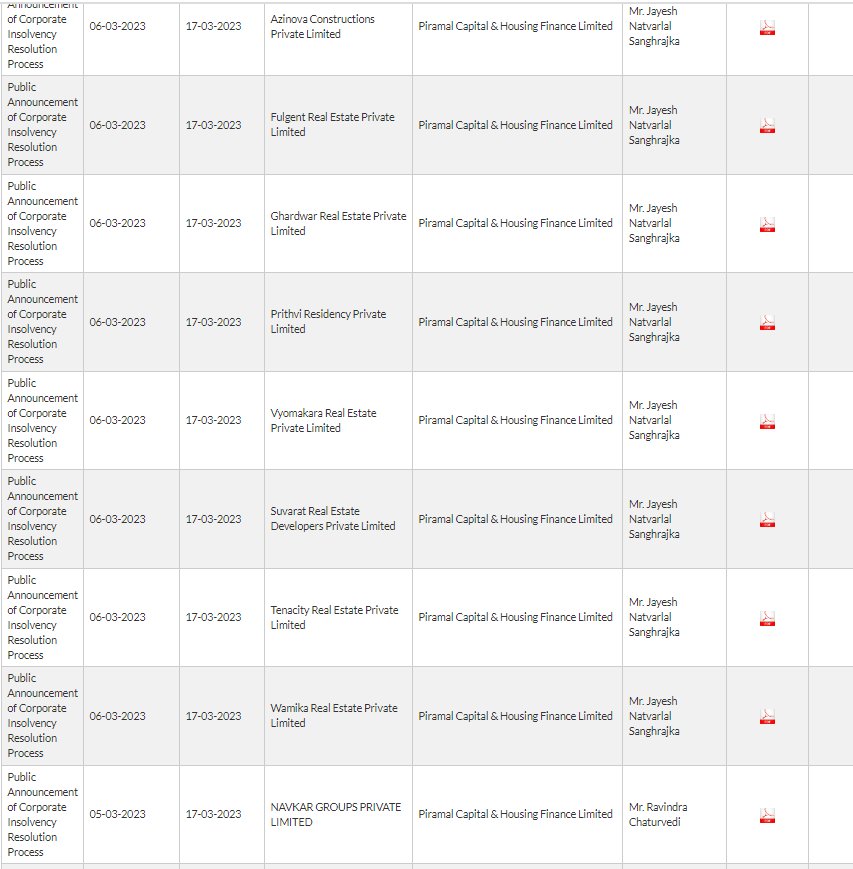

PCHFL initiated insolvency against 9 real estate companies in March. These are perhaps part of the DHFL (POCI) book.

The total trigger claim of all 9 companies amounts to ~INR 8,000 crores.

Source: IBBI

PCHFL initiated insolvency against 9 real estate companies in March. These are perhaps part of the DHFL (POCI) book.

The total trigger claim of all 9 companies amounts to ~INR 8,000 crores.

Source: IBBI

There was pending litigation between DHFL creditors, challenging the decision to sell 40,000 cr of wholesale loans to PEL at Rs 1. There was a court case, and there has been no news about it for the last nine months. And suddenly, PEL filed cases against the defaulter, as pointed out by @Jay_Shah . Maybe PEL waited for some time to get clarity (and a verdict on their side) before pursuing the cases further for litigation. No one knows; even PEL has not said anything recently, so it might be speculation.

Additionally, the Real estate market is on full steam. For example, DLF sold out their $1 billion luxury project within 72 hours. Also, only selected people are offered the opportunity to view the flats (invitation only). Other projects are also reporting a similar trend.

Anarock is also hinting at the same things.

