Synopsis:

The Company and certain subsidiaries act as a Contract Development and manufacturing organization offering both APIs and formulations. The Group’s critical care business deals in the inhalation anesthesia market. The group’s consumer products business is primarily an India-centric consumer healthcare business with a strong brands portfolio.

- 15 Manufacturing Sites across North America, the United Kingdom, and India.

- 100+ Countries commercial presence.

- 68% revenue from Regulated Markets.

- FY22 Revenue - 6701 Cr. → 10 Yr. CAGR: 13%. FY22 EBITDA - 1206 Cr. @ 18% Margin.

- Demerged from Piramal Enterprise Ltd and was listed on BSE and NSE on 19th October 2022.

- Margins Pecking Order: CHG → CDMO → ICH (Breaking Even, Investing heavily in Branding and Marketing).

Details about the 4 Business verticals- CDMO, CHG, ICH, and Others- JVs.

I. Contract development and manufacturing organization (CDMO) - One-stop shop for early-stage research to manufacturing

- End-to-end development and manufacturing services through a globally integrated network of facilities to innovator and generic companies worldwide, ranging from drug discovery and clinical development to commercial manufacturing of active pharmaceutical ingredients (APIs) and formulations for global pharmaceuticals and biotech companies across the drug lifecycle, which includes (i) drug discovery, (ii) pre-clinical, (iii) clinical trial, (iv) launch of the drug, (v) on-patent and (vi) off-patent.

- Capabilities include handling injectables, HPAPIs (high potency APIs), and antibody-drug conjugates (ADCs).

- Top 10 customers account for 39% of FY22 revenue

- Key Acquisitions:

- 2011: Acquisition of Oxygen Bio Research: Based in Ahmedabad, India. Oxygen is a 7-year-old discovery services company. Helps to partner with its client companies at the early stage of drug life cycle. <<63 Cr.>>. On February 26, 2014, acquired the balance 10% stake <<11.6 Cr.>>

- 2015: Acquisition of Coldstream Laboratories Inc. (“Coldstream”) - Development and manufacturing of sterile injectable products. Fill and finish options to certain existing antibody drug conjugate customers in Grangemouth, Scotland. << USD 30.65 million>>

- 2016: Acquisition of Ash Stevens Inc. (“Ash Stevens”) - Engaged in the business of manufacturing high-potency APIs. Synergistic with our antibody drug conjugates and injectables business. <<USD 44.8 million>>

- 2020: Agreement with G&W Laboratories Inc. for the acquisition of its solid oral dosage drug product manufacturing facility in Sellersville, Pennsylvania <<USD 17.5 million>>

- 2021: Initial stake of 27.78% in Yapan << 102 Cr.>>. Based in Hyderabad. Acquired further stake of 5.55% << 20.35 Cr.>>. Specializes in Vaccines and Biologics.

- FY22: Acquired a 100% stake in Hemmo Pharmaceuticals. Peptide API development and manufacturing. << 775 Cr.>>

- Key Data Points:

- CDMO sites across North America, Europe, and India

- Capabilities across drug substance and drug product

- Top 3 in India | 13th largest globally

- Service offerings across the Lifecycle of the molecule

- Value proposition: Reduced time-to-market and operational complexity; lower supply chain costs

- Scale Matters in the CDMO Market | CDMO Firms >$100m in Size have a disproportionate share of the market | % of Firms 63 % of Market Share

- Biotech and Mid Pharma emerging as an important customer category

- Pharma companies increasing outsourcing to “integrated service providers”

- ~500 customers

- $157m of Growth-oriented customer-led Brownfield Capex committed across multiple sites for the CDMO business over the next 18 to 24 months.

- FY22 Revenue - 59% | 3960 Cr. → 10 Yr. CAGR: 11%

- Addressable market size: ~ USD 130 Bn

II. Complex Hospital Generics:

-

Branded hospital generics portfolio comprising inhalation and injectable anaesthesia, pain management drugs, and intrathecal spasticity management drugs.

-

Key Acquisitions:

- 2014: Joint Venture and Shareholders’ agreement with Navin Fluorine International Limited (an Arvind Mafatlal Group Company) to form a Joint Venture Company named Convergence Chemicals Private Limited to develop, manufacture, and sell specialty fluorochemicals to be used for healthcare business. PEL holds 51% of the equity share capital. In 2020, increased stake to 100% by buying out NFIL’s 49% stake in CCPL at 65.10 Crores.

