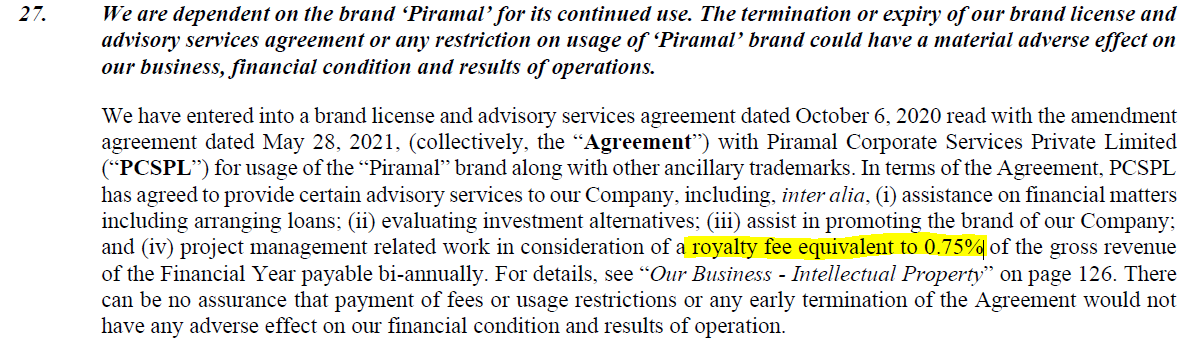

… last is PPL pays 0.75% as a brand royalty to Piramal for using their brand.

29 Likes