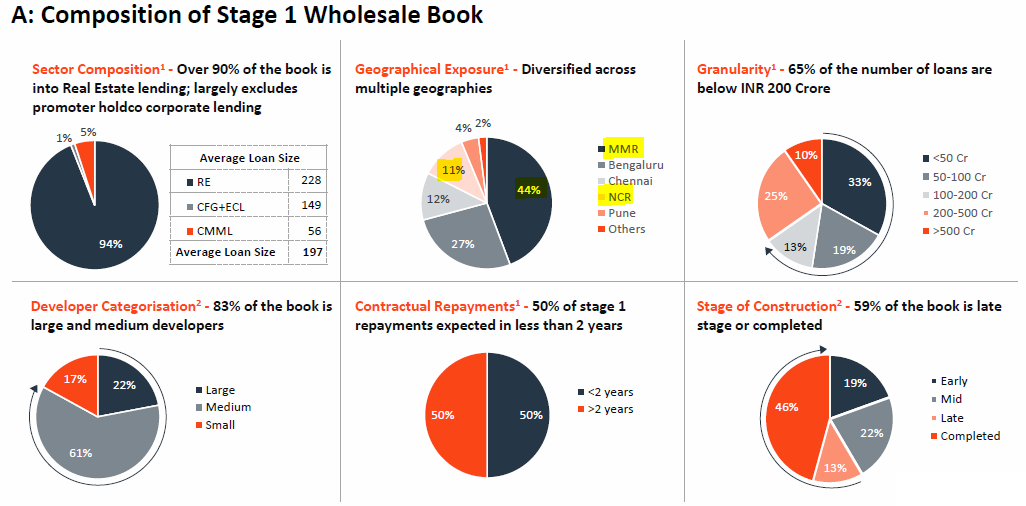

This means the luxury market in Mumbai, Banglore and NCR is showing higher demand. And this is the market which constitutes more than 80% of PEL lending. Hopefully, this will also help them recover more money than they have budgeted.

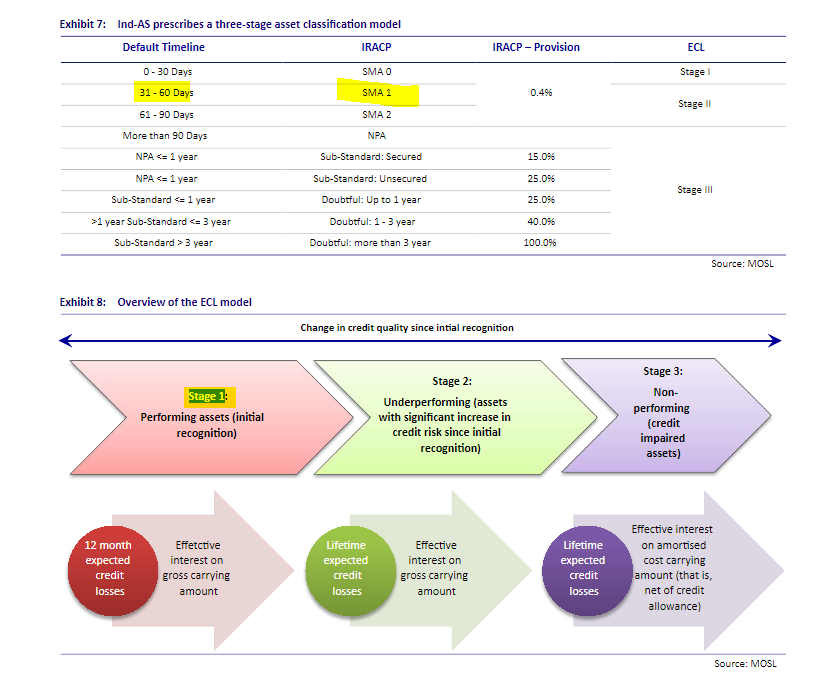

This is the definition of stage 1 (document is little old, and there may be slight different now)

The real estate market has been on the upswing for the last 4/5 quarters, but this is when PEL reported record-breaking losses due to more provisions. So it is challenging to think about what PEL will deliver versus what we believe. Hopefully, the worst is behind in terms of provisions, and they will report better performance, but when it comes to PEL, never say never.

Following is the rational for 5 year growth period, contrary views invited -:

Provisions:

Legacy Wholesale Book - 54% of the Outstanding AUM.

Stage 3 Book is ~ 10.7% of the Book and PCR is 72% which is conservative but what troubles me is the Stage 2 Wholesale Book addition which they did in Sep Quarter. This book stands at 19% and PCR on this is only 29%.

Given in Infra loans the Loss Given Default runs high even with secured assets, low LTV etc which is evident from their distressed sales, so I don’t trust the Secured Assets commentary from Management on this. By the time you get hold of those assets there are new dead Skeletons.

Some of this 19% is obviously going to flow in Stage 3 in the coming Quarters and there will be provisions.

I have factored in 50% of the Stage 2 Book flowing into Stage 3 and same 70% PCR given elevated Provisioning in recent Quarters but supported by additional recoveries from DHFL book.