- 2016: Acquisition of injectable anaesthesia and pain management products from Janssen Pharmaceutical NV - Five additional injectable anaesthesia and pain management products, namely, Sublimaze, Sufenta, Rapifen, Dipidolor, and Hypnomidate. Provided access to over 50 countries in which these five products were being marketed. Upfront consideration of US$155 million.

- 2017: Acquisition of portfolio of intrathecal spasticity and pain management drugs from Mallinckrodt LLC - The portfolio acquired includes Gablofen (baclofen), a severe spasticity management product, which is currently marketed in the United States, and two pain management products, which are currently under development. Gablofen has also been approved for launch in eight European markets. for a consideration of USD 171 Million.

-

Key Data Points:

- Product Categories:

- Inhalation Anaesthesia: Revenue Contribution → 67%

- Injectable Anaesthesia and pain management: Revenue Contribution → 19%

- Intrathecal Therapy: Revenue Contribution → 5%

- Other Injectables: Revenue Contribution → 5%

- 4th Largest Inhaled Anaesthesia Player Globally

- High barriers to entry and low competition | Branded nature for the bulk of the portfolio

- 6000+ customers | Commercial presence in over 100 countries

- Differentiated portfolio of 40 products spanning inhalation anaesthesia and injectable

- 36+ SKUs in the pipeline with an addressable market of US$6.8bn

- Vertically Integrated Manufacturing Capabilities (Key Starting Material @ Dahej and Finished Products @ Bethlehem, USA, and Digwal, India)

- FY22 Revenue - 30% | 2002 Cr. → 10 Yr. CAGR: 17%

- Addressable market size: ~ USD 54 Bn

- Product Categories:

III. India Consumer Products business

- The Over-the-counter (OTC) market portfolio comprises various brands and products across key categories including skincare, gastro-intestinal care, women’s intimate range, kid’s wellbeing and baby care, pain management, oral and respiratory healthcare. Brands include Saridon, Lacto Calamine, I-Pill, Supradyn, Polycrol, and Tetmosol.

- Key corporate actions and acquisitions:

- 2010: Acquired “I-pill” brand of Cipla for an aggregate consideration of Rs. 101 Cr.

- 2015: Acquisition of "Little’s”, a baby-care brand - Portfolio comprising the entire product range across six categories of products including feeding bottles, skin-care, grooming accessories, apparel, and toys for babies. The “Little’s” brand which caters to children in the age group of 0 – 4 years also complemented the existing “Jungle Magic” brand in our Consumer Products business which carried products for children who were 5 – 10 years old. [75 Cr.]

- 2015: Acquisition of five OTC brands from Organon India Private Limited and MSD BV - Brands such as Naturolax, Lactobacil, and Farizym. [92 Cr.]

- 2016: Acquisition of four OTC brands from Pfizer India - Ferradol which is a nutritional supplement for children and adults, Neko which is a medicated soap, Sloan’s which is a muscular pain reliever available in balm and liniment forms and Waterbury’s Compound which is used for building immunity against cough and cold. [121 Cr.]

- 2018: Acquisition of Digeplex and associated brands from Shreya Lifesciences - strengthened position in the Gastro-Intestinal (GI) segment and is complementary to existing brands - Polycrol and Naturolax, in the GI segment. [103 Cr.]

- 2018: Acquired marketing rights of Supradyn, Becozym C Forte & Benadon from Bayer

- Key Data Points:

- Ranked 10th in the OTC segment in India

- Strengthened presence in alternate channels with over 8,700 modern trade stores, our own website, and 24 eCommerce platforms (up from 2 in FY18) in the ICH business

- Investments in Brand Promotion and Marketing

- Launching Multiple New Products and Brand Extensions

- Presence in ~200K chemists and cosmetics stores and 10K+ kids, toys and gift shops

- Strong focus on E-commerce, contributed 15% of revenues in FY22

- Launch of direct-to-customer website, Wellify.in

- 40 new products launched in FY22 in the ICH business

- FY22 Revenue - 11% | 741 Cr. → 10 Yr. CAGR: 18%

- Addressable market size: ~ USD 7 Bn

IV. Ophthalmology Branded Products:

- Allergan India Limited (‘AIL’): AIL is a 51:49 Joint Venture between Allergan Inc., USA, and Piramal Healthcare Limited. Piramal Ownership - 49%