So expecting ~ 1300 crores of additional Provisioning spread over the next 1.5 year.

Growth:

I’ve assumed ~ 20% growth over the next few years for Retail Side. Then at the end of five years I’ve backtracked their total Portfolio according to their own targets of 70% Retail and that leads to a Total AUM of 91000 Cr.

This automatically adjusts the Growth in 2.0 and Degrowth in 1.0 Portfolio.

Retail - 63750 and remaining Wholesale 1.0 and 2.0

Net growth over the next 5 Years comes to around 7%.

ROA Tree:

Over the next five years given retail shift have assumed Yield on Loan Book tilting to 13% from 12.4% levels currently. Interest Costs at 8.35%.

Have kept Credit Costs elevated to 2% of the AUM for the first few years and then 1.75% thereafter.

OPEX continues to grow in line with Loan book growth at 7%.

Other Income continues to grow in line with the growth in Retail Book since that is the Primary Driver.

With this Story their leverage increases at the end of five year and improves the ROE(8.3%) but still the ROE doesn’t manage to beat the Cost of Capital. I’ve assumed Terminal value at Y5.

Where will the Alpha come from? - For a company that has an OPEX/Total Assets Cost of 3.45% NIMs of ~6% don’t justify being in the business lending to relatively Risky Segments since there will always be elevated Credit Costs. The other Income as % of Assets is also low given there is low net growth in AUM. If the OPEX grows at a slower pace than Loan Book and Other Income growth there will be improvement in ROA. If their Credit Costs are controlled that will lead to additional improvement and they might be able to get to their Cost of Capital.

Investments - If they wind down their Shriram Investments and do a buyback at Current Price that will be value Accretive to Shareholders. Institutional Investors should push for this.Somebody suggested this in the latest Concall as well.

Taking the Investments and JVs at 0.75 * Book value the NBFC Biz trades at 0.5 times Book value. Market has already factored in a lot of Pessimism in the Price. If Jairam can turnaround the company in the next year by Controlled Provisions and Controlled Stage 2+3 there will definitely be rerating.

My guess is they will not do a buyback, rather use the money for acquisitions…they have mentioned and demonstrated that “M&A is in their DNA”.

Any members from Mumbai and staying close to Andheri/Jogeshwari East…their land is in Majaswadi…but I am not able to find any details from MahaRERA portal…anyone can help with some digging?

Any idea how it wlll be reported in Q4? Will be gain or any other adjustment?

Hi

Only 15% is cash while 85% is in securities which shall be paid as securities so best they can do is put 15% as realized gain and 85% as deferred assets/investments which shall be realized basis JM financial recovery.

Bigger point however remains is why there was just one bidder, also they did not get price which was 10% higher the reserve price that they had proposed for minimum. There can be multiple reasons for that, few can be as below

If they report 15% of cash as Profit (assuming this loan is part of a wholesale pool valued at Rs 1), then it will result in a Profit of Rs 382 cr.

Give or take a few cr of expenses; it should result in more than 200-300 cr of Profit. If that is the case (although this is too good to be true as I feel I am missing something), it is the PAT PEL who shall report on the quarterly operations (if they choose to report).

The remaining 85% - 2167cr- shall be as provided as a security receipt. I am unsure if this will be paid any interest on it, although PEL may benefit if JM Financial ARC recovers more than they paid for.

Hi, I am not aware of the details of ARC transaction but know how an ARC transaction happen. Will illustrate from an example below.

Suppose I have bad assets of 100cr (please note this is gross) and against this I have a provision of 50cr so net asset or we call Net book value is 50cr.

Now suppose I get a valuation of 70cr for my net book value so this will be considered as 40% premium on my NBV.

Now I get 85% as security receipt and 15% as cash on the valuation I receive. In my case the valuation is 70cr hence 60cr security receipt and 10cr cash.(approx.)

One very important point here is each account is treated individually. This means if my bad asset has cumulatively 5 accounts A,B,C,D,E then I would calculate profit or loss for each account individually.

Let say the 10cr cash which I received is for an account which have a net book value of 15cr that means I would recognize 5cr loss. This also means my balance 35cr of NET book value(50-15) gets 60cr as valuation.