- FY22 Revenue - 414 Cr. → 10 Yr. CAGR: 9%

Financials:

Data from the ARs of Piramal Enterprise Ltd and author’s analysis:

1. Income Snapshot

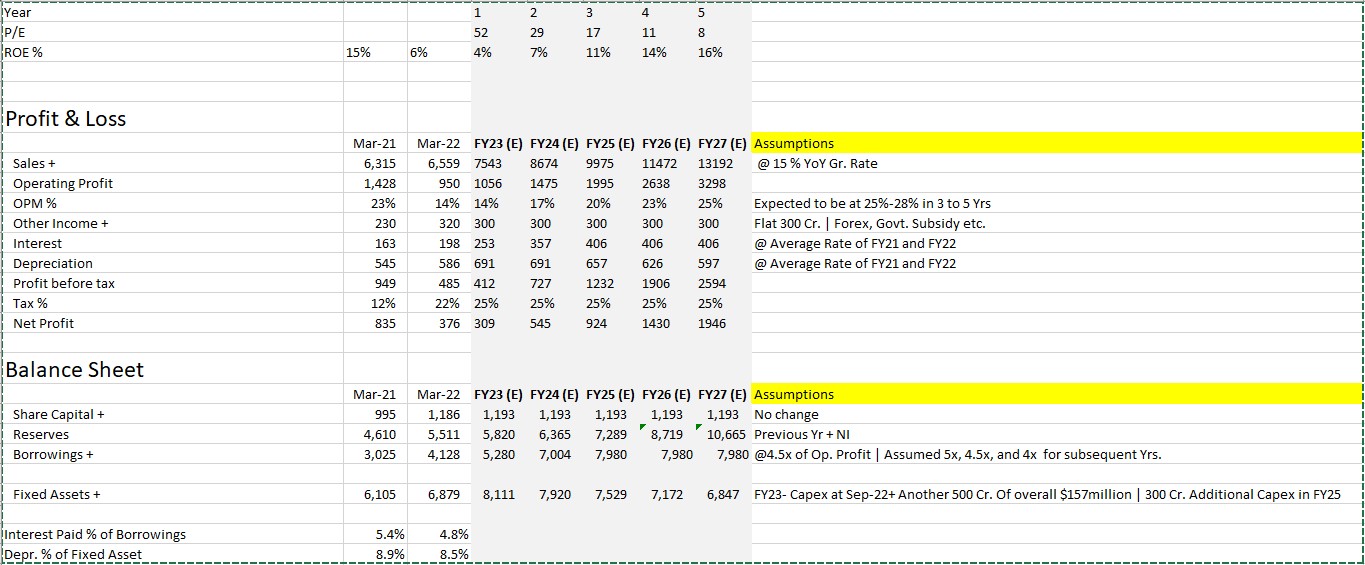

- After breaking even at the EBITDA level from 2016 onwards, the operating margins reached closer to 20%. However, the operating margins of the recent two quarters have been ~10% for the latest two-quarters of FY23.Per say management, 2nd half margins will be way better due to lumpiness in the CDMO business. In the 3 to 5 Yrs. timeframe, the goal is to reach the level of 25-28%.

- Using FY22 revenue as the base, the CAGR of revenue has been 11%+ when measured using blocks of 3 Yrs., 5 Yrs., 7 Yrs., and 10 Yrs. Per say management, the revenue growth rate will be in Mid-Teens for the near term.

| 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 10 Yr. | 7 Yr. | 5 Yr. | 3 Yr. | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 6700 | 5776 | 5419 | 4819 | 4449 | 3973 | 3590 | 3166 | 2877 | 2477 | 2079 | 1673 | 12% | 11% | 11% | 12% |

| EBITDA | 1191 | 1241 | 1433 | 523 | 800 | 593 | 246 | -498 | -61 | -154 | 298 | 98 | 15% | - | 15% | 32% |

| EBITDA Margin % | 18% | 21% | 26% | 11% | 18% | 15% | 7% | - | - | - | 14% | 6% | - | - | - | - |