SR(85%) 60cr valuation for 35cr of net book value

CASH(15%) 10cr valuation for 15cr of net book value

TOTAL 70cr valuation for 50cr of net book value

In short if the valuation is higher than NBV I recognize profit ( if cash recovered) and if valuation is lower than NBV I recognize loss.(regardless of cash received or not)

Even in SR if any account individually has a valuation less then NBV I recognize loss. The loss can be recognized over 2 quarters.

If the entire bad loan just has 1 account then the transaction is very simple.

I would recommend everybody to go through Yesbank Q3 concall and result as they concluded the largest ARC transaction.

Is the Royalty that “Piramal” family is charging PPLPharma, applicable to PEL as well?? Any idea…Please through some light if anyone already knows about it.

To set context- Primal Pharma has come out with rights offer. In the document they have mentioned that PPL pays 0.75% of gross revenue as royalty to Piramal’s. Please refer below link for more details (links)

The royalties have been on for long. Quantum has gone now gone up to 0.75%. Now even PEL will pay 0.75% royalty on revenue going forward, which for a fin services company seems quite high. This is as per my tele call with IR guy at PEL.

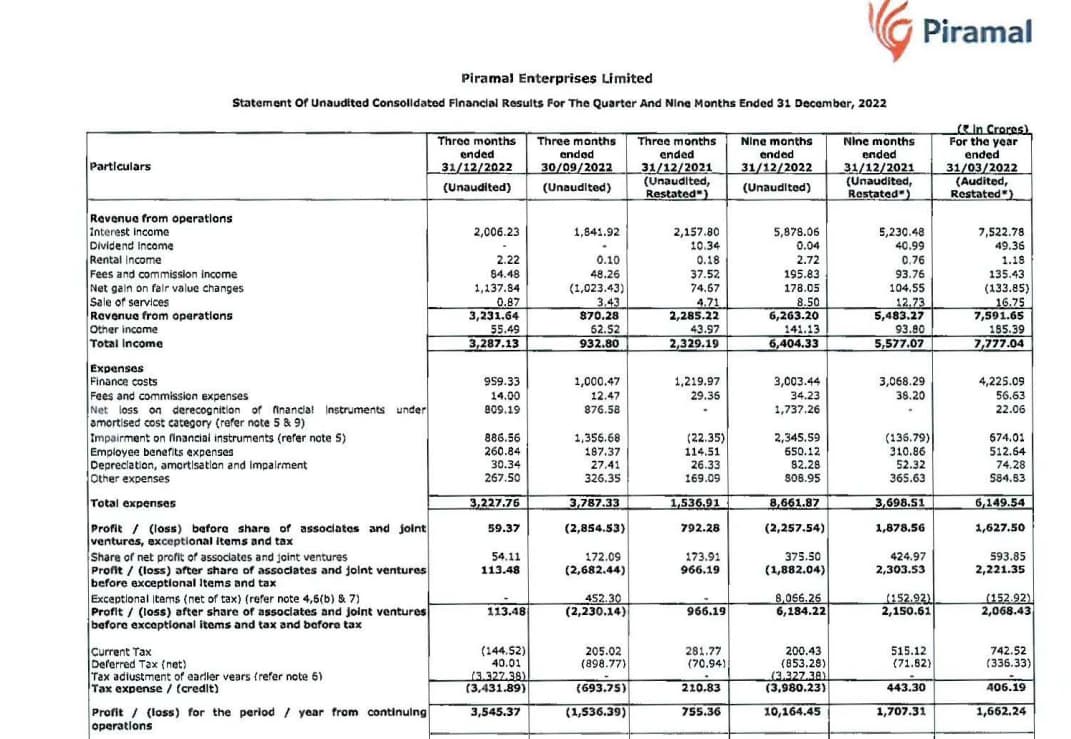

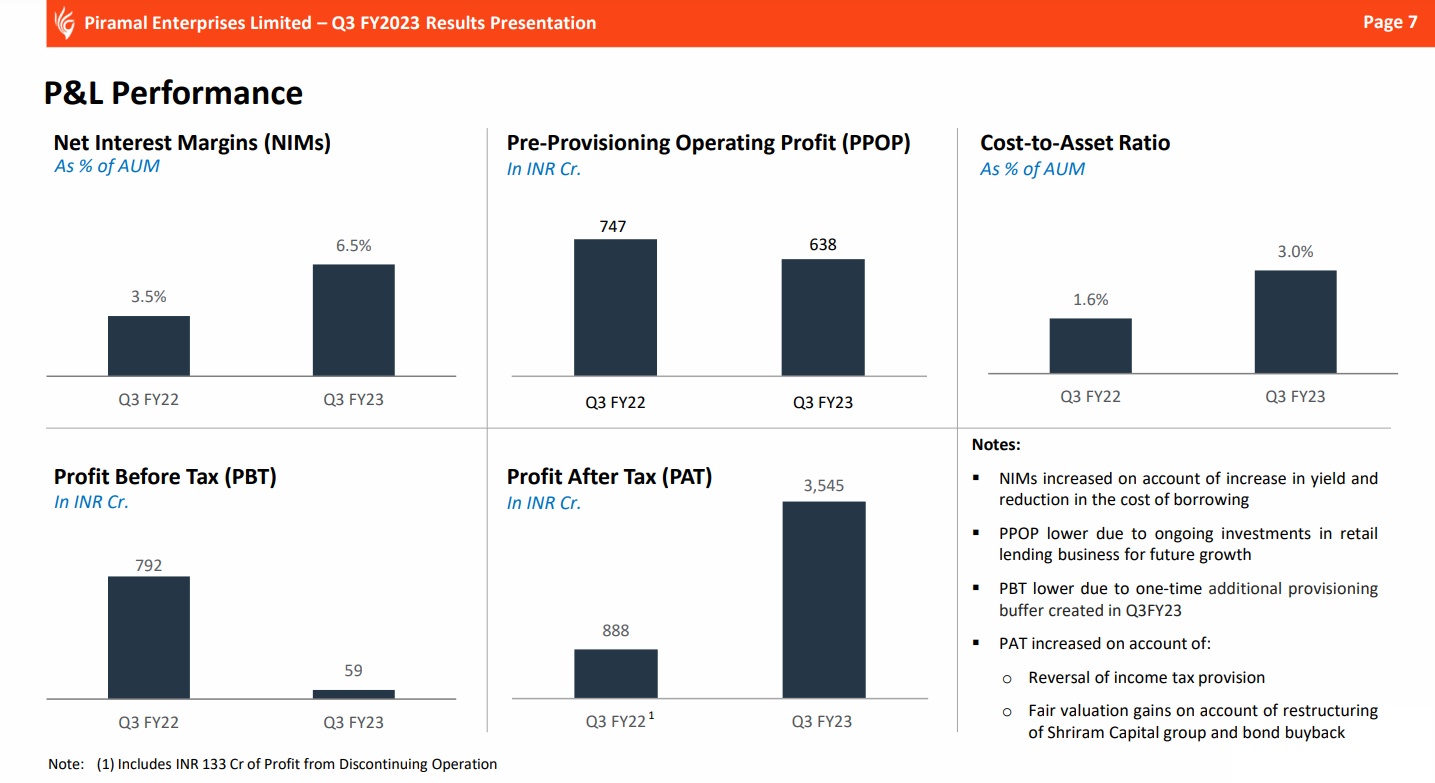

Was looking at Q3 results in detail. I don’t understand how PPOP is shown as 638Cr in the presentation? As per my calculations it should be 1755Cr (Total income - total expenses + expenses related to provisioning and write offs). Is this a typo?

I think you want to exclude “Net gain on fair value changes (~1137 crs)” though it is coming at 618 but company might include & exclude from other expense/income based on it’s type. Thanks!

Piramal Enterprises Q4 FY’23 results are out. Here is the link:

I feel there is potential for the mcap to go up in the future.

they have deferred tax asset of 1.8k cr, investment in Shriram Fin worth about 4k (not considering investment in unlisted entities of Shriram group), the land in Andheri East (Mumbai) their value on BS has increased by 1k cr to 2.3k cr (Surprisingly no one asks the management about this land project on the analyst call). On the business front sequentially the income seemed to be slowing down and expenses increasing, is there any challenge in scaling the business.

The retail AUM is increasing, but not inflecting in the income, am I missing something.

Disc: invested from pre demerger days

Above news item give out names of distressed accounts. I wish company would have been transparent enough with its investors to declare these in their investor presentations or at least speak about them in the investor concall. This one issue of lack of transparency is dragging this stock down for years as market is unsure about how many more skeletons in the cupboard… ![]()