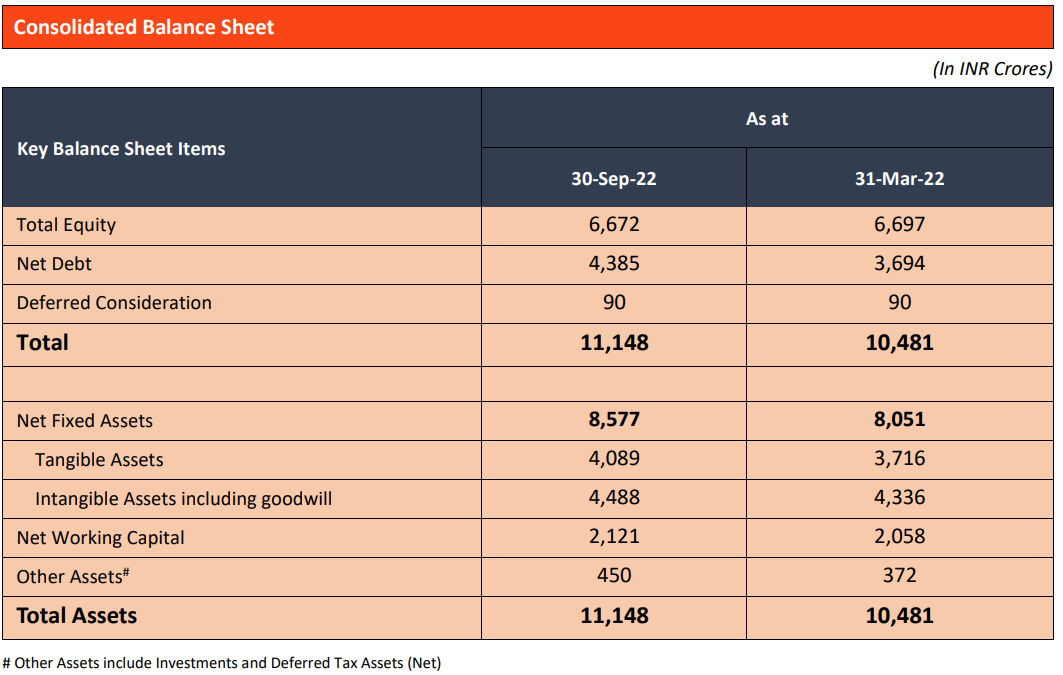

2. Balance Sheet Snapshot

- Net Debt is already at the threshold of ~4.5x of EBITDA, an upper limit conveyed by the management. Ongoing Capex is expected to be financed using internal cash generation and refinancing the retried portion of the debt.

- One-third of the balance sheet assets are goodwill and intangibles due to various acquisitions over the year.

What’s interesting?

- India’s pharma industry will benefit from the fiscal pressures in developed countries alongside the China-Plus-One pressures. Piramal’s US, Canadian, and UK facilities could benefit from the reshoring trends.

- The non-compete period with Abbott is now over, opening up new possibilities.

- Committed $ 157 Million of growth-oriented Capex investment across FY23 and FY24 for various sites at Aurora, Pithampur, Riverview, Grangemouth, and Morpeth.

- Global footprint with a diversified revenue base, presence in attractive segments with high entry barriers, capability to meet a wide range of customer requirements across multiple geographies, and best-in-class quality track record, provides greater stability from a long-term investment perspective

Risks:

- The CDMO business, which contributes ~60% to the revenue, is lumpy in terms of how the deliveries are scheduled across the year.

- Being a global pharma business and presence across the drug lifecycle, margin percentages will never reach the level of an India-based manufacturer such as Divis (40% OPM).

- No audited and published past track record: FY23 will be the first year when the business will formally publish its standalone numbers.

- Regulatory headwinds

- Supply chain disruptions and volatility in raw material costs

Valuation Dimensions:

1. Relative Perspective

- Considered top 20 businesses on the basis of Sales.

- Filtered out some businesses that lacked the expected fundamental characteristics of PPL - Sales growth >= 10% for the block of 3 and 5 years and OPM % between 18% to 25%.

- Below listed are the comparable ones and PPL valuation is almost at the bottom of this group on the basis of CMP/Sales, keeping OPM% in view.

| Name | Mkt Cap (Cr.) | CMP/ Sales | OPM % | Sales (Cr.) | Sales Var 3Yrs % | Sales Var 5Yrs % | Assets (Cr.) |

|---|---|---|---|---|---|---|---|

| Biocon | 32956 | 4 | 20 | 9042 | 14 | 16 | 22664 |

| Piramal Pharma | 15841 | 2.4 | 14 | 6559 | 12 | 11 | 13671 |

| Ipca Labs. | 21687 | 4 | 18 | 5906 | 16 | 13 | 7898 |

| Abbott India | 43039 | 8 | 23 | 5163 | 10 | 11 | 4100 |

| Granules India | 8884 | 2.1 | 20 | 4197 | 18 | 22 | 4858 |

| Ajanta Pharma | 15671 | 4 | 24 | 3597 | 18 | 11 | 4448 |

2. Outside Perspective

In October 2020, the Company completed the sale/transfer of the pharmaceutical business, held by the company directly and through its subsidiaries, to Piramal Pharma Limited (‘PPL’), a subsidiary of PEL(‘Transaction’) and PPL received 3,523.40 Crores on the closure of the Transaction for 20% equity investment from CA Alchemy Investments, an affiliated entity of CAP V Mauritius Limited, an investment fund managed and advised by affiliated entities of The Carlyle Group Inc. The Transaction valued the pharmaceutical business at an enterprise value of USD 2,775 Million (~18,000 Cr.).

3. Management’s Views:

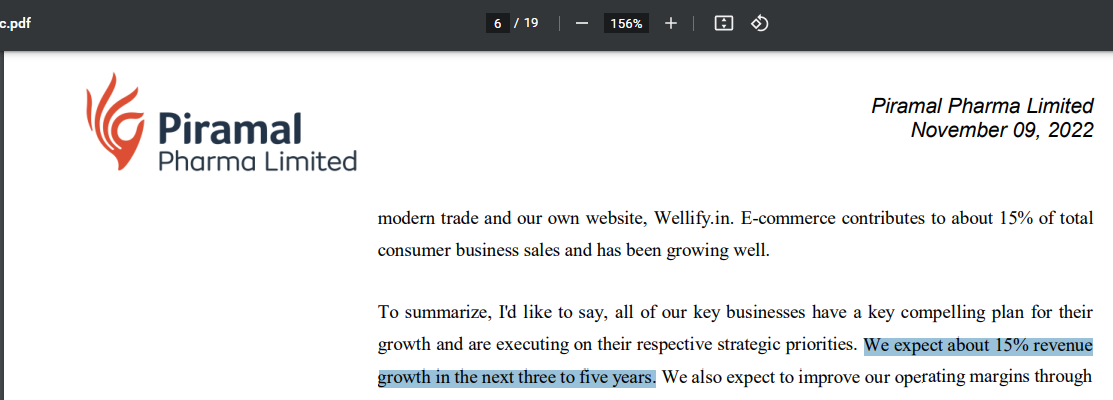

- In the medium-to-long term, we expect about 15% revenue growth across the businesses and expect the EBITDA margins to reach 25-28% in the three to five years timeframe.

- In terms of margin, considering the current inflationary scenario and energy prices, Ukraine-Russia conflict, execution issues at CDMO [significant attrition at our overseas sites during the pandemic and customers changed the phasing for the delivery], and highly volatile environment, I don’t think it would be prudent to make guidance right now. So, we’ll keep that for later. But on revenue, we are targeting a growth of high-teens as demand remains strong. expect to improve our operating margins through scale advantages

- Cap debt at about four times the EBITDA of the business.

- Historically, H2 has always been much stronger than H1, with about 55% of total revenue, and 66% of the EBITDA being booked in H2. We expect a similar trend to follow this year as well.

- From 2010 onwards, PPL has spent ~4400 Cr. to acquire various businesses that are now part of the listed company. Considering the time value of money using a compounding rate of 7%, the spent amount will be worth ~6200 Cr.

Sources:

- Various ARs of PEL

- Conference Calls of PEL and PPL

- Investor’s presentation of PEL and PPL

- Interview @ Peter DeYoung – GBReports

Disclosure:

Not Invested. Still under due diligence.

")